Quick Navigation

Report Overview

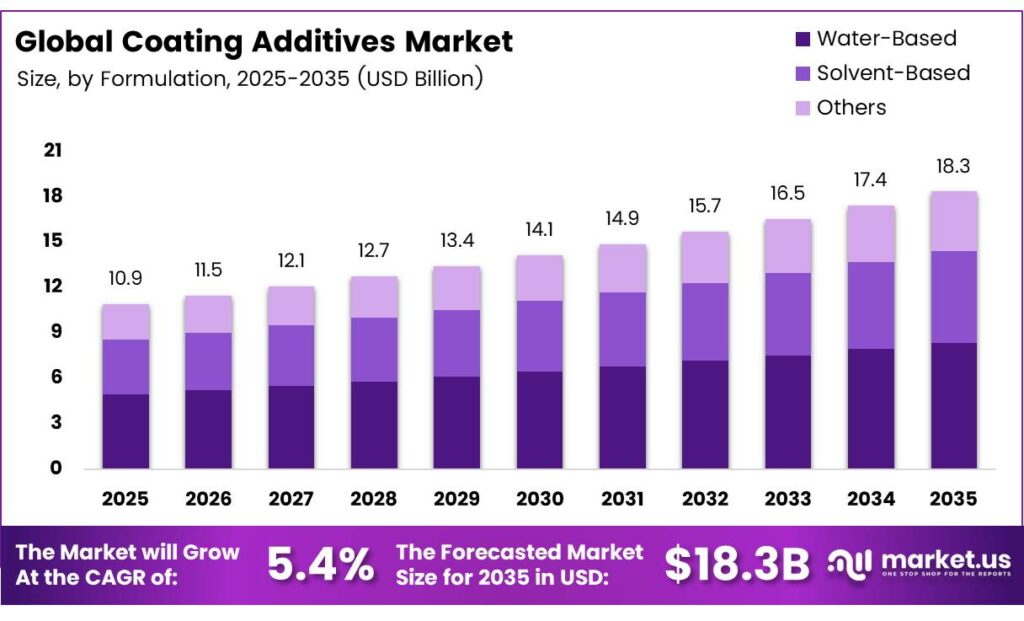

The Global Coating Additives Market size is expected to be worth around USD 18.3 billion by 2035 from USD 10.9 billion in 2025, growing at a CAGR of 5.4% during the forecast period 2026 to 2035.

Coating additives are specialty chemicals that manufacturers incorporate into paint and coating formulations to enhance specific performance properties. These substances improve surface finish, durability, application behavior, and environmental compliance across architectural, automotive, industrial, and marine coatings. Consequently, they represent a critical ingredient in modern coatings chemistry.

The RSC journal Sustainable Chemistry and Engineering, activation with zeolite-based materials in a coating system, reduced total VOC content by 89% compared with an untreated control, measured via GC-MS. This finding highlights the transformative role that advanced additive chemistries play in enabling coatings manufacturers to meet increasingly stringent environmental standards worldwide.

Growth opportunities continue to emerge across electronics, EV battery thermal management, and smart industrial coating systems. Demand for functional additives that deliver self-healing, anti-corrosion, and sensor-compatible surface performance is accelerating. Furthermore, the expansion of digital formulation platforms and AI-assisted additive selection is helping manufacturers shorten development cycles and improve product consistency at scale.

Key Takeaways

- The Global Coating Additives Market is valued at USD 10.9 billion in 2025 and is projected to reach USD 18.3 billion by 2035 at a CAGR of 5.4% during the forecast period 2026 to 2035.

- Thickeners dominate the market with a 38.9% share in 2025.

- Water-Based coatings hold the leading position with a 52.8% market share.

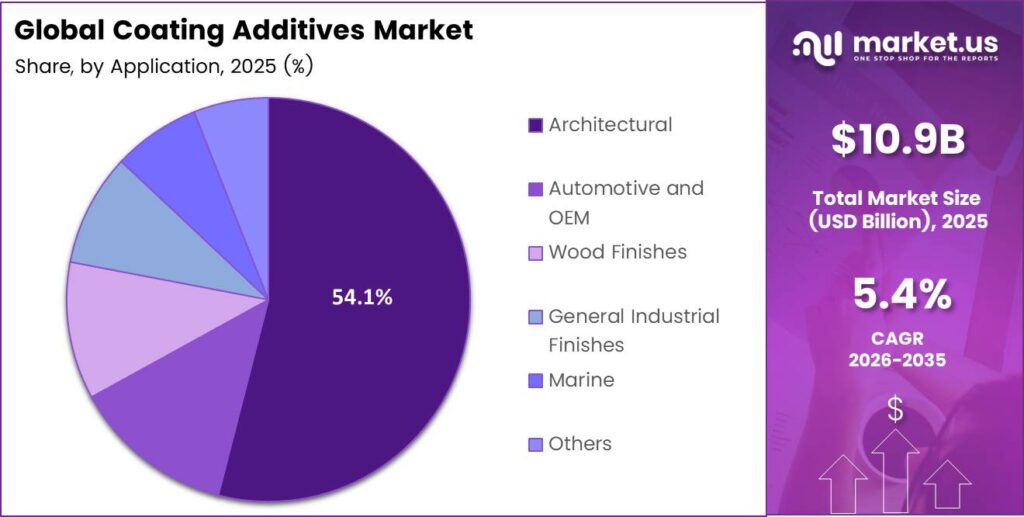

- The Architectural segment leads with a 54.1% share of the total market.

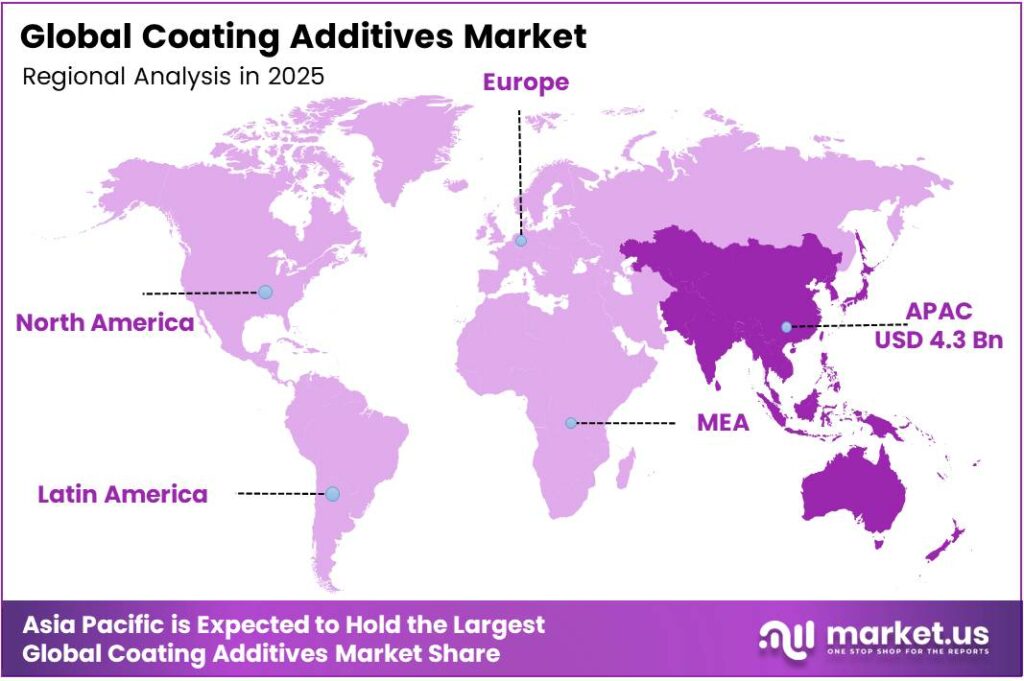

- Asia Pacific is the dominant region, accounting for 39.7% of the global market, valued at USD 4.3 billion.

By Additive Type Analysis

Thickeners dominate with 38.9% due to their essential role in controlling coating viscosity and application stability across all major end-use segments.

In 2025, Thickeners held a dominant market position in the By Additive segment of the Coating Additives Market, with a 38.9% share. Thickeners provide critical viscosity control in architectural and industrial coatings, ensuring stable application, reduced sagging, and consistent film build. Their compatibility with both water-based and solvent-based systems makes them the most universally demanded additive category.

Defoamers represent a high-volume additive category supporting virtually every coating system that involves mechanical mixing or spray application. These compounds suppress and eliminate foam generated during manufacturing and application. Moreover, defoamers are especially critical in water-based coatings, where surfactant activity creates persistent foaming challenges that directly affect film quality.

Dispersants enable uniform pigment distribution within coating formulations, preventing flocculation and settling during storage and application. Their role is particularly significant in high-pigment-load architectural and industrial systems. Additionally, advanced polymeric dispersants improve color strength and gloss while reducing the total pigment required per liter of coating produced.

By Formulation Analysis

Water-Based formulations dominate with 52.8% due to regulatory pressure for low-VOC coatings and strong adoption across architectural and industrial applications.

In 2025, Water-Based formulations held a dominant market position in the By Formulation segment of the Coating Additives Market, with a 52.8% share. Environmental regulations across North America, Europe, and the Asia Pacific increasingly restrict solvent use in coatings, driving formulators toward water-based platforms. Additives for these systems must address stability, film formation, and rheology under aqueous conditions.

Solvent-Based coatings continue to serve demanding industrial, marine, and automotive OEM applications where superior chemical resistance and film hardness are required. These systems rely on high-performance additives for wetting, leveling, and anti-sag properties. However, tightening VOC regulations in key markets are gradually shifting formulators toward hybrid and reduced-solvent alternatives.

Others, including powder coatings and UV-curable systems, represent a fast-growing formulation segment requiring specialized additive packages. Powder coatings eliminate solvent entirely, demanding flow control and degassing additives optimized for melt-phase processing. Additionally, UV and electron-beam curable systems need photoinitiator-compatible wetting and surface-slip additives to meet precision finish requirements.

By Application Analysis

Architectural coatings dominate with 54.1% due to consistently high global demand for interior and exterior decorative paints across residential and commercial construction.

In 2025, Architectural coatings held a dominant market position in the By Application segment of the Coating Additives Market, with a 54.1% share. Residential and commercial construction activity worldwide sustains a strong demand for interior and exterior paints. Coating additives in this segment focus on open-time extension, scrub resistance, stain blocking, and mildew prevention to meet consumer expectations.

Automotive and OEM coatings represent a high-value application segment that demands precise additive performance in primer, basecoat, and clearcoat layers. Wetting agents, leveling aids, and anti-cratering additives are essential for a defect-free surface finish. Moreover, EV platform growth is expanding demand for additives supporting both conventional and battery-pack thermal coating systems.

Wood Finishes require additive packages that balance penetration, open time, and surface gloss while maintaining compatibility with both water-based and solvent-based lacquer systems. Anti-blocking and slip additives are especially important for furniture and flooring applications. Additionally, market growth in premium wood coatings for interior design drives demand for specialty matting and soft-touch surface additives.

Key Market Segments

By Additive Type

- Thickeners

- Defoamers

- Dispersants

- Opacifiers

- Others

By Formulation

- Water-Based

- Solvent-Based

- Others

By Application

- Architectural

- Automotive and OEM

- Wood Finishes

- General Industrial Finishes

- Marine

- Others

Emerging Trends

Nano-Structured Additives and Smart Surface Technologies Gain Momentum

The coating additives market shows a clear shift toward nano-structured additive chemistries that deliver superior barrier performance, mechanical reinforcement, and optical transparency. Manufacturers increasingly adopt matte, soft-touch, and anti-fingerprint additive packages to meet consumer expectations in premium electronics and household goods. UV and EB curing technology adoption in coil-coating lines can reduce energy consumption by at least 60% compared with conventional thermal curing, signaling a transformative move across the coatings value chain.

AI-Driven Formulation and Robotic Application Reshape Product Development

Coating formulators increasingly use digital platforms and AI-assisted additive selection tools to accelerate development workflows and improve first-pass formulation success. Simultaneously, the rising deployment of high-speed robotic spray lines drives demand for tailor-made rheology packages optimized for automated application. Consequently, additive suppliers now develop purpose-built solutions for specific spray equipment configurations rather than universal rheology modifiers.

Drivers

Protective Coatings Demand and Automotive OEM Requirements Fuel Additive Consumption

Rapid expansion of infrastructure rehabilitation projects across bridges, marine assets, and energy equipment drives strong demand for high-performance protective coating additives. In the same period, rising automotive OEM and refinish coating volumes require advanced wetting, leveling, and surface defect-control solutions.

Alternative VOC-mitigation treatments achieved 78% VOC reduction using heated-air purging and 73% using PEG extraction, demonstrating the active role additive innovation plays in environmental compliance across the automotive coatings sector.

Powder Coating Growth and Multi-Functional Additive Demand Strengthen Market Momentum

Consumer appliance, furniture, and industrial metal finishing industries accelerate the adoption of powder coatings, creating new demand for specialized additive packages addressing flow, degassing, and surface leveling in melt-phase systems. Moreover, manufacturers increasingly require multi-functional additives that simultaneously improve scratch resistance, anti-blocking behavior, gloss retention, and process efficiency. This performance consolidation trend reduces formulation complexity and lowers the total cost of ownership for coating producers.

Restraints

Raw Material Price Volatility Disrupts Additive Formulation Economics

Persistent price instability in specialty monomers, silicones, wax derivatives, and performance minerals directly impacts additive manufacturing costs and margin stability. Suppliers struggle to pass cost increases to end customers under long-term supply contracts. Consequently, raw material price swings reduce investment confidence in new capacity expansion and limit the speed of innovation across the coating additives value chain.

Long Qualification Timelines Slow Commercial Adoption of New Additive Chemistries

Complex reformulation cycles and extended customer qualification processes create significant delays between additive development and revenue generation. Coatings manufacturers require thorough performance validation before switching established additive suppliers, particularly in regulated end markets such as automotive OEM and marine. Therefore, new entrants and innovative additive chemistries face long commercialization lead times that limit overall market agility.

Growth Factors

Energy-Curable and EV-Related Coating Applications Open New Additive Markets

Emerging demand for additives tailored to UV-curable, electron-beam, and energy-curable coating technologies creates new growth avenues in electronics and flexible packaging. A technical paper referencing an EU Horizon 2020 low-temperature-cure powder coating project estimates that converting to low-temperature polyester and HAA systems can deliver 40 to 70% energy savings in the curing step.

Smart Industrial Coatings and Next-Generation Functional Additives Expand Market Scope

Fast-growing demand for functional additives in EV battery thermal management and dielectric coatings represents a high-value opportunity for specialty chemistry suppliers. Arkema published a coatings case study confirming that UV and electron-beam curing technology adoption in coil-coating production lines can reduce energy consumption by at least 60% relative to conventional thermal curing, based on direct feedback from coil-coating industry operators and end users.

Regional Analysis

Asia Pacific Dominates the Coating Additives Market with a Market Share of 39.7%, Valued at USD 4.3 Billion

Asia Pacific leads the global coating additives market with a 39.7% share, valued at USD 4.3 billion in 2025. China, India, Japan, and South Korea drive this dominance through massive architectural construction activity, expanding automotive production, and rapid growth in consumer electronics manufacturing. Moreover, government infrastructure investment programs across the region sustain consistently high demand for both decorative and industrial coating systems that require specialty additive solutions.

North America maintains a strong market position supported by well-established automotive OEM, aerospace, and industrial coating industries. Stringent EPA and state-level VOC regulations accelerate the adoption of water-based formulations and low-emission additive packages. Additionally, active infrastructure renewal programs funded by federal legislation stimulate demand for high-performance protective coatings across bridges, pipelines, and public facilities.

Europe represents a mature but innovation-driven coating additives market shaped by rigorous EU REACH and VOC Directive compliance requirements. Formulators in Germany, France, and the UK prioritize sustainable chemistry, including bio-based and low-toxicity additive alternatives. Furthermore, the region’s strong automotive and industrial manufacturing base sustains demand for precision surface additives across premium-quality coating systems.

Latin America presents a developing but growing market for coating additives, led by Brazil and Mexico’s construction and automotive sectors. Urbanization trends and rising middle-class consumer demand support growth in decorative architectural coatings. However, economic volatility and currency fluctuations in key markets occasionally moderate investment in premium coating formulations and specialty additive adoption across the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BASF SE stands as a global leader in coating additives, offering a comprehensive portfolio that spans rheology modifiers, wetting agents, defoamers, and dispersants across water-based and solvent-based systems. The company serves architectural, automotive, and industrial coating markets worldwide. Moreover, BASF’s continuous investment in sustainable chemistry and bio-based additive innovation positions it strongly as low-VOC formulation demands accelerate globally.

Altana AG, through its specialty chemicals divisions, supplies high-performance surface additives, matting agents, and wax-based solutions to coatings formulators across Europe, North America, and the Asia Pacific. The company focuses on premium additive performance for automotive refinish, wood, and industrial coating applications. Additionally, Altana’s investment in effect pigments and functional surface modifiers broadens its value proposition in decorative and protective coating markets.

DOW Inc. develops a broad range of coating additive technologies, including rheology modifiers, coalescent agents, and biocide solutions, serving water-based architectural and industrial formulators. DOW’s global manufacturing and technical service network supports customers across all major regions. Furthermore, the company’s active research into sustainable raw material platforms aligns with the industry’s transition toward lower-emission and higher-performance coating formulations.

Nouryon specializes in surface chemistry and performance additives for architectural, industrial, and protective coatings, offering wetting, dispersing, and anti-settling solutions for complex formulation requirements. The company’s strong focus on customer-specific technical collaboration supports successful additive adoption in demanding applications. Additionally, Nouryon’s commitment to sustainable chemistry development makes it a preferred partner for formulators targeting low-VOC and bio-based coating compliance.

Top Key Players in the Market

- BASF SE

- Altana AG

- DOW Inc.

- Nouryon

- Evonik Industries AG

- Arkema

- Eastman Chemical Company

- Ashland Inc.

- Clariant AG

- The Lubrizol Corporation

Recent Developments

- In 2025, BASF’s relevance here sits mainly in its Dispersions & Resins business, which says its portfolio includes a broad range of additives for coatings, including defoamers, dispersing agents, film-forming agents, rheology modifiers, wetting agents, and surface modifiers. BASF also says this division holds a top-three market position in more than 80% of its strategic business areas.

- In 2025, Dow’s exposure comes through Performance Materials & Coatings, especially the Coatings & Performance Monomers business. In its SEC-filed annual report, Dow says this business makes critical ingredients and additives that improve paints and coatings, including dispersants, opacifiers, surfactants, protective and functional coatings, and rheology modifiers.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 10.9 Billion |

| Forecast Revenue (2035) | USD 18.3 Billion |

| CAGR (2026-2035) | 5.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Additive Type (Thickeners, Defoamers, Dispersants, Opacifiers, Others), By Formulation (Water-Based, Solvent-Based, Others), By Application (Architectural, Automotive and OEM, Wood Finishes, General Industrial Finishes, Marine, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | BASF SE, Altana AG, DOW Inc., Nouryon, Evonik Industries AG, Arkema, Eastman Chemical Company, Ashland Inc., Clariant AG, The Lubrizol Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |