Quick Navigation

Report Overview

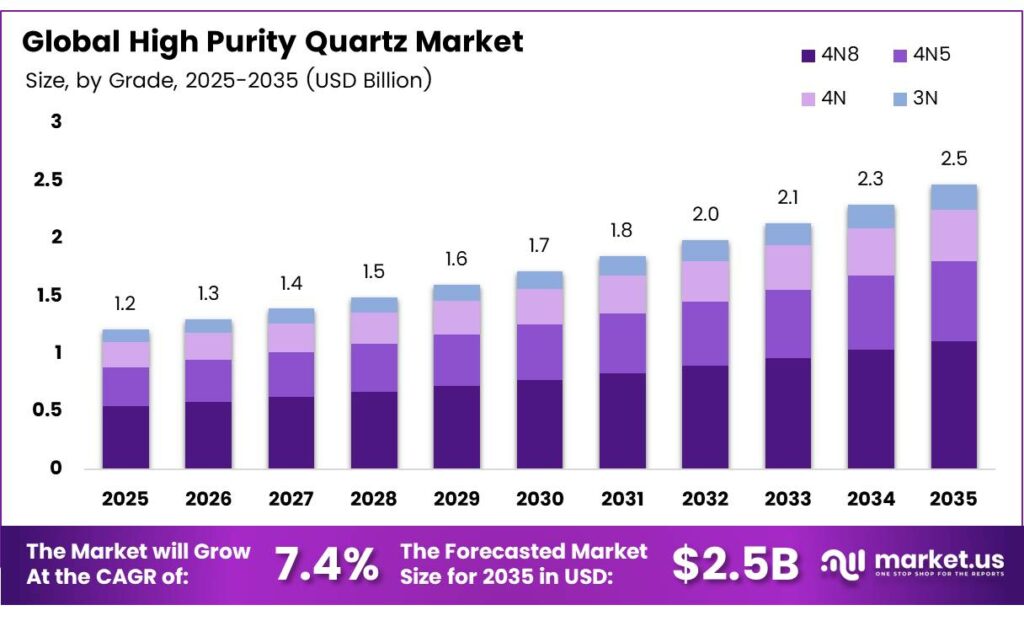

The Global High Purity Quartz Market size is expected to be worth around USD 2.5 billion by 2035 from USD 1.2 billion in 2025, growing at a CAGR of 7.4% during the forecast period 2026 to 2035.

High-purity quartz refers to silicon dioxide (SiO2) material refined to extremely low impurity levels. Industries such as semiconductors, solar photovoltaics, and advanced optics rely on this material. Manufacturers process natural quartz through multi-stage purification to meet strict grade specifications for critical applications.

Purification technology advances drive consistent quality improvements across the industry. High-purity quartz leaching purification using OL reagent achieved a 92.65% removal rate of impurity elements, resulting in a total impurity content of 16.98 μg/g and a product yield of 93% under optimized conditions in 2025. These results highlight how process innovation directly improves feedstock quality for end-use manufacturers.

Solar and semiconductor applications further validate the need for extreme purity standards. High-purity quartz crucibles used for Czochralski pullers in silicon PV ingot manufacturing are produced from natural quartz sand refined to 99.997% SiO2 purity, as of current industry practice. This standard reflects how demanding end-markets actively shape upstream quality requirements.

Regulatory frameworks around critical minerals increasingly classify high-purity quartz as a strategic material. The United States, European Union, and several Asia-Pacific governments now include it in critical mineral lists. Therefore, policy support for exploration, processing, and stockpiling continues to grow steadily.

Key Takeaways

- The Global High Purity Quartz Market is valued at USD 1.2 billion in 2025 and is projected to reach USD 2.5 The 4N segment holds a dominant share of 38.9% in 2025.

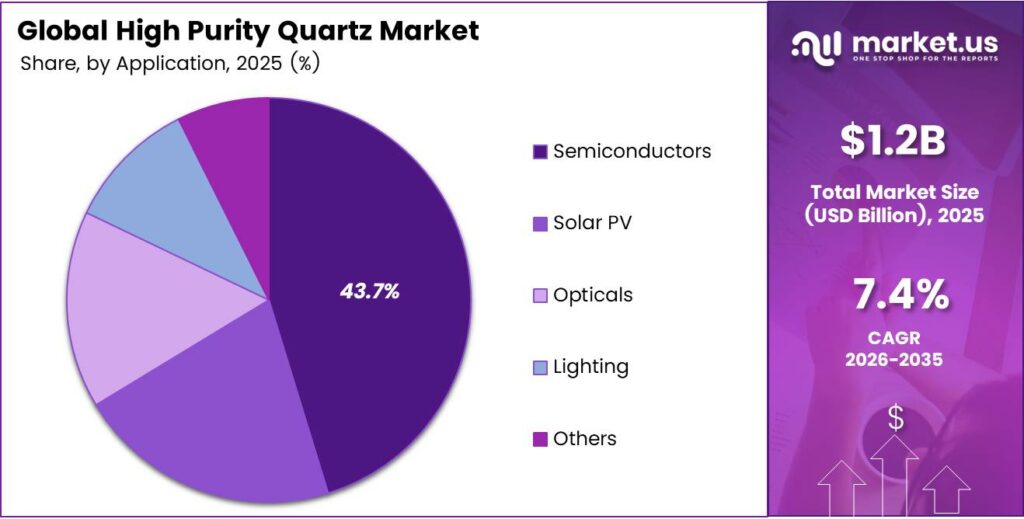

- The Semiconductors segment leads with a 43.7% market share in 2025.

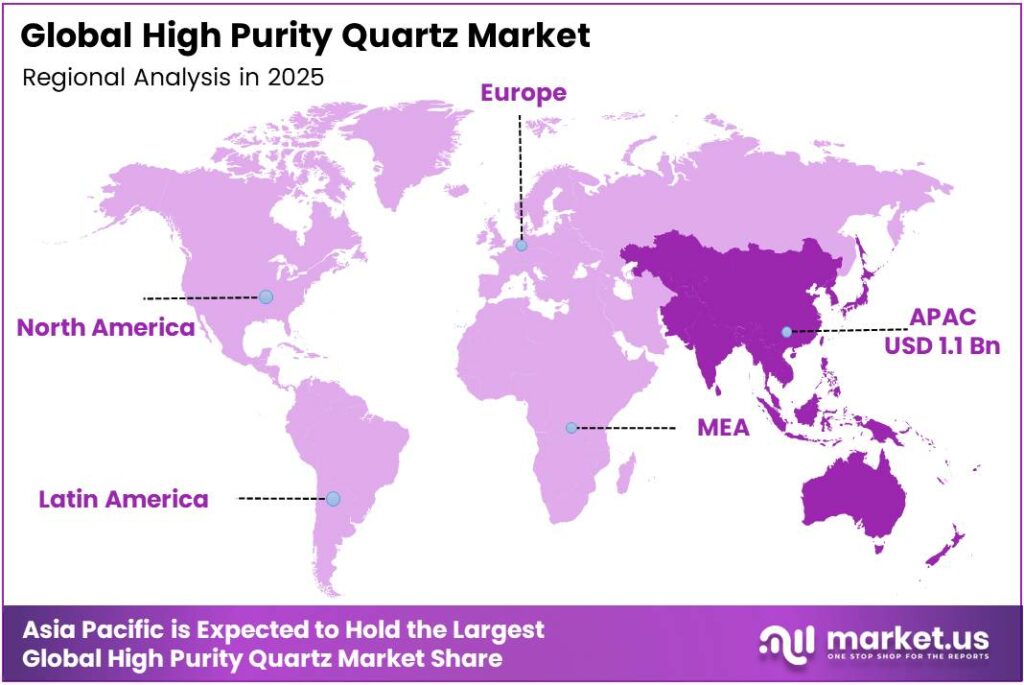

- Asia-Pacific dominates the global market with a 49.6% share, valued at USD 1.1 billion in 2025.

By Grade Analysis

4N dominates with 38.9% due to its widespread use in semiconductor and solar photovoltaic applications.

In 2025, the 4N segment held a dominant market position in the By Grade segment of the High Purity Quartz Market, with a 38.9% share. This grade meets the purity threshold required by both semiconductor manufacturers and solar crucible producers. Moreover, its balance of cost-efficiency and performance drives strong, consistent adoption across advanced manufacturing sectors globally.

4N8 represents the ultra-premium tier of the high-purity quartz market. Manufacturers targeting extreme-purity applications such as advanced lithography and high-power optics rely on this grade. However, its higher processing cost and limited natural deposit availability restrict broader adoption, keeping its market share smaller compared to the dominant 4N grade.

4N5 serves applications that demand purity levels between standard 4N and ultra-high 4N8 specifications. Optical fiber production and precision instrument manufacturing commonly use this grade. Additionally, its growing role in photonics and specialty lighting systems positions it as an emerging grade segment with steady demand growth through the forecast period.

By Application Analysis

Semiconductors dominate with 43.7% due to the intensive use of high-purity quartz in wafer fabrication equipment and crucibles.

In 2025, the Semiconductors segment held a dominant market position in the By Application segment of the High Purity Quartz Market, with a 43.7% share. Wafer fabrication facilities consume large volumes of quartz tubes, crucibles, and components. Furthermore, increasing chip complexity and miniaturization drive demand for even higher purity grades, reinforcing this segment’s leading market position through the forecast period.

The Solar PV segment represents the second largest and fastest-growing application area. Czochralski silicon ingot production for photovoltaic cells requires high-grade quartz crucibles at scale. Moreover, expanding renewable energy targets globally continues to increase solar panel manufacturing capacity, directly translating into higher demand for high-purity quartz feedstock across all major producing regions.

The Opticals segment serves precision lens, prism, and window manufacturing for scientific, defense, and industrial uses. High-purity fused quartz provides excellent transmission across ultraviolet to infrared spectra. Additionally, growth in extreme-ultraviolet lithography systems for advanced chip manufacturing creates new premium demand within this application category that supports above-average pricing.

Key Market Segments

By Grade

- 4N8

- 4N5

- 4N

- 3N

By Application

- Semiconductors

- Solar PV

- Opticals

- Lighting

- Others

Emerging Trends

AI-Driven Miniaturization Raises Purity Demand Standards

Artificial intelligence chip architectures require progressively finer semiconductor nodes. These advanced designs demand quartz components with purity levels exceeding conventional specifications. Mixed-acid hot-pressure leaching in 2025 significantly increased quartz purity by efficiently removing metal contaminants, mica, and feldspar, enabling feedstock suitable for next-generation applications. Therefore, purification innovation directly supports this trend.

Sustainable Mining and Supply Sovereignty Shape Industry Direction

Global manufacturers increasingly adopt circular-economy approaches in quartz processing to reduce waste and energy consumption. Trade-aligned policies now treat high-purity quartz as a strategic mineral, prompting governments to prioritize domestic sourcing. Consequently, supply chain localization accelerates across North America and Europe, reshaping procurement strategies and encouraging long-term supplier partnerships for reliable feedstock access.

Drivers

Semiconductor and Solar Demand Accelerates High-Purity Quartz Consumption

Next-generation semiconductor wafer fabrication and memory chip production demand ultra-high purity quartz components at scale. Solar photovoltaic ingot crucible manufacturing similarly consumes large volumes of refined quartz. using a bubble-free layer in high-purity quartz crucibles limited iron contamination while maintaining quartz purity levels above 99.999% in semiconductor-grade Czochralski silicon systems during confirming critical performance requirements.

5G Networks and Government Onshoring Policies Expand Market Base

Rapid expansion of 5G infrastructure and high-bandwidth optical fiber networks creates sustained demand for precision quartz components. Advanced Ceramic Composites data confirms fused quartz used in wafer-processing equipment exhibits a thermal expansion coefficient around 0.54 × 10⁻⁶/K and purity above 99.99% SiO2, enabling low-defect manufacturing. Moreover, government-backed critical mineral onshoring initiatives in North America and Europe expand domestic processing investment.

Restraints

Natural Deposit Scarcity Limits Global Raw Material Supply

Ultra-pure quartz deposits meeting commercial-grade specifications occur in very few locations worldwide. Geological scarcity restricts the volume of raw material available for processing, creating persistent supply pressure. Additionally, exploration and qualification of new deposits requires years of testing and investment, which means supply cannot easily expand to meet sudden increases in market demand.

High Processing Costs Create Barriers to Market Entry and Scaling

Advanced extraction, multi-stage purification, and rigorous quality-control processes require significant capital investment. Operational costs for maintaining cleanroom-grade processing environments add further financial pressure on producers. Consequently, smaller operators face difficulty competing with established producers who benefit from economies of scale, limiting the number of viable market participants and constraining overall supply chain flexibility.

Growth Factors

Purification Technology Breakthroughs Improve Cost Efficiency at Scale

Hybrid bioleaching and microwave-assisted purification technologies offer significant cost reduction potential for high-purity quartz producers. These innovations reduce chemical usage and energy consumption while improving yield. High-purity quartz demand for solar PV crucibles caused average HPQ prices to rise from under USD 10/kg to over USD 20/kg between 2021 and 2023, highlighting the economic value that efficient purification technologies now deliver.

Emerging Markets and Advanced Applications Expand Addressable Demand

Rapid urbanization and electronics manufacturing growth across Southeast Asia, India, and Latin America create new demand centers for high-purity quartz. Czochralski silicon found that thicker bubble-free high-purity quartz crucible layers improved thermal conductivity and reduced Fe and Al dissolution into the melt, advancing performance benchmarks. Expanding applications in extreme-ultraviolet lithography and high-power lasers add premium demand segments.

Regional Analysis

Asia-Pacific Dominates the High Purity Quartz Market with a Market Share of 49.6%, Valued at USD 1.1 Billion

Asia-Pacific leads the global high-purity quartz market with a 49.6% share, valued at USD 1.1 billion in 2025. China drives this dominance through its massive semiconductor and solar PV manufacturing base. Japan and South Korea contribute a significant demand through advanced electronics production. Moreover, government investments in domestic quartz processing capacity across the region continue to reinforce Asia-Pacific’s leading position through the forecast period.

North America represents a high-growth regional market driven by semiconductor onshoring initiatives and critical mineral policy support. The United States government actively funds domestic quartz supply chain development through the CHIPS Act and related programs. Additionally, growing demand from defense optics, advanced lithography, and renewable energy installations sustains strong regional consumption of premium-grade quartz materials.

Europe maintains a strategically important position in the global high-purity quartz market. Germany, the UK, and Scandinavia anchor regional demand through precision engineering, optical manufacturing, and solar energy expansion. Furthermore, the European Union’s Critical Raw Materials Act formally designates high-purity quartz as strategic, prompting investment in regional supply chain resilience and driving growth in domestic processing capacity.

The Middle East and Africa region presents emerging opportunities driven by industrialization and energy transition investments. Gulf Cooperation Council countries expand solar energy installations, creating new downstream demand for quartz crucibles. However, limited domestic processing infrastructure and reliance on imported refined quartz currently constrain regional market development, requiring substantial investment to build competitive local supply capabilities.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Australian Silica Quartz Group Ltd operates as a prominent raw material supplier focused on high-purity silica extraction across Australian mineral-rich regions. The company targets semiconductor and solar PV end markets with its refined quartz products. Moreover, its strategic position in the Asia-Pacific supply chain makes it a key feedstock partner for manufacturers requiring consistent, high-grade quartz material at an industrial scale.

Creswick Quartz Pty Ltd specializes in the production of high-purity quartz sand and related processed materials. The company serves both domestic Australian customers and international export markets across Asia and Europe. Additionally, its focus on developing premium-grade quartz grades positions it competitively as global demand for higher purity specifications continues to expand across semiconductor, solar, and optical application segments.

HPQ Materials focuses on developing advanced quartz purification technologies and specialty quartz-derived materials. The company pursues innovation-led growth through proprietary processing methods that improve purity levels and yield efficiency. Consequently, its technology development approach differentiates it from conventional mining-focused suppliers and positions it as a solutions provider for manufacturers seeking cost-effective access to ultra-high purity quartz feedstock.

Imerys brings global mineral processing expertise to the high-purity quartz market through its diversified industrial minerals portfolio. The company operates processing facilities across multiple continents, supplying refined quartz products to semiconductor, optical, and specialty industrial customers. Furthermore, its established distribution network, deep technical expertise, and long-standing customer relationships provide a durable competitive foundation across all major regional markets.

Top Key Players in the Market

- Australian Silica Quartz Group Ltd

- Creswick Quartz Pty Ltd

- HPQ Materials

- Imerys

- Jiangsu Pacific Quartz Co., Ltd

- Momentive Technologies

- Nordic Mining ASA

- Russian Quartz LLC

- Sibelco

- The Quartz Corporation

Recent Developments

- In 2025, Australian Silica Quartz Group Ltd is focused on critical minerals, including quartz projects in Queensland. Its key recent activity in the high-purity quartz/silica sector (or closely related metallurgical-grade silicon quartz for polysilicon production) centers on the Quartz Hill project.

- In 2025, Creswick Quartz Pty Ltd’s public information will be available from the company or government websites. The company is noted in some technical contexts as holding high-purity quartz feedstock (>99.99% SiO₂) in historic gold mining tailings north of Ballarat, Victoria, which reportedly requires only water washing for silicon production suitability.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.2 Billion |

| Forecast Revenue (2035) | USD 2.5 Billion |

| CAGR (2026-2035) | 7.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Grade (4N8, 4N5, 4N, 3N), By Application (Semiconductors, Solar PV, Opticals, Lighting, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Australian Silica Quartz Group Ltd, Creswick Quartz Pty Ltd, HPQ Materials, Imerys, Jiangsu Pacific Quartz Co., Ltd, Momentive Technologies, Nordic Mining ASA, Russian Quartz LLC, Sibelco, The Quartz Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |