Quick Navigation

Report Overview

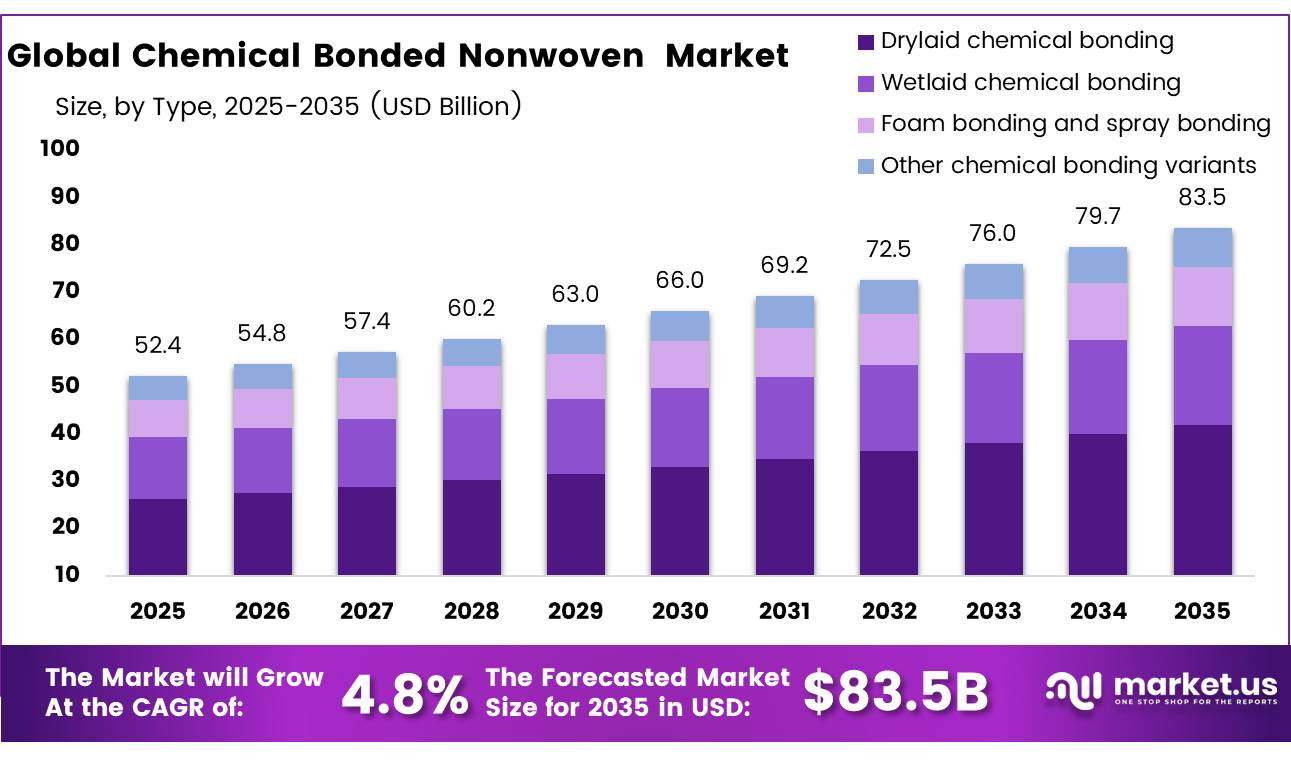

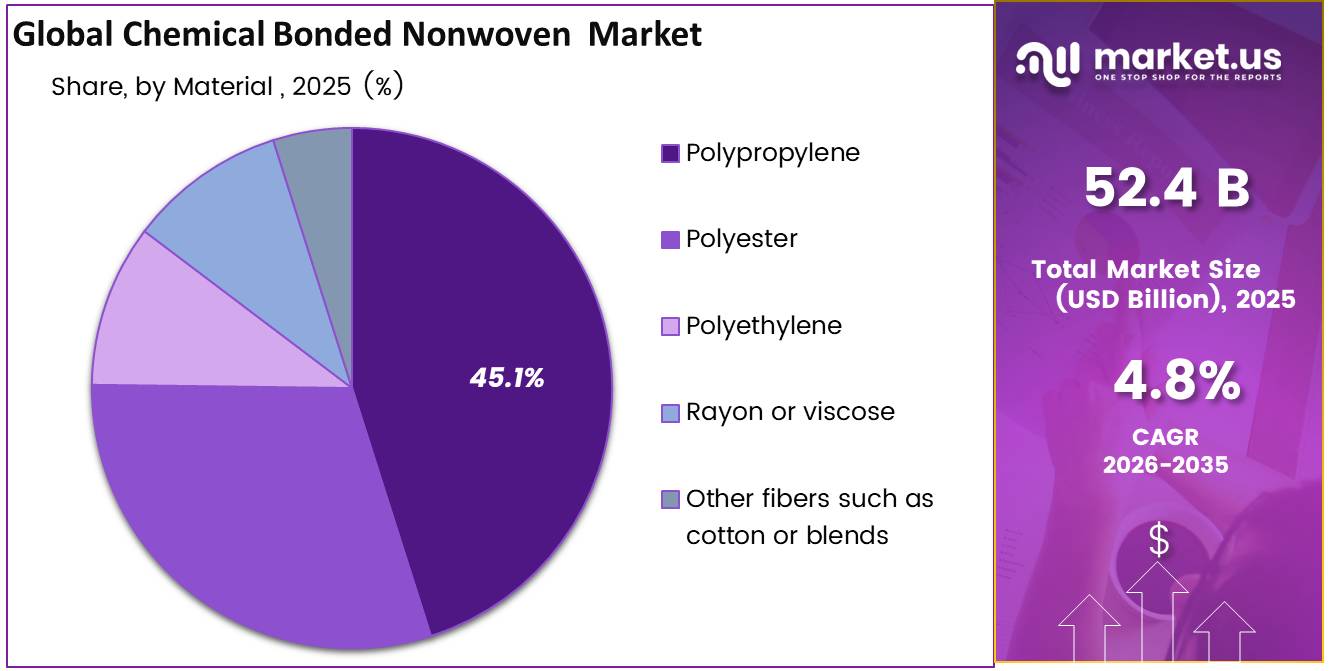

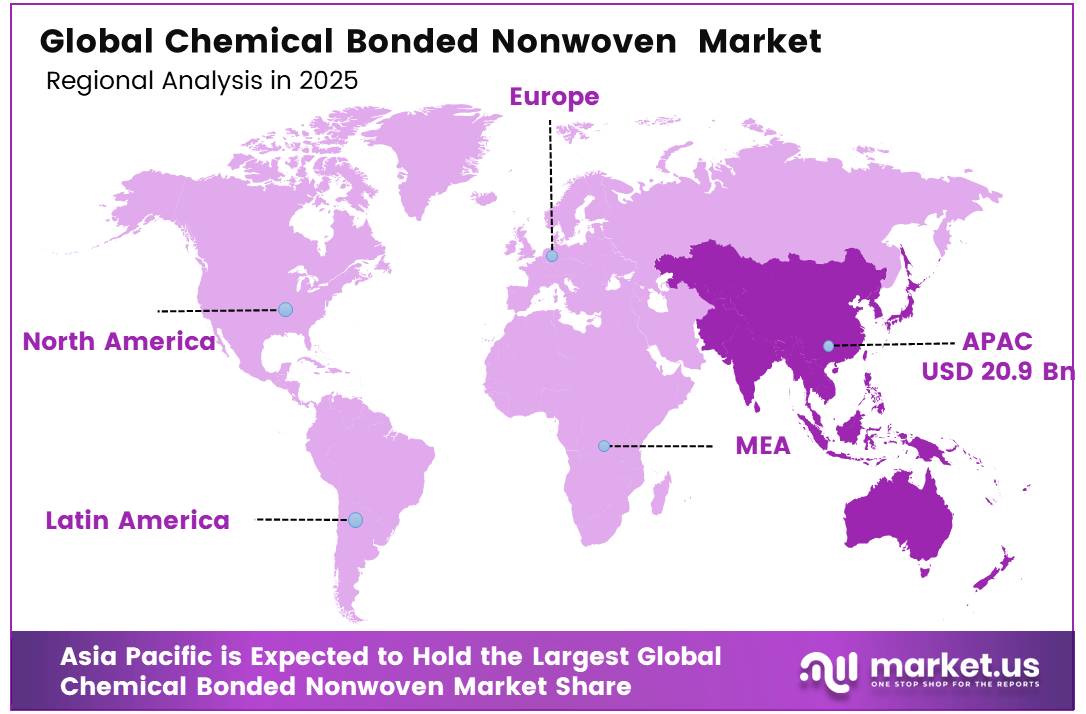

The Global Chemical Bonded Nonwoven Market size was estimated at USD 52.4 billion in 2025, which is expected to grow up to USD 83.5 billion in 2035 with a CAGR of 4.8%. In 2025, Asia Pacific held a dominant market position, capturing more than a 40.1% share, holding USD 20.99 billion in revenue.

Chemical Bonded Nonwovens are technically engineered textiles created through chemical bonding of webs made up of fibers, used mainly in hygiene, healthcare, filtration, automotive interior, and construction applications. The Global Chemical Bonded Nonwovens Market can be broadly segmented into four major categories based on their types: Drylaid Chemical Bonding, Wetlaid Chemical Bonding, Foam & Spray Bonding, and Others Chemical Bonding Types.

- In March 2026, Berry Global Inc. announced the start-up of the new drylands chemical bonding line in Suzhou, China, having an additional annual capacity of 35,000 metric tons for premium hygiene coverstock, wherein more than 68% of the output has been committed already through long-term contracts with Asia Pacific-based major FMCG companies like Unicharm and Essity from 2026 to 2029.

Key Takeaways

- The global chemical bonded nonwoven market was valued at USD 52.4 billion in 2025.

- The global market is projected to grow at a CAGR of 4.8% and is estimated to reach USD 83.5 billion by 2035.

- On the basis of type, the Drylaid Chemical Bonding dominated the market, constituting 50.1% of the total market share.

- Based on the material, the Polypropylene material dominated the chemical bonded nonwoven market, with a substantial market share of around 45.1%.

- Among the application, Hygiene Products held a major share in the chemical bonded nonwoven market, 40.2% of the market share.

- Among the end use, Hygiene And Personal Care is the most considerable within the market, accounting for around 40.3% of the revenue.

- In 2025, the Asia Pacific was the most dominant region in the chemical bonded nonwoven market, accounting for 40.1% of the total global consumption

The global chemical bonded nonwoven market is really taking off, mainly due to a big increase in demand for disposable hygiene products in Asia Pacific and Africa. In these regions, there’s still a lot of room for growth when it comes to things like diapers. Healthcare developments worldwide, such as India’s Ayushman Bharat plan and hospital expansions from Saudi Vision 2030, are boosting continuous need from institutions for medical-grade nonwovens.

At the same time, stricter air and water quality rules in the US, EU, and China speed up the use of chemically bonded filtration materials. Plus, cheaper polypropylene fibers and more efficient production lines mean bigger profits for top companies in the industry.

Chemical Bonded Nonwoven Market Segment

Type Analysis

Drylaid Chemical Bonding represents dominant Segment in the Market.

Drylaid Chemical Bonding leads the type category with an impressive 50.1% market share, valued at around US$ 26.2 billion by 2025. The strength of this segment is backed by matured airlaid and carding lines, ease with regard to high-speed binder saturation and latex application technologies, and its suitability for incorporation in the hygiene and medical product production lines. Around 65% of the global disposable hygiene nonwovens are produced by using drylaid chemical bonding because of its ease regarding fiber mix possibilities and processing speeds.

Some of the major players like Berry Global, Kimberly-Clark, and Avgol Nonwovens have their massive drylaid lines in operation with speeds of over 800 m/min. The capital maturity of drylaid processes and availability of low-priced polypropylene and polyester fibers ensure its dominance till 2035.

Wetlaid Chemical Bonding is the fastest-growing type segment is boosted by increasing demand for high-uniformity filters and high-quality medical wipes. This growth is attributed to increasing stringent air and water filtration standards for the HVAC, pharmaceutical, and water treatment industries

Material Analysis

Polypropylene Are the Most Widely Used Materials

Polypropylene (PP) dominates the material category with a market share of about 45.1%. The popularity of PP lies in its low density moisture resistance, suitability to dry- and wet-laid processes, and lower cost relative to polyester and specialty fibers. World PP fiber production exceeded 8.3 million metric tons in 2024, providing sufficient feedstock for nonwoven producers. PP’s hydrophobicity suits PP in use for outer and acquisition layers of diaper cores, feminine hygiene pads, and adult incontinence disposables.

Polyester is the most rapidly-growing material category,driven by increasing demand for heat-resistant nonwovens for air filters and automotive interior components due to its higher melting temperature and higher modulus than polypropylene.

Application Analysis

Hygiene Products Held a Major Share of the Market.

The Hygiene Products segment represents the largest application category, capturing a 40.2% share of the global chemical bonded nonwoven market. This dominance is underpinned by structural, non-cyclical demand for disposable diapers, feminine hygiene pads, adult incontinence products, and wet wipes across both mature and emerging markets.

Chemically bonded nonwovens serve critical functional roles in these products as coverstock, acquisition distribution layers, and back sheets, with manufacturers such as Procter And Gamble, Unicharm, and Essity consuming over 1.2 million metric tons per year of chemically bonded nonwoven substrates. Diaper penetration rates remaining below 31% in South and Southeast Asia and below 18% in Sub-Saharan Africa represent a substantial unrealized volume opportunity through 2035, while the rapidly aging populations of China, Japan, and Western Europe are driving accelerating demand for adult incontinence nonwovens.

The Medical Products application is the fastest growing segment, driven by continuous demand for surgical drapes, isolation gowns, wound dressings, and hospital bed linen. The Filtration Media segment holds a significant share due to its use in industrial air filtration and water treatment applications. Automotive Interiors and Components continue to grow alongside rising vehicle production and increasing soundproofing requirements. The remaining application categories complete the overall spectrum.

End Use Analysis

Chemical Bonded Nonwoven Are Mostly Utilized in Hygiene And Personal Care

The hygiene and personal care market segment holds dominance in end use at 40.3%, owing to the consistent non-cyclical demand for diapers, feminine care pads, adult incontinence care products, and wet wipes due to the estimated birth population in Africa and South Asia aged between 0-4 years of 750 million by 2030 and premiumization of urban Asia Pacific markets post-2028.

Medical and healthcare represent the fastest-growing end-use market segment, supported by the growth of healthcare infrastructure on a global basis, the use of single-use protective materials, and growth in surgeries in APAC and MEA countries that have hospital building out programs run by their governments. Automotive grows alongside the growth of light vehicles as well as insulation requirements. Building and construction use nonwovens in roofing and house wrapping.

Key Market Segments

By Type

- Drylaid Chemical Bonding

- Wetlaid Chemical Bonding

- Foam Bonding and Spray Bonding

- Other Chemical Bonding Variants

By Material

- Polypropylene

- Polyester

- Polyethylene

- Rayon or Viscose

- Other fibers such as cotton or blends

By Application

- Hygiene Products

- Medical Products

- Filtration Media

- Automotive Interiors and Components

- Construction and Industrial Uses

By End Use

- Hygiene and Personal Care

- Medical and Healthcare

- Automotive

- Building and Construction

- Industrial and Household Products

Drivers

Hygiene & Disposable Products Surge

The most powerful structural engine for chemical bonded nonwovens in 2026 is the accelerating global demand for disposable personal hygiene products — baby diapers, adult incontinence pads, sanitary napkins, and wipes — where chemically bonded materials function as the primary acquisition-distribution layers (ADL), coverstock, and airlaid absorbent cores. The hygiene nonwoven segment is projected to grow at a CAGR of over 6% through 2028, and India’s nonwoven market alone generated USD 1.5 billion in 2024, on track for USD 2.3 billion by 2030 at a 7.6% CAGR, outpacing the broader textile industry.

APAC players such as Avgol Industries launched “Hygiene 360” sustainable product lines in 2025 while Spunweb India expanded installed capacity by approximately 53% with two new production lines, signaling a decisive supply buildout to match structural demand. The business model implication for converters is a shift toward high-volume contract structures where proprietary OEKO-TEX-compliant binder formulations — tuned for ultra-low skin-contact irritation and rapid liquid strike-through — command 15–25% premiums over commodity grades.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hygiene & Disposable Products Surge | +1.9% | APAC core (India, China, SE Asia), LATAM spill-over, MEA emerging | Medium term (2–4 yrs) |

| Healthcare & Medical Nonwoven Expansion | +1.5% | Global; North America & EU regulated, India fastest-growing APAC node | Short term (≤ 2 yrs) |

| Industrial Filtration & Air Quality Regulation | +1.2% | North America (EPA), EU (IED revisions), APAC industrial corridors | Medium term (2–4 yrs) |

| Infrastructure Boom & Geotextile Demand | +1.0% | APAC (India, China BRI), MEA, LATAM | Long term (≥ 4 yrs) |

| Sustainability Mandates & Bio-Based Binder Transition | +0.8% | EU regulatory core, North America secondary, APAC regulatory lag | Medium term (2–4 yrs) |

| Automotive Lightweighting & EV Acoustics | +0.6% | EU OEM hubs, North America, China EV corridors | Long term (≥ 4 yrs) |

Restraints

Tightening VOC & Chemical Emission Regulations

In the EU, REACH Regulation Amendment 2023/2055 and the EU’s broader plastics strategy mandate that from May 31, 2026, manufacturers and industrial downstream users of synthetic polymer microparticles (SPM) — a category that directly implicates certain binder chemistries used in nonwovens — must submit annual quantified emission reports to the European Chemicals Agency (ECHA); non-compliant entities face reputational exposure and potential market access restrictions, while compliance costs for mid-sized converters are estimated to add EUR 0.8–1.5 million annually in monitoring infrastructure, legal advisory, and process re-engineering.

The EU Packaging Regulation (EU) 2025/240 entering force in August 2026 further compresses the commercial space for binder-heavy nonwoven materials in packaging and single-use applications, mandating recyclability and recycled content thresholds that chemical bonded constructions typically cannot meet without reformulation. China’s domestic air quality standards — specifically the GB 3095-2012-derived textile air pollutant emission standards — impose organic HAP limits of 0.016 kg per kg of dyeing and finishing materials, a threshold that older, high-throughput chemical bonding lines exceed without secondary abatement systems costing USD 2–4 million per production line.

The aggregate compliance burden across jurisdictions is forcing capital reallocation away from expansion and toward remediation: manufacturers are diverting an estimated 15–22% of their annual CapEx budgets toward emission control systems, low-VOC binder reformulation, and regulatory reporting infrastructure, thereby delaying capacity additions and product innovation cycles by 18–30 months. This regulatory drag is modeled to suppress the segment’s CAGR by approximately -0.8 percentage points over the 2026–2030 horizon, with the sharpest impact falling on EU-based and China-based producers who face concurrent domestic enforcement alongside export-market compliance requirements.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Petrochemical Binder Price Volatility (PP, SB Latex, Acrylic) | -1.5% | Global — APAC, North America, EU core | Short term (≤ 2 years) |

| Tightening VOC & Chemical Emission Regulations | -0.8% | EU primary; North America, China secondary | Medium term (2–4 years) |

| Escalating Trade Tariffs & Protectionist Trade Barriers | -0.9% | North America–APAC corridors; India, China, EU | Short term (≤ 2 years) |

| APAC Low-Cost Overcapacity & Margin Compression | -0.7% | EU, North America (import-exposed); APAC domestic | Medium term (2–4 years) |

| Biodegradable & Alternative Bonding Technology Substitution | -0.6% | EU, North America; emerging APAC regulatory push | Long term (≥ 4 years) |

| Skilled Labor Shortages & High CapEx Barriers to Modernization | -0.5% | North America, EU, Emerging Markets | Medium term (2–4 years) |

Opportunity

Bio-Based & Sustainable Binder Platform

Chemical bonded sub-segment bio-binder penetration remains below 8% of total binder volume — implying an under-monetized TAM gap of ~USD 600–900 million by 2030. EU PPWR (applying August 12, 2026) and REACH SVHC restrictions (250 substances as of June 2025) create a captive reformulation demand window where bio-acrylic and PLA-compatible binders priced at 25–40% premiums over petroleum equivalents can be locked into exclusive 3–5 year converter supply agreements before the compliance window closes.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| Bio-Based & Sustainable Binder Platform | +1.8% | EU regulatory core, North America, India pilot markets | Short term (≤ 2 years) |

| EV Battery Separator TAM Entry | +1.5% | China EV corridors, North America (IRA-driven), EU (EUBBR) | Medium term (2–4 years) |

| Precision Agricultural Nonwovens in Emerging Markets | +1.2% | India, Sub-Saharan Africa, SE Asia (Indonesia, Vietnam) | Medium term (2–4 years) |

| Functionalized Smart Nonwoven Substrates | +1.0% | North America, EU (medtech), Japan, South Korea | Long term (≥ 4 years) |

| High-Efficiency Filtration Media Specification Upgrade | +0.8% | North America (EPA), EU (IED), APAC urban industrial | Medium term (2–4 years) |

| Fragmented Market Roll-Up & M&A Consolidation | +0.7% | India, ASEAN, Eastern Europe | Short–Medium term (1–4 years) |

Challenges

Binder Penetration & Web Uniformity Control

At standard production line speeds of 80–150 meters per minute, binder saturation via immersion, kiss-roll, or foam application systems produces coefficient-of-variation (CV%) metrics for add-on weight that routinely range from 4.5–8.0% even on well-maintained equipment, compared to a quality specification ceiling of ≤3.0% demanded by premium medical, filtration, and automotive OEM customers; this translates to defect reject rates of 6–12% of gross output for sub-premium converters, with waste-adjusted cost-per-square-meter rising by USD 0.04–0.12 depending on binder add-on rate and fiber substrate cost.

The challenge intensifies when processing heterogeneous fiber blends — such as polyester/rayon or PP/lyocell compositions — where differential fiber hydrophilicity creates localized binder pooling, dry-spot formation, and uneven bond strength distribution that causes inter-lot tensile strength variation of ±15–20% at the rolls level, making supply specifications adherence for medical wipes or high-loft automotive acoustics applications extremely difficult to guarantee.

At the machine engineering level, upgrading from legacy saturation systems to closed-loop gravimetric add-on control with inline NIR scanning — the current state-of-the-art that reduces add-on CV% to ≤1.8% — requires CapEx of USD 1.5–3.0 million per line for the sensor and control infrastructure alone, excluding line downtime during retrofit which averages 18–22 days per line; given that a typical chemical bonded nonwoven facility operates 3–6 production lines, the total investment burden of USD 4.5–18 million concentrated within a 3–5 year technology cycle represents a friction level that the majority of the industry’s regionally fragmented mid-size producers cannot absorb, sustaining a two-tier quality market that structurally limits premium segment penetration and suppresses the segment’s effective CAGR by approximately -1.1 percentage points.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Binder Penetration & Web Uniformity Control | -1.1% | Global — APAC, EU, North America | Long term (≥ 4 years) |

| Energy-Intensive Drying Oven Decarbonization | -0.8% | EU primary; North America, China secondary | Medium term (2–4 years) |

| Circular Economy & End-of-Life Recyclability Gap | -0.9% | EU regulatory core; North America, APAC | Long term (≥ 4 years) |

| Talent Scarcity in Process Chemistry & Engineering | -0.7% | North America, EU; emerging APAC manufacturing hubs | Medium term (2–4 years) |

| Digital Transformation & Process Intelligence Lag | -0.6% | Global — highest in APAC SME base | Medium term (2–4 years) |

| End-Use Market Concentration & Customer Dependency | -0.5% | Hygiene-heavy APAC; medical-heavy North America, EU | Short term (≤ 2 years) |

Geopolitical Impact Analysis

Geopolitical Trade Shifts Reshaping Chemical Bonded Nonwoven Supply Chains

Geopolitics is swiftly changing the landscape of global chemical trade, with increased tariffs, greater protectionism, and shifting political allegiances speeding up the restructuring of supply chains within key regions. In the chemical bonded nonwovens industry, US-China trade tension, which includes Section 301 tariffs of 25% applied to Chinese imports of nonwovens, is quickly facilitating the localization of production facilities in Vietnam, India, and Mexico for the benefit of customers from North America and Europe without the threat of tariff exposure. China’s pre-eminence as the producer of polypropylene fiber yarn poses the risk of future disruption to nonwovens producers worldwide.

EU’s Green Deal and CBAM, which becomes operational in 2026, will make it more expensive to ship nonwovens produced by high-emission economies into Europe, thus giving European producers producing sustainably priced benefits. In addition, India’s PLI program is supporting quick local growth, thus reducing import reliance until 2027. Cross-border commerce will become essential for diversifying supply chains and ensuring resilience, as the Middle East countries’ investments in healthcare infrastructure will create stable, government-supported demand for medical-grade nonwovens until 2035.

Regional Analysis

Asia Pacific Leads Global Nonwovens Production, While Developed Markets Focus on High-Value Applications

Asia Pacific is the leading region accounting for 40.1% of global revenues in 2025 due to China’s dominance as the leading producer of disposable hygiene nonwovens globally, rapid growth in the domestic hygiene industry in India, and exports-driven manufacturing activities in Southeast Asia. This region features large-scale drylaid chemical bonding operations operating at economies-of-scale levels. Rapidly growing Indian nonwoven industry, driven by PLI support, had the best regional growth.

Europe and North America are considered to be the mature, high-margin markets characterized by an emphasis on premium medical, automotive, and specialty filtration nonwovens, facilitated by robust regulations and vertical integration, featuring such players as Freudenberg, Ahlstrom, Berry Global, and Johns Manville. MIDDLE EAST AND AFRICA is witnessing a rapid evolution driven by investment in healthcare facilities and increasing hygiene practices. LATIN AMERICA is gradually evolving, with Brazil being at the forefront of disposable hygiene applications development.

Key Regions and Countries Covered

North America

- The US

- Canada

Europe

- Germany

- France

- The UK.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of Asia Pacific

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC Countries

- South Africa

- Rest of Middle East & Africa

Key Players Analysis

The global chemical bonded nonwoven market is characterized by moderately concentrated competition, with leading players including Berry Global, Freudenberg Performance Materials, Kimberly-Clark, Ahlstrom, and DuPont competing on the basis of economies of scale, technological leadership in binder innovation, diversified geographic manufacturing footprints, and deep application expertise across hygiene, medical, filtration, and automotive end markets.

Market leaders are actively pursuing sustainability-driven investments and geographic expansion across Asia Pacific to capture growing hygiene and medical industry demand. Competitive differentiation is increasingly defined by the ability to develop bio-based and low-emission binder systems, scale high-speed drylaid production lines in cost-competitive markets, and secure long-term supply agreements with major FMCG and healthcare institutional buyers.

The Major Players In The Market

- Berry Global Inc.

- Freudenberg Performance Materials

- Kimberly-Clark Corporation

- Ahlstrom

- Fitesa SA

- Glatfelter Corporation

- Johns Manville

- DuPont de Nemours Inc.

- Suominen Corporation

- Sandler AG

- TWE Group GmbH

- Avgol Nonwovens

- Toray Industries Inc.

- Lydall Inc.

- Fibertex Nonwovens A S

- Avgol Nonwovens

- Toray Industries Inc

- Other companies

Key Development

- March 2026, Berry Global Inc. launched an additional drylaid chemical bonding production line at its facility in Suzhou, China, with 35,000 metric tons of yearly capacity exclusively for high-end hygiene cover stock products in the Asia-Pacific region.

- February 2026, Freudenberg Performance Materials unveiled its innovative EVO-Bond Bio-Acrylate binder solution for use in medical-grade nonwovens in Europe, attaining EN 13795 surgical barrier standards with 40% reduced carbon emissions.

- January 2026, Kimberly-Clark Corporation invested US$ 180 million in a modern chemical-bonded nonwoven manufacturing plant in South Carolina to be operational by Q3 2027, focusing on filtration and premium hygiene applications.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 52.4 Billion |

| Forecast Revenue (2035) | USD 83.5 Billion |

| CAGR (2026-2035) | 4.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Drylaid Chemical Bonding, Wetlaid Chemical Bonding, Foam Bonding & Spray Bonding, Other Chemical Bonding Variants), By Material (Polypropylene, Polyester, Polyethylene, Rayon or Viscose, Other Fibers such as Cotton or Blends), By Application (Hygiene Products, Medical Products, Filtration Media, Automotive Interiors & Components, Construction & Industrial Uses), By End Use (Hygiene & Personal Care, Medical & Healthcare, Automotive, Building & Construction, Industrial & Household Products) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC – China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America – Brazil, Mexico & Rest of Latin America; Middle East & Africa – GCC, South Africa & Rest of MEA |

| Competitive Landscape | Berry Global Inc, Freudenberg Performance Materials, Kimberly-Clark Corporation, Ahlstrom, Fitesa S.A., Glatfelter Corporation, Johns Manville, DuPont de Nemours, Inc., Suominen Corporation, Sandler AG, TWE Group GmbH, Lydall Inc., Fibertex Nonwovens A/S, Avgol Nonwovens, Toray Industries, Inc., and Other Key Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |