Quick Navigation

Report Overview

The Orthopedic Devices Market Size is expected to be worth around US$ 96.4 billion by 2034 from US$ 62.7 billion in 2024, growing at a CAGR of 4.4% during the forecast period 2025 to 2034.

Growing demand for orthopedic devices has increased due to the rising prevalence of musculoskeletal disorders, sports injuries, and joint degeneration. The need for advanced implants, prosthetics, and fixation devices continues to grow as more individuals require surgical interventions for mobility restoration. According to research from the American Academy of Pediatrics and the National SAFE KIDS Campaign, over 3.5 million children under 14 sustain sports or recreation-related injuries annually, with more than 775,000 requiring emergency medical treatment.

Technological advancements in 3D printing and biomaterials have improved the precision and durability of implants, enhancing patient outcomes. Minimally invasive orthopedic procedures and robotic-assisted surgeries have gained traction, reducing recovery times and improving surgical accuracy. Increasing awareness of injury prevention has expanded the market for bracing and support systems.

Healthcare providers incorporate regenerative medicine and biologics to accelerate bone healing and cartilage repair. Artificial intelligence and data analytics enhance preoperative planning and personalized treatment approaches. Manufacturers focus on cost-effective and durable implant designs to improve accessibility. As orthopedic conditions rise, innovation in device technology and surgical techniques will continue shaping the future of orthopedic care.

Key Takeaways

- In 2024, the market for Orthopedic Devices generated a revenue of US$ 62.7 billion, with a CAGR of 4.4%, and is expected to reach US$ 96.4 billion by the year 2033.

- The product type segment is divided into joint replacement/ orthopedic implants, trauma , sports medicine , orthobiologics, and others, with joint replacement/ orthopedic implants taking the lead in 2024 with a market share of 40.8%.

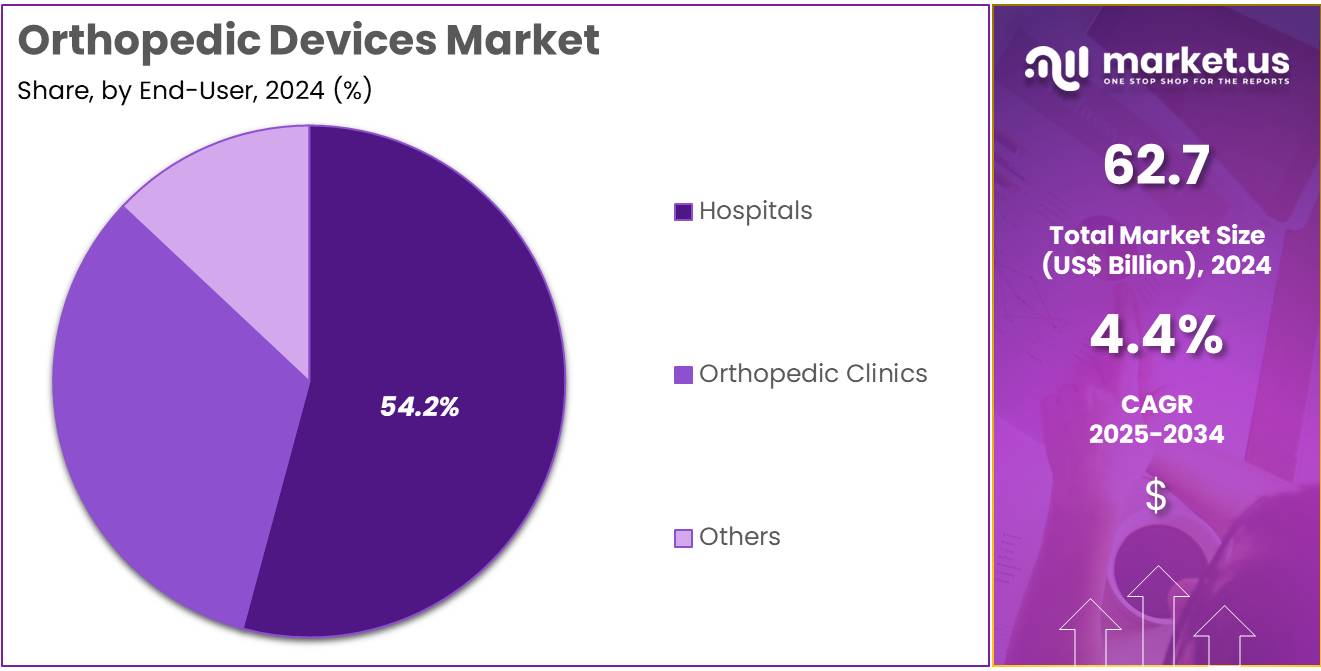

- Considering end-user, the market is divided into hospitals, orthopedic clinics, and others. Among these, hospitals held a significant share of 54.2%.

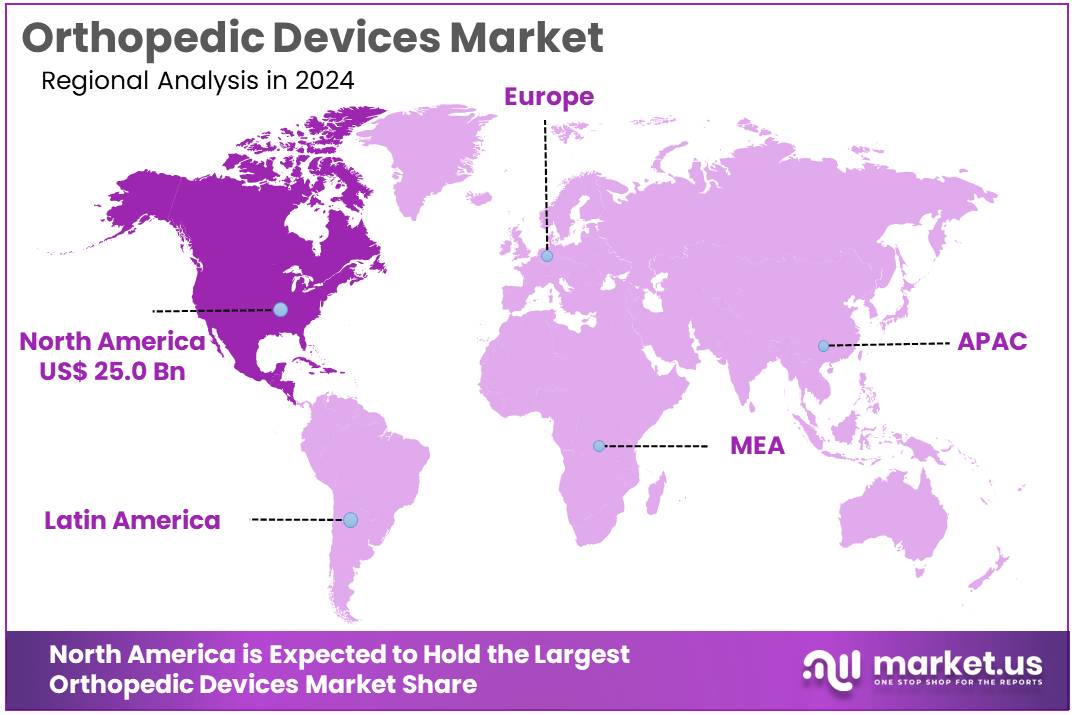

- North America led the market by securing a market share of 39.8% in 2024.

Product Type Analysis

The joint replacement/ orthopedic implants segment led in 2024, claiming a market share of 40.8% owing to the increasing prevalence of age-related musculoskeletal disorders, such as arthritis, and the rising demand for minimally invasive procedures. As the global population ages, the need for joint replacement surgeries is anticipated to grow, with orthopedic implants providing effective solutions for patients suffering from joint pain and limited mobility.

Technological advancements in materials, surgical techniques, and implant designs are likely to further drive the segment’s growth, offering enhanced durability, reduced recovery times, and improved patient outcomes. Additionally, the growing awareness of joint health and the expansion of healthcare infrastructure in emerging markets are expected to support the continued growth of the joint replacement/orthopedic implants segment.

End-user Analysis

The hospitals held a significant share of 54.2% due to the increasing number of orthopedic procedures being performed in hospital settings. Hospitals are expected to remain the primary healthcare providers for orthopedic surgeries, including joint replacements and trauma treatments, due to their ability to offer advanced surgical facilities and post-operative care.

The demand for orthopedic devices in hospitals is likely to be fueled by the rising incidence of musculoskeletal conditions, such as fractures, osteoarthritis, and sports-related injuries. Furthermore, advancements in minimally invasive surgery and robotic-assisted techniques are expected to further enhance the appeal of hospital-based orthopedic procedures, contributing to the growth of the hospitals segment in the orthopedic devices market.

Key Market Segments

By Product Type

- Joint Replacement/ Orthopedic Implants

- Lower Extremity Implants

-

-

- Foot & Ankle Implants

- Hip Implants

- Knee Implants

- Spinal Implants

- Dental

- Dental Implants

- Craniomaxillofacial Implants

- Upper Extremity Implants

- Shoulder Implants

- Hand & Wrist Implants

- Elbow Implants

-

- Trauma

- Implants

- Accessories

- Instruments

- Sports Medicine

- Body Reconstruction & Repair

- Body Support & Recovery

- Body Monitoring & Evaluation

- Accessories

- Orthobiologics

- Viscosupplementation

- Synthetic Bone Substitutes

- Stem Cell Therapy

- Demineralized Bone Matrix

- Bone Morphogenetic Protein (BMP)

- Allograft

- Others

By End-user

- Hospitals

- Orthopedic Clinics

- Others

Drivers

Rise in Global Geriatric Population Driving the Orthopedic Devices Market

Rising life expectancy and an aging population are anticipated to drive the orthopedic devices market due to an increased prevalence of age-related bone and joint disorders. An October 2024 report from the World Health Organization projects a significant rise in the global elderly population, with individuals aged 60 and above expected to grow from 12% of the total population in 2015 to 22% by 2050.

This demographic shift means the number of seniors will expand from 1 billion in 2020 to over 2.1 billion by mid-century. Osteoporosis, arthritis, and degenerative joint diseases are more common in older adults, leading to higher demand for joint replacements and spinal implants. The adoption of minimally invasive procedures in orthopedics is growing to cater to elderly patients seeking faster recovery and reduced post-surgical complications.

Increased healthcare expenditure in developed economies is improving access to advanced orthopedic treatments. The demand for customized orthopedic implants is rising due to advancements in 3D printing technology. The introduction of robotic-assisted surgeries is enhancing precision in joint replacement procedures. Government initiatives supporting elderly healthcare infrastructure are contributing to market expansion.

Research in regenerative medicine, including stem cell therapy for bone and cartilage repair, is gaining traction. The expansion of orthopedic rehabilitation services is improving post-surgical recovery outcomes. The availability of wearable technologies for monitoring musculoskeletal health is further promoting preventive orthopedic care.

Restraints

High Cost of Orthopedic Devices is Restraining the Market

Growing concerns over the affordability of orthopedic devices are anticipated to limit market expansion, particularly in low-income regions. The high cost of implants, such as knee and hip replacements, makes orthopedic treatments inaccessible to many patients. Advanced robotic-assisted orthopedic surgeries, while improving outcomes, require substantial investment, increasing the financial burden on healthcare systems.

The lack of adequate reimbursement policies in several countries discourages patients from opting for expensive procedures. Strict regulatory requirements for new orthopedic devices increase the time and cost of product approvals, slowing market growth. Many developing countries lack sufficient orthopedic specialists and infrastructure to support high-demand surgical interventions.

The need for frequent follow-up treatments, physical therapy, and potential revision surgeries further adds to the long-term expenses associated with orthopedic implants. Some patients delay or avoid orthopedic procedures due to financial constraints, leading to a lower adoption rate in cost-sensitive markets.

Opportunities

Growing Prevalence of Musculoskeletal Disorders as an Opportunity for the Orthopedic Devices Market

Rising musculoskeletal disorders are expected to create significant opportunities in the orthopedic devices market as the need for effective treatment solutions increases. A Lancet Rheumatology study revealed that musculoskeletal disorders have more than doubled globally over the past three decades, increasing from 221 million cases in 1990 to 494 million in 2020. Forecasts suggest that by 2050, cases will rise by an additional 115%, reaching approximately 1.06 billion worldwide.

The surge in musculoskeletal conditions is fueling demand for orthopedic implants, braces, and rehabilitation devices. Technological advancements, including bioresorbable implants and smart prosthetics, are improving patient outcomes. Increasing awareness about early diagnosis and intervention for musculoskeletal disorders is driving demand for orthopedic consultations and surgeries.

Sports-related injuries and occupational hazards are contributing to the growing need for joint and ligament repair devices. The expansion of outpatient orthopedic centers is providing patients with faster access to specialized treatments. Telemedicine and digital health platforms are enhancing musculoskeletal disorder management through remote consultations and physical therapy programs. The integration of AI in orthopedic imaging is improving diagnosis and personalized treatment planning, further supporting market growth.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors significantly impact the orthopedic devices market. On the positive side, increasing healthcare investments and the growing prevalence of orthopedic conditions, such as osteoarthritis and osteoporosis, drive demand for advanced orthopedic solutions. An aging global population also contributes to the market’s expansion, as older individuals are more likely to experience musculoskeletal issues that require orthopedic treatment.

Additionally, improvements in healthcare infrastructure, particularly in emerging economies, offer new growth opportunities for orthopedic device manufacturers. However, economic downturns and healthcare budget cuts can lead to reduced spending on elective surgeries and expensive orthopedic treatments, slowing market growth.

Geopolitical uncertainties, including trade tensions and regulatory differences across regions, could disrupt the global supply chain and increase production costs for orthopedic products. Despite these challenges, ongoing technological innovations in materials and surgical techniques, along with the increasing demand for minimally invasive procedures, ensure continued positive growth for the market.

Trends

High Popularity of Robotic-Assisted Surgery Driving the Orthopedic Devices Market

High popularity of robotic-assisted surgery is a recent trend significantly driving the orthopedic devices market. Increasing demand for precise, minimally invasive procedures is expected to boost the adoption of robotic systems in orthopedic surgeries. These technologies offer enhanced accuracy, reduced complications, and quicker recovery times, which makes them particularly appealing to both healthcare providers and patients.

The rising interest in robotic-assisted surgery is likely to lead to more widespread integration of robotic systems in orthopedic procedures. As the technology continues to evolve, it is anticipated that robotic-assisted surgeries will become a standard practice in orthopedic care, further expanding the market. Stryker UK Limited reports that Mako robotic-assisted surgery is performed on roughly 13,000 patients each month.

The integration of real-time imaging and robotic precision in orthopedic procedures has led to enhanced accuracy, minimal tissue disruption, and faster post-surgical recovery. As the popularity of robotic-assisted surgeries grows, the orthopedic devices market is projected to experience significant expansion.

Regional Analysis

North America is leading the Orthopedic Devices Market

North America dominated the market with the highest revenue share of 39.8% owing to the increasing prevalence of musculoskeletal disorders and advancements in surgical technology. According to the American College of Rheumatology, over 450,000 hip replacements and approximately 790,000 knee replacements are performed annually in the United States, underscoring the rising demand for joint reconstruction solutions.

The growing adoption of robotic-assisted procedures enhanced surgical precision, reduced recovery times, and improved patient outcomes, fueling greater adoption among healthcare providers. Technological innovations, including 3D-printed implants and bioresorbable materials, further contributed to market expansion.

The aging population, particularly in the U.S. and Canada, significantly increased the need for joint replacement and fracture management solutions. Favorable reimbursement policies and insurance coverage for orthopedic procedures encouraged higher patient adoption rates. Additionally, partnerships between medical device companies and research institutions accelerated the development of next-generation implants, further strengthening North America’s position as a leader in orthopedic innovation.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is poised for rapid growth in the orthopedic market, primarily due to substantial healthcare investments and broader access to surgical interventions. The establishment of Tynor Orthotics’ advanced manufacturing facility in Mohali, Punjab, in January 2024 exemplifies the region’s efforts to enhance orthopedic support solutions.

The prevalent rise in conditions like osteoporosis, arthritis, and sports-related injuries in nations such as India, China, and Japan fuels the demand for joint reconstruction and trauma fixation products. Further supporting this growth are expanding healthcare infrastructures and government initiatives that promote medical tourism, improving access to advanced surgical procedures.

Collaborative efforts between local manufacturers and global medical device companies are set to increase product availability and affordability. The trend towards minimally invasive orthopedic surgeries drives the demand for precision-engineered implants and surgical tools. Moreover, increasing consumer awareness of post-operative rehabilitation and non-invasive solutions is expected to contribute significantly to market expansion in the Asia Pacific region.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the orthopedic devices market focus on developing advanced implants, robotic-assisted surgical systems, and biologics to enhance patient outcomes. Companies invest in research and development to improve implant materials, design, and longevity for joint reconstruction and trauma care. Strategic collaborations with hospitals and research institutions drive innovation and accelerate product adoption.

Geographic expansion into regions with increasing orthopedic surgeries supports further market growth. Many players also emphasize digital integration, such as AI-powered preoperative planning and real-time surgical navigation, to improve procedural accuracy and efficiency. Stryker is a leading company in this market, offering innovative orthopedic solutions, including joint replacement implants and robotic-assisted surgical systems like Mako.

The company prioritizes technological advancements and strong partnerships with healthcare providers to improve surgical precision and patient recovery. Stryker’s commitment to innovation and global expansion solidifies its position as a key player in orthopedic healthcare.

Top Key Players in the Orthopedic Devices Market

- Zimmer Biomet

- UCLA School of Dentistry

- Stryker

- Smith+Nephew

- Medtronic

- Enovis

- DePuy Synthes

- CONMED Corporation

Recent Developments

- In January 2024: Enovis completed the acquisition of LimaCorporate S.p.A., a globally recognized leader in orthopedic solutions. This acquisition strengthens Enovis’ presence in the orthopedic reconstruction sector by incorporating Lima’s advanced surgical innovations into its product portfolio.

- In November 2023: Researchers at the UCLA School of Dentistry introduced a breakthrough dental implant technology that utilizes ultraviolet (UV) light. The innovative method involves exposing titanium implants to UV light for one minute, effectively eliminating hydrocarbons and reducing the likelihood of post-surgical complications.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 62.7 billion |

| Forecast Revenue (2034) | US$ 96.4 billion |

| CAGR (2025-2034) | 4.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Joint Replacement/ Orthopedic Implants (Lower Extremity Implants (Foot & Ankle Implants, Hip Implants, and Knee Implants), Spinal Implants, Dental (Dental Implants and Craniomaxillofacial Implants), and Upper Extremity Implants (Shoulder Implants, Hand & Wrist Implants, and Elbow Implants)), Trauma (Implants, Accessories, and Instruments), Sports Medicine (Body Reconstruction & Repair, Body Support & Recovery, Body Monitoring & Evaluation, and Accessories), Orthobiologics (Viscosupplementation, Synthetic Bone Substitutes, Stem Cell Therapy, Demineralized Bone Matrix, Bone Morphogenetic Protein (BMP), and Allograft), and Others), By End-user (Hospitals, Orthopedic Clinics, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Zimmer Biomet, UCLA School of Dentistry, Stryker, Smith+Nephew, Medtronic, Enovis, DePuy Synthes, and CONMED Corporation. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |