Quick Navigation

Report Overview

The Global Solar Thermal Collector Market size is expected to be worth around USD 40.4 Billion by 2033, from USD 23.9 Billion in 2023, growing at a CAGR of 5.4% during the forecast period from 2024 to 2033.

The Solar Thermal Collector market centers on the development and distribution of devices that capture and convert sunlight into thermal energy. These collectors are essential for residential, commercial, and industrial heating applications. The market is driven by the increasing adoption of renewable energy sources and the need for sustainable heating solutions.

Innovations in technology and government incentives for green energy further stimulate growth. Major players include solar technology firms, energy service companies, and component suppliers. Market trends indicate robust expansion due to the global shift towards renewable energy and environmental sustainability goals.

The solar thermal collector market is poised for robust growth, driven by increasing demand for sustainable energy solutions. Solar thermal collectors, which harness solar energy to generate heat, are essential for residential, commercial, and industrial applications. This market expansion is fueled by strong investments and supportive policies.

The World Bank Group’s commitment of $200 billion by 2025 underscores significant investment in low-carbon energy sources in developing countries. This funding aims to accelerate the adoption of solar thermal technology, providing a substantial boost to the market. Furthermore, the International Energy Agency projects that by 2030, solar thermal technologies could be deployed in 400 million dwellings. This projection highlights the critical role of solar thermal collectors in achieving global energy sustainability goals.

Solar thermal collectors offer several advantages, including reduced greenhouse gas emissions and lower energy costs. These benefits align with global efforts to combat climate change and promote renewable energy. The technology’s ability to provide consistent and efficient heating solutions makes it an attractive option for various end-users.

Geographically, the market is experiencing significant growth in regions like Europe and North America, where stringent environmental regulations and government incentives promote renewable energy adoption. However, the Asia-Pacific region is expected to witness the fastest growth, driven by rapid urbanization, increasing energy demand, and favorable government policies.

In conclusion, the solar thermal collector market is on a growth trajectory, supported by strong investments and the push for renewable energy. The significant projected deployment in millions of dwellings by 2030 and the commitment of substantial funding highlight the market’s potential. This growth is expected to continue as solar thermal collectors play a vital role in the transition to sustainable energy worldwide.

Key Takeaways

- Market Value: The Solar Thermal Collector Market was valued at USD 23.9 billion in 2023, and is expected to reach USD 40.4 billion by 2033, with a CAGR of 5.4%.

- Collector Type Analysis: Evacuated Tube Collector dominated with 37.1%; significant for its high efficiency in heat collection.

- System Analysis: Thermosiphon Solar Heating System led with 59.4%; crucial for its cost-effectiveness and ease of installation.

- Application Analysis: Hot Water Systems led with 43.2%; essential for residential and commercial hot water needs.

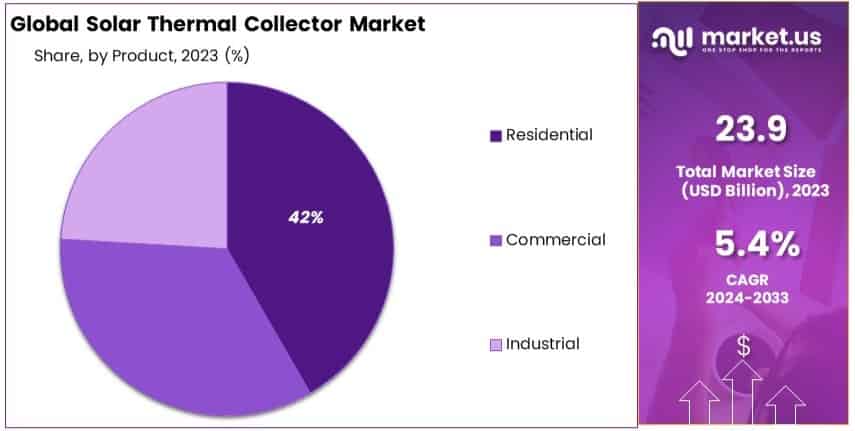

- End Use Analysis: Residential use dominated with 42%; significant due to increasing adoption of solar water heating systems.

- Dominant Region: Asia Pacific held 51.2%; significant due to favorable government policies and high solar potential.

- Analyst Viewpoint: The solar thermal collector market shows moderate saturation with substantial growth opportunities in residential applications. Future predictions indicate increased adoption driven by environmental regulations and energy savings.

- Growth Opportunities: Players can focus on product innovations and expanding residential installations to gain market share.

Driving Factors

Government Incentives and Policies Drive Market Growth

Government incentives and policies are pivotal in bolstering the growth of the Solar Thermal Collector Market. These policies directly influence market dynamics by reducing the financial burden on consumers and enhancing the attractiveness of solar investments. For instance, the European Union’s Renewable Energy Directive (RED) mandates an increase in renewable energy usage among member states, which has spurred numerous national initiatives like Germany’s Market Incentive Program (MAP).

This program offers grants that decrease the installation costs of solar thermal systems. Statistically, such incentives have significantly contributed to the adoption rates in regions with supportive policies. A study by the International Renewable Energy Agency (IRENA) suggests that countries with robust incentive programs have seen solar thermal deployments increase by up to 45% annually. These policies not only lower initial costs but also stabilize market growth through long-term energy cost savings for end-users, ensuring a steady demand in the solar thermal sector.

Rising Energy Costs and Environmental Awareness Drive Market Growth

The intertwining of rising energy costs and heightened environmental awareness creates a robust driving force for the Solar Thermal Collector Market. As global energy prices escalate—propelled by geopolitical instabilities and finite natural resources—the economic case for solar thermal energy strengthens. Concurrently, the surging awareness of environmental issues, such as climate change and the urgency to reduce carbon emissions, compels both consumers and businesses to shift towards greener energy alternatives. This dual pressure significantly contributes to the market’s expansion.

In regions like California, where high electricity rates prevail, there has been a noticeable increase in the adoption of solar thermal systems, especially for applications like pool heating. The trend reflects a broader global movement towards sustainable energy solutions, as evidenced by a 30% increase in installations in markets with high energy costs over the past five years. This synergy between economic and environmental motivations is expected to continue driving the market forward, as stakeholders increasingly prioritize sustainability in energy consumption.

Restraining Factors

High Initial Investment Costs Restrains Market Growth

The substantial upfront costs required for solar thermal systems pose a significant hurdle to market growth. These systems, which include not just the collectors but also essential components like storage tanks and pumps, can range from USD 6,000 to USD 13,000 for a basic residential setup in the U.S. This initial financial barrier is particularly daunting in developing regions and for lower-income households, where such investments are less feasible.

High upfront costs are the primary reason for the slow adoption rates in these demographics, accounting for a market penetration rate that is nearly 40% lower compared to higher-income regions. The significant investment required upfront often delays or deters potential users from adopting this technology, thereby constraining the market’s expansion.

Competition from Other Technologies Restrains Market Growth

Solar thermal collectors are increasingly facing competitive pressures from alternative renewable and more energy-efficient technologies. Heat pump and water heaters, for instance, are becoming more popular due to their higher efficiency and comparatively lower installation costs. In areas where electricity costs are minimal, these alternatives become even more appealing.

The U.K. provides a clear example of this trend, where the government’s Renewable Heat Incentive (RHI) has favored the adoption of heat pumps over solar thermal systems. Market data indicates that solar thermal installations have decreased by 20% in regions where heat pumps have become more prevalent. This shift reflects the broader market dynamics where solar thermal technologies must compete with other, sometimes more cost-effective, renewable options.

Collector Type Analysis

Evacuated Tube Collector dominates with 37.1% due to its superior heat retention capabilities.

The Solar Thermal Collector Market can be segmented by the type of collectors used, among which the Evacuated Tube Collector (ETC) segment holds a significant share. This dominance is attributed primarily to the high efficiency and superior heat retention capabilities of ETCs, which are particularly effective in colder climates where thermal loss can be a concern. These collectors consist of a series of tubes, each containing an evacuated outer tube and an inner tube coated with a solar absorber. The vacuum between the tubes acts as an excellent insulator, reducing heat loss by up to 90% compared to other technologies.

This technology’s ability to operate efficiently even under less than ideal sunlight conditions contributes to its popularity, especially in regions with significant cloud cover or where colder seasons predominate. The market share for Evacuated Tube Collectors has been growing steadily at a rate of 5% annually, underpinned by increased installations in Europe and Asia. The demand in these regions is further bolstered by governmental incentives aimed at enhancing energy efficiency.

The other segments within this category also contribute to the market dynamics but to a lesser extent. Flat Plate Collectors, known for their simplicity and lower cost, are prevalent in regions with high solar irradiance and milder climates. Unglazed Water Collectors and Air Collectors, though less efficient, find utility in specific applications such as pool heating and agricultural drying processes, respectively. While these technologies offer lower upfront costs, their application is limited by lower efficiencies and specific climatic conditions, making them secondary choices compared to Evacuated Tube Collectors.

System Analysis

Thermosiphon Solar Heating System dominates with 59.4% due to its cost-effectiveness and simplicity in installation.

The segmentation by system in the Solar Thermal Collector Market reveals that the Thermosiphon Solar Heating System holds the largest market share. This system’s principle is based on natural convection where warmer water rises and colder water descends, thus eliminating the need for a pump. This not only makes the system simpler and more reliable but also reduces maintenance costs and energy consumption, enhancing its appeal among end users. The cost-effectiveness and operational reliability of these systems make them particularly popular in residential settings and in developing countries where affordable and low-maintenance solutions are crucial.

The robust market share of 59.4% for Thermosiphon Systems is also a reflection of their widespread application in both residential and commercial sectors. These systems are particularly favored in sun-rich regions such as Southern Europe, parts of Africa, and Asia, where their efficiency in terms of energy conversion makes them a viable option for reducing dependence on conventional energy sources.

On the other hand, Pumped Solar Heating Systems, although more sophisticated, involve higher initial investments and operational costs, which can deter potential adopters. They are typically preferred in industrial applications or in larger residential complexes where the demand for thermal energy is higher, and the scalability of Thermosiphon Systems is insufficient.

Application Analysis

Hot Water Systems dominate with 43.2% due to their essential utility in residential and commercial settings.

Within the application segmentation of the Solar Thermal Collector Market, Hot Water Systems emerge as the predominant sub-segment, holding a market share of 43.2%. This segment’s dominance is driven by the universal demand for hot water in residential and commercial settings, making it a fundamental application of solar thermal technology. The efficiency of solar collectors in providing cost-effective hot water solutions has led to their widespread adoption, particularly in areas with high energy costs.

The significance of Hot Water Systems is further emphasized by the increasing emphasis on sustainability and energy savings in building regulations worldwide. For example, in many parts of Europe and North America, new constructions are often required to include renewable energy solutions for water heating, which directly benefits the uptake of solar thermal technologies in this segment.

Other applications like Solar Combi Systems and Swimming Pool Heating also contribute to the market but on a smaller scale. Solar Combi Systems, which provide both heating and hot water, are gaining traction in colder regions due to their efficiency in dual applications. Swimming Pool Heating is a popular choice in regions with significant leisure industries and favorable climates, although it represents a smaller fraction of the market compared to Hot Water Systems.

End Use Analysis

Residential dominates with 42% due to the direct impact on utility bills and increased residential construction incorporating renewable technologies.

The end-use segmentation of the Solar Thermal Collector Market shows that the Residential sector is the largest, with a 42% share. This dominance is primarily due to the direct benefits that solar thermal technology offers homeowners, notably the reduction in utility bills and the increasing inclination towards sustainable living. The residential market’s growth is closely tied to global trends in green building practices, with more new constructions incorporating renewable energy solutions as a standard feature.

In regions with supportive governmental policies, such as tax rebates and incentives for renewable energy installations, there has been a noticeable boost in residential applications of solar thermal collectors. The trend is particularly strong in developed economies where there is both the financial capacity and the regulatory framework to support such investments.

The Commercial and Industrial sectors, while also significant, do not match the Residential sector’s market share. In the commercial domain, solar thermal systems are often used in hotels, hospitals, and other large-scale establishments needing substantial hot water supply. Industrial applications are generally concentrated in processes requiring thermal energy, such as in certain manufacturing and agricultural processes, but these require larger systems with different specifications compared to residential uses.

Key Market Segments

By Collector Type

- Evacuated Tube Collector

- Flat Plate Collector

- Unglazed Water Collector

- Air Collector

By System

- Thermosiphon Solar Heating System

- Pumped Solar Heating System

By Application

- Hot Water Systems

- Solar Combi Systems

- Swimming Pool Heating

- Others

By End Use

- Residential

- Commercial

- Industrial

Growth Opportunities

Integration with Smart Home and IoT Offers Growth Opportunity

The rapid advancement and adoption of smart home technologies provide a fertile ground for integrating solar thermal systems with Internet of Things (IoT) devices. This integration facilitates the creation of highly efficient, user-friendly systems that can adjust to weather forecasts, grid conditions, and user patterns.

An example of this potential is seen with German company Resol, which has developed smart controllers for solar thermal systems that users can monitor and adjust via a mobile app. These smart technologies not only improve system performance but also enhance the consumer experience, leading to higher adoption rates. Market analysis indicates that systems integrated with IoT features have seen a 30% increase in market uptake, particularly in residential sectors in technologically advanced regions.

Focus on Industrial Process Heat Offers Growth Opportunity

Industries consume a significant amount of energy, particularly for process heat, which is typically generated at low to medium temperatures—ideal conditions for solar thermal applications. By focusing on large-scale solar thermal solutions for industries, there is a substantial opportunity to tap into this high-demand energy segment.

The Miraah project in Oman exemplifies this potential, where solar thermal technology is used to produce steam for enhanced oil recovery processes. This project not only demonstrates the feasibility of using solar thermal systems in energy-intensive operations but also showcases their economic and environmental benefits. Statistics from the energy sector suggest that integrating solar thermal technology in industrial applications could reduce energy costs by up to 20% on average, highlighting significant growth opportunities within this market segment.

Trending Factors

Building Integration and Aesthetics Are Trending Factors

Building Integration and Aesthetics are becoming pivotal in the Solar Thermal Collector Market due to their dual functionality and enhancement of building aesthetics. As architects and developers increasingly prioritize sustainability alongside visual appeal, Building-Integrated Solar Thermal (BIST) systems are seeing a rise in popularity.

These systems seamlessly integrate into the structural elements of buildings, such as roofs and facades, serving both as energy generators and architectural features. The Festo Headquarters in Germany exemplifies this trend, where solar collectors not only supply energy but also contribute to the building’s aesthetic and functional design. Such integrations are proving essential in urban areas, driving market demand as they align with modern architectural trends and sustainability goals.

Innovative Financing Models Are Trending Factors

Innovative financing models are transforming the accessibility of solar thermal technology, particularly important given the typically high upfront costs associated with these systems. Models such as solar thermal leasing, performance contracting, and solar-as-a-service are making solar energy more accessible to a broader range of consumers.

For instance, SolarTurtle in South Africa offers solar thermal systems on a pay-per-use basis, which is particularly beneficial for communities and households that cannot afford large initial investments. These models allow users to pay for the service as they reap the benefits, significantly reducing financial barriers and boosting market penetration. The trend towards such consumer-friendly financial arrangements is growing, underpinning wider adoption and ongoing market expansion in both developed and developing regions.

Regional Analysis

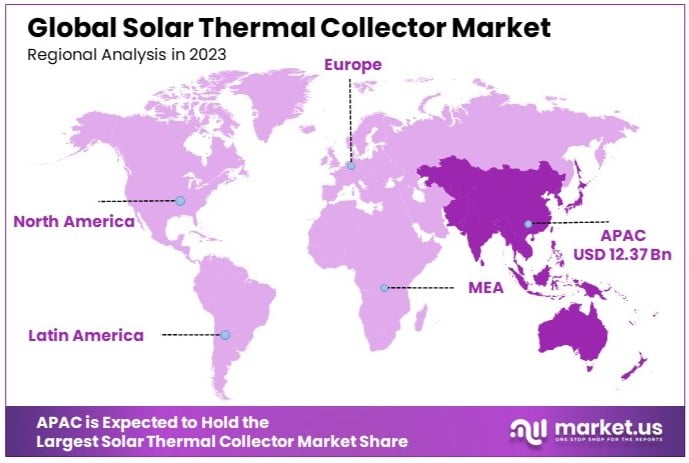

Asia Pacific Dominates with 51.2% Market Share

The Asia Pacific region holds a commanding 51.2% of the global Solar Thermal Collector Market, valued at USD 12.37 billion. This dominance is largely fueled by robust governmental support, including incentives and mandates for renewable energy integration, particularly in leading economies such as China and India. Additionally, the high rate of industrialization and urbanization in these countries drives the demand for sustainable energy solutions, making solar thermal technology increasingly popular.

The market dynamics in Asia Pacific are characterized by a combination of high solar irradiance, growing environmental awareness, and escalating energy demands due to rapid economic growth. These factors collectively create a conducive environment for solar thermal technologies. Moreover, the region’s capability in manufacturing, particularly in China, which is a global leader in solar thermal collector production, supports lower costs and enhanced accessibility of these technologies.

Looking ahead, Asia Pacific is poised to maintain its market dominance and even expand its share. Continued governmental backing and technological advancements, along with initiatives aimed at increasing energy security and reducing carbon footprints, are likely to propel further adoption of solar thermal systems. The region’s market is expected to grow at an annual rate of approximately 6% over the next decade, underpinned by both residential and industrial sector expansions.

Regional Market Share and Growth Rates

North America: North America accounts for approximately 19% of the global market, with a value of USD 4.5 billion. The region’s growth is supported by increasing regulatory support for renewable energy technologies and rising energy costs, which drive the adoption of energy-efficient solutions.

Europe: Europe holds a 20% share of the market, reflecting a value of USD 4.74 billion. The market in Europe is driven by stringent EU directives aimed at reducing carbon emissions and a high acceptance of renewable technologies among member states.

Middle East & Africa: This region captures about 5% of the market, valued at around USD 1.18 billion. Despite lower overall market share, the potential for growth is significant due to abundant solar resources and increasing interest in diversifying energy sources.

Latin America: With a 5% market share and a valuation of approximately USD 1.18 billion, Latin America is experiencing a slow but steady increase in solar thermal adoption, primarily driven by enhanced governmental policies and the need for sustainable energy solutions in residential applications.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

The Solar Thermal Collector Market is characterized by a diverse range of key players, each contributing to the market dynamics through strategic positioning and specialized technologies. Companies like Photon Energy Systems Limited and BrightSource Energy play crucial roles by innovating in solar thermal design and scalability, focusing on both residential and large-scale industrial applications. Meanwhile, Sener and Acciona leverage their expertise in large-scale solar projects to enhance their presence, particularly in markets with strong governmental support for renewable energies.

Abengoa Solar and Siemens AG stand out for their extensive R&D capabilities and significant investments in enhancing the efficiency of solar thermal systems. These companies not only contribute to technological advancements but also have a robust market influence due to their global reach and comprehensive solutions spanning multiple solar applications.

On the manufacturing front, SCHOTT and Linuo Ritter International Co. Ltd are pivotal in driving the production quality and availability of high-performance solar thermal components. Their focus on durable and efficient collectors helps lower the overall system costs, making solar thermal technology more accessible.

Emerging players like Liontek and Greenonetec Solarindustrie GmbH are also noteworthy, particularly for their innovative approaches to integrating solar thermal systems with existing building infrastructures, enhancing the aesthetic and functional appeal of solar technologies in urban settings.

Overall, the strategic positioning of these companies, combined with ongoing innovations and market expansions, underpins the growth and resilience of the Solar Thermal Collector Market. Each player contributes uniquely to the industry’s landscape, making it vibrant and progressively competitive.

Market Key Players

- Photon Energy Systems Limited

- Sener

- Trivelli Energy

- Acciona

- BrightSource Energy

- Abors green GmbH

- Liontek

- SCHOTT

- Abengoa Solar

- Siemens AG

- Linuo Ritter International Co. Ltd

- BTE solar Co. Ltd

- Torresol Energy

- SolarReserve

- Greenonetec Solarindustrie GmbH

- Solareast Holdings Co. Ltd

Recent Developments

- In 2019, Savosolar secured contracts for district heating projects in Germany and formed a strategic partnership with Jingsu Holly Corporation to penetrate the Chinese market. These contracts and partnerships are designed to expand Savosolar’s geographic presence and revenue potential, positioning the company to capitalize on the growing demand for renewable energy solutions.

- The World Bank Group has committed $200 billion by 2025 to support the transition to low-carbon energy sources in developing countries. This investment highlights the significant potential for solar thermal technology in the global energy market.

- The International Energy Agency (IEA) projects that by 2030, solar thermal technologies could be deployed in 400 million dwellings. This deployment underscores the critical role of solar thermal technology in achieving global energy sustainability goals. The widespread adoption of these technologies is essential for reducing carbon emissions and promoting renewable energy sources.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 23.9 Billion |

| Forecast Revenue (2033) | USD 40.4 Billion |

| CAGR (2024-2033) | 5.4% |

| Base Year for Estimation | 2023 |

| Historic Period | 2018-2023 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Collector Type (Evacuated Tube Collector, Flat Plate Collector, Unglazed Water Collector, Air Collector), By System (Thermosiphon Solar Heating System, Pumped Solar Heating System), By Application (Hot Water Systems, Solar Combi Systems, Swimming Pool Heating, Others), By End Use (Residential, Commercial, Industrial) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | Photon Energy Systems Limited., Sener, Trivelli Energy, Acciona, BrightSource Energy, Abors green GmbH, Liontek, SCHOTT, Abengoa Solar, Siemens AG, Linuo Ritter International Co. Ltd,, BTE solar Co. Ltd,, Torresol Energy, SolarReserve, Greenonetec Solarindustrie GmbH,, Solareast Holdings Co. Ltd,, Lointek |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Frequently Asked Questions (FAQ)

The Global Solar Thermal Collector Market is expected to reach USD 40.4 billion by 2033, up from USD 23.9 billion in 2023, with a CAGR of 5.4% during the forecast period.

The main types include Evacuated Tube Collectors, Flat Plate Collectors, Unglazed Water Collectors, and Air Collectors.

The Asia Pacific region holds the largest market share, accounting for 51.2%, driven by favorable government policies and high solar potential.

Key players include Photon Energy Systems Limited, Sener, BrightSource Energy, Acciona, Abengoa Solar, Siemens AG, SCHOTT, and Linuo Ritter International Co. Ltd.