Quick Navigation

Report Overview

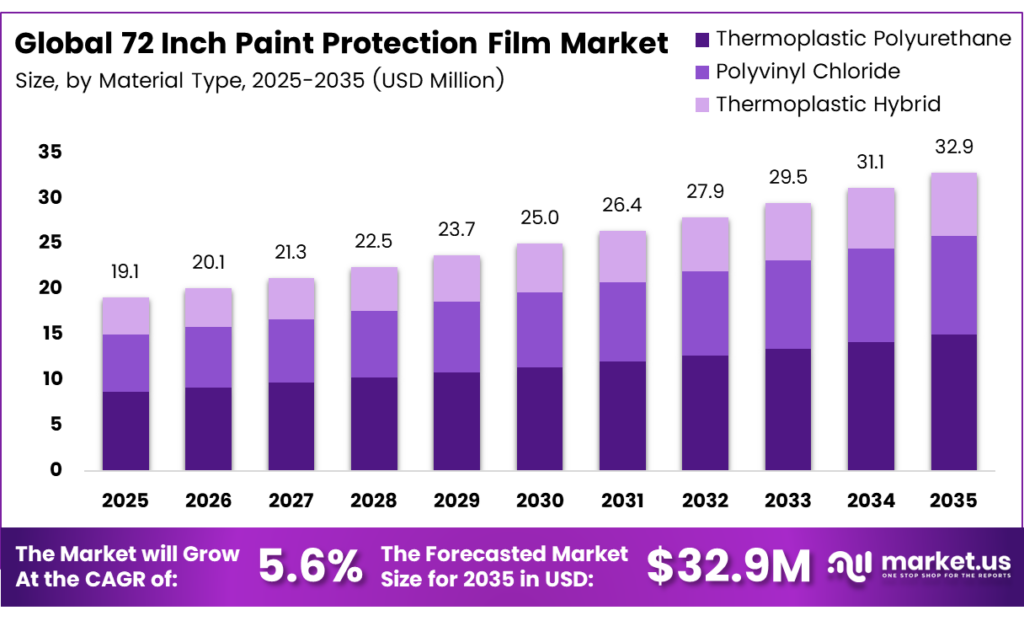

The Global 72 Inch Paint Protection Film Market size is expected to be worth around USD 32.9 million by 2035 from USD 19.1 million in 2025, growing at a CAGR of 5.6% during the forecast period 2026 to 2035.

The 72-inch paint protection film market covers extra-wide surface protection films designed to shield vehicle panels, aerospace components, and electronic surfaces from damage. These films deliver seamless coverage across large body panels such as hoods, roofs, and doors. Consequently, they reduce the need for visible seams that compromise both aesthetics and protection quality.

Self-healing paint protection film can reduce stone chips and abrasions to vehicle paint by up to 87%, based on independent laboratory testing of modern polyurethane films with self-healing topcoats. This capability provides measurable, quantifiable value to consumers and directly supports strong pricing power for premium 72-inch wide-format film products across both automotive and non-automotive end-use applications.

Thermoplastic polyurethane remains the dominant material in this market due to its outstanding flexibility, optical clarity, and long-term durability. Manufacturers increasingly prefer TPU over older alternatives such as PVC because it resists yellowing, cracking, and adhesive breakdown. Moreover, TPU films support advanced features like self-healing topcoats that respond to heat and minor abrasion.

Automotive applications drive the largest share of demand across this market segment. Vehicle owners, detailing studios, and OEM service networks install wide-format films on SUVs, electric vehicles, pickup trucks, and luxury sedans. Additionally, growing vehicle premiumization trends push consumers toward full-panel and full-body protection solutions.

Key Takeaways

- The Global 72 Inch Paint Protection Film Market is valued at USD 19.1 million in 2025 and is projected to reach USD 32.9 million by 2035 at a CAGR of 5.6% during the forecast period 2026 to 2035.

- Thermoplastic Polyurethane (TPU) holds the dominant position with a 76.3% market share in 2025.

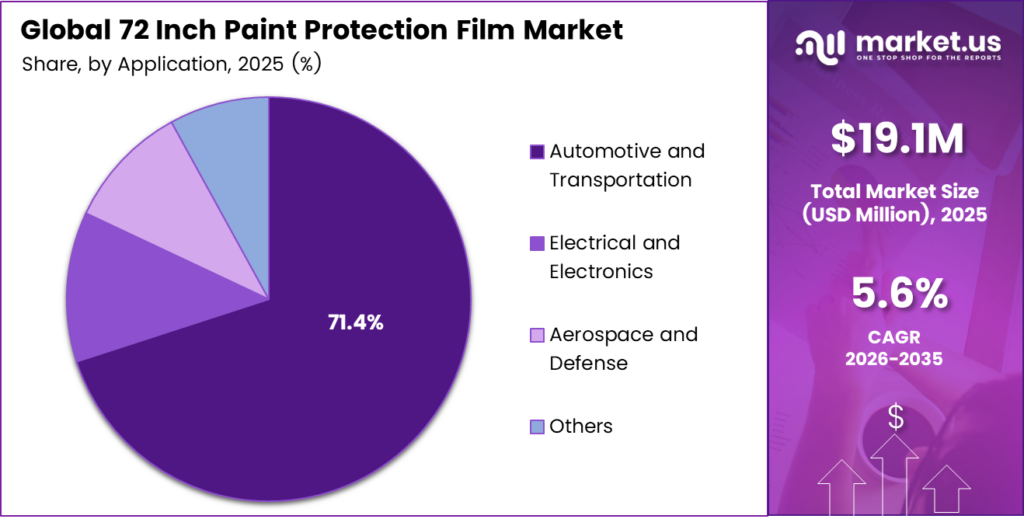

- Automotive and Transportation lead with a 71.4% market share in 2025.

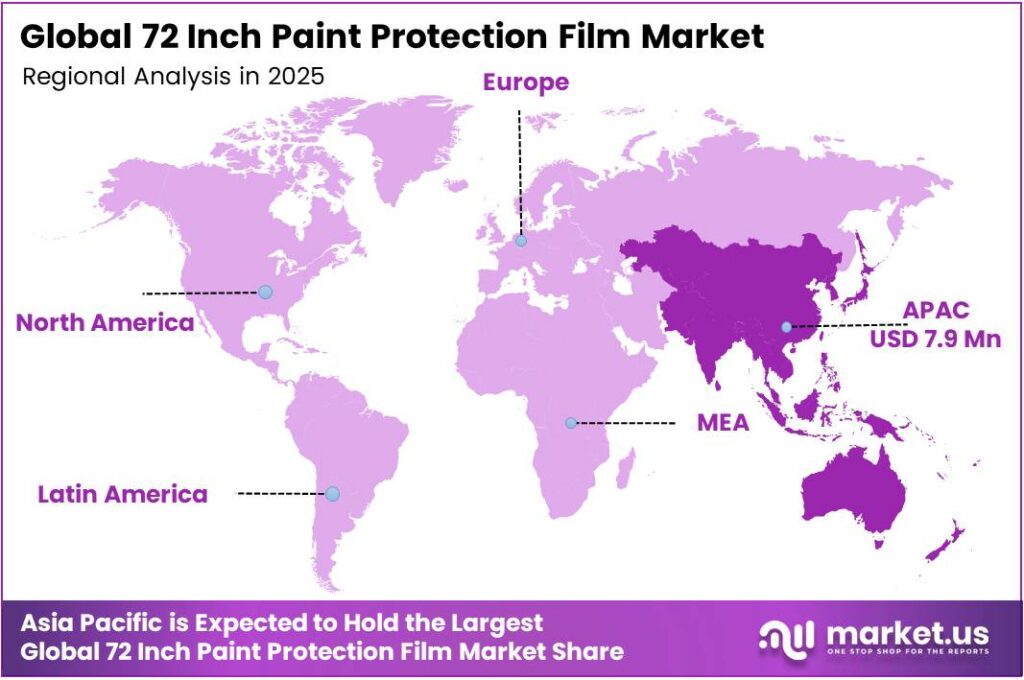

- Asia-Pacific dominates the regional landscape with a 41.1% market share, valued at USD 7.9 million in 2025.

By Material Type Analysis

Thermoplastic Polyurethane (TPU) dominates with 76.3% due to its superior clarity, flexibility, and self-healing performance.

In 2025, Thermoplastic Polyurethane (TPU) held a dominant market position in the By Material Type segment of the 72 Inch Paint Protection Film Market, with a 76.3% share. TPU films deliver outstanding optical clarity, high stretchability, and long-term resistance to yellowing. Moreover, their compatibility with self-healing topcoat technologies makes them the preferred choice for premium automotive and specialty surface protection applications.

Polyvinyl Chloride (PVC) films serve as a cost-effective alternative for budget-conscious buyers and entry-level applications. However, PVC materials remain prone to discoloration and reduced flexibility over extended use. Consequently, professional installers and OEM networks increasingly transition away from PVC toward higher-performing thermoplastic solutions that offer better long-term value and appearance retention.

Thermoplastic Hybrid (TPH) films occupy a middle-ground position between TPU and PVC in the material type segment. TPH formulations attempt to balance cost efficiency with improved performance characteristics compared to standard PVC. Additionally, manufacturers develop TPH products for applications where full TPU-grade performance is not required, helping broaden addressable market reach across price-sensitive customer segments.

By Application Type Analysis

Automotive and transportation dominate with 71.4% due to the rising demand for full-panel seamless vehicle surface protection.

In 2025, Automotive and Transportation held a dominant market position in the By Application Type segment of the 72 Inch Paint Protection Film Market, with a 71.4% share. SUVs, electric vehicles, luxury sedans, and pickup trucks drive the bulk of film installations. Moreover, expanding aftermarket detailing networks and OEM partnerships continue to accelerate the adoption of extra-wide format protection solutions across global automotive markets.

Electrical and Electronics applications represent a growing secondary demand stream for wide-format protective films. Manufacturers apply these films to protect sensitive device casings, display panels, and equipment housings from scratches and environmental exposure. Therefore, the electronics segment offers meaningful diversification potential as producers seek applications beyond traditional automotive surface protection markets.

Aerospace and Defense applications utilize high-performance protective films to shield aircraft surfaces, military vehicle panels, and structural components from abrasion and weather-related damage. These end-users demand films that meet strict performance and durability standards. Consequently, premium TPU wide-format films are increasingly gaining specification approvals within aerospace and defense procurement programs globally.

Key Market Segments

By Material Type

- Thermoplastic Polyurethane (TPU)

- Polyvinyl Chloride (PVC)

- Thermoplastic Hybrid (TPH)

By Application Type

- Automotive and Transportation

- Electrical and Electronics

- Aerospace and Defense

- Others

Emerging Trends

Matte, Satin, and Colored PPF Finishes Reshape Premium Vehicle Customization

Vehicle owners increasingly prefer satin, matte, and colored paint protection film finishes over traditional clear coatings. This shift reflects growing demand for personalization beyond basic surface protection. Self-healing PPF films recover up to 90% of their original surface appearance after minor scratches, making stylistic customization options more durable and commercially attractive to premium vehicle buyers.

Hydrophobic Nano-Topcoats and Mobile Installation Services Expand Market Reach

Manufacturers integrate hydrophobic, self-cleaning, and nano-topcoat layers into next-generation wide-format PPF products. These advanced surface properties enhance daily usability and reduce maintenance requirements for vehicle owners. Moreover, the rapid growth of mobile installation services and dedicated premium detailing studios significantly expands customer accessibility, making professional-grade protection available to a broader geographic and demographic audience.

Drivers

Rising Demand for Seamless Full-Panel Coverage Across SUVs, EVs, and Luxury Vehicles

Consumer demand for full-panel, seam-free protection across large vehicle surfaces drives strong adoption of 72-inch wide TPU films. SUV owners, EV manufacturers, and luxury vehicle buyers all prioritize flawless paint preservation. Premium PPF products use a film thickness of 6–8 mils, which optimally combines impact resistance with effective self-healing behavior, delivering measurable protection value that justifies premium pricing in competitive markets.

Consumer Focus on Resale Value and UV Protection Accelerates Premium PPF Adoption

Vehicle owners increasingly invest in scratch-, UV-, and stone-chip-resistant PPF solutions to preserve resale value over time. Self-healing PPF can reduce paint fading from UV exposure by up to 98%, thanks to UV-resistant topcoat formulations. Therefore, this performance benefit positions premium 72-inch paint protection films as a high-value, financially rational investment for both individual consumers and fleet operators.

Restraints

High Material and Installation Costs Limit Wider Mass-Market Penetration

Premium-grade 72-inch TPU paint protection films carry significantly higher material costs compared to standard, narrower films. Professional installation adds further expense, reducing accessibility for budget-conscious vehicle owners. Self-healing PPF carries a higher initial cost than traditional films but offers longer lifespans of about 7–10 years versus 5–7 years, which helps justify the investment but still limits immediate mass-market adoption.

Performance Variability and Installation Quality Challenges Undermine Consumer Confidence

Improper installation remains a significant barrier to consistent product performance across the 72-inch PPF market. Adhesive failure, edge lifting, and long-term yellowing in lower-quality film grades reduce consumer trust and repeat purchase rates. A 2025 guide from 3M India shows full-vehicle PPF installations range from INR 20,000 to INR 250,000, highlighting how wide cost variability creates market confusion and hesitation among prospective buyers.

Growth Factors

Commercial Fleet and Non-Automotive Surface Protection Applications Create New Revenue Streams

Strong untapped demand exists across commercial fleets, delivery vans, aerospace platforms, and medical equipment segments seeking large-surface seamless protection. These non-automotive applications represent substantial growth opportunities for wide-format PPF manufacturers. Vehicles fitted with self-healing PPF retain a showroom-finish appearance for up to 8 years, a durability claim that resonates strongly with fleet operators focused on total cost of ownership.

Asia-Pacific Premiumization and Eco-Friendly Innovation Drive Long-Term Market Expansion

Accelerating vehicle ownership and premiumization trends across Asia-Pacific and other emerging markets generate growing demand for high-quality surface protection solutions. Self-healing PPF functions through an elastomeric polyurethane top layer that relaxes and realigns at approximately 60°C, erasing minor scratches when exposed to heat. Moreover, innovation in eco-friendly TPU formulations and anti-contamination coatings positions the market for sustained expansion through the forecast period.

Regional Analysis

Asia-Pacific Dominates the 72 Inch Paint Protection Film Market with a Market Share of 41.1%, Valued at USD 7.9 Million

Asia-Pacific holds the leading position in the global 72 Inch Paint Protection Film Market, commanding a 41.1% share valued at USD 7.9 million in 2025. Rapid vehicle ownership growth, a thriving automotive aftermarket, and rising consumer spending on vehicle aesthetics drive this dominance. Moreover, strong manufacturing ecosystems in China, Japan, South Korea, and India support both local demand and export supply of wide-format PPF products.

North America represents a mature and high-value market for premium paint protection film solutions. Vehicle owners in the United States and Canada demonstrate a strong willingness to pay for professional-grade, full-panel protection on luxury vehicles, trucks, and SUVs. Additionally, a well-established network of certified detailing studios and OEM dealership programs supports consistent installation demand across the region.

Europe maintains steady demand for high-performance surface protection films, particularly in Germany, the UK, and France, where luxury vehicle ownership rates remain high. European consumers value long-term paint preservation and environmental durability. Consequently, manufacturers targeting this region focus on TPU-based, eco-compliant formulations that meet evolving regulatory standards while delivering premium optical clarity and self-healing performance.

Latin America presents an emerging opportunity for 72-inch paint protection film suppliers as vehicle ownership expands in Brazil and Mexico. Growing middle-class disposable income and increasing consumer awareness of paint preservation benefits support gradual market development. However, price sensitivity in the region continues to favor mid-range film solutions over ultra-premium TPU grades in the near term.

The Middle East and Africa region shows a growing appetite for premium automotive surface protection, particularly in GCC countries where luxury vehicle ownership rates are high. Extreme heat and UV exposure conditions in the region create strong functional demand for high-performance, UV-resistant protective films. Therefore, wide-format TPU products with superior heat tolerance and optical stability attract increasing interest from detailing professionals and vehicle owners alike.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

3M holds a prominent position in the global paint protection film market through its extensive product portfolio, deep OEM relationships, and established global distribution network. The company serves automotive, industrial, and aerospace end-users with a range of wide-format protective film solutions. Moreover, its strong brand recognition among professional detailing studios reinforces its authority in premium surface protection segments worldwide.

Eastman Chemical Company is a leading raw material and finished film supplier that brings deep polymer chemistry expertise to the paint protection film market. The company develops advanced TPU formulations that support self-healing, optical clarity, and long-term weather resistance. Additionally, Eastman’s integration across the supply chain gives it a competitive advantage in controlling film quality, consistency, and the development of next-generation protective solutions.

Schweitzer-Mauduit International, Inc. applies its materials science capabilities to deliver engineered surface protection films for demanding automotive and specialty applications. The company’s focus on high-performance film technologies positions it well within the growing premium segment of the wide-format paint protection film market. Consequently, its product development efforts align closely with evolving industry requirements for durability, aesthetics, and multi-surface application flexibility.

Avery Dennison leverages its global manufacturing infrastructure and pressure-sensitive materials expertise to serve both automotive OEM and aftermarket PPF segments effectively. The company offers a range of protective film solutions designed for large-panel coverage and professional installation environments. Furthermore, Avery Dennison’s ongoing investment in sustainable materials and adhesive innovation supports its long-term competitive positioning across key markets in North America, Europe, and Asia-Pacific.

Top Key Players in the Market

- 3M

- Eastman Chemical Company

- Schweitzer-Mauduit International, Inc.

- Avery Dennison

- XPEL Inc.

- RENOLIT SE

- Saint-Gobain S.A.

Recent Developments

- In 2025, 3M appears to be pushing its PPF offer in two practical directions: new product positioning and installer workflow tools. On the product side, 3M introduced 3M Protection Wrap Film Color Series, positioned as a single film that combines protection with styling and supports dry installation.

- In 2025, SWM, the most relevant current lens, is Mativ, the combined company. Mativ’s 2024 annual report explicitly says its advanced films portfolio includes paint protection films used in the transportation aftermarket channel. The same report says Mativ is planning investments in capacity and capabilities in release liners, specialty tapes, optical films, and health care for 2025.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 19.1 Million |

| Forecast Revenue (2035) | USD 32.9 Million |

| CAGR (2026-2035) | 5.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material Type (Thermoplastic Polyurethane (TPU), Polyvinyl Chloride (PVC), Thermoplastic Hybrid (TPH)), By Application Type (Automotive and Transportation, Electrical and Electronics, Aerospace and Defense, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | 3M, Eastman Chemical Company, Schweitzer-Mauduit International Inc., Avery Dennison, XPEL Inc., RENOLIT SE, Saint-Gobain S.A. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |