Quick Navigation

Report Overview

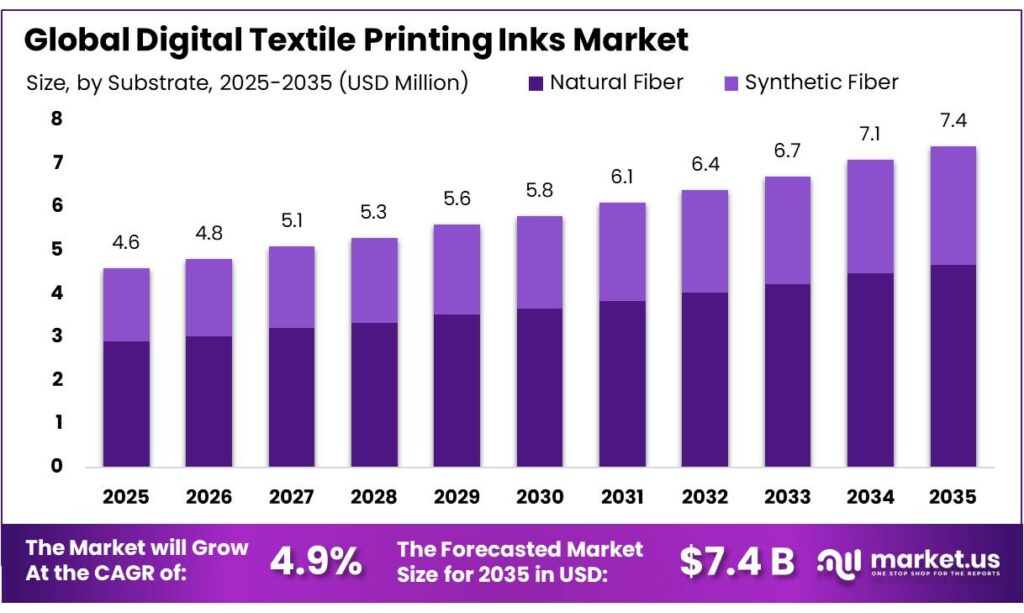

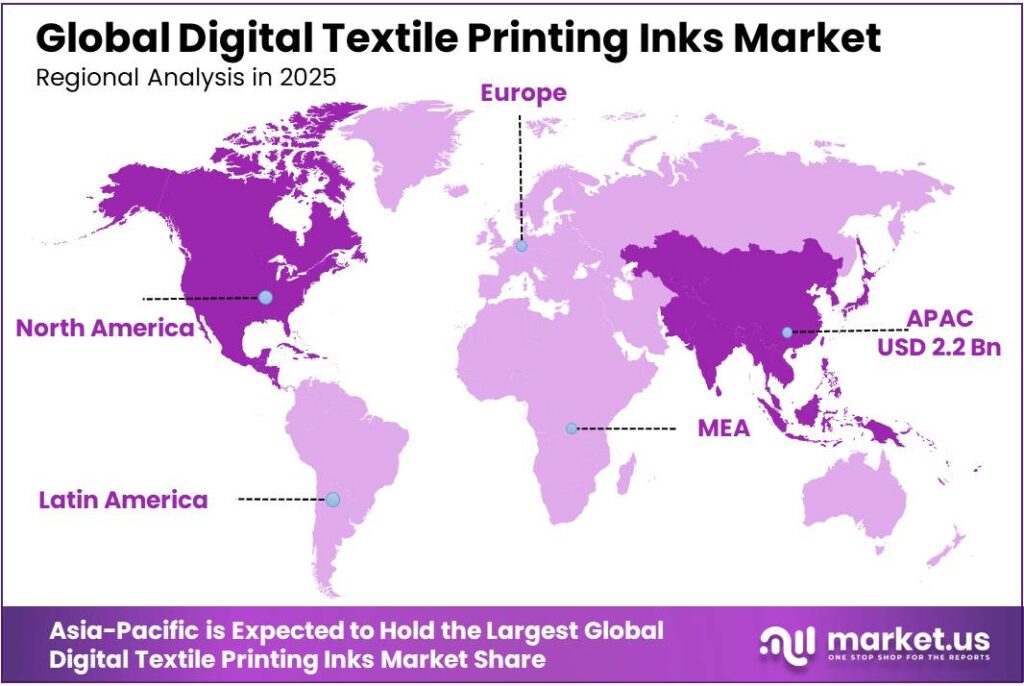

The Global Digital Textile Printing Inks Market size is expected to be worth around USD 7.4 Billion by 2035, from USD 4.6 Billion in 2025, growing at a CAGR of 4.9% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 48.1% share, holding USD 2.2 Billion revenue.

Digital textile printing inks represent the chemistry layer that enables direct-to-fabric, roll-to-roll, and hybrid on-demand textile production. The segment is becoming strategically important because apparel and home-textile producers are under pressure to shorten lead times, reduce inventory risk, and improve environmental performance at the print stage.

Its industrial relevance is reinforced by the broader textile base: global fiber production reached a record 124 million tonnes in 2023, showing the scale of substrate demand that digital inks can potentially address. At the same time, world trade in goods and services rose to US$34.65 trillion in 2025, indicating that textile supply chains remain globally integrated and commercially significant.

The industrial scenario is increasingly shaped by sustainability regulation and circularity requirements rather than by volume expansion alone. In the European Union, average consumption of clothing, footwear, and household textiles reached 19 kg per person in 2022, equivalent to about 8.5 million tonnes across the EU, while textile waste generation stood at about 6.94 million tonnes, or 16 kg per person.

These figures are raising pressure on converters, mills, brands, and ink suppliers to move toward lower-waste decoration processes, especially pigment-based digital systems that can reduce wet processing steps. Globally, UNEP states that the sector generates 92 million tonnes of textile waste every year, while garment production doubled from 2000 to 2015 and average garment use duration fell by 36%, all of which strengthen the business case for more efficient digital print workflows.

Growth is also being supported by policy and compliance. The European Commission’s textiles strategy sets a 2030 vision for textiles that are more durable, recyclable and competitive, pushing the industry toward cleaner chemistry and smarter production. On the chemical side, OEKO-TEX states that ECO PASSPORT applies to chemicals, colourants and auxiliaries for textile production and is recognized by ZDHC from Level 1 to Level 3; it also connects to a network of over 35,000 certified companies.

In parallel, UNEP launched a $43 million programme with Bangladesh, Indonesia, Pakistan and Viet Nam to reduce hazardous chemicals in textiles; those four countries account for nearly 15% of global clothing exports, and wet processing can use 0.58 kg of chemical inputs per 1 kg of fabric produced. These developments support higher adoption of certified digital textile inks.

Regulatory momentum is also important. The European Commission adopted its textile strategy on 30 March 2022; the Ecodesign for Sustainable Products Regulation entered into force in July 2024; and, on 9 April 2025, the Commission launched consultation work on the Digital Product Passport, which is intended to improve product data transparency for consumers, businesses, and public authorities. Together, these initiatives are pushing the industry toward traceable, circular, and lower-impact textile production systems, where digital inks are well positioned.

Key Takeaways

- Digital Textile Printing Inks Market size is expected to be worth around USD 7.4 Billion by 2035, from USD 4.6 Billion in 2025, growing at a CAGR of 4.9%.

- Reactive held a dominant market position, capturing more than a 34.8% share.

- Natural Fiber held a dominant market position, capturing more than a 63.5% share.

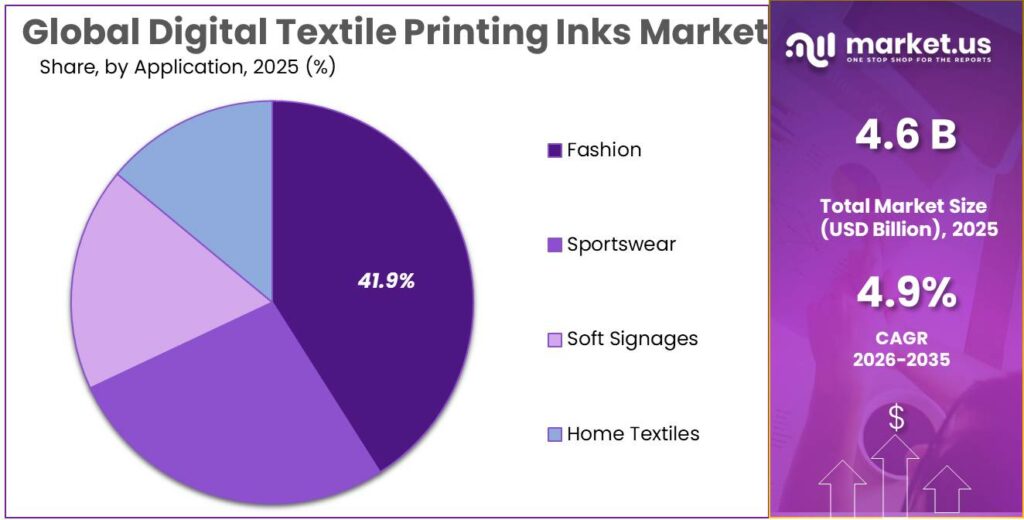

- Fashion held a dominant market position, capturing more than a 41.9% share.

- Asia-Pacific holds the leading position in the digital textile printing inks market, accounting for 48.1% share with a market value of around USD 2.2 billion.

By Type Analysis

Reactive inks lead strongly with 34.8% driven by high color vibrancy and fabric compatibility

In 2025, Reactive held a dominant market position, capturing more than a 34.8% share. This strong presence is mainly linked to its excellent bonding with natural fibers such as cotton, which continues to be widely used in the textile industry. Manufacturers prefer reactive inks because they produce bright, long-lasting colors and maintain softness in fabrics, which is important for clothing and home textiles. The demand remained steady throughout 2025 as fashion brands focused more on quality and durability in printed fabrics.

By Substrate Analysis

Natural fiber segment stays ahead with 63.5% supported by strong demand in cotton-based textiles

In 2025, Natural Fiber held a dominant market position, capturing more than a 63.5% share. This leadership mainly comes from the high use of cotton and other natural fabrics in everyday clothing, home textiles, and fashion products. Digital printing on natural fibers is widely preferred because it gives better color absorption and a softer finish, which consumers value. Throughout 2025, brands continued to focus on comfort and quality, which kept the demand for natural fiber printing steady.

By Application Analysis

Fashion segment leads with 41.9% as demand for customized and fast-changing styles grows

In 2025, Fashion held a dominant market position, capturing more than a 41.9% share. This was mainly driven by the rising need for quick design changes and shorter production cycles in the apparel industry. Digital textile printing fits well with fashion trends where brands want flexibility, small batch production, and unique designs. Throughout 2025, designers and manufacturers relied heavily on digital inks to create detailed prints with vibrant colors, helping them respond faster to changing consumer preferences.

Key Market Segments

By Type

- Reactive

- Acid

- Direct Disperse

- Sublimation

- Pigment

By Substrate

- Natural Fiber

- Synthetic Fiber

By Application

- Fashion

- Sportswear

- Soft Signages

- Home Textiles

Emerging Trends

Shift toward eco-friendly and water-based inks is becoming the new normal

One of the most noticeable trends in digital textile printing inks is the growing shift toward eco-friendly and water-based formulations. This is mainly driven by stricter environmental rules and rising awareness among brands and consumers. In recent years, over 31% of digitally printed textiles have already been produced using water-based inks, helping reduce environmental impact by nearly 60% compared to solvent-based options. This clearly shows how fast the industry is moving toward cleaner alternatives.

In 2025, manufacturers focused more on reducing water usage, chemical discharge, and emissions during production. Many countries have also introduced limits on harmful emissions like VOCs, pushing companies to adopt safer ink solutions. By 2026, this shift became even stronger as textile brands started promoting sustainability as a core value, not just an option. Water-based inks are gaining popularity because they are less toxic and easier to manage in production. This trend is not just about compliance, it is also about brand image and long-term cost savings.

Rise of customization and fast production cycles shaping ink demand

Another key trend is the growing need for customization and faster production, especially in fashion and e-commerce. Digital textile printing allows manufacturers to quickly create unique designs without long setup times. The overall digital textile printing market is expanding quickly, reaching around USD 2.9 billion in 2025 and about USD 3 billion in 2026, showing steady growth in adoption. This growth directly supports the demand for advanced inks that can deliver high-quality results at speed.

Drivers

Rising textile and apparel demand is pushing digital printing adoption

One of the biggest drivers for digital textile printing inks is the steady growth of the textile and apparel industry worldwide. The demand for clothing and home textiles is increasing every year, and this directly pushes the need for faster and more flexible printing solutions. For example, the global apparel market was already valued at around US$ 1.8 trillion in 2024 and is expected to grow further in the coming years. In India alone, the textile and apparel market is projected to reach nearly US$ 190 billion by 2025–26, showing strong domestic consumption.

This kind of large-scale demand creates pressure on manufacturers to produce designs quickly and efficiently. Digital textile printing inks become a natural choice because they reduce setup time and allow quick design changes compared to traditional methods. In 2025, many apparel brands shifted toward short production cycles and customized designs, which increased the use of digital inks.

Strong government support and cotton ecosystem boosting printing demand

Another key factor is the strong backing from governments and the availability of raw materials like cotton. Cotton alone accounts for around 23% of global fibre production, and India is one of the largest producers and consumers of it. This matters because natural fibers like cotton are widely used in digital textile printing, especially with reactive inks.

Governments are also actively supporting the textile sector. For instance, initiatives like the Production Linked Incentive (PLI) scheme have already attracted ₹7,343 crore in investments, helping expand manufacturing capacity. At the same time, schemes like MITRA parks are designed to bring the entire textile value chain—from fiber to printing—into one place, making production more efficient

Restraints

High initial setup cost limits adoption for small manufacturers

One major restraining factor for digital textile printing inks is the high initial investment required to set up digital printing systems. Compared to traditional printing methods, digital textile printers, compatible inks, and maintenance systems cost significantly more. This becomes a real challenge, especially for small and medium textile units that operate on tight budgets. For context, the textile sector is largely made up of small players— in India, over 80% of textile units are MSMEs, according to Ministry of Textiles India. Many of these businesses find it difficult to shift to digital systems due to cost pressure.

In 2025, this financial barrier continued to slow down adoption in developing regions where traditional printing is still cheaper to run. Even though digital printing reduces waste and saves time in the long run, the upfront cost makes businesses hesitate. By 2026, while some larger manufacturers adopted the technology, smaller units remained cautious. Government schemes are trying to help, but the gap between affordability and technology adoption still exists.

Limited awareness and skill gap in adopting new printing technologies

Another important restraint is the lack of technical knowledge and skilled workforce required to operate digital textile printing systems. Unlike traditional printing, digital printing needs trained operators who understand software, color management, and machine handling. Many regions still face a shortage of such skilled workers. According to National Skill Development Corporation, India alone needs to skill millions of workers across industries, including textiles, to meet modern manufacturing demands.

Opportunity

Growing shift toward sustainable and low-water textile production

One major growth opportunity for digital textile printing inks is the increasing shift toward sustainable production in the textile industry. Traditional textile printing uses a large amount of water and chemicals, which creates environmental pressure. In contrast, digital printing uses significantly less water and reduces chemical waste, making it a better option for modern manufacturing. Studies show that digital textile printing can drastically reduce water and chemical consumption compared to conventional methods.

In 2025, many textile manufacturers started moving toward cleaner production methods due to stricter environmental regulations and growing consumer awareness. Governments are also pushing sustainability goals through textile policies and eco-friendly initiatives. For example, India’s textile policies focus on promoting sustainable processing and reducing environmental impact through modern technologies.

Rapid expansion of digital textile printing market creating new ink demand

Another major opportunity comes from the fast growth of digital textile printing itself, which directly increases the need for specialized inks. The global digital textile printing market reached around USD 5.0 billion in 2025 and continues to grow at a strong pace. This growth is supported by rising demand for customized clothing, fast fashion, and on-demand production. As printing technology expands, the need for high-performance inks also increases.

Government support for textile modernization and digital adoption is also playing a role in this shift. As more companies invest in digital printing machines and infrastructure, the demand for compatible inks grows alongside. This creates a long-term opportunity for ink manufacturers to innovate and supply better-quality, efficient, and sustainable products.

Regional Insights

Asia-Pacific dominates with 48.1% share driven by strong textile manufacturing base

Asia-Pacific holds the leading position in the digital textile printing inks market, accounting for 48.1% share with a market value of around USD 2.2 billion, making it the most dominant regional segment. This leadership is mainly supported by the region’s well-established textile manufacturing ecosystem, especially in countries like China, India, Bangladesh, and Vietnam, which collectively contribute a large portion of global textile exports.

The region benefits from cost-effective production, availability of raw materials, and a strong labor base, which makes it attractive for both traditional and digital textile operations.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Sun Chemical is one of the largest players in printing inks, with annual revenue around USD 3.5 billion and nearly 20,000 employees globally. The company has a strong presence in packaging and textile inks, supported by its parent DIC Corporation, which itself generates over ¥1054 billion in revenue. Its wide global network and continuous investment in pigment and ink technologies make it a key supplier in digital textile printing markets.

Dover Corporation plays a significant role through its digital printing and identification segment. In 2025, the company reported USD 8.1 billion in revenue and about 24,000 employees worldwide. Its imaging and identification division supports textile printing technologies, including ink systems. Strong investment of nearly USD 165 million in R&D in 2025 highlights its focus on innovation and expanding capabilities in industrial and digital printing markets.

BASF SE is the world’s largest chemical producer, with revenue of €68.9 billion in 2023 and around 111,991 employees globally. The company supplies pigments, chemicals, and raw materials used in textile inks. Its strong financial scale allows continuous development of high-performance and sustainable solutions. BASF’s involvement in pigments and coatings directly supports the advancement of digital textile printing inks across multiple industrial applications.

Top Key Players Outlook

- Sun Chemical Group Cooperatief U.A.

- Kornit Digital Ltd.

- Dover Corporation

- BASF SE

- DyStar Singapore Pte Ltd

- Zhengzhou Hongsam Digital Science & Technology Co., Ltd.

- Huntsman International LLC

- Sawgrass Technologies Inc.

- SPGPrints

- Zhejiang Lanyu Digital Technology Co. Ltd

Recent Industry Developments

Sun Chemical Group Coöperatief U.A. plays a strong and steady role in the digital textile printing inks space, mainly through its expertise in pigments, color chemistry, and inkjet technologies. As of 2025, the company operates with over 21,000–22,000 employees globally and is part of the larger DIC Group, which together generates more than USD 8.5 billion in annual sales, giving it a solid financial base to support innovation in digital inks.

In 2026, Kornit continues to expand its ink and consumables segment through its “All-Inclusive Click” model, generating about USD 25 million in recurring revenue, which reflects growing adoption of its ink-based subscription approach.

BASF SE plays a foundational role in the digital textile printing inks market, mainly through its strong presence in pigments, dyes, and specialty chemicals that are essential for ink formulations. In 2025, BASF reported €59.7 billion in total sales and €6.6 billion EBITDA, reflecting its massive scale and ability to support multiple industries, including textiles and printing

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 4.6 Bn |

| Forecast Revenue (2035) | USD 7.4 Bn |

| CAGR (2026-2035) | 4.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Reactive, Acid, Direct Disperse, Sublimation, Pigment), By Substrate (Natural Fiber, Synthetic Fiber), By Application (Fashion, Sportswear, Soft Signages, Home Textiles) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Sun Chemical Group Cooperatief U.A., Kornit Digital Ltd., Dover Corporation, BASF SE, DyStar Singapore Pte Ltd, Zhengzhou Hongsam Digital Science & Technology Co., Ltd., Huntsman International LLC, Sawgrass Technologies Inc., SPGPrints, Zhejiang Lanyu Digital Technology Co. Ltd |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |