Quick Navigation

Report Overview

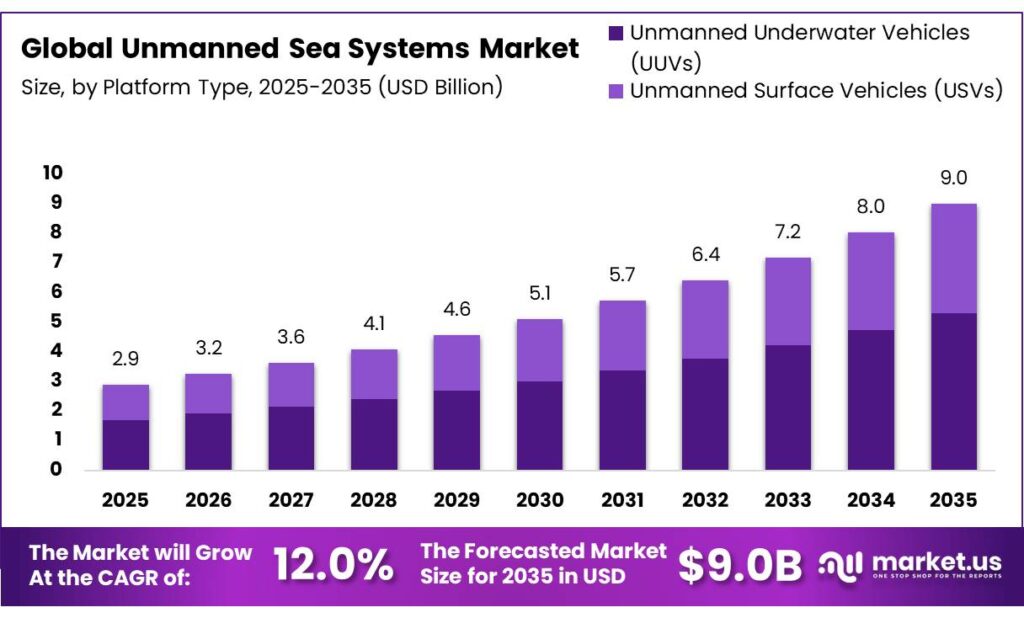

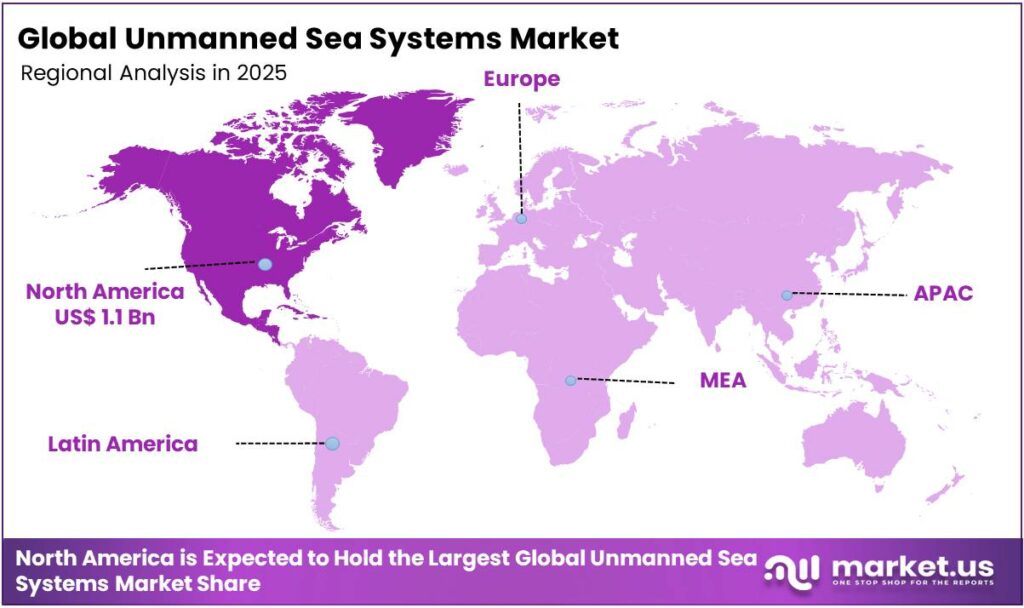

The Global Unmanned Sea Systems Market size is expected to be worth around USD 9.0 Billion by 2035, from USD 2.9 Billion in 2025, growing at a CAGR of 12.0% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 37.9% share, holding USD 1.1 Billion revenue.

Unmanned sea systems (USS), often referred to as unmanned maritime systems (UMS), are vehicles that operate on or below the surface of the water without a human crew on board. The unmanned sea systems market is characterized by diverse platform types, operational domains, and mission profiles, with adoption driven by both commercial and defense imperatives. North America leads regional deployment, reflecting concentrated defense programs, high UUV utilization, and institutional adoption by agencies such as the U.S. Navy and NOAA.

Small and UUV platforms dominate due to their flexibility, access to shallow and confined areas, extended operational endurance, and stealth capabilities, while diesel and gas-turbine propulsion enables long-duration and high-speed missions. Commercial applications, such as offshore inspection, infrastructure maintenance, and seabed mapping, account for the majority of operational use, leveraging repetitive, predictable, and high-precision tasks.

Defense applications, while mission-critical, remain more selective and specialized, including surveillance, mine countermeasures, and tactical strikes, with deployments influenced by geopolitical tensions. Operational trends emphasize autonomy, modular payloads, interoperability, and data integration, while challenges include power constraints, regulatory non-standardization, and endurance limitations. The unmanned sea systems increasingly serve as integral tools across scientific, commercial, and military maritime operations.

Key Takeaways

- The global unmanned sea systems market was valued at USD 2.9 billion in 2025.

- The global unmanned sea systems market is projected to grow at a CAGR of 9.0% and is estimated to reach USD 9.0 billion by 2035.

- On the basis of platform type, unmanned underwater vehicles (UUVs) dominated the market, constituting 58.8% of the total market share.

- Based on the vehicle size, small vehicles dominated the unmanned sea systems market, with a substantial market share of around 47.9%.

- Based on the propulsion, the diesel and gas-turbine systems led the market, comprising 41.5% of the total market.

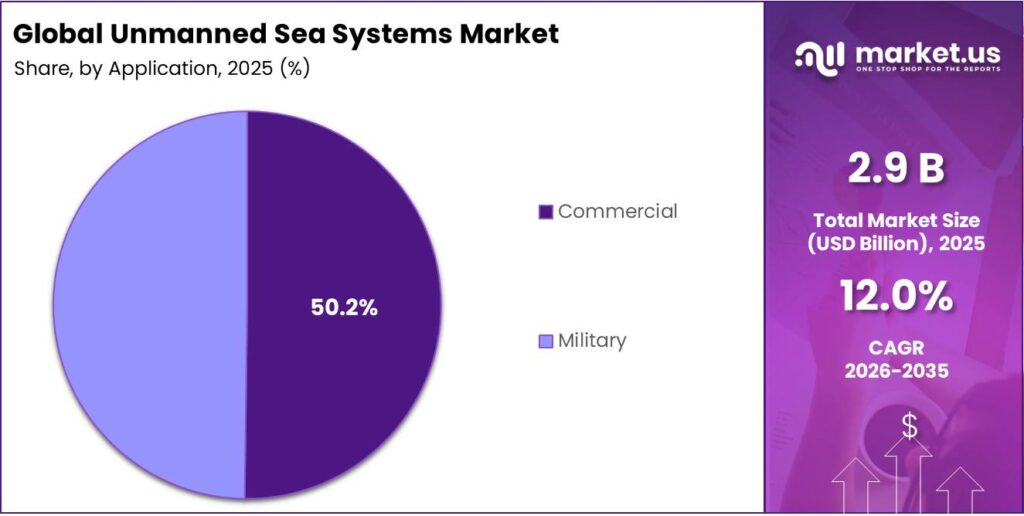

- Among the applications, commercial applications held a major share in the unmanned sea systems market, 50.2% of the market share.

- In 2025, North America was the most dominant region in the unmanned sea systems market, accounting for 37.9% of the total global consumption.

Platform Type Analysis

Unmanned Underwater Vehicles (UUVs) are a Prominent Segment in the Market.

The unmanned sea systems market is segmented based on platform types into unmanned underwater vehicles (UUVs) and unmanned surface vehicles (USVs). The unmanned underwater vehicles (UUVs) led the market, comprising 58.8% of the market share, due to mission necessity, operational stealth, and environmental access. UUVs operate in the subsurface domain, which is critical for mine countermeasures, anti-submarine warfare, seabed mapping, and pipeline inspection, tasks that cannot be performed from the surface with comparable precision. Their ability to function at depth enables direct interaction with underwater infrastructure and terrain. They offer low observability, as underwater operations reduce detection by radar and visual systems, making them suitable for sensitive defense and surveillance missions.

Additionally, UUVs can operate in high sea states and harsh weather with less impact than surface platforms, improving mission continuity. In contrast, USVs are constrained to surface-level tasks such as patrol and monitoring, limiting their applicability. The broader range of critical underwater use cases drives higher utilization of UUVs.

Vehicle Size Analysis

Small Unmanned Sea Systems Dominated the Market.

On the basis of the vehicle size, the unmanned sea systems market is segmented into small, medium, and large. The small unmanned sea systems dominated the market, comprising 47.9% of the market share, due to their operational flexibility, ease of deployment, and lower logistical burden. They can be rapidly deployed from small vessels, shorelines, or even by a few personnel, avoiding the need for the dedicated launch-and-recovery infrastructure required by larger platforms.

Their compact size enables access to shallow waters, confined spaces, and complex subsea environments such as ports, pipelines, and offshore installations, where medium or large-sized systems face maneuverability constraints. Small systems support distributed and swarm-based operations, allowing multiple units to be deployed simultaneously for coverage, redundancy, and mission resilience.

This is particularly relevant for tasks such as mine detection and environmental monitoring. Additionally, they typically require simpler maintenance, lower power systems, and shorter training cycles, facilitating broader adoption across defense, research, and commercial users compared to more complex medium and large platforms.

Propulsion Analysis

Diesel and Gas-Turbine Vehicles Are Most Utilized as Unmanned Sea Systems.

Based on the propulsion, the unmanned sea systems market is divided into electric, hybrid, diesel, gas-turbine, and renewable (solar/wave). The diesel and gas-turbine vehicles dominated the unmanned sea systems market, with a notable market share of 41.5%, due to their high energy density, endurance, and sustained power output, which are critical for extended missions and high-speed operations.

These propulsion systems enable platforms to operate continuously, supporting long-range patrol, surveillance, or military strike missions that electric or hybrid systems, constrained by battery capacity, cannot sustain. Gas-turbine and diesel engines further provide consistent performance under varying sea conditions, including rough weather and strong currents, whereas solar- or wave-powered systems are limited by environmental variability.

Additionally, these conventional engines allow rapid refueling and predictable logistics, facilitating immediate redeployment. In contrast, electric, hybrid, or renewable-powered systems excel in quiet or short-duration tasks but remain constrained in endurance, speed, and payload energy supply, limiting their applicability across diverse naval and offshore operations.

Application Analysis

Commercial Applications Held a Major Share of the Unmanned Sea Systems Market.

Among the applications, 50.2% of the total global consumption of unmanned sea systems is in commercial applications, due to the scale, frequency, and predictability of operational tasks in industries such as offshore energy, subsea infrastructure, and oceanographic research.

Commercial missions, such as pipeline inspection, seabed mapping, environmental monitoring, and port security, require repetitive, high-precision, and long-duration operations that can be efficiently performed by unmanned platforms without human intervention. These applications tolerate lower operational risk and benefit from continuous data collection, making the cost and maintenance profile of unmanned systems favorable.

In contrast, military use often demands high-endurance, survivable platforms with stealth, weapon integration, or rapid redeployment, which increases technical complexity and operational risk. Consequently, commercial sectors exploit unmanned sea systems for persistent, structured tasks where automation delivers measurable efficiency and safety gains, whereas military applications remain more selective and mission-specific.

Key Market Segments

By Platform Type

- Unmanned Underwater Vehicles (UUVs)

- Remotely Operated Vehicles (ROVs)

- Autonomous Underwater Vehicles (AUVs)

- Unmanned Surface Vehicles (USVs)

- Autonomous Surface Vehicles (ASVs)

- Remotely Operated Surface Vehicles (ROSVs)

By Vehicle Size

- Small

- Medium

- Large

By Propulsion

- Electric

- Hybrid

- Diesel and Gas-Turbine

- Renewable (Solar/Wave)

By Application

- Military

- Intelligence, Surveillance, and Reconnaissance (ISR)

- Mine Counter-Measures (MCM)

- Anti-Submarine Warfare (ASW)

- Logistics and Resupply

- Commercial

- Environment Monitoring

- Infrastructure Inspection

- Hydrographic Survey

- Others

Drivers

Defense & Surveillance Drives the Unmanned Sea Systems Market.

The utilization of Unmanned Sea Systems (USS) for defense and surveillance is primarily driven by the requirement for persistent maritime domain awareness (MDA) and the mitigation of personnel risk in high-threat environments. The unmanned undersea vehicles were explicitly prioritized for surveillance, intelligence collection, and tactical oceanography as early as U.S. Navy planning directives, demonstrating long-standing institutional demand for persistent maritime awareness.

Government entities are significantly reallocating resources toward unmanned capabilities. For instance, the U.S. Department of Defense programmed over US$2.6 billion for unmanned aircraft systems in 2023, encompassing 29 dedicated procurement programs. The U.S. Congressional Research Service analysis notes that unmanned vehicles are suited for dull, dirty, or dangerous missions, enabling extended-duration surveillance without risking personnel, while supporting sensor payloads and autonomous operations.

Defense forces prioritize these systems to enhance combat accuracy and conduct intelligence, surveillance, and reconnaissance (ISR) missions while reducing soldier casualties. Naval forces deploy USS for specialized tasks, including mine countermeasures, anti-submarine warfare (ASW), and continuous underwater patrolling. These defense imperatives, risk reduction, persistent ISR coverage, and expanded operational reach, anchor sustained deployment of unmanned maritime systems.

Restraints

Non-Standardization of Regulations Might Pose a Challenge to the Unmanned Sea Systems Market.

The adoption of Unmanned Sea Systems (USS) faces significant structural impediments centered on regulatory fragmentation and energy density limitations. These factors collectively constrain operational autonomy and cross-border deployment. The absence of a unified international legal framework creates regulatory gaps, particularly under the United Nations Convention on the Law of the Sea (UNCLOS), which lacks a direct normative framework for unmanned vehicles.

Autonomous underwater vehicles (AUVs) remain outside ongoing efforts led by international bodies to regulate autonomous ships, creating classification uncertainty under the United Nations Convention on the Law of the Sea (UNCLOS). The absence of consensus on whether AUVs qualify as ships implies that, in some cases, they may lack defined navigational rights or obligations under maritime safety conventions.

Furthermore, UNCLOS does not explicitly differentiate between remotely operated and autonomous systems, reinforcing interpretive inconsistency across national regimes. Operationally, this ambiguity extends to surveillance use, where issues such as territorial sovereignty and admissibility of unmanned-collected data remain unresolved.

Opportunities

Deep-Sea Exploration & Mapping Creates Opportunities in the Unmanned Sea Systems Market.

Deep-sea exploration and mapping represent a primary growth vector for Unmanned Sea Systems (USS), driven by international mandates to close critical data gaps in the global seafloor record. As of 2017, only 6% of the ocean floor was mapped to modern standards, and by 2024, this figure reached 26.1%, largely through the deployment of autonomous technologies.

The National Oceanic and Atmospheric Administration (NOAA) indicates that about 23% of the global seafloor has been mapped in high resolution, leaving the majority of ocean bathymetry unresolved. Complementary NOAA program documentation notes that mapping below 200 meters depth relies increasingly on remotely operated and autonomous underwater systems, reflecting their centrality in deep-ocean data acquisition.

Advanced autonomous underwater vehicles (AUVs) have demonstrated extreme-depth reliability. The Vityaz-D (Russia) successfully conducted a three-hour mission at 10,028 meters in the Mariana Trench. Institutional programs such as the Seabed 2030 Project, a collaborative project between the Nippon Foundation and GEBCO, aim for complete high-resolution mapping by 2030, implying sustained deployment demand for unmanned systems.

Trends

Rising Applications in the Offshore Industry.

The offshore industry increasingly adopts unmanned sea systems (USS) to enhance operational safety and efficiency in inspecting and maintaining critical underwater infrastructure, such as oil and gas platforms, pipelines, and offshore wind turbines. These systems enable continuous inspection of degradation processes such as corrosion and fatigue in underwater infrastructure, which are otherwise difficult to monitor manually.

Utilizing unmanned systems for offshore wind farm inspections can reduce costs by up to 70% compared to traditional rope-access methods. Additionally, the deployment of these systems reduces revenue loss from infrastructure downtime by up to 90%. Similarly, autonomous and remotely operated vehicles (ROVs) mitigate risks by eliminating the need for human divers in hazardous high-pressure environments.

Unmanned underwater vehicles (UUVs) are critical for structural health monitoring (SHM), performing path planning and asset tracking to detect damage on subsea cables and hydroelectric dams. Strategic partnerships, such as the memorandum of understanding between Japan’s MODEC and Terra Drone Corporation, focus on enhancing drone capabilities for inspecting Floating Production Storage and Offloading (FPSO) units. The inspection workload, infrastructure aging, and safety constraints institutionalize unmanned systems as integral to offshore operations.

Geopolitical Impact Analysis

Increased Trade of Unmanned Sea Systems Amid Geopolitical Tensions.

The geopolitical tensions are materially accelerating the deployment and operational validation of unmanned sea systems, with conflict-driven evidence demonstrating both capability scaling and doctrinal shifts. Ukrainian-developed maritime drones, such as the Magura V5 and Sea Baby, had hit 17 and destroyed 15 Russian naval and air targets over two years. These systems, costing approximately US$300,000 per unit, have disabled vessels worth tens of millions of dollars. By mid-2023, such deployments contributed to forcing elements of the Russian Black Sea Fleet into a defensive posture, illustrating a strategic impact disproportionate to platform size.

In 2026, U.S. unmanned surface vessels logged more than 450 operational hours and over 2,200 nautical miles during patrol missions in the Middle East, indicating sustained endurance deployment under real-world conditions. Institutionally, geopolitical competition is driving structural adoption. NATO-linked exercises such as REPMUS, described as the largest unmanned maritime systems exercise globally, focus on interoperability and multi-domain integration among allied forces.

The battlefield effectiveness, endurance metrics, and institutional restructuring indicate that geopolitical tensions are not only accelerating adoption but also embedding unmanned maritime systems into core naval strategy and force design.

Regional Analysis

North America Held the Largest Share of the Global Unmanned Sea Systems Market.

In 2025, North America dominated the global unmanned sea systems market, holding about 37.9% of the total global consumption, anchored by the defense deployment, institutional investment, and technological leadership. The U.S. Department of Defense (DoD) serves as the primary institutional anchor, programming billions for unmanned integration. For instance, the FY2023 budget allocated over US$2.6 billion for unmanned aircraft, which serves as a cross-domain technological precursor for maritime autonomous systems.

The U.S. Navy is actively expanding unmanned fleets across surface and subsurface domains, integrated into broader fleet architecture and mission planning. These systems are designed for long-endurance missions and high-risk operations, reinforcing operational reliance on autonomy.

The National Oceanic and Atmospheric Administration (NOAA) deploys UUVs for oceanographic mapping and data collection, expanding non-defense applications alongside military use. High defense concentration, majority regional share metrics, and dual-use institutional deployment establish North America as the principal center of unmanned maritime system development and utilization.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of unmanned sea systems focus on capability differentiation, operational integration, and lifecycle support to strengthen competitive positioning. A primary activity is advanced autonomy and AI integration, enabling navigation, obstacle avoidance, and mission execution with minimal human intervention. Firms further prioritize modular, payload-agnostic designs, allowing rapid reconfiguration for missions such as mine countermeasures, seabed mapping, or infrastructure inspection. Strategic collaboration with naval agencies and public institutions is central, with manufacturers participating in government-led trials and exercises to validate performance under real-world conditions. In parallel, companies invest in endurance improvements, including hybrid propulsion and energy-efficient systems, to extend mission duration.

Another focus area is interoperability, ensuring compatibility with existing naval platforms and command systems. Similarly, manufacturers emphasize data capabilities, including secure transmission, real-time analytics, and integration with broader maritime surveillance networks, enhancing operational value beyond the platform itself.

The Major Players in The Industry

- TKMS GmbH

- BAE Systems plc

- General Dynamics Corporation

- Lockheed Martin Corporation

- Unique Group

- Teledyne Technologies Incorporated

- Saab AB

- L3Harris Technologies, Inc.

- Maritime Robotics AS

- The Boeing Company

- Exail Technologies SA

- Elbit Systems Ltd.

- SAILDRONE, Inc.

- EDGE Group PJSC

- SeaRobotics Corporation

- Ocean Aero

- Textron Inc.

- Sea Machines Robotics, Inc.

- Thales Group

- Kongsberg Gruppen ASA

- Other Key Players

Key Development

- In February 2026, TKMS and Israel Aerospace Industries (IAI) announced the delivery of the BlueWhale, a large autonomous underwater vehicle (AUV), to the German Navy. The handover is a key component in TKMS’s efforts to expand the maritime ecosystem of the future.

- In February 2026, Lockheed Martin unveiled its Lamprey Multi‑Mission Autonomous Undersea Vehicle, an unmanned underwater vehicle that can attach itself to ships, launch torpedoes, and deploy airborne drones.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$2.9 Bn |

| Forecast Revenue (2035) | US$9.0 Bn |

| CAGR (2026-2035) | 12.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Platform Type (Unmanned Underwater Vehicles (UUVs) and Unmanned Surface Vehicles (USVs)), By Vehicle Size (Small, Medium, and Large), By Propulsion (Electric, Hybrid, Diesel, and Gas-Turbine, and Renewable (Solar/Wave)), By Application (Commercial and Military) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | TKMS GmbH, BAE Systems plc, General Dynamics Corporation, Lockheed Martin Corporation, Unique Group, Teledyne Technologies Incorporated, Saab AB, L3Harris Technologies, Inc., Maritime Robotics AS, The Boeing Company, Exail Technologies SA, Elbit Systems Ltd., SAILDRONE, Inc., EDGE Group PJSC, SeaRobotics Corporation, Ocean Aero, Textron Inc., Sea Machines Robotics, Inc., Thales Group, Kongsberg Gruppen ASA, and Other Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |