Quick Navigation

Report Overview

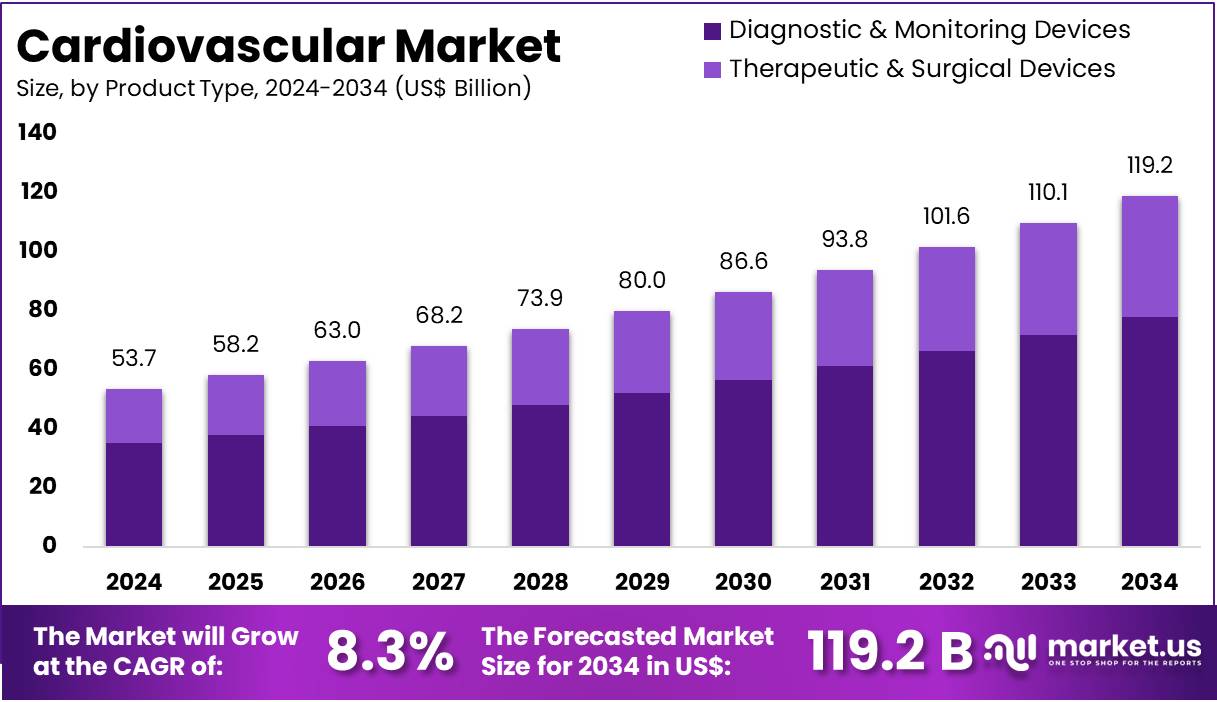

The Cardiovascular Market size is expected to be worth around US$ 119.2 billion by 2034 from US$ 53.7 billion in 2024, growing at a CAGR of 8.3% during the forecast period 2025 to 2034.

Increasing prevalence of cardiovascular diseases (CVD) worldwide has significantly boosted the demand for cardiovascular products and services. Factors such as sedentary lifestyles, unhealthy diets, high tobacco usage, and rising stress levels contribute to the growing incidence of heart conditions. The cardiovascular market includes a wide range of applications, such as diagnostic tools, medical devices, surgical procedures, and pharmaceutical products aimed at treating conditions like coronary artery disease, hypertension, arrhythmia, and heart failure.

Technological advancements, including the development of minimally invasive surgeries, robotic surgeries, and the introduction of next-generation diagnostic devices, have created new opportunities for market growth. The demand for heart health monitoring devices, such as wearable ECG monitors and implantable cardiac devices, has risen due to increased awareness of preventive healthcare and the need for continuous monitoring of heart conditions.

Moreover, innovations in drug therapies and cardiovascular interventions continue to enhance patient outcomes and reduce recovery times. According to the World Health Organization (WHO), published in 2023, cardiovascular diseases remain the leading cause of death globally, accounting for 32% of all deaths, emphasizing the critical importance of ongoing advancements in this field to address the growing healthcare burden.

Key Takeaways

- In 2023, the market for cardiovascular generated a revenue of US$ 53.7 billion, with a CAGR of 8.3%, and is expected to reach US$ 119.2 billion by the year 2033.

- The product type segment is divided into diagnostic & monitoring devices and therapeutic & surgical devices, with diagnostic and monitoring devices taking the lead in 2023 with a market share of 65.3%.

- Considering application, the market is divided into coronary artery disease (CAD), heart failure, cardiac arrhythmia, and others. Among these, coronary artery disease (CAD) held a significant share of 48.5%.

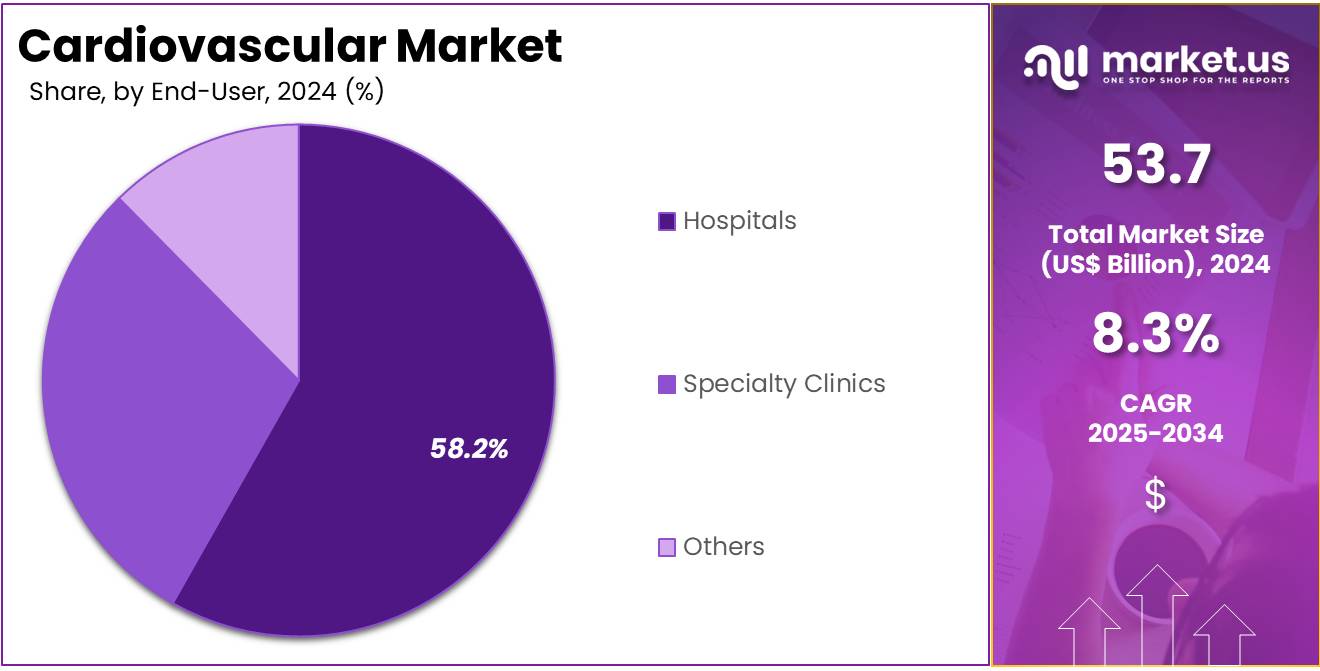

- Furthermore, concerning the end-user segment, the market is segregated into hospitals, specialty clinics, and others. The hospitals sector stands out as the dominant player, holding the largest revenue share of 58.2% in the cardiovascular market.

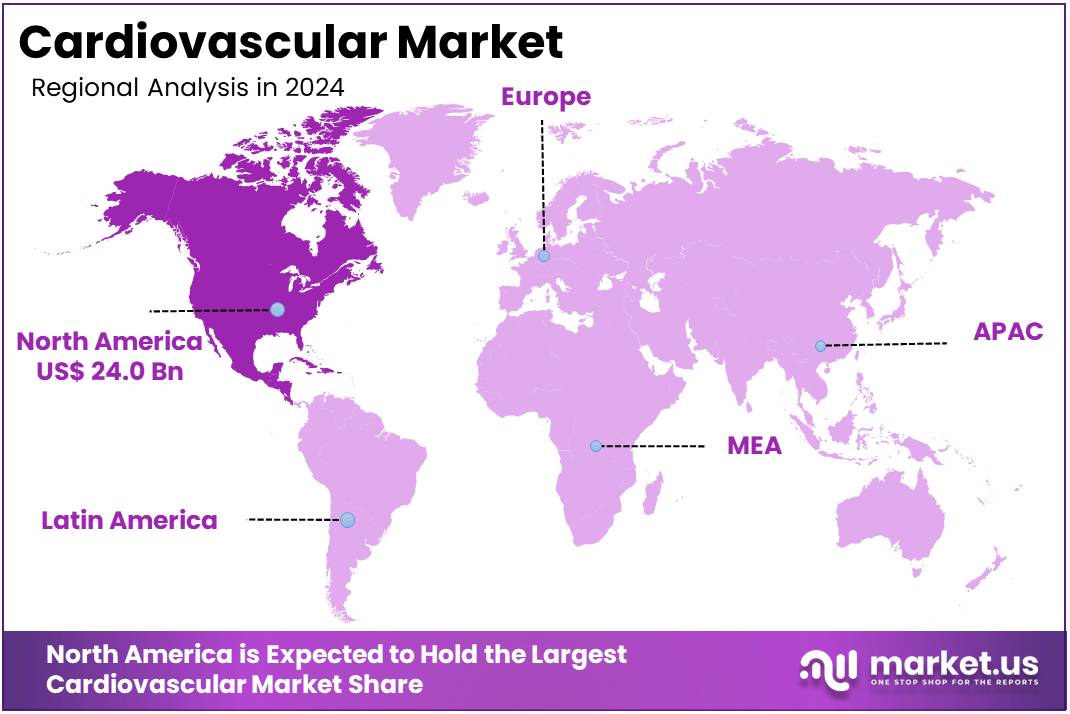

- North America led the market by securing a market share of 44.7% in 2023.

Product Type Analysis

The diagnostic and monitoring devices segment led in 2023, claiming a market share of 65.3% owing to as healthcare providers increasingly prioritize early detection and continuous monitoring of cardiovascular conditions. The rising prevalence of heart diseases, including coronary artery disease and heart failure, is anticipated to drive demand for advanced diagnostic tools such as ECG machines, blood pressure monitors, and portable devices for real-time data analysis.

Technological advancements, including the development of wearable and non-invasive monitoring devices, are likely to contribute to the segment’s expansion by enabling more accessible and accurate diagnostics. Additionally, the growing trend of personalized medicine and the need for continuous monitoring of patients with chronic cardiovascular conditions are projected to fuel the adoption of these diagnostic and monitoring devices, thereby promoting their growth in the market.

Application Analysis

The coronary artery disease (CAD) held a significant share of 48.5% as CAD remains one of the leading causes of mortality worldwide. The increasing prevalence of risk factors such as hypertension, diabetes, and unhealthy lifestyles is expected to drive the demand for effective treatments and diagnostic solutions for CAD. The growing awareness of CAD and its early signs is likely to promote earlier diagnosis and intervention, leading to better patient outcomes.

Additionally, advancements in imaging technology and the development of innovative treatments, such as drug-eluting stents and minimally invasive surgeries, are anticipated to further contribute to the growth of the CAD segment. As the global burden of CAD continues to rise, healthcare systems are expected to invest more in preventive care and treatment options, boosting demand for CAD-related services and products.

End-user Analysis

The hospitals segment experienced significant growth, capturing a 58.2% revenue share. This growth is driven by the increasing number of cardiovascular procedures performed in hospital settings. Hospitals remain the primary choice for complex interventions, including heart surgeries, catheterizations, and heart failure management. The rising incidence of cardiovascular diseases, especially in aging populations, is fueling demand for specialized care. Advanced treatment options are in high demand as more patients seek comprehensive cardiovascular services. Hospitals continue to play a crucial role in managing heart-related conditions efficiently.

The demand for cardiovascular treatments is encouraging hospitals to adopt cutting-edge technologies. Many hospitals are expanding their cardiology departments to accommodate growing patient needs. Healthcare systems are focusing on improving outcomes and reducing costs, reinforcing hospitals’ leadership in cardiovascular care. As a result, hospitals are expected to maintain their dominant position in the market. The increasing emphasis on advanced medical solutions will continue to drive growth. This trend ensures that hospitals remain at the forefront of cardiovascular treatment and innovation.

Key Market Segments

By Product Type

- Diagnostic & Monitoring Devices

- Electrocardiogram (ECG)

- Remote Cardiac Monitoring

- Others

- Therapeutic & Surgical Devices

- Ventricular Assist Devices (VAD)

- Cardiac Rhythm Management (CRM) Devices

- Catheter

- Stents

- Heart Valves

- Others

By Application

- Coronary Artery Disease (CAD)

- Heart Failure

- Cardiac Arrhythmia

- Others

By End-user

- Hospitals

- Specialty Clinics

- Others

Drivers

Rising Prevalence of Cardiovascular Diseases is Driving the Market

The global rise in cardiovascular diseases (CVDs) is driving demand for advanced medical devices and treatments. According to the World Health Organization (WHO), CVDs remain the leading cause of death worldwide, claiming an estimated 17.9 million lives annually. This alarming figure highlights the urgent need for improved cardiovascular care. As cases continue to rise, healthcare systems are prioritizing innovative solutions. The focus is on early diagnosis, minimally invasive procedures, and advanced treatment options. These developments aim to reduce mortality rates and improve patient outcomes.

The increasing burden of CVDs has led to significant investments in medical technologies. Healthcare providers are adopting advanced imaging, remote monitoring, and AI-driven diagnostics to enhance patient care. Additionally, novel therapies such as drug-eluting stents and bioresorbable scaffolds are gaining traction. Governments and private sectors are funding research to develop more effective interventions. The continuous rise in cardiovascular cases underscores the necessity for innovation. This ongoing demand is fueling growth in the cardiovascular market.

Restraints

High Treatment Costs are Restraining the Market

Despite technological advancements, the high cost of cardiovascular treatments remains a major challenge. In 2021, cardiovascular diseases cost the European Union (EU) economy an estimated €282 billion annually. Of this, €155 billion was spent on health and long-term care, making up 11% of total EU health expenditure. Converting this to U.S. dollars using the 2021 exchange rate of 1 Euro = 1.183 USD, the total cost reached approximately $333 billion, while health and long-term care costs amounted to about $183 billion. These high expenses put pressure on healthcare systems.

The financial burden of cardiovascular treatments limits patient access, especially in low- and middle-income countries. Many patients avoid necessary procedures due to high costs, leading to worsening health outcomes. Advanced cardiovascular therapies remain expensive, restricting widespread adoption despite their benefits. Healthcare budgets face growing strain, making it difficult to allocate resources efficiently. These financial barriers slow market expansion, preventing innovative treatments from reaching broader populations in need. Addressing cost challenges is crucial for market growth.

Opportunities

Technological Innovations are Creating Growth Opportunities

Advancements in medical technology are driving significant growth in the cardiovascular market. Minimally invasive procedures, such as transcatheter aortic valve implantation (TAVI), have transformed treatment methods. These procedures reduce recovery times and improve patient outcomes compared to traditional surgeries. Patients experience less pain and shorter hospital stays, making these treatments more appealing. As demand for less invasive options grows, healthcare providers are adopting these techniques. The increasing preference for TAVI and similar procedures is expanding the market, attracting more patients seeking safer and effective treatments.

The integration of artificial intelligence (AI) in cardiovascular diagnostics is further enhancing market growth. AI-powered tools improve early disease detection, leading to timely interventions. These technologies analyze medical images with high accuracy, reducing diagnostic errors. AI also supports personalized treatment plans by assessing patient data in real time. The combination of AI and advanced medical procedures enhances healthcare efficiency. As AI-driven solutions gain adoption, the cardiovascular market is poised for continuous expansion, offering better care and improved patient outcomes.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors significantly influence the cardiovascular market. Economic downturns can lead to reduced healthcare funding, limiting access to advanced treatments and technologies. Geopolitical tensions may disrupt global supply chains, affecting the availability of essential medical devices and pharmaceuticals.

For instance, trade disputes can result in increased tariffs, escalating the costs of imported medical equipment. However, global initiatives aimed at combating cardiovascular diseases, such as collaborative research programs and funding from international health organizations, provide positive momentum. These efforts facilitate the development and dissemination of innovative treatments, improving patient outcomes worldwide. Despite economic and political challenges, the collective commitment to addressing cardiovascular health continues to drive progress in the market.

Trends

Emphasis on Preventive Healthcare is a Recent Trend

A notable trend in the cardiovascular market is the growing emphasis on preventive healthcare. Healthcare systems are increasingly focusing on early detection and management of risk factors to curb the incidence of cardiovascular diseases. This shift towards prevention is evident in public health campaigns promoting healthy lifestyles and regular screenings. Moreover, wearable technology that monitors vital signs in real-time enables individuals to manage their health proactively. This proactive approach aims to reduce the long-term burden of cardiovascular diseases on both individuals and healthcare infrastructures.

Regional Analysis

North America is leading the Cardiovascular Market

North America held the largest market share of 44.7% in 2024 due to multiple key factors. The aging population in the United States significantly increased demand for cardiovascular care. In 2023, approximately 16.5% of U.S. residents were aged 65 and older. Advancements in medical technology led to more effective cardiovascular treatments, improving patient outcomes and increasing adoption. The rising prevalence of risk factors, such as hypertension and obesity, further drove demand. According to the CDC, nearly 48% of U.S. adults had hypertension between August 2021 and August 2023.

The growing awareness of cardiovascular health also fueled demand for screening and diagnostic services. Government initiatives focused on improving healthcare infrastructure and access to cardiovascular care contributed to market expansion. The integration of telemedicine and digital health solutions enhanced service accessibility, particularly in underserved areas. Additionally, North America’s well-established healthcare systems and high healthcare spending facilitated the widespread adoption of cardiovascular treatments. These factors collectively drove strong market growth in the region during 2024.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow at the fastest CAGR due to several key factors. The region’s aging population is increasing the demand for cardiovascular services. The United Nations projects that by 2050, the number of older people in Asia and the Pacific will reach 1.3 billion, up from 600 million in 2020. Additionally, the rising prevalence of risk factors such as hypertension and obesity is driving demand for cardiovascular interventions. The World Health Organization states that in 2022, 31% of adults worldwide did not meet recommended physical activity levels. This inactivity contributes to the growing burden of cardiovascular diseases.

Economic growth in China and India is improving middle-class purchasing power, making healthcare more accessible. Government initiatives are supporting healthcare infrastructure and cardiovascular care. These efforts aim to enhance access to treatments and preventive measures. Increasing awareness of cardiovascular health is also driving demand for screening and diagnostic services. Public health campaigns and early detection programs are improving patient outcomes. These factors collectively support the strong growth of the cardiovascular market in Asia Pacific during the forecast period.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the cardiovascular market focus on expanding their product portfolios with innovative devices and treatments for heart diseases, including stents, pacemakers, and diagnostic tools. Companies invest in research and development to improve the efficacy of treatments, reduce side effects, and enhance patient outcomes. Strategic partnerships with healthcare providers and research institutions help drive adoption and expand market reach. Emphasis on minimally invasive procedures and personalized medicine has further propelled market growth. Many players also prioritize global expansion to address the increasing demand for cardiovascular care.

Medtronic is a leading company in this market, offering a wide range of cardiovascular products, including coronary stents, heart valves, and diagnostic devices. The company focuses on technological innovation and expanding its portfolio through acquisitions, strengthening its position as a key player in the cardiovascular industry. Medtronic’s commitment to improving heart disease treatments and patient care has established it as a leader in the field.

Top Key Players in the Cardiovascular Market

- Siemens Healthcare GmbH

- Philips

- Medtronic

- GE HealthCare

- Edwards Lifesciences Corporation

- Cardinal Health

- Boston Scientific Corporation

- Abbott

Recent Developments

- In October 2024, Philips introduced its latest advancements in interventional cardiology at the Transcatheter Cardiovascular Therapeutics (TCT) conference. The newly developed solutions aim to optimize procedural workflows, enhance diagnostic precision, and improve patient recovery outcomes in minimally invasive cardiac treatments.

- In April 2024, Medtronic launched the Avalus Ultra valve, an innovative surgical aortic tissue valve designed for improved implantation efficiency and long-term durability. This next-generation device focuses on simplifying surgical procedures while enhancing patient outcomes in cardiac care.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 53.7 Billion |

| Forecast Revenue (2034) | US$ 119.2 Billion |

| CAGR (2025-2034) | 8.3% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Diagnostic & Monitoring Devices (Electrocardiogram (ECG), Remote Cardiac Monitoring, and Others), Therapeutic & Surgical Devices (Ventricular Assist Devices (VAD), Cardiac Rhythm Management (CRM) Devices, Catheter, Stents, Heart Valves, and Others)), By Application (Coronary Artery Disease (CAD), Heart Failure, Cardiac Arrhythmia, and Others), By End-user (Hospitals, Specialty Clinics, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Siemens Healthcare GmbH, Philips, Medtronic, GE HealthCare, Edwards Lifesciences Corporation, Cardinal Health, Boston Scientific Corporation, and Abbott. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |