Quick Navigation

Report Overview

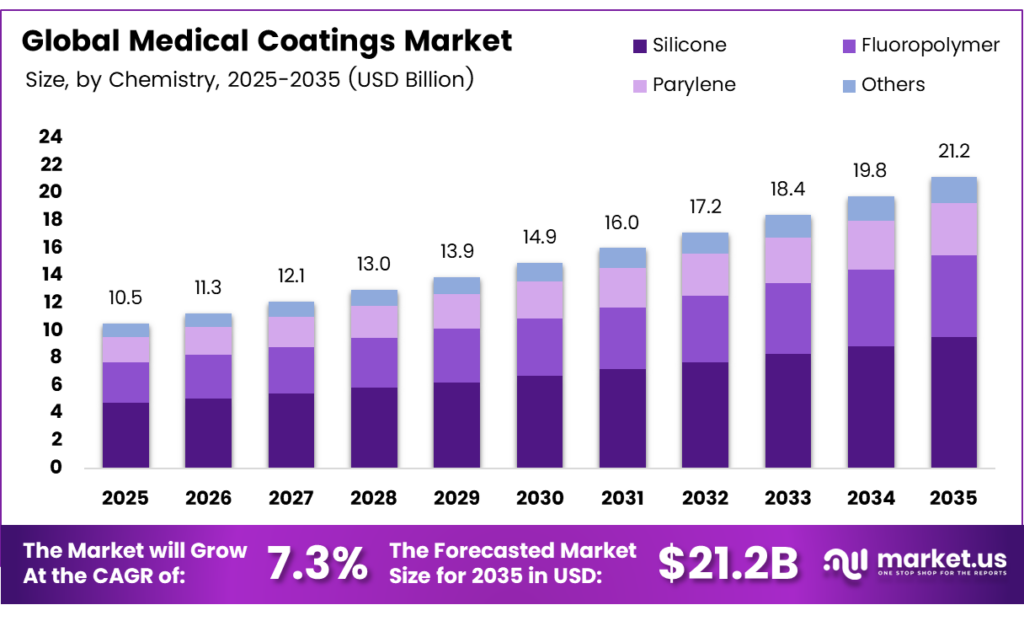

The Global Medical Coatings Market size is expected to be worth around USD 21.2 billion by 2035 from USD 10.5 billion in 2025, growing at a CAGR of 7.3% during the forecast period 2026 to 2035.

The medical coatings market covers specialized surface treatments applied to medical devices, implants, and surgical tools. These coatings improve device performance by adding properties such as antimicrobial protection, lubricity, and biocompatibility. Consequently, healthcare providers rely on coated devices to improve patient outcomes and reduce procedure-related risks.

Antimicrobial coatings are among the most critical product categories in this market. Chlorhexidine/silver sulfadiazine-coated catheters reduced catheter-related bloodstream infection (CRBSI) rates by approximately 40% compared with standard uncoated catheters. This finding highlights the strong clinical value of antimicrobial surface treatments in reducing hospital-acquired infections.

Hydrophilic coatings also demonstrate measurable clinical benefits. Frontiers in Cellular and Infection Microbiology, an Ag-alloy hydrogel-coated urinary catheter achieved a 47% reduction in the catheter-associated urinary tract infection (CAUTI) rate compared with a standard comparator. These results reinforce growing clinical confidence in advanced lubricious and antimicrobial coating solutions for urinary care applications.

Key Takeaways

- The Global Medical Coatings Market is valued at USD 10.5 billion in 2025 and is projected to reach USD 21.2 billion by 2035 at a CAGR of 7.3% during the forecast period 2026 to 2035.

- Silicone holds the dominant position with a 32.5% market share in 2025.

- Antimicrobial coatings lead with a 32.4% share in 2025.

- Dip and Spray holds the largest share at 37.8% in 2025.

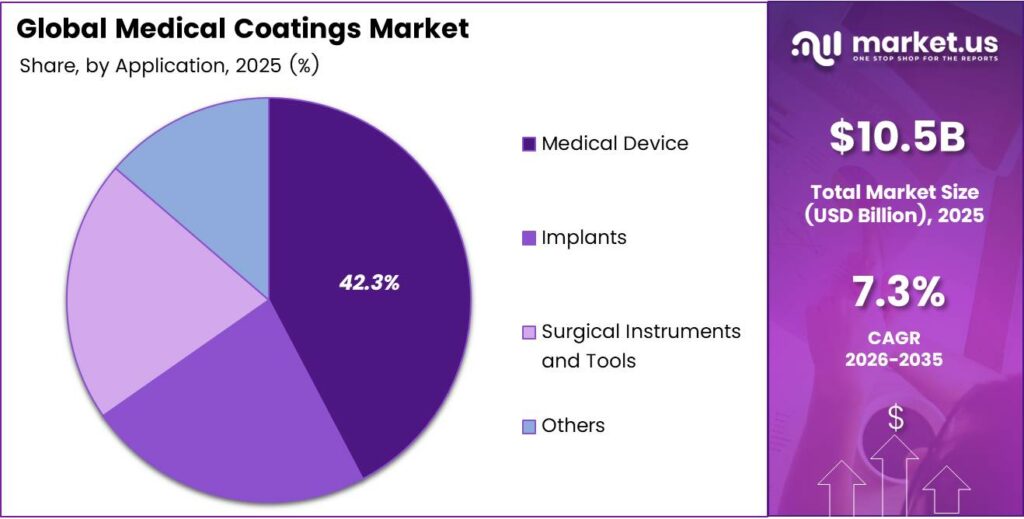

- Medical Device is the dominant segment with a 42.3% share in 2025.

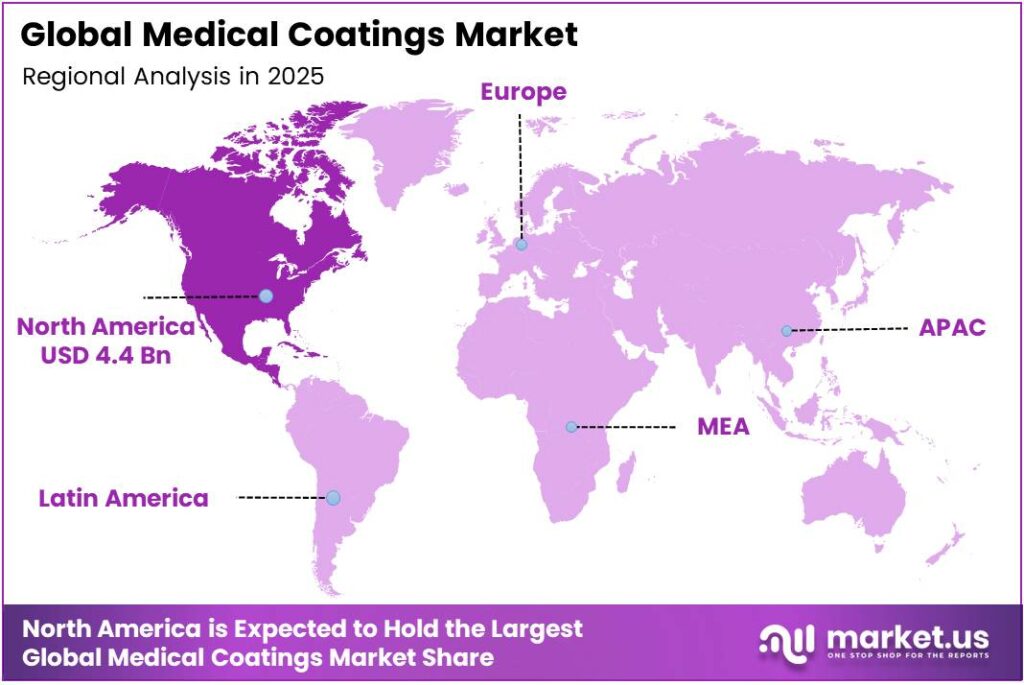

- North America dominates the regional landscape with a 41.9% share, valued at USD 4.4 billion in 2025.

By Chemistry Analysis

Silicone dominates with 32.5% due to its superior biocompatibility and versatility across medical device applications.

In 2025, Silicone held a dominant market position in the By Chemistry segment of the Medical Coatings Market, with a 32.5% share. Silicone coatings offer exceptional biocompatibility, flexibility, and chemical resistance. Moreover, they perform reliably across a wide range of medical devices, including catheters and implants, making them the preferred chemistry choice for device manufacturers globally.

Fluoropolymer coatings serve applications that require low friction and high chemical resistance. These coatings are widely applied on guidewires and surgical tools where non-stick and lubricious properties are critical. Additionally, fluoropolymers demonstrate excellent thermal stability, which supports their adoption in devices exposed to sterilization processes during clinical use.

By Coating Function Type Analysis

Antimicrobial coatings dominate with 32.4% due to rising infection control demands across healthcare facilities.

In 2025, Antimicrobial coatings held a dominant market position in the By Coating Function Type segment of the Medical Coatings Market, with a 32.4% share. Healthcare facilities increasingly demand infection-resistant surfaces on catheters, implants, and surgical tools. Therefore, antimicrobial coatings using silver, chlorhexidine, and other agents have become essential for reducing device-associated infections in clinical settings.

Hydrophilic/Lubricious coatings improve device navigation through anatomical pathways by significantly reducing surface friction. These coatings are critical for catheters and endoscopes, where smooth insertion reduces patient discomfort and procedural risk. Moreover, hydrophilic coatings absorb water to activate their lubricating properties, providing consistent performance during minimally invasive procedures.

By Deposition Technology Analysis

Dip and Spray dominates with 37.8% due to its cost-effectiveness and compatibility with high-volume device production.

In 2025, Dip and Spray held a dominant market position in the By Deposition Technology segment of the Medical Coatings Market, with a 37.8% share. This method allows manufacturers to coat large batches of devices efficiently and at lower costs. Moreover, dip and spray processes are compatible with a wide variety of coating chemistries, making them highly versatile across different medical device types.

Chemical Vapor Deposition (CVD) enables the deposition of highly uniform, thin-film coatings on complex device geometries. CVD is particularly suited for parylene and silicon-based coatings where precise thickness control is required. Additionally, this technology produces pinhole-free coatings, which is critical for implantable electronics and devices requiring complete surface coverage and barrier protection.

By Application Analysis

Medical Device dominates with 42.3% due to the broad base of coated devices used across clinical settings globally.

In 2025, Medical Device held a dominant market position in the By Application segment of the Medical Coatings Market, with a 42.3% share. Catheters, diagnostic equipment, and drug delivery devices constitute a large portion of coated medical products. Therefore, the high volume and diversity of medical devices requiring protective and functional surface treatments drive consistent demand across this application category.

Implants represent a high-value application segment where coating performance directly affects patient safety and device longevity. Orthopedic, cardiovascular, and dental implants require biocompatible and anti-thrombogenic coatings to function safely within the body. Moreover, the growing volume of implant surgeries driven by aging populations continues to expand demand for high-performance implant coating solutions worldwide.

Surgical Instruments and Tools utilize coatings primarily to reduce friction, prevent corrosion, and maintain sterility during procedures. Lubricious and antimicrobial coatings improve instrument handling and reduce cross-contamination risks in operating rooms. Additionally, coated surgical instruments require less frequent replacement, which supports cost efficiency for hospitals and surgical centers managing large instrument inventories.

Key Market Segments

By Chemistry

- Silicone

- Fluoropolymer

- Parylene

- Others

By Coating Function Type

- Antimicrobial

- Hydrophilic/Lubricious

- Anti-thrombogenic/Hemocompatible

- Others

By Deposition Technology

- Dip and Spray

- Chemical Vapor Deposition (CVD)

- Plasma Spray

- Others

By Application

- Medical Device

- Implants

- Surgical Instruments and Tools

- Others

Emerging Trends

Multifunctional Coatings Gain Ground in Medical Device Development

Medical device manufacturers are shifting toward multifunctional coatings that combine antimicrobial, lubricious, and biocompatible properties in a single surface treatment. This approach reduces manufacturing complexity while improving device performance. Moreover, plasma and UV-curable coating technologies are gaining adoption for their precision application capabilities and faster processing speeds across high-volume production environments.

Surface Modification and Collaborative Innovation Drive Coating Advancements

Advanced surface modification techniques are improving device longevity and functional safety in clinical settings. Coating providers and medical device manufacturers are forming strategic collaborations to accelerate the development of next-generation solutions. Antimicrobial-coated catheters showed an odds ratio of 0.64 for CRBSIs per 1,000 catheter-days, demonstrating a measurable clinical impact that is driving wider adoption of surface-modified devices.

Drivers

Infection Control Demands and Antimicrobial Coating Adoption Accelerate Market Growth

Healthcare institutions are actively seeking infection-resistant medical devices to reduce hospital-acquired infection rates. Antimicrobial coatings on catheters, implants, and surgical tools directly address this clinical priority. Lubricant-impregnated catheter coatings reduced sliding friction during urethral insertion by more than 50% compared with uncoated catheters, demonstrating measurable performance improvements that support broader clinical adoption.

Minimally Invasive Procedures and Aging Population Fuel Device Coating Demand

Increasing adoption of minimally invasive surgical techniques requires devices with superior lubricious and biocompatible coatings for safe navigation through anatomical pathways. Additionally, the global aging population is driving higher utilization of implantable and catheter-based devices. Consequently, coating manufacturers are investing in advanced biocompatible and hydrophilic solutions to meet rising clinical performance requirements from device developers worldwide.

Restraints

Regulatory Complexity Slows Approval of New Medical Coating Materials

Stringent regulatory approval processes present a significant barrier for coating manufacturers seeking market entry. Regulatory bodies require extensive biocompatibility, toxicology, and clinical performance testing before approving new coating materials for medical use. Moreover, approval timelines can extend across multiple years, delaying the commercialization of innovative coating technologies and limiting manufacturers’ ability to respond quickly to evolving clinical needs.

High Development Costs Limit Accessibility of Specialized Medical Coatings

Research, development, and application of specialized medical coatings involve substantial financial investment. Smaller manufacturers and emerging-market healthcare providers often struggle to absorb these costs. Additionally, CR-BSI rates decreased from 3.3 to 2.1 per 1,000 catheter-days after introducing coated catheters, reinforcing clinical value but also underscoring the need for cost-effective coating adoption pathways for broader healthcare access.

Growth Factors

Smart Coatings and Nanotechnology Open New Therapeutic Opportunities

Drug-eluting and smart coatings are expanding the therapeutic potential of medical devices by enabling controlled, targeted drug release from device surfaces. Nanotechnology integration further enhances the functional properties of these coatings, improving durability and biological interaction. The field of antimicrobial medical device coatings expanded nearly 30-fold over 20 years, confirming sustained and accelerating innovation across this technology domain.

Emerging Markets and Sustainability Trends Broaden the Growth Horizon

Improving healthcare infrastructure in emerging economies across Asia, Africa, and Latin America is creating significant untapped demand for medical coatings. Additionally, device manufacturers are facing growing pressure to adopt eco-friendly and sustainable coating formulations that reduce environmental impact. Therefore, coating providers that develop green chemistry solutions will gain a competitive advantage while addressing both regulatory sustainability mandates and evolving customer procurement requirements.

Regional Analysis

North America Dominates the Medical Coatings Market with a Market Share of 41.9%, Valued at USD 4.4 Billion

North America leads the global medical coatings market with a 41.9% share, valued at USD 4.4 billion in 2025. The region benefits from a highly developed healthcare infrastructure, a large base of medical device manufacturers, and strong regulatory frameworks that drive the adoption of advanced surface treatment technologies. Moreover, high procedural volumes and significant investment in infection control solutions sustain market leadership across the United States and Canada.

Europe holds a significant position in the medical coatings market, supported by a robust medical device manufacturing sector in Germany, France, and the United Kingdom. Stringent EU regulations on biocompatibility and device safety encourage the adoption of high-performance coating materials. Additionally, growing demand for minimally invasive procedures and long-term implants continues to drive coating innovation across the region.

Asia Pacific represents the fastest-growing region in the medical coatings market, driven by rapidly expanding healthcare infrastructure in China, India, and South Korea. Rising medical device production capacity and growing domestic patient populations are accelerating demand for specialized coating solutions. Furthermore, government investments in healthcare modernization programs are creating favorable conditions for medical coating providers to expand their regional presence.

The Middle East and Africa region is experiencing steady growth in medical coatings adoption, supported by increasing healthcare spending and rising awareness of infection control in clinical settings. GCC countries are investing in advanced hospital infrastructure, which is creating new demand for coated medical devices. However, limited local manufacturing capacity and import dependency remain challenges for broader market penetration across this region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

AST Products, Inc. is a specialized provider of surface treatment and coating solutions for medical devices, with a focus on hydrophilic and lubricious coatings. The company serves catheter and guidewire manufacturers seeking reliable coating partnerships. Moreover, AST Products has built a strong reputation for custom coating development, enabling device makers to meet specific clinical and regulatory performance requirements for diverse applications.

Axalta Coating Systems brings extensive expertise in high-performance coatings across multiple industries, including medical applications. The company leverages its advanced chemistry capabilities to develop durable, biocompatible surface treatments for medical devices. Additionally, Axalta’s global manufacturing network and strong R&D infrastructure position it well to serve medical device clients requiring consistent quality and regulatory-compliant coating formulations across international markets.

Biocoat, Inc. specializes exclusively in hydrophilic coating technologies for the medical device industry. The company provides coating services and materials that improve device lubricity and biocompatibility for catheters, guidewires, and endoscopes. Furthermore, Biocoat’s focused expertise and regulatory knowledge make it a trusted partner for device manufacturers navigating complex FDA and international approval requirements for coated medical product development.

Covalon Technologies Ltd. develops advanced medical coating and wound care solutions with a strong emphasis on antimicrobial and infection-prevention applications. The company’s proprietary coating technologies address critical clinical challenges in catheter-related and wound-associated infections. Covalon has established partnerships with healthcare systems seeking evidence-based coating solutions that improve patient safety and reduce the clinical and economic burden of hospital-acquired infections.

Top Key Players in the Market

- AST Products, Inc.

- Axalta Coating Systems

- Biocoat, Inc.

- Covalon Technologies Ltd.

- Freudenberg Medical

- Harland Medical Systems

- Hydromer, Inc.

- Medicoat AG

- Merit Medical Systems

- Momentive Performance Materials

- PPG Industries

- Precision Coating Co.

Recent Developments

- In 2025, Biocoat announced the formation of Surmodics Services & Technologies, following merger and divestiture transactions. This is a major change in how the business is being organized and presented to customers in hydrophilic coatings.

- In 2025, Covalon announced publication of a peer-reviewed clinical study on VALGuard Line Guard, reporting a significant reduction in CLABSIs at a pediatric hospital. Covalon’s later fiscal 2025 release again highlighted that publication as a landmark milestone.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 10.5 Billion |

| Forecast Revenue (2035) | USD 21.2 Billion |

| CAGR (2026-2035) | 7.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Chemistry (Silicone, Fluoropolymer, Parylene, Others), By Coating Function Type (Antimicrobial, Hydrophilic/Lubricious, Anti-thrombogenic/Hemocompatible, Others), By Deposition Technology (Dip and Spray, Chemical Vapor Deposition (CVD), Plasma Spray, Others), By Application (Medical Device, Implants, Surgical Instruments and Tools, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | AST Products, Inc., Axalta Coating Systems, Biocoat, Inc., Covalon Technologies Ltd., Freudenberg Medical, Harland Medical Systems, Hydromer, Inc., Medicoat AG, Merit Medical Systems, Momentive Performance Materials, PPG Industries, Precision Coating Co. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |