Quick Navigation

Report Overview

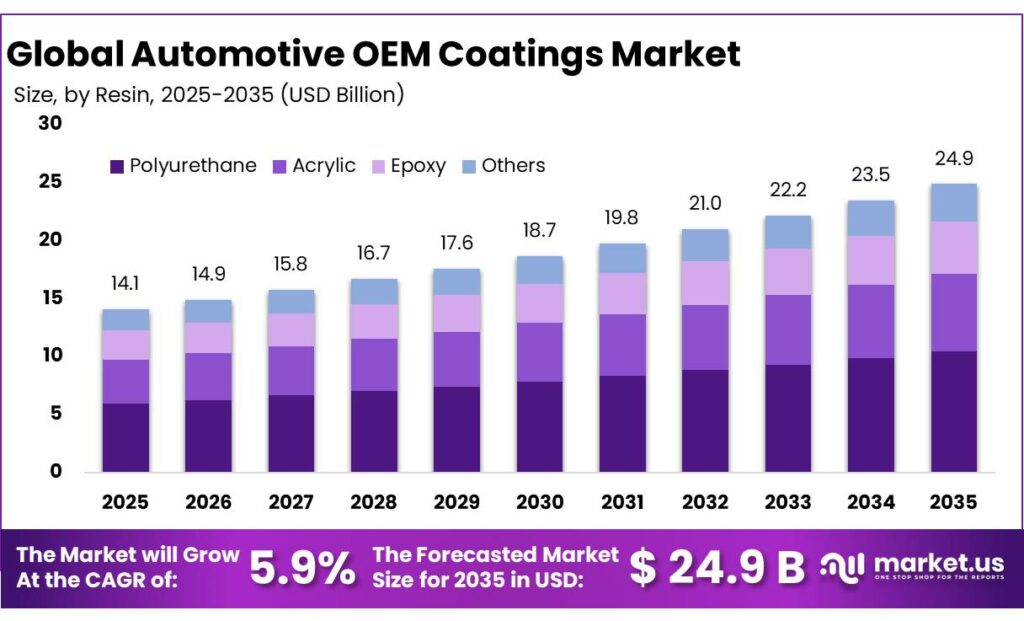

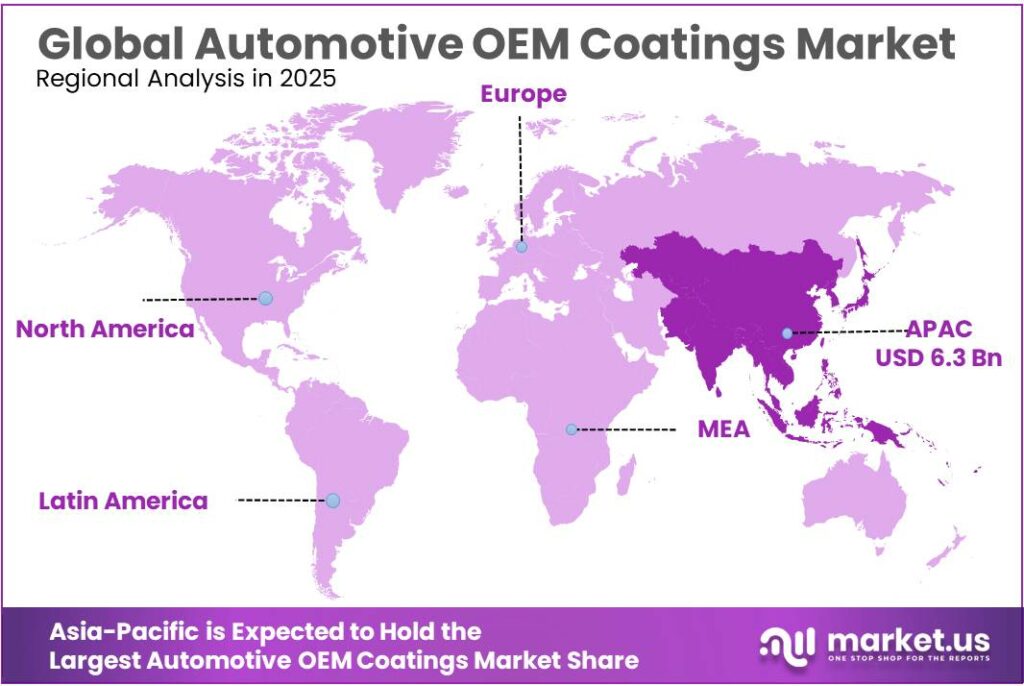

The Global Automotive OEM Coatings Market size is expected to be worth around USD 24.9 Billion by 2035, from USD 14.1 Billion in 2025, growing at a CAGR of 5.9% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 45.1% share, holding USD 6.3 Billion revenue.

Automotive OEM coatings remain a strategically important materials segment because every new vehicle requires tightly specified primer, basecoat, clearcoat, and e-coat systems that protect the body shell, support corrosion resistance, and deliver finish quality at industrial scale. The industry backdrop remains sizable even without relying on private market-estimate providers: global motor vehicle production reached about 92.5 million units in 2024, while the European Union registered around 10.6 million new cars in 2024, up 0.8% year on year.

In parallel, battery-electric cars represented 13.6% of EU new-car registrations in 2024, confirming that coating systems are increasingly being designed around lightweight substrates, energy-efficient curing, and appearance requirements for EV platforms.

On the other side, electrification is sustaining medium-term technical demand: the IEA reported that electric car sales exceeded 17 million globally in 2024, rising by more than 25% and surpassing a 20% share of total car sales. That shift matters because EV architectures push coating suppliers toward thinner film builds, improved thermal and chemical durability, and lower-emission process chemistries.

The principal demand drivers are regulatory pressure, decarbonisation targets and the need to improve paint-shop economics. In the EU, passenger cars are responsible for around 16% of total CO2 emissions and vans for about 3%, which keeps pressure on automakers to reduce lifecycle emissions and improve manufacturing efficiency. Passenger cars also remain dominant in mobility demand, accounting for 73% of passenger-kilometres travelled in the EU in 2022, reinforcing the strategic importance of durable, high-throughput OEM finishing systems.

In parallel, regulatory and public-sector support remains active: the European Commission’s 5 March 2025 Automotive Action Plan outlines measures across five key areas, while the Commission also said the related programme will make €1 billion available for 2025–2027 for the automotive sector. In the U.S., the Department of Energy announced up to $88 million in FY2025 Vehicle Technologies Office funding for advanced transportation solutions.

BASF remains strategically important: its Coatings division reported €11,849 million in sales in 2024, and in November 2025 BASF Coatings commissioned a new automotive OEM coatings plant in Münster, Germany to increase production efficiency for high-demand colors.

Key Takeaways

- Automotive OEM Coatings Market size is expected to be worth around USD 24.9 Billion by 2035, from USD 14.1 Billion in 2025, growing at a CAGR of 5.9%.

- Base Coat held a dominant market position, capturing more than a 43.8% share.

- Polyurethane held a dominant market position, capturing more than a 42.9% share.

- Water-based held a dominant market position, capturing more than a 48.2% share.

- Passenger Cars held a dominant market position, capturing more than a 74.9% share.

- Asia-Pacific held the leading position in the Automotive OEM Coatings market, accounting for 45.1% of the global share and reaching USD 6.3 Billion.

By Product Analysis

Base Coat leads the Automotive OEM Coatings Market with 43.8% share, supported by its critical role in color quality and vehicle finish consistency.

In 2025, Base Coat held a dominant market position, capturing more than a 43.8% share. This strong position was mainly driven by its essential use in delivering the final color appearance, gloss depth, and visual appeal of vehicles in OEM production lines. Automakers continued to prioritize high-quality exterior finishes that improve brand identity and consumer appeal, making base coat a key part of the coating system. Its ability to provide uniform color distribution, metallic and pearlescent effects, and compatibility with advanced clear coat layers further supported its widespread adoption.

By Resin Analysis

Polyurethane dominates the Automotive OEM Coatings Market with 42.9% share, driven by its strong durability and premium finish performance.

In 2025, Polyurethane held a dominant market position, capturing more than a 42.9% share. This leading position was supported by its wide use in automotive OEM coatings where long-term durability, surface protection, and appearance quality remain top priorities. Vehicle manufacturers continued to prefer polyurethane-based coatings because they offer excellent resistance to scratches, weather exposure, chemicals, and UV radiation, all of which are important for maintaining vehicle finish over time. The resin also plays a major role in delivering smooth gloss, color retention, and strong adhesion across different coating layers, making it highly suitable for modern production standards.

By Technology Analysis

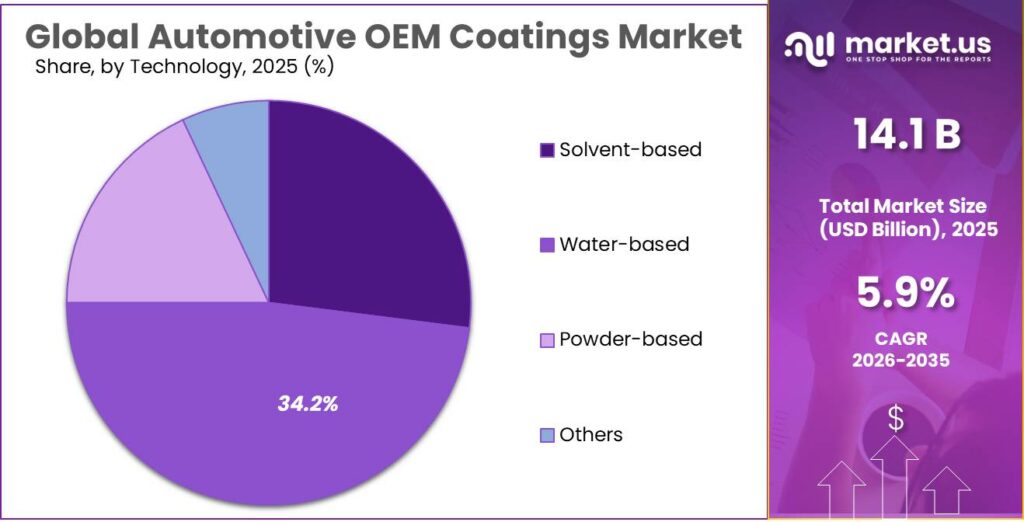

Water-based technology leads the Automotive OEM Coatings Market with 48.2% share, supported by stricter emission norms and wider OEM adoption.

In 2025, Water-based held a dominant market position, capturing more than a 48.2% share. This strong market presence was largely driven by the automotive industry’s growing shift toward low-emission and environmentally safer coating solutions. OEM manufacturers increasingly adopted water-based technologies because they significantly reduce volatile organic compound emissions while still delivering strong color quality, smooth finish, and reliable coating performance. The technology remained highly preferred for base coat and primer applications, where consistency, appearance, and compliance with environmental regulations are equally important.

By Application Analysis

Passenger cars dominate the Automotive OEM Coatings Market with 74.9% share, fueled by high production volumes and stronger demand for premium finishes.

In 2025, Passenger Cars held a dominant market position, capturing more than a 74.9% share. This leading share was mainly supported by the consistently high production volume of passenger vehicles across both developed and emerging automotive markets. OEM coating demand remained strongest in this segment because passenger cars require advanced coating layers for visual appeal, corrosion protection, surface durability, and brand-specific styling. Automakers continued to invest heavily in premium exterior finishes, metallic shades, matte effects, and long-lasting clear coats to improve vehicle aesthetics and customer preference, which directly increased coating consumption in this category.

Key Market Segments

By Product

- Clear Coat

- Base Coat

- Primer

- E-coat

- Others

By Resin

- Polyurethane

- Acrylic

- Epoxy

- Others

By Technology

- Solvent-based

- Water-based

- Powder-based

- Others

By Application

- Passenger Cars

- Commercial Vehicles

Emerging Trends

Smart, Low-VOC Coating Technologies Are Emerging as the Latest Industry Trend

One of the most visible latest trends in the Automotive OEM Coatings market is the fast shift toward smart low-VOC and water-based coating systems integrated with automated paint shops. This trend is becoming stronger as automakers modernize production lines with robotics, AI-guided spray systems, and precision curing technologies that reduce paint waste and improve finish consistency.

A major reason behind this shift is the continued rise in electric vehicle production, where lightweight panels, battery casings, and mixed substrates need advanced coating chemistry. According to the International Energy Agency, electric car sales exceeded 17 million units in 2024, and are expected to cross 20 million units in 2025.

EV-Focused Specialty Finishes and Functional Layers Are Gaining Momentum

Another major trend is the rise of EV-focused specialty finishes and functional protective layers. Modern electric vehicles are increasingly using matte shades, satin metallic effects, anti-scratch clear coats, and thermal-management coatings for battery housings. The same IEA outlook shows that EV sales were already up 35% year-on-year in the first quarter of 2025, highlighting how quickly this design-led coating demand is growing.

Governments are also indirectly supporting this trend through EV incentives, clean mobility targets, and stricter fleet emission standards, especially in Europe, China, and India. As a result, OEM coating suppliers are now developing finishes that do more than decoration—they also improve heat resistance, UV durability, and surface protection for new lightweight materials.

Drivers

Rising Global Vehicle Production is the Core Growth Engine

One of the biggest driving factors for the Automotive OEM Coatings market is the steady rise in global vehicle production. Every new vehicle coming off an assembly line needs multiple coating layers, including e-coat, primer, base coat, and clear coat, which directly increases coating consumption. According to the International Organization of Motor Vehicle Manufacturers (OICA), global vehicle production crossed 92.5 million units in 2024, showing how strongly manufacturing activity is supporting coating demand worldwide.

This production momentum has been especially strong in passenger cars and electric vehicles, where appearance quality, corrosion resistance, and long-term durability are critical. As automakers expand manufacturing capacity in Asia-Pacific, Europe, and North America, OEM paint shops are seeing higher throughput, which naturally lifts demand for advanced coating systems.

Environmental Regulations and Water-Based Shift are Accelerating Demand

Another major growth driver is the stricter environmental regulation around volatile organic compound (VOC) emissions from automotive paint shops. Governments across Europe, the U.S., China, and India are pushing manufacturers toward cleaner industrial processes, which is rapidly increasing the adoption of water-based and low-VOC coating technologies. These rules are not only reducing emissions but also reshaping OEM coating line investments toward more sustainable formulations.

This shift is highly important because modern water-based coatings now offer strong color consistency, corrosion protection, and fast curing performance, making them suitable for large-scale vehicle production. In 2025 and 2026, automakers are also upgrading robotic paint systems and bake ovens to support these technologies at scale. As sustainability targets become stricter and EV manufacturing rises, the use of eco-friendly coatings is expected to increase further.

Restraints

Raw Material Price Volatility Remains a Major Barrier for Automotive OEM Coatings

One of the biggest restraining factors for the Automotive OEM Coatings market is the constant fluctuation in raw material prices. The industry depends heavily on titanium dioxide, polyurethane intermediates, epoxy resins, solvents, and specialty additives, all of which are closely linked to mining output, petrochemical feedstocks, and global energy costs.

A strong example is titanium dioxide, one of the most important white pigments used in automotive coatings. The U.S. Geological Survey notes that around 95% of titanium is consumed in the form of titanium dioxide pigment, widely used in paints and coatings.

Supply Chain and Energy Cost Pressure Slows Profitability

Another key restraint linked to the same issue is the impact of energy-driven supply chain costs on coating production. Automotive OEM coatings require controlled manufacturing conditions, resin synthesis, solvent recovery, and high-temperature curing support, all of which are energy intensive.

When fuel and industrial energy prices rise, the delivered cost of coating materials also increases. The U.S. Energy Information Administration regularly tracks diesel and fuel cost changes that directly affect freight and chemical transport economics.

Opportunity

Electric Vehicle Expansion is Creating the Biggest Growth Opportunity

One of the strongest growth opportunities for the Automotive OEM Coatings market is the rapid expansion of electric vehicle production worldwide. Every EV requires advanced lightweight coating systems that can protect mixed-material bodies, battery enclosures, and new design-focused exterior panels.

This is creating fresh demand for high-performance OEM coatings, especially for water-based base coats, low-temperature curing systems, and coatings designed for aluminum and composite substrates. According to the International Energy Agency, global electric car sales are expected to exceed 20 million units in 2025, representing more than one-quarter of total car sales worldwide.

Government EV Policies and India’s Push Add Long-Term Potential

Another major opportunity is the policy-led growth coming from emerging automotive manufacturing hubs, especially India. Government initiatives around EV adoption, local manufacturing, and emission reduction are encouraging automakers to expand production capacity, which directly supports OEM coating demand. A strong example is India, where EV sales increased from 50,000 units in 2016 to 2.08 million units in 2024, according to NITI Aayog and VAHAN-based data.

Regional Insights

Asia-Pacific dominated the Automotive OEM Coatings Market with 45.1% share, reaching USD 6.3 Billion, supported by unmatched vehicle production scale and rapid EV-led coating demand.

Asia-Pacific held the leading position in the Automotive OEM Coatings market, accounting for 45.1% of the global share and reaching USD 6.3 Billion. The region’s dominance is strongly linked to its massive automotive manufacturing base, led by China, India, Japan, and South Korea.

According to OICA, Asia continues to remain the center of global automotive production, with China alone producing 31.3 million vehicles in 2024, while India also reported strong annual production growth of nearly 4.7%, reinforcing the region’s coating consumption advantage.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BASF BASF remains one of the most influential players in automotive OEM coatings, backed by €68.9 billion in total group sales in 2025 and strong investments in performance materials and surface solutions. Its automotive coatings business benefits from deep expertise in electrocoat, primer, basecoat, and clearcoat technologies. The company’s numerical strength lies in its large global manufacturing network across 90+ countries, helping OEMs secure supply consistency.

Nippon Paint Holdings Nippon Paint stands out in Asia-Pacific automotive OEM coatings through its strong OEM partnerships and measurable sustainability gains. In 2025, its automotive coatings solutions demonstrated up to 71% CO₂ emission reduction, showing strong technological progress in low-energy curing and eco-efficient formulations.

AkzoNobel Akzo Nobel remains a major player in automotive OEM coatings through its performance coatings division and strong European OEM relationships. A key 2025 numerical highlight was its €1.4 billion India business transaction, which sharpened its focus toward industrial and automotive coatings expansion. The company continues to benefit from strong demand in powder coatings, water-based systems, and specialty clearcoats.

Top Key Players Outlook

- BASF SE

- PPG Industries Inc.

- Nippon Paints Holdings Co. Ltd

- Akzo Nobel N.V.

- Axalta Coating Systems Ltd

- Berger Paints India Ltd

- Kansai Paint Co. Ltd

- The Sherwin-Williams Company

- KCC Corporation

- Covestro AG

Recent Industry Developments

In 2025, BASF SE remained one of the most influential companies in the Automotive OEM Coatings sector, supported by its strong global coatings business scale and deep partnerships with leading vehicle manufacturers. The company’s coatings-related business generated around €3.8 billion in annual sales, with a major share coming from automotive OEM and refinish solutions, showing its strong numerical presence in this space.

In 2025, PPG Industries Inc. maintained a strong position in the Automotive OEM Coatings sector, supported by its global scale, advanced paint technologies, and deep relationships with major vehicle manufacturers. The company reported US$15.9 billion in total net sales for full-year 2025, showing the financial strength behind its coatings-led business model.

In 2025, Nippon Paint Holdings strengthened its position in the Automotive OEM Coatings sector with clear numerical growth and strong Asia-led OEM demand. The company reported ¥203.2 billion in FY2025 automotive coatings revenue, making automotive one of its core business segments and accounting for 11% of total FY2025 revenue mix.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 14.1 Bn |

| Forecast Revenue (2035) | USD 24.9 Bn |

| CAGR (2026-2035) | 5.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Clear Coat, Base Coat, Primer, E-coat, Others), By Resin (Polyurethane, Acrylic, Epoxy, Others), By Technology ( Solvent-based, Water-based, Powder-based, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | BASF SE, PPG Industries Inc., Nippon Paints Holdings Co. Ltd, Akzo Nobel N.V., Axalta Coating Systems Ltd, Berger Paints India Ltd, Kansai Paint Co. Ltd, The Sherwin-Williams Company, KCC Corporation, Covestro AG |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |