Quick Navigation

Report Overview

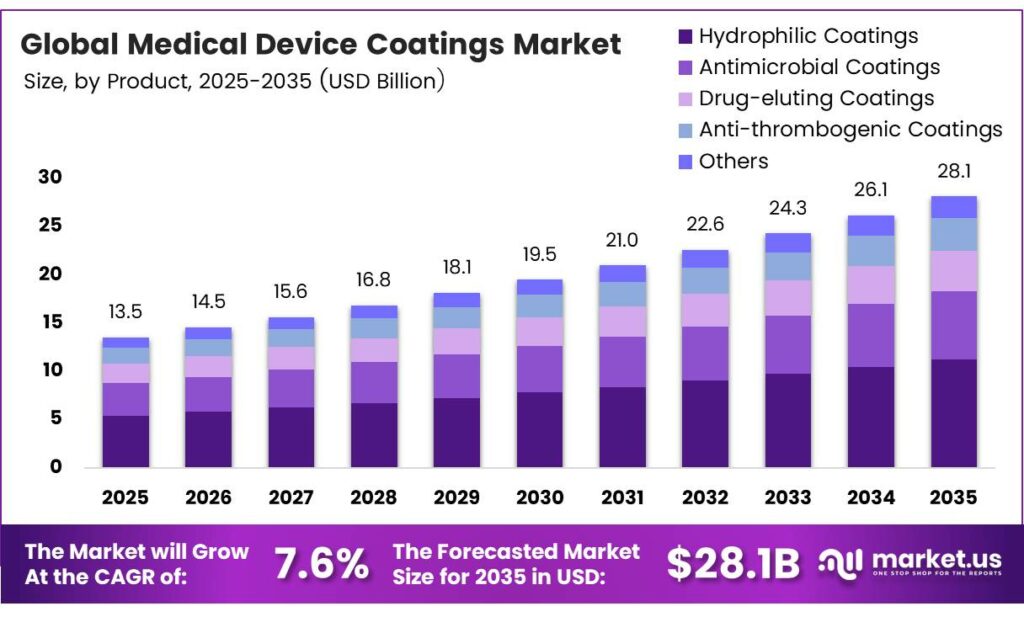

The Global Medical Device Coatings Market size is expected to be worth around USD 28.1 billion by 2035 from USD 13.5 billion in 2025, growing at a CAGR of 7.6% during the forecast period 2026 to 2035.

The medical device coatings market covers specialized surface treatments applied to implants, catheters, surgical instruments, and diagnostic tools. These coatings improve device performance by reducing friction, preventing infection, and enhancing biocompatibility. Consequently, they play a critical role in patient safety and treatment outcomes across multiple clinical areas.

R&D investment continues to surge across the industry, with companies focusing on multi-functional coatings and smart drug-delivery surfaces. Academic and industry partnerships accelerate development cycles. Antimicrobial implant coatings, including gentamicin, silver, iodine, and DAC-hydrogel, reduced implant-associated infection odds by 73–90% compared with uncoated orthopedic implants, demonstrating powerful clinical value.

Hydrophilic coatings show remarkable performance gains in device navigation and patient comfort. Hydrophilic coatings can reduce the friction coefficient to below 0.01 in medical-device interfaces, enabling smoother catheter and guidewire advancement. This performance level directly supports the clinical push toward less traumatic, more precise interventional procedures.

Key Takeaways

- The Global Medical Device Coatings Market is valued at USD 13.5 billion in 2025 and is projected to reach USD 28.1 billion by 2035 at a CAGR of 7.6% during the forecast period from 2026 to 2035.

- Hydrophilic Coatings dominate the By Product segment with a market share of 34.8% in 2025.

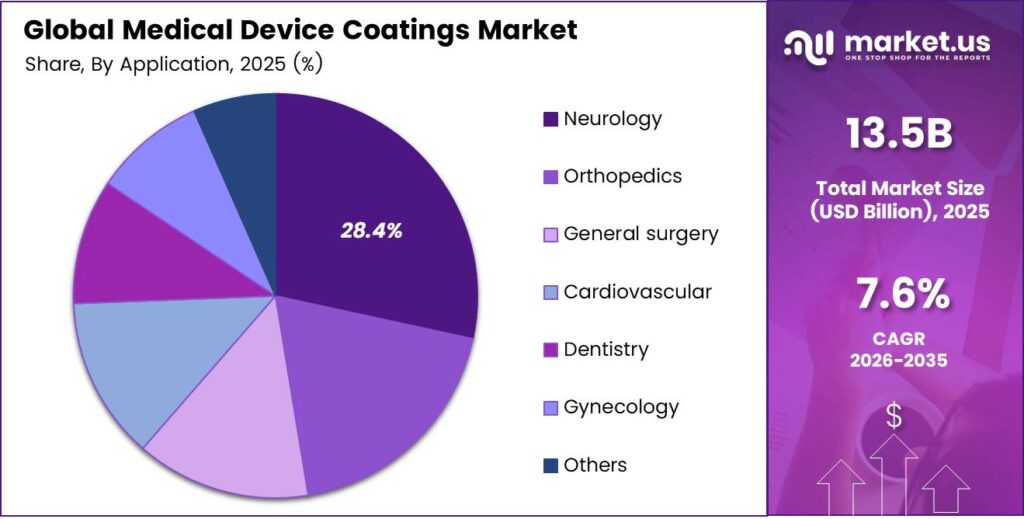

- Neurology leads the By Application segment with a market share of 28.4% in 2025.

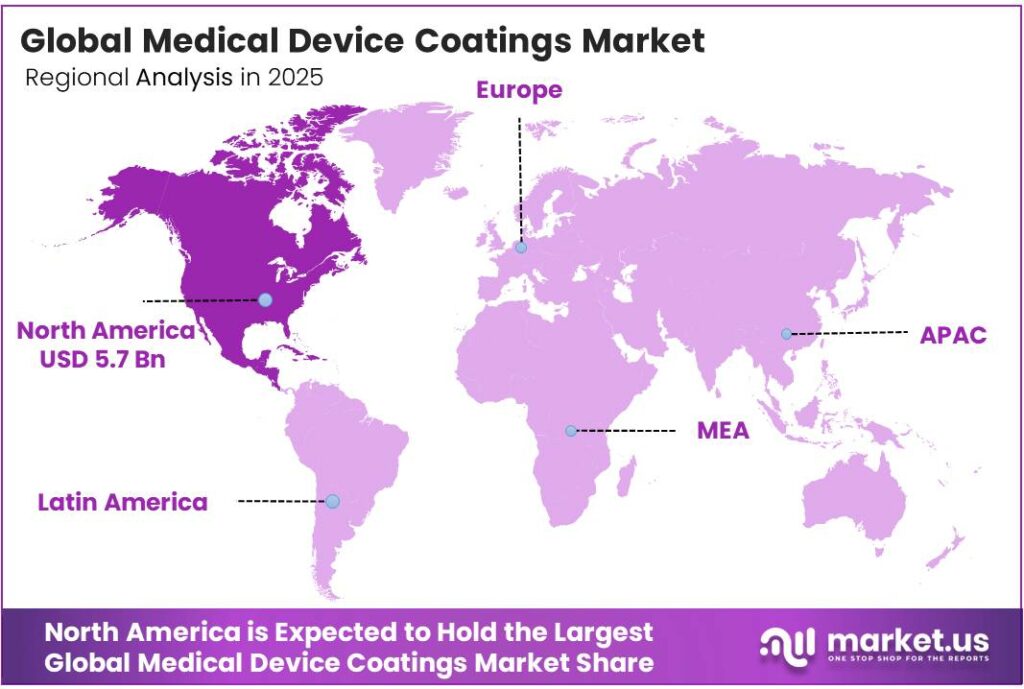

- North America dominates the regional landscape with a market share of 42.1%, valued at USD 5.7 billion in 2025.

By Product Analysis

Hydrophilic Coatings dominate with 34.8% due to superior lubricity and broad device compatibility.

In 2025, Hydrophilic Coatings held a dominant market position in the By Product segment of the Medical Device Coatings Market, with a 34.8% share. These coatings reduce surface friction significantly, enabling smoother device insertion and navigation. Moreover, their compatibility with catheters, guidewires, and endoscopes makes them the most widely adopted coating type across clinical settings.

Antimicrobial Coatings represent a fast-growing product segment driven by rising hospital-acquired infection rates. These coatings incorporate agents such as silver and iodine to inhibit bacterial colonization on implant surfaces. Additionally, their proven clinical effectiveness in reducing postoperative complications positions them as a key segment in infection-control-focused procurement strategies.

Drug-eluting Coatings serve a specialized but critical role in cardiovascular and interventional device applications. These coatings release therapeutic agents directly at the implant site, controlling localized drug delivery over defined periods. Consequently, drug-eluting stents and orthopedic implants using these coatings show reduced restenosis and improved long-term patient outcomes.

By Application Analysis

Neurology dominates with 28.4% due to high device complexity and critical biocompatibility requirements.

In 2025, Neurology held a dominant market position in the By Application segment of the Medical Device Coatings Market, with a 28.4% share. Neurological devices, including brain stimulators, shunts, and neurovascular catheters, demand advanced surface coatings to ensure precise navigation and tissue compatibility. Moreover, the sensitivity of neural environments makes biocompatible coatings a non-negotiable design requirement.

Orthopedics represents a major application area driven by the global rise in joint replacement and spinal implant procedures. Antimicrobial and hydrophilic coatings help reduce infection risk and improve implant osseointegration. Additionally, aging populations in developed markets continue to expand orthopedic procedure volumes, sustaining strong demand for performance-enhancing coatings.

General Surgery applications benefit from coatings that reduce friction on laparoscopic and endoscopic tools. These coatings improve instrument maneuverability during minimally invasive procedures. Consequently, surgical teams report better procedural control and reduced tissue trauma when using coated instruments in standard operative environments.

Key Market Segments

By Product

- Hydrophilic Coatings

- Antimicrobial Coatings

- Drug-eluting Coatings

- Anti-thrombogenic Coatings

- Others

By Application

- Neurology

- Orthopedics

- General Surgery

- Cardiovascular

- Dentistry

- Gynecology

- Others

Emerging Trends

Eco-Friendly and Multi-Functional Coatings Reshape Product Development

Medical device manufacturers increasingly prefer eco-friendly and non-toxic coating materials to meet sustainability goals and regulatory expectations. Additionally, multi-functional coatings that combine lubricity, antimicrobial action, and drug-eluting properties in a single layer are gaining commercial traction. The hydrophilic TPU/PVP catheter coating reduced the friction coefficient from approximately 1.3 to 0.02, representing a 98.5% reduction, confirming the clinical value of advanced surface engineering.

Anti-Thrombogenic Integration and Cross-Industry Collaborations Accelerate Innovation

Next-generation devices increasingly integrate anti-thrombogenic and anti-fouling coatings to extend implant longevity and patient safety. Moreover, collaborations between medical device manufacturers and specialized coating technology providers accelerate innovation cycles. These partnerships allow faster translation of laboratory breakthroughs into regulatory-approved, commercially viable coatings for cardiovascular, neurological, and orthopedic applications.

Drivers

Minimally Invasive Procedures and Antimicrobial Needs Fuel Coating Demand

Rising demand for minimally invasive surgical procedures directly drives the adoption of advanced biocompatible coatings across catheters, guidewires, and endoscopes. Hydrophilic coatings reduce device friction and trauma during insertion. Moreover, antimicrobial-coated urinary catheters achieved a statistically significant 20% reduction in catheter-associated urinary tract infections, with an odds ratio of 0.80, demonstrating measurable clinical and economic benefits for healthcare systems.

Implant Expansion and Coating Technology Advances Drive Specialty Segment Growth

Global growth in cardiovascular stenting and orthopedic implant procedures continues to boost demand for specialty coatings. Drug-eluting and anti-thrombogenic coatings play a central role in improving long-term implant outcomes. Additionally, technological advancements in hydrophilic and polymer-based coating formulations improve device navigation, surface durability, and therapeutic precision, giving manufacturers a competitive clinical advantage in high-growth device categories.

Restraints

Regulatory Complexity Slows Entry of Novel Coating Technologies

Stringent regulatory approval processes in the United States, Europe, and other major markets create significant delays for novel coating technologies. Manufacturers must conduct extensive biocompatibility testing and clinical validation before commercialization. Consequently, long approval timelines increase development costs and reduce the speed at which innovative coatings reach healthcare providers and patients.

High Production Costs Limit Market Penetration in Price-Sensitive Segments

Advanced coating materials, such as nanotechnology-based formulations and biodegradable polymers, involve high production and processing costs. Smaller manufacturers and cost-sensitive healthcare markets find adoption challenging. Therefore, premium pricing for advanced coated devices limits their penetration in developing economies and budget-constrained hospital systems, slowing overall market expansion despite strong clinical demand.

Growth Factors

Smart Coatings and Nanotechnology Open New Market Opportunities

Emerging demand for smart coatings with integrated drug delivery and biosensing capabilities creates significant new commercial opportunities. Nanotechnology-enabled surfaces offer enhanced antimicrobial performance, controlled drug release, and real-time monitoring potential. Antibiotic-coated catheters maintained antibacterial activity for over 40 days, demonstrating that advanced coatings can provide extended therapeutic protection, reducing the need for repeat procedures and systemic antibiotic use.

Developing Markets and R&D Investment Expand the Global Coating Addressable Market

Rapid healthcare infrastructure growth in Asia Pacific, Latin America, and the Middle East expands the global addressable market for medical device coatings. Rising surgical volumes in these regions drive demand for coated implants and minimally invasive instruments. Moreover, increasing investments in R&D for customized and patient-specific coating solutions allow manufacturers to address unmet clinical needs and differentiate in a competitive global marketplace.

Regional Analysis

North America Dominates the Medical Device Coatings Market with a Market Share of 42.1%, Valued at USD 5.7 Billion

North America leads the global Medical Device Coatings Market, capturing 42.1% of the total market share and generating USD 5.7 billion in 2025. The region benefits from a highly advanced healthcare system, strong R&D investment, and a robust regulatory framework. Moreover, high surgical procedure volumes and early adoption of innovative coated devices continue to reinforce North America’s market leadership position.

Europe represents a mature and innovation-driven market for medical device coatings. Strong manufacturing capabilities in Germany, France, and the UK support consistent product development. Additionally, EU regulatory harmonization through the Medical Device Regulation framework encourages investment in biocompatible and performance-enhancing coating technologies across the region.

Asia Pacific emerges as the fastest-growing regional market, driven by expanding healthcare infrastructure and rising surgical volumes in China, India, and Japan. Government health initiatives and increasing medical tourism activity further stimulate demand. Consequently, global coating manufacturers actively expand their presence in the region through partnerships and local production facilities.

Latin America presents growing opportunities for medical device coating adoption, particularly in Brazil and Mexico. Rising chronic disease rates and improving healthcare access drive surgical procedure growth. Additionally, international manufacturers increasingly target Latin American markets by offering cost-effective coated device solutions tailored to the region’s healthcare budget realities.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

SurModics Inc. is a leading surface modification and drug delivery solutions provider serving the global medical device industry. The company specializes in hydrophilic and hemocompatible coatings applied to interventional cardiology and peripheral vascular devices. Moreover, SurModics consistently invests in expanding its coating portfolio through targeted R&D and strategic partnerships with device manufacturers.

Sono-Tek Corporation develops ultrasonic spray coating systems widely used in applying thin, uniform coatings on medical devices. Its technology supports hydrophilic, drug-eluting, and antimicrobial coating applications across catheters, stents, and surgical instruments. Additionally, the company’s non-contact spray systems reduce material waste and enable precise coating thickness control, which is critical for regulatory compliance.

DSM operates as a global science-based company with a dedicated medical coatings business offering biocompatible surface solutions. The company delivers hydrophilic lubricious coatings and anti-thrombogenic treatments for interventional, diagnostic, and implantable devices. Furthermore, DSM’s deep expertise in polymer chemistry and material science allows it to support customized coating development programs for complex device geometries.

Hydromer, Inc. specializes in hydrophilic polymer coatings for medical devices, with particular strength in catheter and guidewire lubricity applications. The company offers proprietary coating chemistries that meet strict FDA and ISO biocompatibility standards. Hydrogel coatings retained over 95% functionality after sterilization and simulated physiological exposure, reflecting the durability standards that leading firms like Hydromer prioritize in product development.

Top Key Players in the Market

- SurModics Inc.

- Sono-Tek Corp.

- DSM

- Hydromer, Inc.

- Covalon Technologies Ltd.

- Infinita Biotech Private Ltd.

- Materion Corp.

- Biocoat Incorporated

- Harland Medical Systems

- Medicoat AG

Recent Developments

- In 2025, SurModics is a major player in outsourced hydrophilic coatings. The FTC said the deal would combine two leading outsourced hydrophilic-coatings suppliers and alleged the combined company would control more than 50% of that market. The FTC also emphasized that hydrophilic coatings are critical in neurovascular, coronary, peripheral vascular, and structural heart procedures.

- In 2025, Sono-Tek’s recent developments point to strong medical-device coating equipment demand. In its SEC filing for the quarter. The company said medical-market growth was driven by stent coating systems, balloon catheter coating platforms, and emerging diagnostic device applications.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 13.5 Billion |

| Forecast Revenue (2035) | USD 28.1 Billion |

| CAGR (2026-2035) | 7.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Hydrophilic Coatings, Antimicrobial Coatings, Drug-eluting Coatings, Anti-thrombogenic Coatings, Others), By Application (Neurology, Orthopedics, General Surgery, Cardiovascular, Dentistry, Gynecology, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | SurModics Inc., Sono-Tek Corp., DSM, Hydromer, Inc., Covalon Technologies Ltd., Infinita Biotech Private Ltd., Materion Corp., Biocoat Incorporated, Harland Medical Systems, Medicoat AG |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |