Quick Navigation

Report Overview

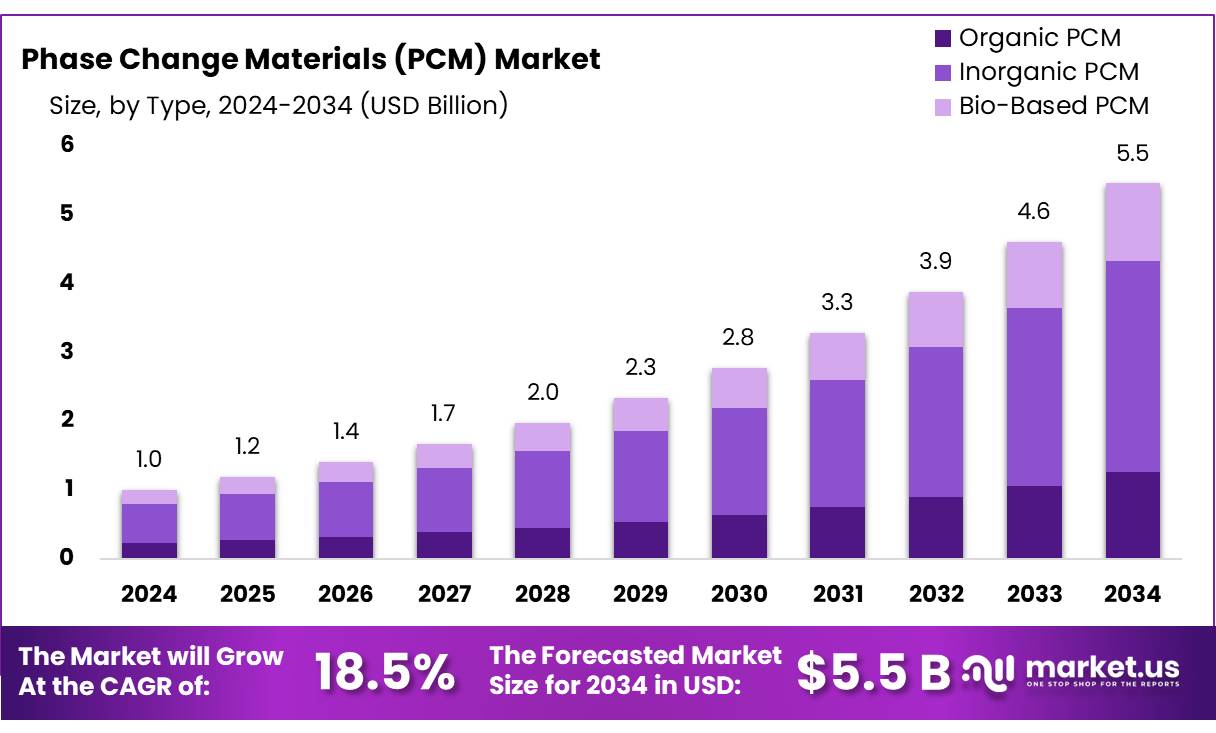

The Global Phase Change Materials (PCM) Market size is expected to be worth around USD 5.5 Billion by 2034, from USD 1.0 Billion in 2024, growing at a CAGR of 18.5% during the forecast period from 2025 to 2034.

Phase Change Materials (PCMs) are pivotal in enhancing energy efficiency across various sectors, including construction, automotive, electronics, and renewable energy. Their unique ability to absorb and release thermal energy during phase transitions enables effective temperature regulation, contributing to reduced energy consumption and improved thermal management.

In the construction industry, PCMs are integrated into building materials such as insulation, wallboards, and roofing to optimize indoor temperature regulation. This integration leads to decreased reliance on heating and cooling systems, thereby reducing energy costs and promoting sustainable building practices. For instance, Germany’s construction sector, the largest in Europe, is actively incorporating PCMs to meet energy efficiency goals. The German government has set a target to build 400,000 new housing units annually, with 100,000 being publicly subsidized, emphasizing affordable and energy-efficient housing solutions.

The automotive sector, particularly the electric vehicle (EV) segment, is witnessing increased adoption of PCMs for thermal management. In 2023, approximately 14 million new electric cars were registered globally, marking a 35% increase from 2022 and bringing the total to 40 million EVs on the road . PCMs play a crucial role in maintaining optimal battery temperatures, thereby enhancing battery life and performance. For example, incorporating paraffin-based PCMs with a melting point around 67°C can improve battery capacity utilization from 60% (with air cooling) to 90%, while also extending battery lifespan.

In the renewable energy sector, PCMs are employed for thermal energy storage, enhancing the efficiency and reliability of solar and wind power systems. According to the International Energy Agency (IEA), solar photovoltaic (PV) generation increased by a record 156 TWh in 2020, representing a 23% growth from 2019 . The integration of PCMs in solar thermal systems and PV panels aids in managing temperature fluctuations, thereby improving overall system performance.

Government initiatives worldwide are fostering the adoption of PCMs. In Europe, the European Union’s “Carbon Credit” initiative incentivizes the use of PCMs in building and HVAC applications by offering 10-20 times more carbon credits compared to other green insulating materials . Germany’s amendment to its Buildings Energy Act (GEG), effective from January 2024, mandates that new heating systems achieve a 65% renewable energy contribution, further promoting PCM integration in building systems.

Key Takeaways

- Phase Change Materials (PCM) Market size is expected to be worth around USD 5.5 Billion by 2034, from USD 1.0 Billion in 2024, growing at a CAGR of 18.5%.

- Inorganic PCM held a dominant market position, capturing more than a 56.3% share.

- Encapsulated Phase Change Materials (PCMs) held a dominant market position, capturing more than a 67.9% share.

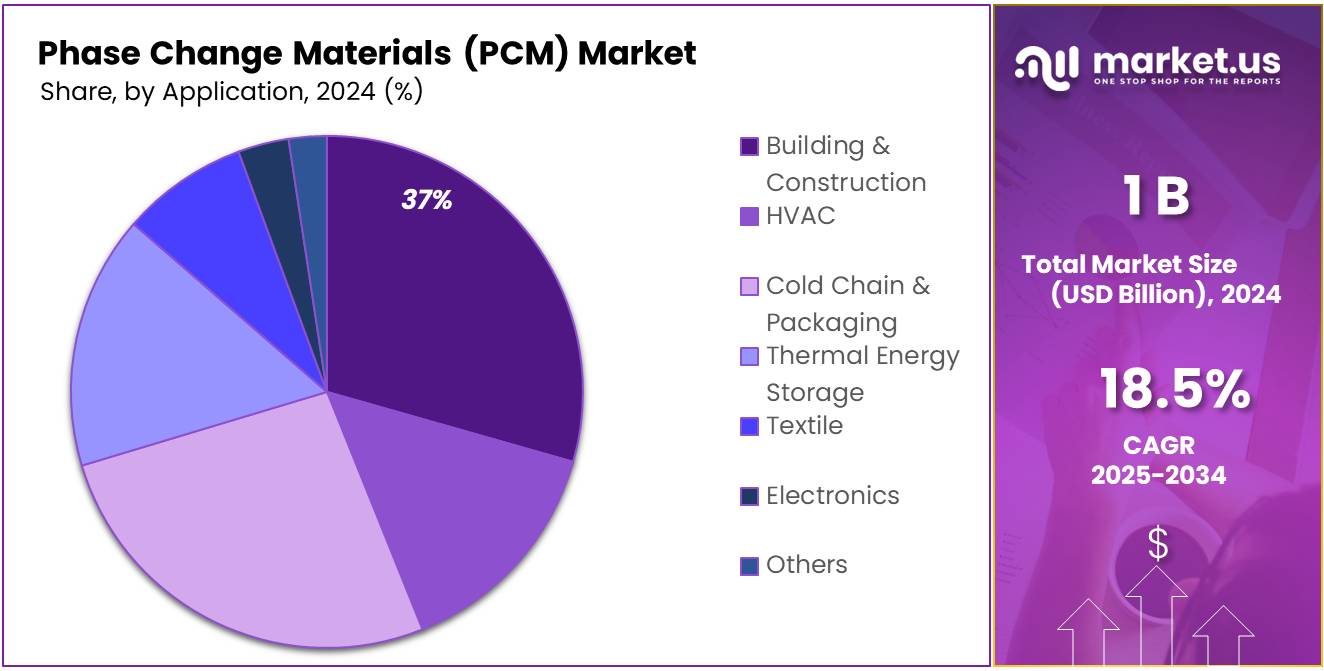

- Building & Construction held a dominant market position, capturing more than a 36.7% share.

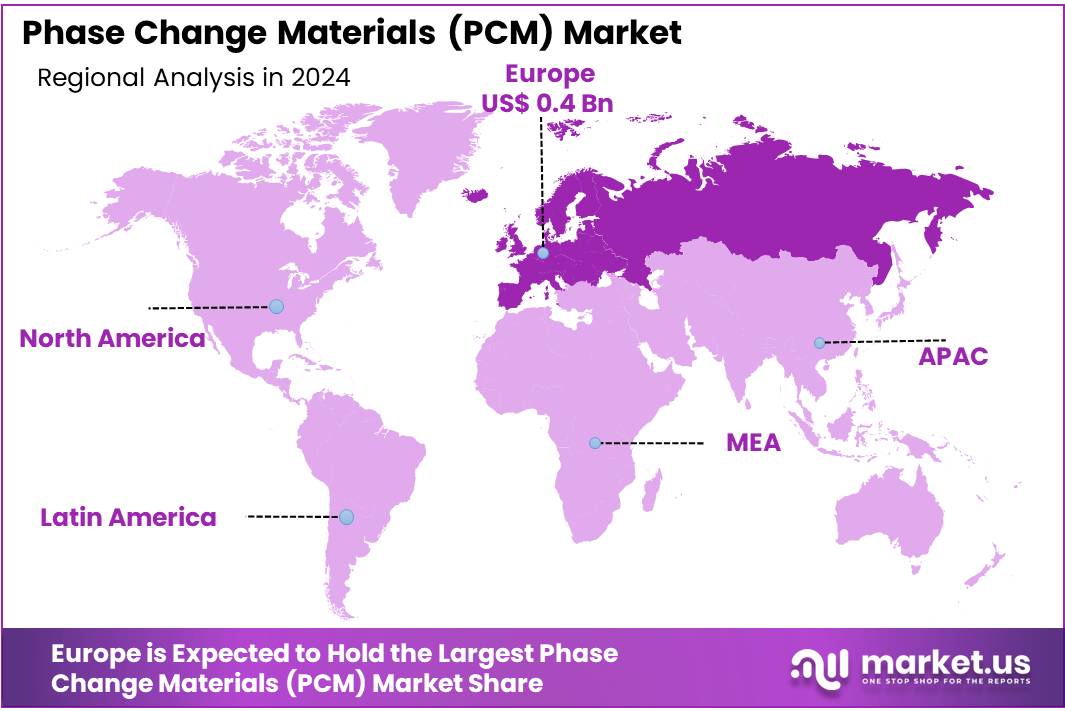

- Europe emerged as the leading region in the Phase Change Materials (PCM) market, holding a dominant share of 43.9%, with the market valued at approximately USD 0.4 billion.

By Type

Inorganic PCM leads with 56.3% in 2024 owing to its high thermal conductivity and stability.

In 2024, Inorganic PCM held a dominant market position, capturing more than a 56.3% share. This strong lead is largely due to the material’s superior thermal conductivity, non-flammability, and ability to handle higher operating temperatures compared to organic alternatives. Inorganic PCMs, such as salt hydrates and metallics, are widely used in building and construction, HVAC systems, and cold chain logistics where consistent and efficient heat storage is essential. Their long-term thermal cycling stability makes them ideal for large-scale industrial applications. As industries continue to seek safer and more efficient energy storage solutions, the use of inorganic PCMs is expected to remain high through 2025, especially in countries focusing on energy conservation and sustainable infrastructure.

By Form

Encapsulated PCMs lead the way with 67.9% share in 2024, thanks to their versatility and clean handling.

In 2024, Encapsulated Phase Change Materials (PCMs) held a dominant market position, capturing more than a 67.9% share. Their popularity stems from their ability to be safely integrated into various systems without the risk of leakage or material degradation. By enclosing the PCM in a protective shell—either micro or macro encapsulation—these materials maintain structural integrity and perform reliably over repeated thermal cycles.

This form is especially favored in industries like textiles, construction, electronics, and refrigeration where cleanliness, precise temperature control, and ease of installation matter. Looking ahead into 2025, the demand for encapsulated PCMs is likely to grow further as more manufacturers focus on compact and efficient thermal energy solutions for both industrial and consumer applications.

By Application

Building & Construction takes the lead with 36.7% share in 2024 driven by the push for energy-efficient buildings.

In 2024, Building & Construction held a dominant market position, capturing more than a 36.7% share in the Phase Change Materials (PCM) market. The segment’s strong performance is closely linked to the rising demand for energy-efficient structures and stricter building codes aimed at reducing energy consumption.

PCMs are being used in wallboards, roofing materials, insulation panels, and floor systems to help regulate indoor temperatures by absorbing excess heat during the day and releasing it at night. This reduces the need for active heating and cooling, cutting energy costs significantly. In 2025, this trend is expected to continue as both residential and commercial developers look for sustainable building solutions that meet green certification standards and contribute to long-term operational savings.

Key Market Segments

By Type

- Organic PCM

- Inorganic PCM

- Bio-Based PCM

By Form

- Encapsulated

- Non-Encapsulated

By Application

- Building & Construction

- HVAC

- Cold Chain & Packaging

- Thermal Energy Storage

- Textile

- Electronics

- Others

Drivers

Rising Demand for Energy-Efficient Cold Chain Solutions Drives PCM Market Growth

One of the major driving factors for the Phase Change Materials (PCM) market is the increasing need for energy-efficient cold chain systems, particularly in the food and pharmaceutical industries. Proper temperature control during storage and transportation is crucial for maintaining the quality and safety of perishable goods. According to the Food and Agriculture Organization of the United Nations (FAO), nearly 14% of the world’s food is lost between harvest and retail, largely due to inadequate temperature management. This has led to a growing focus on advanced cooling technologies, where PCMs play a vital role by providing reliable thermal regulation without excessive energy consumption.

In 2023, the global cold chain logistics market was valued at approximately USD 233 billion, with a projected annual growth rate of over 14% through 2030, reflecting the expanding need for sustainable temperature-controlled solutions. PCMs offer an efficient way to store and release thermal energy, reducing reliance on traditional refrigeration systems that consume large amounts of electricity and contribute to greenhouse gas emissions.

Government initiatives also reinforce this trend. For example, the U.S. Department of Energy promotes energy-saving technologies in food storage and transportation to reduce operational costs and environmental impact. The USDA has actively supported programs to modernize cold storage facilities, encouraging the adoption of PCM-based systems to improve energy efficiency and extend product shelf life. Similarly, the European Union’s Green Deal includes targets to enhance sustainability across the supply chain, pushing industries to implement eco-friendly solutions like PCMs for cold chain logistics.

The adoption of PCMs helps food companies cut energy costs while ensuring temperature-sensitive products such as dairy, meat, and frozen goods remain safe during transit. This balance of sustainability and performance makes PCMs a preferred choice in cold chain management, and it is expected that demand will rise steadily as global food supply chains become more complex and regulated. The role of PCMs in reducing food loss and improving energy efficiency in cold chains is a clear factor fueling the market’s ongoing growth.

Restraints

High Initial Costs and Integration Challenges Limit PCM Market Growth

A major restraining factor for the Phase Change Materials (PCM) market is the relatively high upfront cost and technical challenges involved in integrating PCMs into existing systems, especially in the food cold chain and storage sectors. While PCMs offer energy savings and improved temperature control over time, the initial investment in materials, encapsulation technology, and specialized installation can be a significant barrier for many companies.

According to the Food and Agriculture Organization (FAO), reducing food loss along the cold chain is critical, yet many small and medium-sized enterprises in developing regions struggle to adopt advanced thermal technologies due to budget constraints. For instance, the FAO reports that cold chain infrastructure investments in low- and middle-income countries remain below the levels required to meet global food safety standards, with only about 30% of perishable foods benefiting from controlled temperature conditions during transport and storage.

Government initiatives, while supportive of energy efficiency, sometimes focus more on large-scale industrial applications, leaving smaller players without sufficient financial aid or incentives to adopt PCMs. Although programs like the USDA’s Cold Storage Infrastructure Grant aim to help modernize facilities, the complex requirements for PCM integration—such as compatibility with existing refrigeration units and long-term durability under fluctuating temperatures—can discourage widespread use.

Moreover, PCMs must be carefully selected and engineered for specific applications, as improper use can lead to material degradation or insufficient thermal performance. These technical challenges add to the overall cost and risk, limiting the speed of adoption in the food industry’s cold chain.

Opportunity

Expansion of Sustainable Packaging in Food Industry Offers Growth Opportunities for PCM Market

One of the significant growth opportunities for the Phase Change Materials (PCM) market lies in the rising demand for sustainable and temperature-controlled packaging solutions in the food industry. As consumers become more conscious about food safety and environmental impact, companies are seeking innovative ways to extend product shelf life while reducing carbon footprints. PCMs are increasingly being used in active packaging to maintain optimal temperatures during transportation and storage of perishable foods such as dairy, seafood, fruits, and vegetables.

According to the Food and Agriculture Organization (FAO), food loss in perishable items remains a critical global issue, with nearly 20% of fruits and vegetables and 35% of fish being lost due to inadequate cold chain and packaging solutions. This creates a clear need for technologies that can maintain consistent temperatures without relying heavily on energy-intensive refrigeration methods.

Governments are also supporting this shift towards sustainable food packaging. The European Union’s Circular Economy Action Plan promotes the development and adoption of eco-friendly packaging materials, encouraging innovations such as PCM-based thermal packaging. Likewise, the U.S. Department of Agriculture has funded initiatives aimed at improving cold chain infrastructure with an emphasis on environmentally friendly technologies.

Trends

Integration of Phase Change Materials in Cold Chain Logistics Enhances Sustainability and Efficiency

A significant trend in the Phase Change Materials (PCM) market is their increasing integration into cold chain logistics, particularly within the food industry. This adoption is driven by the need to maintain product quality, reduce spoilage, and enhance energy efficiency during transportation and storage of perishable goods.

Phase Change Materials play a crucial role in this context by providing passive thermal regulation. They absorb and release latent heat during phase transitions, helping to maintain stable temperatures within the desired range without the need for continuous energy input. This capability is particularly valuable in reducing the reliance on energy-intensive refrigeration systems, leading to lower operational costs and a smaller carbon footprint.

Government initiatives are also supporting the adoption of PCMs in cold chain logistics. For instance, the Indian government’s National Centre for Cold-chain Development (NCCD) has been actively promoting the development of cold chain infrastructure, focusing on environmentally friendly technologies and energy efficiency. The NCCD aims to reduce food loss and improve the efficiency of the cold chain, which aligns with the benefits offered by PCMs.

Regional Analysis

Europe Dominates the Phase Change Materials Market with 43.9% Share Valued at USD 0.4 Billion

In 2024, Europe emerged as the leading region in the Phase Change Materials (PCM) market, holding a dominant share of 43.9%, with the market valued at approximately USD 0.4 billion. This leadership is driven by the region’s strong focus on energy efficiency, sustainability, and stringent regulatory frameworks aimed at reducing carbon emissions across multiple sectors, including construction, automotive, and cold chain logistics. European countries have been early adopters of PCM technologies, especially in green building initiatives where PCMs are integrated into insulation materials to reduce energy consumption for heating and cooling.

The European Union’s commitment to achieving climate neutrality by 2050 under the European Green Deal has intensified demand for innovative energy storage and management solutions. Governments across the region have introduced incentives and funding schemes that promote the use of PCMs in new construction projects and retrofits. For example, Germany’s Energy Saving Ordinance (EnEV) mandates strict energy efficiency standards, encouraging developers to adopt materials like PCMs that improve thermal regulation.

Additionally, the growing pharmaceutical and food industries in Europe are increasingly investing in PCM-based cold chain solutions to maintain product quality during transportation, further boosting market growth. The rise in e-commerce and demand for temperature-sensitive products has accelerated the adoption of PCMs in packaging and logistics.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BASF SE is a global chemical giant actively involved in the development and production of advanced Phase Change Materials (PCMs). The company focuses on creating sustainable thermal energy storage solutions for applications in construction, packaging, and industrial processes. BASF’s innovative PCMs offer enhanced energy efficiency and temperature regulation, aligning with global trends toward sustainability. Leveraging strong R&D capabilities and a broad product portfolio, BASF continues to expand its presence in the PCM market, targeting sectors like cold chain logistics and building insulation to meet growing energy-saving demands.

Climator Sweden AB specializes in manufacturing high-performance Phase Change Materials designed primarily for temperature control and thermal management applications. Their PCMs are widely used in the cold chain, healthcare, and transportation sectors to maintain precise temperature conditions. The company emphasizes sustainability and energy efficiency by providing eco-friendly solutions that reduce reliance on traditional cooling methods. Climator Sweden AB leverages innovation and customization to cater to varied industry needs, strengthening its position as a key player in the global PCM market.

Cold Chain Technologies is a leading provider of temperature assurance packaging and Phase Change Materials for the food, pharmaceutical, and biotech industries. Their PCM products are engineered to maintain strict temperature ranges during transport and storage, ensuring product integrity and compliance with regulatory standards. The company invests heavily in R&D to enhance PCM performance, focusing on sustainability and reducing energy consumption. Cold Chain Technologies plays a vital role in advancing cold chain efficiency, addressing challenges related to global logistics and perishable goods preservation.

Top Key Players in the Market

- BASF SE

- Climator Sweden AB

- Cold Chain Technologies

- Croda International Plc

- Cryopak

- Honeywell International Inc.

- Laird Technologies, Inc.

- Outlast Technologies LLC

- PCM Products Ltd

- Pluss Advanced Technologies Pvt. Ltd.

- PURETEMP LLC

- RGEES, LLC.

- Rubitherm Technologies GmbH

- Sasol

Recent Developments

In 2024, CCT continued to innovate with its Koolit® Advanced PCM Gel, a flexible, leak-proof gel pack that provides uniform thermal protection for temperature-sensitive shipments.

In 2024, Climator continued to innovate in the PCM sector, focusing on enhancing the performance and versatility of ClimSel™ to meet the growing demand for energy-efficient and environmentally friendly solutions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 1.0 Bn |

| Forecast Revenue (2034) | USD 5.5 Bn |

| CAGR (2025-2034) | 18.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Organic PCM, Inorganic PCM, Bio-Based PCM), By Form (Encapsulated, Non-Encapsulated), By Application (Building and Construction, HVAC, Cold Chain and Packaging, Thermal Energy Storage, Textile, Electronics, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | BASF SE, Climator Sweden AB, Cold Chain Technologies, Croda International Plc, Cryopak, Honeywell International Inc., Laird Technologies, Inc., Outlast Technologies LLC, PCM Products Ltd, Pluss Advanced Technologies Pvt. Ltd., PURETEMP LLC, RGEES, LLC., Rubitherm Technologies GmbH, Sasol |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |