Quick Navigation

Report Overview

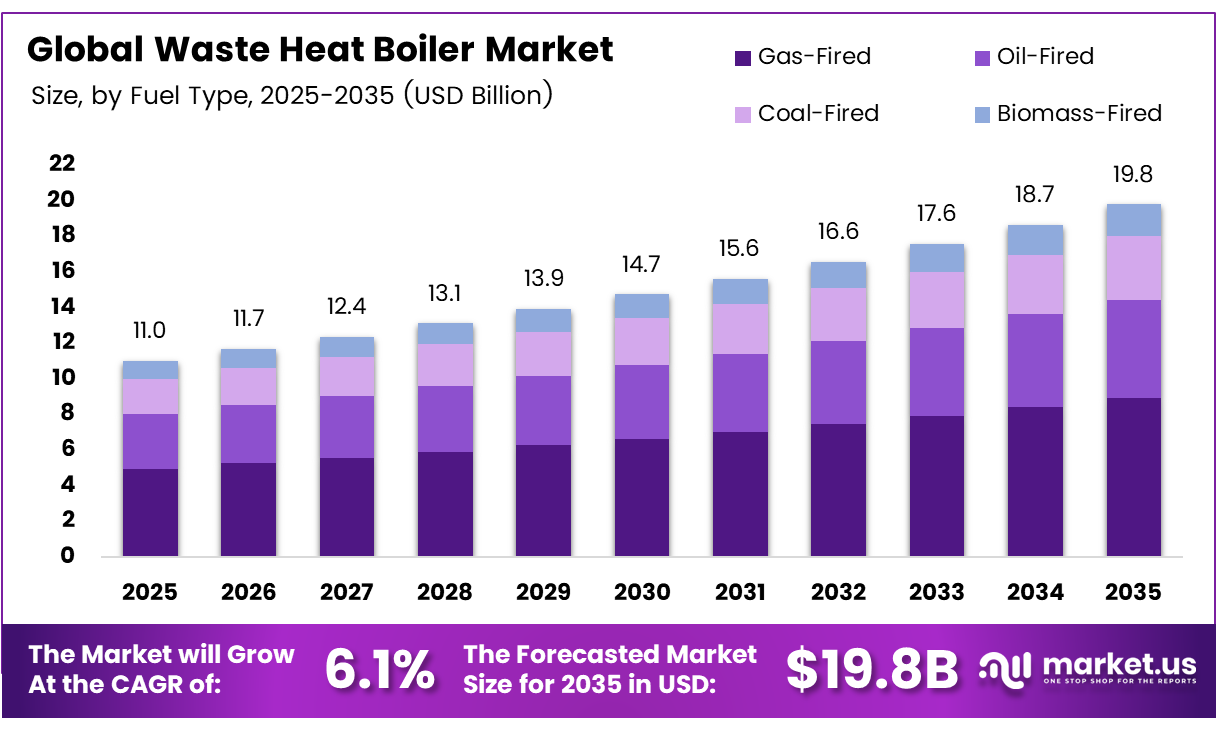

The Global Waste Heat Boiler Market size is expected to be worth around USD 19.8 billion by 2035 from USD 11.0 billion in 2025, growing at a CAGR of 6.1% during the forecast period 2026 to 2035.

Waste heat boilers recover thermal energy from exhaust gases, industrial off-gases, and turbine outputs that would otherwise escape unused. These systems convert recovered heat into usable steam or power, reducing the total fuel input a facility requires. This structural role in energy efficiency makes them a core capital investment for energy-intensive industries.

Cement, steel, and chemical manufacturing facilities drive the adoption of waste heat recovery boilers by integrating them into their core process infrastructure. Industrial operators choose these systems not just for compliance, but because they directly lower per-unit production costs. The financial case for adoption strengthens as energy prices remain elevated across major industrial economies.

Economizer-based waste heat recovery raises boiler efficiency from 88% to over 93%. A 5% point efficiency gain at scale represents millions in annual fuel savings for large industrial operators. This level of measurable performance improvement shifts procurement decisions from cost centers to strategic infrastructure choices.

Cogeneration and combined heat and power (CHP) infrastructure further extend the utility of waste heat boilers by enabling simultaneous electricity and steam output from a single fuel input. Refineries and petrochemical facilities increasingly embed these systems into their process design. The result is a tighter integration between energy recovery and production throughput.

Boiler economizers that preheat feedwater from 100°C to 180°C can cut fuel needed for the same steam output by 8–12%. This fuel reduction directly translates into lower operating expenditure for industrial buyers, making the payback period on capital investment a stronger commercial argument. Facilities running high-load operations gain the most measurable return.

Key Takeaways

- The Global Waste Heat Boiler Market was valued at USD 11.0 billion in 2025 and is forecast to reach USD 19.8 billion by 2035 at a CAGR of 6.1% during the forecast period 2026 to 2035.

- The 10–50 MW segment holds a 34.6% share, representing the dominant capacity range.

- Gas-Fired boilers lead with a 48.3% share of the market.

- Water Tube boilers dominate with a 43.1% share.

- Industrial Processes account for the largest share at 45.7%.

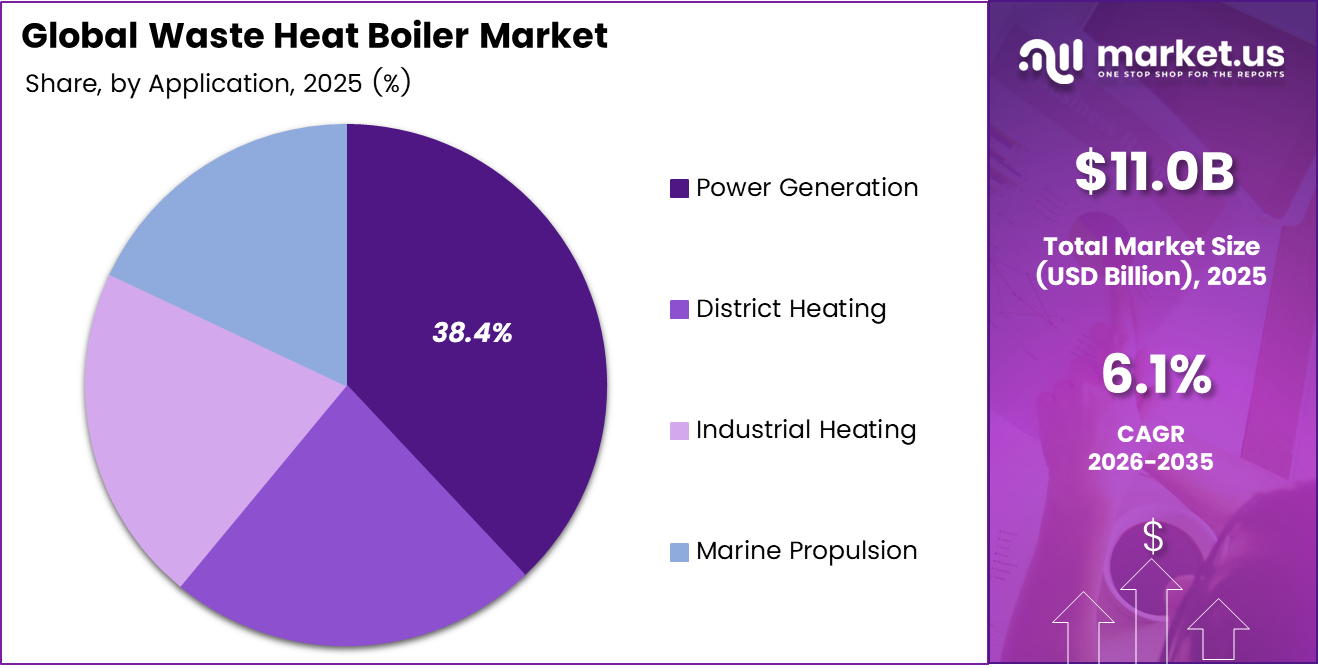

- Power Generation leads with a 38.4% share.

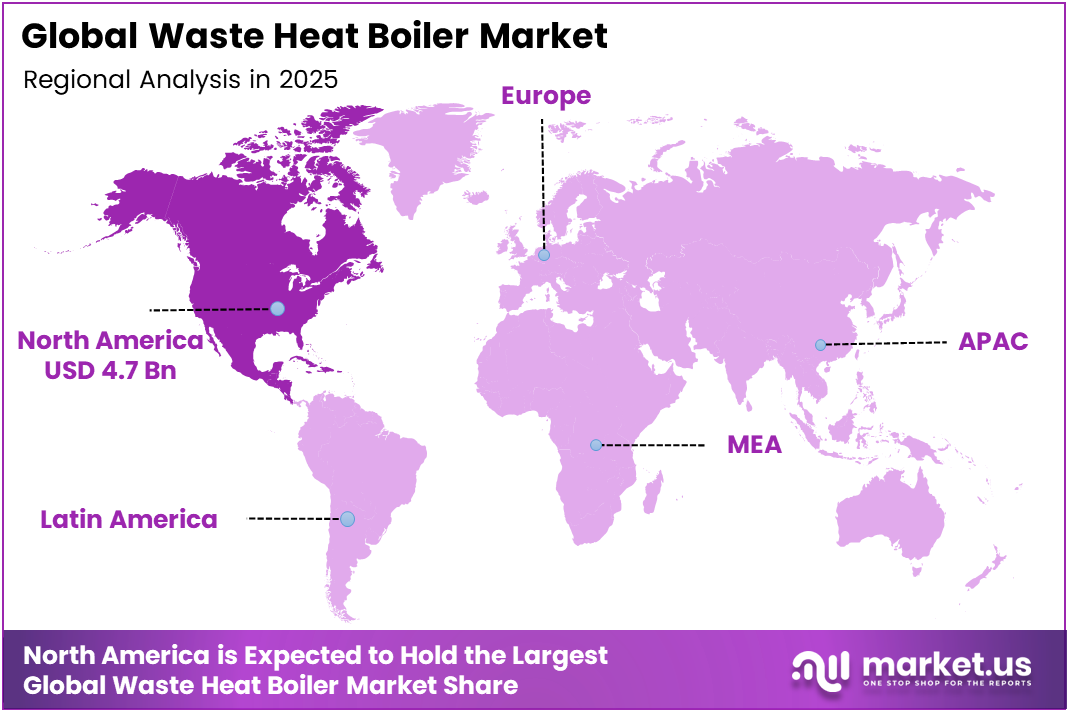

- North America dominates regional markets with a 42.7% share, valued at USD 4.7 billion in 2025.

Capacity Type Analysis

10–50 MW dominates with 34.6% due to broad industrial process compatibility.

In 2025, 10–50 MW held a dominant market position in the By Capacity Type segment of the Waste Heat Boiler Market, with a 34.6% share. This range fits the thermal output requirements of mid-scale cement, steel, and chemical plants — facilities large enough to justify capital investment but not requiring utility-scale infrastructure. Consequently, procurement cycles in this band are shorter, and project economics are easier to validate.

Less than 10 MW units serve small-scale industrial operations and distributed energy applications where space and budget constraints limit larger installations. These compact recovery systems allow facilities with moderate exhaust volumes to capture usable heat without a full plant overhaul. However, per-unit economics are thinner, making this segment more price-sensitive than higher-capacity ranges.

Fuel Type Analysis

Gas-Fired boilers dominate with 48.3% due to cleaner combustion and regulatory alignment.

In 2025, Gas-Fired boilers held a dominant market position in the By Fuel Type segment of the Waste Heat Boiler Market, with a 48.3% share. Natural gas produces lower particulate and sulfur emissions compared to oil and coal, making gas-fired systems the preferred choice in regions with tightening emission standards. Moreover, the infrastructure for gas supply in industrialized markets is well-established, reducing fuel availability risk for operators.

Oil-Fired waste heat boilers remain relevant in marine, offshore, and remote industrial settings where gas supply infrastructure is limited or unavailable. These units offer operational flexibility in fuel-diverse environments, though higher emission profiles make them less favored under current carbon reduction frameworks. Their share is likely to narrow as gas infrastructure expands in developing industrial regions.

Boiler Type Analysis

Water Tube boilers dominate with 43.1% due to high-pressure steam generation capability.

In 2025, Water Tube boilers held a dominant market position in the By Boiler Type segment of the Waste Heat Boiler Market, with a 43.1% share. Water tube designs handle high-pressure and high-temperature applications that fire tube configurations cannot safely sustain. This technical advantage makes them the standard specification for power generation, large refineries, and continuous-process manufacturing environments.

Horizontal Fire Tube boilers serve lower-pressure applications where operational simplicity and ease of maintenance take priority over maximum thermal performance. Their straightforward construction reduces installation costs and shortens maintenance intervals. However, their pressure ceiling limits use cases to light industrial heating and process support rather than power generation.

Waste Heat Source Type Analysis

Industrial Processes dominate with 45.7% due to continuous high-temperature exhaust availability.

In 2025, Industrial Processes held a dominant market position in the By Waste Heat Source Type segment of the Waste Heat Boiler Market, with a 45.7% share. Cement kilns, steel furnaces, and chemical reactors produce constant, high-volume exhaust streams that make waste heat recovery economically viable at scale. The continuous nature of these processes means recovery systems operate at near-full capacity, shortening payback periods and improving return on capital.

Turbine Exhaust represents a well-established waste heat source in power plants and gas compression stations. Exhaust-gas recovery from turbines feeds heat recovery steam generators (HRSGs), which improve total plant efficiency without additional fuel input. This source type benefits directly from the global expansion of combined cycle power generation infrastructure.

Application Analysis

Power Generation dominates with 38.4% due to the direct conversion of recovered heat to electricity.

In 2025, Power Generation held a dominant market position in the By Application segment of the Waste Heat Boiler Market, with a 38.4% share. Converting recovered exhaust heat into electricity creates a second revenue stream from thermal energy that would otherwise be vented. This dual-output economics makes power generation the most financially compelling application across large industrial and utility-scale installations.

District Heating applications use recovered steam or hot water to supply thermal energy to residential and commercial building networks. This model is most prevalent in Northern Europe and parts of Asia, where centralized heating infrastructure already exists. Waste heat boilers feeding district networks reduce municipal energy costs while enabling industrial facilities to monetize thermal by-products.

Key Market Segments

By Capacity Type

- Less than 10 MW

- 10–50 MW

- 50–100 MW

- Over 100 MW

By Fuel Type

- Gas-Fired

- Oil-Fired

- Coal-Fired

- Biomass-Fired

By Boiler Type

- Water Tube

- Horizontal Fire Tube

- Vertical Fire Tube

- Stirling Engine

By Waste Heat Source Type

- Industrial Processes

- Turbine Exhaust

- Reciprocating Engine Exhaust

- Renewable Energy Sources

By Application

- Power Generation

- District Heating

- Industrial Heating

- Marine Propulsion

Emerging Trends

Modular Design and Decarbonization Strategies Reshape Waste Heat Boiler Specifications

Industrial facilities with constrained floor space now favor modular and compact waste heat boiler configurations that can be retrofitted without major civil works. Vendors responding to this preference gain faster procurement approval from plant engineers. This design shift compresses delivery timelines and lowers total installed cost, making recovery systems accessible to a broader range of industrial sites.

Advances in high-temperature resistant materials extend boiler service life and reduce scheduled downtime in extreme thermal environments. Materials capable of sustaining performance above 500°C unlock applications in high-pressure steam generation that older alloys could not support reliably. In CHP applications, an economizer plus air preheater combination raises total system efficiency to over 95% — a benchmark that newer materials make structurally achievable.

Industrial decarbonization targets are pulling waste heat boilers into hybrid and renewable energy configurations. Facilities pairing recovery systems with biomass or solar thermal inputs reduce net carbon intensity without sacrificing thermal output. This integration trend positions waste heat boilers as infrastructure components within broader low-emission energy strategies, expanding their addressable market beyond traditional fossil-fuel-dependent industries.

Drivers

Emission Mandates and Energy Cost Pressure Accelerate Industrial Deployment of Waste Heat Boilers

Stringent environmental regulations force industrial facilities in North America, Europe, and Asia to reduce carbon output from thermal operations. Waste heat boilers address this requirement by recovering exhaust energy that would otherwise contribute to atmospheric emissions. Compliance timelines set by regulators create non-discretionary procurement cycles, making waste heat recovery a budget line item rather than an optional capital upgrade.

Cement, steel, and chemical manufacturers face dual pressure from rising energy costs and carbon pricing mechanisms. Deploying waste heat recovery technology across these sectors lowers per-unit fuel consumption while generating usable steam or electricity from existing process exhaust. A 2025 boiler-efficiency study found combined waste heat recovery measures produced a 6.2% total efficiency improvement, equivalent to approximately 88 MW — a result that directly translates into measurable operational savings at scale.

Cogeneration and combined heat and power infrastructure multiply the financial return on waste heat recovery investment by enabling simultaneous electricity and thermal output from a single fuel source. Industrial operators using CHP configurations lower their dependence on grid electricity while improving total site energy efficiency. This dual-output economics makes the business case for waste heat boiler adoption compelling even in markets without direct regulatory mandates.

Restraints

Capital Intensity and Operational Complexity Slow Waste Heat Boiler Uptake Among Smaller Industrial Operators

Small and medium enterprises face a structural barrier to waste heat boiler adoption due to high upfront capital requirements and technically demanding installation processes. Unlike large industrial groups with dedicated engineering teams, smaller operators lack the procurement expertise and financial headroom to absorb initial investment costs. This limits market penetration in the long tail of industrial buyers despite strong operational economics for larger facilities.

High-temperature exhaust environments accelerate corrosion and fouling in boiler tubes, heat exchangers, and flue gas paths. Exhaust gas temperatures above 250°C are required for suitable waste heat recovery, while temperatures above 500°C are ideal for high-pressure steam generation — operating ranges that simultaneously drive thermal performance and material degradation. Maintenance complexity at these temperatures increases service costs and requires specialized technical personnel that many operators struggle to retain.

Operational reliability concerns compound the capital barrier for risk-averse buyers. A boiler experiencing unplanned downtime in an integrated industrial process can disrupt upstream and downstream production simultaneously. Consequently, facilities with limited redundancy capacity hesitate to introduce an additional critical system, slowing adoption timelines in sectors where operational continuity outweighs efficiency gains.

Growth Factors

Industrialization in Emerging Economies and Green Energy Funding Expand the Addressable Market for Waste Heat Recovery

Emerging economies in Asia, Africa, and Latin America are building new industrial capacity in cement, steel, and chemicals — sectors where waste heat boiler integration from the design stage is more economical than retrofitting. Greenfield industrial projects offer vendors an earlier and cleaner entry point compared to mature markets. This structural pipeline of new-build industrial investment creates sustained demand for heat recovery systems through the forecast period.

Waste heat recovery power-plant conversion efficiency reaches 18–26% depending on technology and configuration. This efficiency range signals that a meaningful share of industrial exhaust energy remains technically and economically recoverable, representing an untapped revenue stream for facility operators. Refineries and petrochemical processors with large continuous exhaust volumes stand to benefit most from closing this conversion gap.

Government incentive programs and green energy funding mechanisms lower the effective cost of waste heat recovery projects for industrial operators. Digital monitoring and smart automation technologies further improve the investment case by enabling predictive maintenance, reducing unplanned downtime, and optimizing thermal performance in real time. Together, financial incentives and operational intelligence tools remove two of the most significant adoption barriers simultaneously.

Regional Analysis

North America Dominates the Waste Heat Boiler Market with a Market Share of 42.7%, Valued at USD 4.7 Billion

North America leads the global Waste Heat Boiler Market with a 42.7% share valued at USD 4.7 billion in 2025. Mature industrial infrastructure across refining, petrochemical, and power generation sectors creates a large installed base for both new deployments and system upgrades. Moreover, federal and state-level energy efficiency mandates sustain procurement activity across the forecast period.

Europe drives waste heat boiler adoption through binding carbon reduction targets under the EU Green Deal and industrial decarbonization frameworks. The region’s concentration of heavy manufacturing in Germany, France, and the UK generates continuous exhaust streams suited for high-efficiency recovery systems. Additionally, district heating networks in Northern Europe provide ready-made distribution infrastructure for recovered thermal energy.

Asia Pacific represents the fastest-expanding geographic base for waste heat boiler installations, supported by large-scale industrial capacity additions in China, India, and Southeast Asia. Steel, cement, and chemical production in these economies generate substantial exhaust volumes that recovery systems can convert to steam or power. Government-backed energy efficiency programs in China and India further accelerate industrial adoption.

Latin America presents a developing opportunity for waste heat recovery technology, particularly in Brazil and Mexico, where energy-intensive industries such as mining, cement, and food processing operate at scale. Infrastructure investment constraints and fragmented industrial ownership structures slow adoption compared to more consolidated markets. However, rising energy costs are strengthening the financial case for recovery system deployment.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Analysis

General Electric positions itself at the intersection of power generation and industrial heat recovery, leveraging its gas turbine and HRSG portfolio to offer integrated cycle solutions. Its engineering depth enables it to address utility-scale waste-heat boiler projects that smaller vendors cannot serve. This scale advantage makes GE a preferred vendor for large combined cycle and cogeneration project developers globally.

Alstom focuses its waste heat recovery capabilities within the power plant engineering segment, where its thermal systems expertise complements turbine integration projects. The company’s strength in European infrastructure markets aligns well with regulatory pressure driving cogeneration adoption across the continent. Alstom’s project execution track record in large-scale thermal facilities reinforces its competitive position in long-cycle procurement processes.

Siemens applies its industrial automation and energy management capabilities to differentiate waste heat boiler offerings through digital integration. By combining heat recovery hardware with real-time performance monitoring platforms, Siemens addresses the operational efficiency demands of industrial operators seeking predictive maintenance. This technology layering creates switching costs that pure equipment vendors cannot replicate.

Thermax serves the mid-market industrial segment across Asia and other emerging economies with a cost-competitive portfolio of waste-heat recovery boilers tailored for cement, steel, and chemical applications. Its manufacturing base and regional service network give it a structural cost and proximity advantage over Western competitors in high-growth Asian markets. Thermax’s focus on total lifecycle value rather than upfront price creates stronger retention among repeat industrial buyers.

Key Players

- General Electric

- Alstom

- Siemens

- Thermax

- Foster Wheeler

- Mitsubishi Heavy Industries

- Babcock & Wilcox

- Clyde Bergemann

- Doosan Lentjes

- KK Standardkessel GmbH

- Forbes Marshall

- Takuma Co. Ltd

- Byworth Boilers Limited

- Steinmuller Engineering GmbH

- JFE Engineering Corporation

- Clarke Energy

- Thermodyne Engineering System

- Kawasaki Heavy Industries Ltd

Recent Developments

- In 2025, General Electric / GE Vernova continues to supply and service HRSGs for combined-cycle plants. GE Vernova said Japan’s Goi Thermal Power Station uses HRSGs to generate superheated steam and create “up to 50% more energy without additional fuel.” It also announced HRSG-linked equipment scopes for Singapore’s YTL PowerSeraya carbon-capture-ready plant and Poland’s Kozienice CCGT.

- In 2025, Siemens Energy remains active in HRSG/waste-heat power. It signed a waste-heat-to-power pilot with TC Energy in Alberta, capturing waste heat from a pipeline compressor turbine and converting it to emissions-free power, with estimated GHG reductions of 44,000 tons/year. Its 2025 Benson HRSG reference list shows 139 references and includes 2024 Taiwan/Kuo Kuang II entries.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 11.0 Billion |

| Forecast Revenue (2035) | USD 19.8 Billion |

| CAGR (2026-2035) | 6.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Capacity Type (Less than 10 MW, 10–50 MW, 50–100 MW, Over 100 MW), By Fuel Type (Gas-Fired, Oil-Fired, Coal-Fired, Biomass-Fired), By Boiler Type (Water Tube, Horizontal Fire Tube, Vertical Fire Tube, Stirling Engine), By Waste Heat Source Type (Industrial Processes, Turbine Exhaust, Reciprocating Engine Exhaust, Renewable Energy Sources), By Application (Power Generation, District Heating, Industrial Heating, Marine Propulsion) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | General Electric, Alstom, Siemens, Thermax, Foster Wheeler, Mitsubishi Heavy Industries, Babcock & Wilcox, Clyde Bergemann, Doosan Lentjes, KK Standardkessel GmbH, Forbes Marshall, Takuma Co. Ltd, Byworth Boilers Limited, Steinmuller Engineering GmbH, JFE Engineering Corporation, Clarke Energy, Thermodyne Engineering System, Kawasaki Heavy Industries Ltd |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |