Quick Navigation

Report Overview

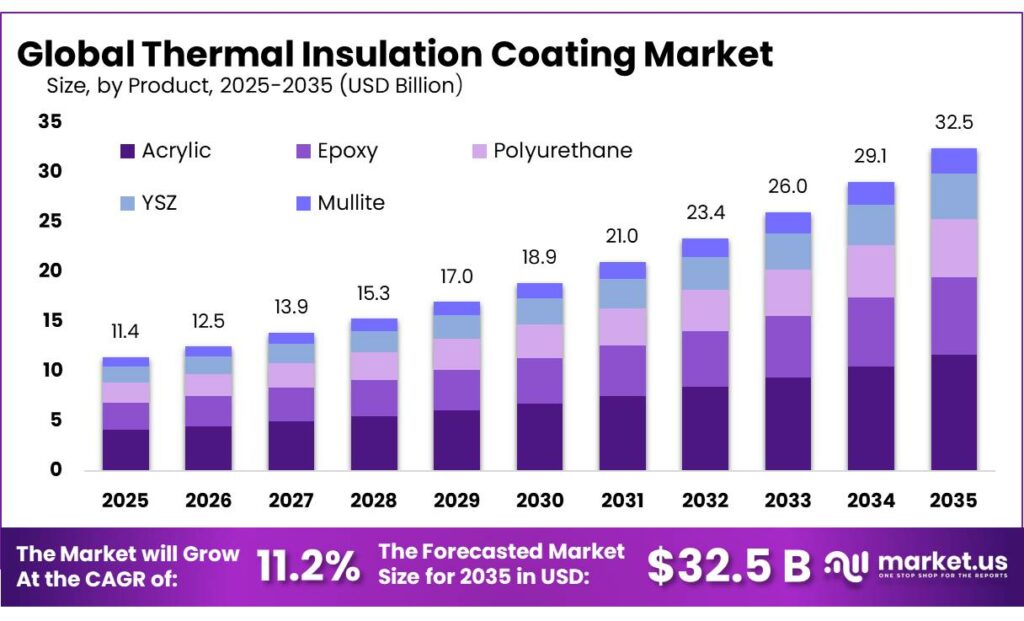

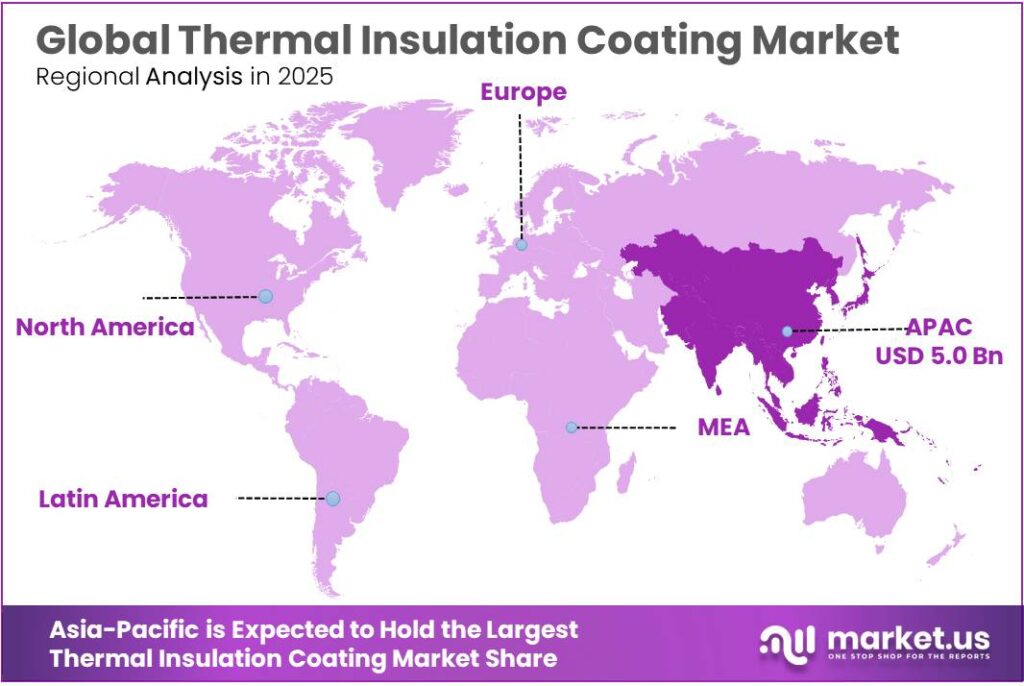

The Global Thermal Insulation Coating Market size is expected to be worth around USD 32.5 Billion by 2035, from USD 11.4 Billion in 2025, growing at a CAGR of 11.2% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 44.4% share, holding USD 5.0 Billion revenue.

The thermal insulation coating industry is positioned as a specialized energy-efficiency and asset-protection segment serving process industries, commercial infrastructure, transport equipment, and temperature-sensitive supply chains. Its value proposition is stronger where conventional lagging is difficult to install or maintain on complex geometries such as tanks, valves, ducts, vessels, and pipelines.

The industrial case remains compelling because the U.S. Department of Energy states that 20% to 50% of industrial energy input is lost as waste heat, while process heating is responsible for 63% of all manufacturing energy use in the United States. In that operating context, spray-applied insulation coatings are increasingly evaluated not only as heat-loss control materials, but also as tools for personnel protection, corrosion-under-insulation mitigation, and uptime improvement.

The current industrial scenario is being shaped by energy-cost pressure and tighter efficiency rules rather than by speculative demand alone. In the European Union, the revised Energy Efficiency Directive sets a binding target to reduce final energy consumption by 11.7% by 2030 versus 2020 projections, which supports investment in retrofit-oriented insulation solutions across factories and utility-intensive sites.

Energy economics also remain relevant: Eurostat reports that non-household electricity prices in the EU increased by 0.9% in the first half of 2025 versus the same period of 2024. That combination of regulation and operating-cost exposure is favorable for thermal insulation coatings, especially in facilities seeking lower heat loss without major shutdowns or bulky cladding systems.

A notable demand driver comes from food and beverage processing, where thermal control directly affects yield, hygiene, and refrigeration performance. FAO reports that 13.2% of food is lost in the supply chain before retail, while UNEP estimates that another 19% is wasted at retail, food service, and household level. FAO also notes that lack of effective refrigeration causes the loss of 526 million tonnes of food production, and that the food cold chain accounts for about 4% of global greenhouse gas emissions.

In parallel, Eurostat reported that the volume of EU retail trade in food, drinks, and tobacco rose by 0.5% year on year in September 2025, indicating continued throughput in downstream food systems. These numbers reinforce why processors, cold stores, and packaging lines continue to value coatings that reduce condensation, improve line safety, and stabilize thermal performance.

Policy direction remains supportive. In Europe, the revised Energy Efficiency Directive entered into force on 10 October 2023 and strengthened reporting and investment obligations around energy efficiency. In the United States, DOE’s Industrial Demonstrations Program explicitly includes food and beverage and process heat, while DOE announced more than $136 million for 66 industrial technology projects on 8 January 2025.

Key Takeaways

- Thermal Insulation Coating Market size is expected to be worth around USD 32.5 Billion by 2035, from USD 11.4 Billion in 2025, growing at a CAGR of 11.2%.

- Acrylic held a dominant market position, capturing more than a 36.7% share.

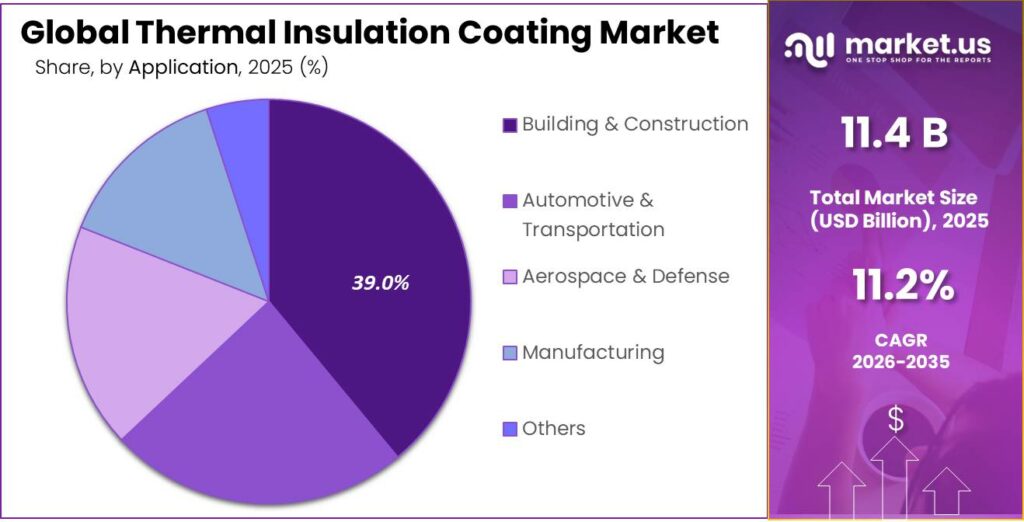

- Building & Construction held a dominant market position, capturing more than a 39.6% share.

- Asia-Pacific held the dominant position in the thermal insulation coating market, accounting for 44.4% of global revenue and reaching nearly USD 5.0 billion.

By Product Analysis

Acrylic dominates with 36.7% share, supported by strong weather resistance and broad use across building surfaces

In 2025, Acrylic held a dominant market position, capturing more than a 36.7% share in the thermal insulation coating market by product. This strong position was mainly supported by its wide use in residential, commercial, and industrial buildings where long-term surface protection and thermal efficiency are important. Acrylic-based coatings remained a preferred choice because they offer a good balance of durability, UV resistance, moisture protection, and easy application on different substrates such as concrete, metal, and exterior walls.

By Application Analysis

Building & Construction leads with 39.6% share, driven by rising demand for energy-efficient building envelopes

In 2025, Building & Construction held a dominant market position, capturing more than a 39.6% share in the thermal insulation coating market by application. This leading position was largely supported by the growing use of insulation coatings across residential towers, commercial spaces, warehouses, and public infrastructure projects where controlling indoor temperature and lowering energy costs remain key priorities. The segment saw strong demand as builders increasingly focused on improving roof, wall, and façade performance without adding significant structural weight.

Key Market Segments

By Product

- Acrylic

- Epoxy

- Polyurethane

- YSZ

- Mullite

By Application

- Building & Construction

- Automotive & Transportation

- Aerospace & Defense

- Manufacturing

- Others

Emerging Trends

Smart cool roof and nano-ceramic coatings are emerging as the latest market trend

One of the latest trends in the thermal insulation coating market is the rapid shift toward smart cool roof and nano-ceramic coating technologies. In 2025, the trend is strongly linked to the rising use of reflective roof coatings that lower roof surface temperatures and reduce cooling energy demand in urban buildings. According to the U.S. Department of Energy, conventional roofs can reach 150°F or more on hot summer afternoons, while cool roof systems are designed to reflect more sunlight and absorb far less heat.

A major trend extension is the move toward multi-functional coatings, where insulation, waterproofing, and UV protection are combined into a single layer. Recent industry developments show reflective and cool roof coating applications in commercial buildings alone were valued at USD 2.1 billion in 2024, showing how fast builders are shifting toward energy-efficient envelope systems.

Government-backed cool roof mandates and urban heat policies are shaping demand trends

Another major latest trend is the rise of city-level cool roof mandates and retrofit incentives, especially in heat-stressed urban regions. Governments are now moving beyond recommendations and directly integrating thermal reflective coatings into building bylaws. A strong recent example comes from Amravati, India, where new cool roof bylaws made reflective roof systems mandatory for selected new buildings. The city’s 2024 heat mapping study found surface temperatures touching 53.7°C, which accelerated policy adoption.

The same policy framework also introduced property tax rebates of up to 10% for certified retrofitted buildings, creating a direct financial push for thermal insulation coatings in both public and private infrastructure. This clearly shows that the latest market trend is no longer only product innovation, but also policy-led adoption through urban cooling programs.

Drivers

Rising building energy use is pushing demand for thermal insulation coatings

One of the biggest growth drivers for the thermal insulation coating market is the sharp rise in building energy use, especially from cooling needs. Buildings currently account for about 30% of global final energy consumption, making them one of the largest energy-using sectors worldwide. The International Energy Agency also notes that buildings constructed under modern energy codes can use up to 50% less energy, which is increasing the shift toward advanced insulation materials and reflective coatings.

In 2025, this trend became even stronger as governments pushed stricter building-efficiency targets and retrofit programs. Thermal insulation coatings are gaining fast acceptance because they help reduce indoor heat gain, improve wall and roof performance, and lower HVAC loads without major structural changes. This makes them especially useful in both old building renovation and new urban construction projects.

Government efficiency programs and retrofit incentives are accelerating adoption

Another major factor driving the thermal insulation coating market is the rapid expansion of government-led energy efficiency initiatives. In 2025, the IEA reported over 250 new or updated energy-efficiency policies introduced across countries representing 85% of global energy demand. This policy momentum is directly supporting demand for insulation coatings in public buildings, commercial spaces, and housing upgrades.

A strong example is the increasing use of building energy codes, retrofit grants, and cool roof regulations. According to IEA policy guidance, replacing inefficient systems and improving building envelopes can reduce energy use dramatically, while efficient building upgrades can lower long-term emissions by more than 95% by 2050 when combined with electrification and low-carbon power.

Restraints

High upfront material and application cost remains a major barrier

One of the biggest restraining factors for the thermal insulation coating market is the high initial cost of premium coating materials and specialized application work. According to the UNEP Global Status Report for Buildings and Construction 2024/2025, the sector is still facing financing gaps even though buildings account for a major share of global energy demand, and limited capital flow continues to slow the adoption of advanced efficiency materials.

In 2025, this cost pressure became more visible in retrofit projects, especially across older commercial buildings where substrate repair and skilled labor added further expense before coating application even began. Many building owners still prefer lower-cost traditional insulation options because the payback period of thermal coatings can feel longer at the procurement stage.

Budget constraints in public retrofit programs slow wider penetration

Another important restraint is the limited budget availability in government and public infrastructure retrofit programs. While trusted organizations like the IEA continue to promote building upgrades, the 2025 Breakthrough Agenda highlights that efficiency gains are often offset by rising climate-control demand and slow modernization of building stock.

In schools, hospitals, warehouses, and municipal buildings, procurement teams often focus on immediate capital expenditure rather than lifecycle savings. This reduces adoption speed, particularly in emerging economies where public renovation budgets are already stretched by rising cement, steel, and labor costs.

Opportunity

Retrofit-led building upgrades are creating the biggest growth opportunity

One of the strongest growth opportunities for the thermal insulation coating market is the massive global push toward building retrofits and renovation of existing structures. Trusted energy agencies highlight that in advanced economies, nearly 80% of the buildings that will exist in 2050 are already built, which means the biggest opportunity now lies in upgrading old roofs, walls, pipelines, and facades rather than relying only on new construction.

Government-backed retrofit grants and building efficiency codes are making this opportunity even stronger in 2025 and 2026. The IEA notes that countries are targeting a doubling of global building retrofit rates by 2030, while incentive schemes are actively lowering upfront upgrade costs for energy-saving materials.

Smart cooling materials and heat-resilient construction open new demand

Another major opportunity is the rise of smart cooling materials and climate-resilient building design, especially in hot regions where cooling demand is growing rapidly. In fact, advanced materials research has already identified more than 130,000 experimentally reported MOF structures for temperature and moisture control applications, showing how fast thermal management innovation is expanding.

This trend creates a clear opening for next-generation thermal insulation coatings that combine reflective, moisture-control, and passive cooling functions. Governments are also supporting this shift through net-zero building pathways and renovation programs. Recent policy outlooks linked to future-ready buildings emphasize insulation upgrades, passive cooling, and heat-resilient envelopes as key interventions for managing rising electricity demand.

Regional Insights

Asia-Pacific dominates the thermal insulation coating market with 44.4% share, reaching USD 5.0 billion on strong construction and energy-efficiency demand

Asia-Pacific held the dominant position in the thermal insulation coating market, accounting for 44.4% of global revenue and reaching nearly USD 5.0 billion, making it the leading regional market in 2025. This strong regional lead is mainly supported by rapid urban construction, expanding industrial infrastructure, and rising energy-efficiency regulations across China, India, Japan, South Korea, and Southeast Asia.

The region continues to benefit from large-scale demand for thermal control solutions in residential towers, logistics parks, factories, warehouses, and commercial buildings where cooling efficiency is becoming a major cost concern. The broader regional market outlook also supports this trend, with Asia-Pacific thermal insulation coating revenue expected to reach USD 5,304.6 million by 2030, advancing at a 7.1% CAGR from 2025 to 2030.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Evonik Industries AG remains a technology-driven specialty chemicals leader with a strong role in advanced additives used in thermal insulation coating formulations, especially in acrylic, silica, and energy-efficient surface technologies. In 2025, the company continued strengthening innovation-led coating solutions, backed by its €1.5 billion additional sales target by 2032 from innovation growth areas. Its strong R&D spending and global production footprint across 100+ countries support premium thermal barrier coating materials for industrial and construction use.

Akzo Nobel N.V. remains one of the strongest global coating companies, supported by €10.7 billion revenue scale across decorative paints and performance coatings. Its thermal insulation coating exposure comes through high-performance industrial coatings, cool roof systems, and energy-saving building envelope technologies. In 2025, the company continued leveraging its strong decorative and industrial brands to support demand from commercial infrastructure and industrial maintenance projects.

Top Key Players Outlook

- Evonik Industries AG

- Mascoat

- Carboline

- Nippon Paint Holdings Co., Ltd.

- Akzo Nobel N.V.

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Kansai Paint Co., Ltd.

- Grand Polycoats Company Pvt. Ltd.

- Sika AG

Recent Industry Developments

Evonik reported €14.1 billion in total revenue in 2025, with operations in more than 100 countries and production facilities across 27 countries, giving it a strong global supply base for insulation-related coating raw materials.

AkzoNobel reported €10,158 million in total revenue in 2025, including €6,068 million from Performance Coatings and €4,090 million from Decorative Paints, both highly relevant to insulation and reflective coating applications. The company also delivered €1,444 million adjusted EBITDA with a 14.2% margin, showing strong financial support for product innovation and thermal management solutions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 11.4 Bn |

| Forecast Revenue (2035) | USD 32.5 Bn |

| CAGR (2026-2035) | 11.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Acrylic, Epoxy, Polyurethane, YSZ, Mullite), By Application (Building And Construction, Automotive And Transportation, Aerospace And Defense, Manufacturing, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Evonik Industries AG, Mascoat, Carboline, Nippon Paint Holdings Co., Ltd., Akzo Nobel N.V., PPG Industries, Inc., The Sherwin-Williams Company, Kansai Paint Co., Ltd., Grand Polycoats Company Pvt. Ltd., Sika AG |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |