Quick Navigation

Report Overview

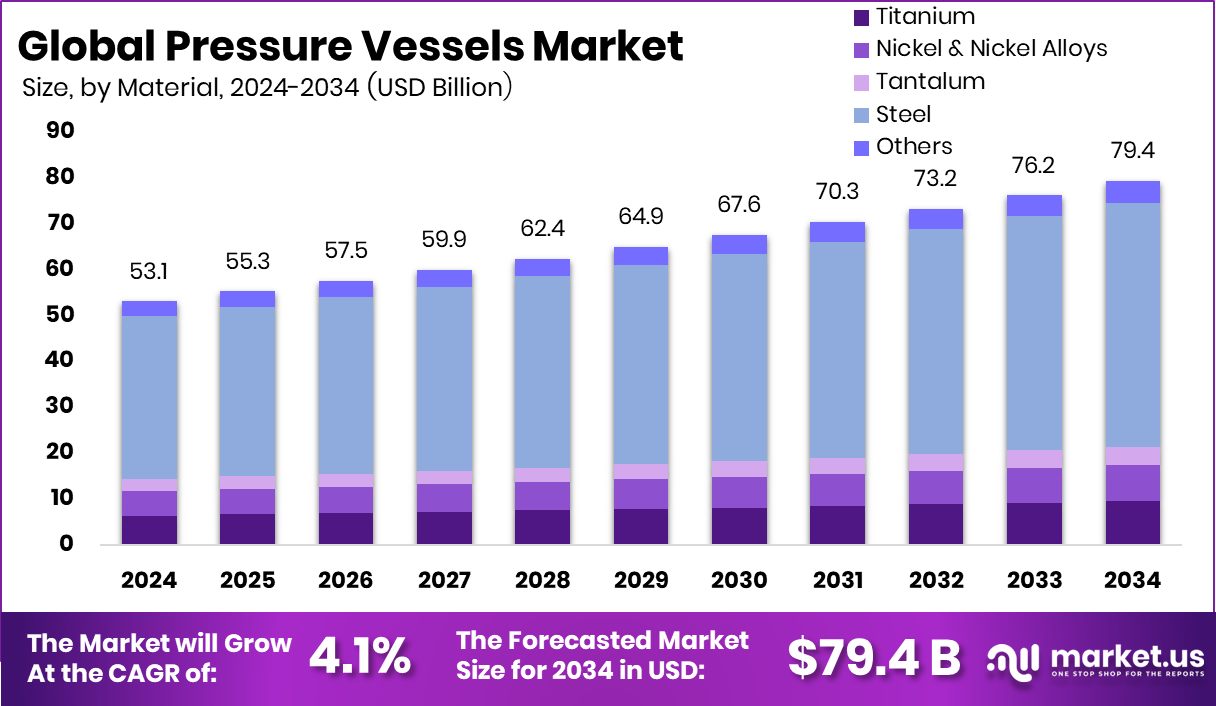

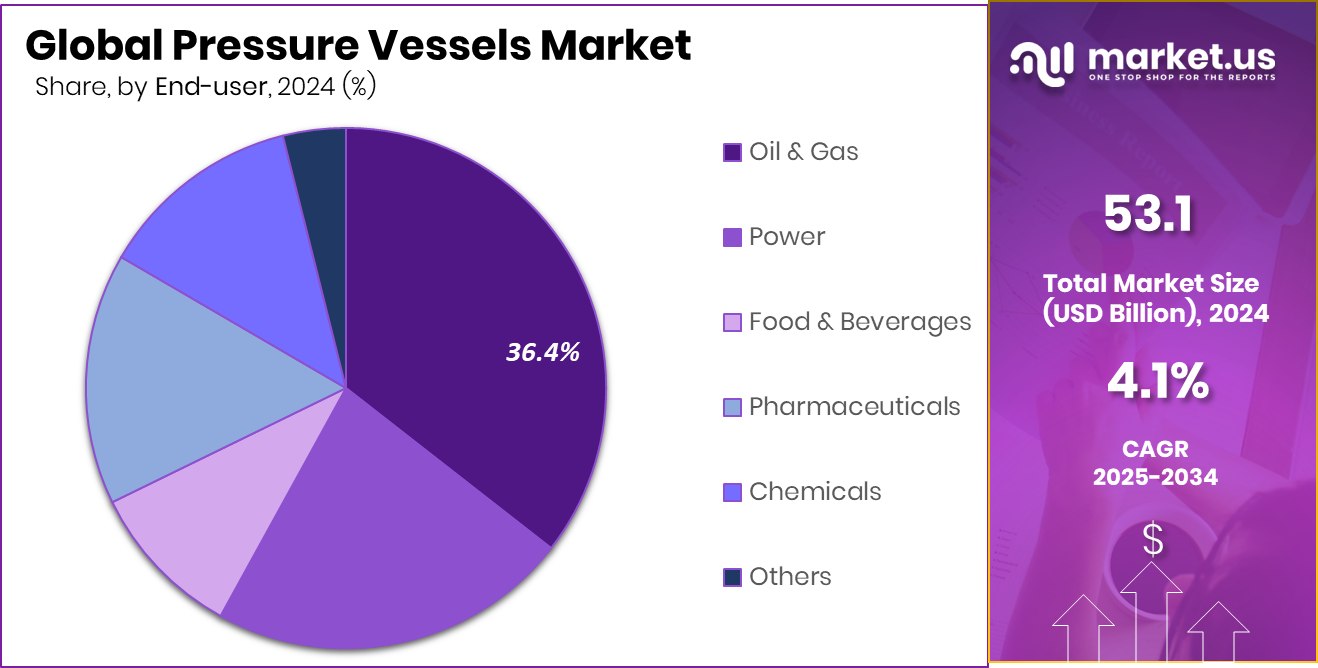

Global Pressure Vessels Market is expected to be worth around USD 79.4 Billion by 2034, up from USD 53.1 Billion in 2024, and grow at a CAGR of 4.1% from 2025 to 2034. With a 43.8% share, Asia-Pacific remained the top region in the pressure vessels market.

Pressure vessels are closed containers designed to hold gases or liquids at a pressure significantly different from ambient pressure. They are commonly used in industries such as oil & gas, chemical processing, power generation, and water treatment. These vessels must adhere to strict engineering standards to ensure safety and reliability, as failure can lead to catastrophic accidents. Depending on the application, pressure vessels can be cylindrical, spherical, or custom-shaped, made from materials like steel, stainless steel, or composite materials to withstand internal and external pressure stresses.

The pressure vessels market refers to the global demand, production, and supply of these containers across different sectors. It includes all associated design, manufacturing, installation, and maintenance services. Growth in this market is largely influenced by expansion in process industries, energy needs, and regulations for safe industrial operations. Governments’ focus on sustainable power and industrial safety drives investment in advanced pressure vessel technologies, making the market essential in energy, chemicals, and infrastructure development.

The pressure vessels market is growing due to increasing global investments in energy infrastructure. With nations expanding their power grids and renewable energy systems, pressure vessels are in high demand for managing high-pressure fluids in both conventional and clean energy plants. Thermal, nuclear, and hydropower setups rely heavily on these vessels to ensure process continuity and safety.

Industrial growth in emerging countries is pushing demand for pressure vessels. As sectors like chemicals, pharmaceuticals, and petrochemicals expand in Asia, Africa, and Latin America, the need for equipment that can safely store and transport pressurized materials increases. These industries rely on pressure vessels for reactor operations, storage, and process efficiency.

Key Takeaways

- Global Pressure Vessels Market is expected to be worth around USD 79.4 Billion by 2034, up from USD 53.1 Billion in 2024, and grow at a CAGR of 4.1% from 2025 to 2034.

- In the pressure vessels market, steel held a 67.3% share due to durability and high-pressure resistance.

- Unfired pressure vessels dominated with a 78.1% share in the Pressure Vessels Market owing to broad industrial use.

- Processing vessels accounted for 57.2% of the Pressure Vessels Market due to demand in chemical operations.

- The oil and gas sector led the Pressure Vessels Market with a 36.4% share, driven by extraction and refining.

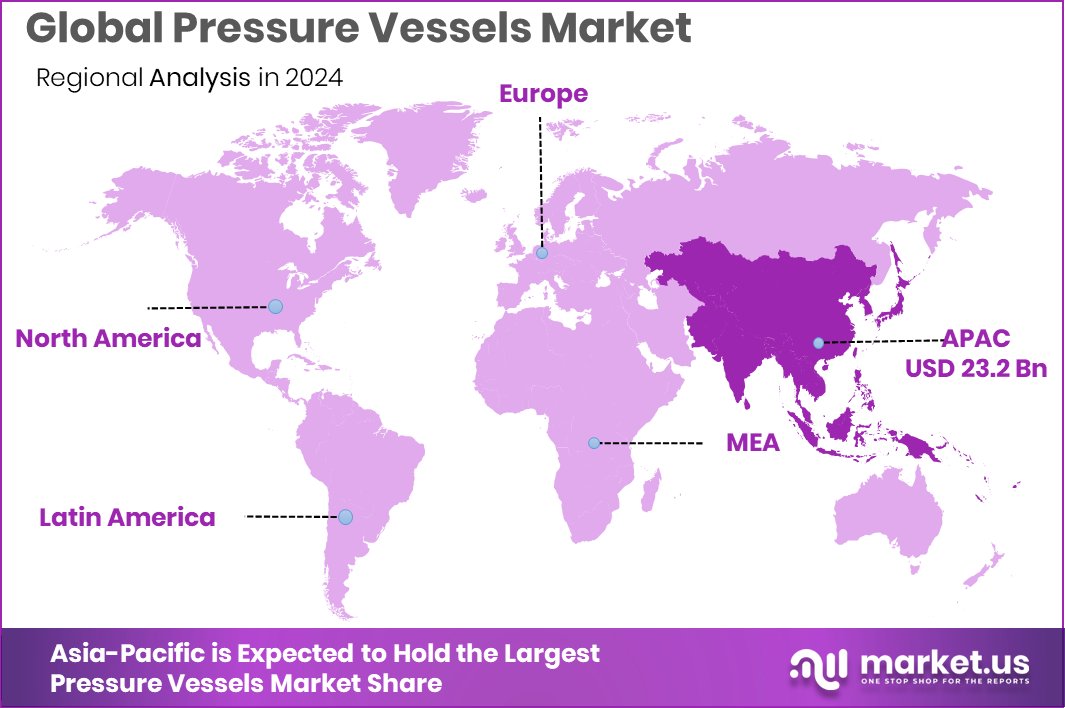

- Rapid industrialization in Asia-Pacific boosted pressure vessel demand to USD 23.2 Bn.

By Material Analysis

In the Pressure Vessels Market, steel held a 67.3% share due to durability.

In 2024, Steel held a dominant market position in the By Material segment of the Pressure Vessels Market, with a 67.3% share. This dominance is attributed to steel’s high strength, durability, and proven performance in handling high-pressure applications across various industries. Steel is widely preferred for its ability to withstand extreme temperatures and corrosion, making it suitable for sectors such as oil & gas, power generation, and chemical processing.

Its structural integrity under both internal and external pressure conditions ensures reliability and long service life, which reduces maintenance costs and operational risks. Furthermore, steel’s versatility in fabrication and welding supports customized designs for industrial needs, enhancing its adoption rate. The availability of different steel grades, including carbon steel and stainless steel, also contributes to its wide usage across diverse pressure vessel requirements.

With industries increasingly prioritizing safety and compliance with pressure containment standards, steel remains the most trusted and regulated material for manufacturing these units. The continued infrastructure development and industrial growth, especially in energy-related projects, further supported the strong demand for steel-based pressure vessels in 2024, reinforcing its leading market share.

By Heat Source Analysis

Unfired Pressure Vessels dominated with a 78.1% share for safer industrial operations.

In 2024, Unfired Pressure Vessels held a dominant market position in the By Heat Source segment of the Pressure Vessels Market, with a 78.1% share. This significant share highlights the widespread use of unfired vessels in industrial applications where indirect heat sources are utilized. These vessels do not contain internal combustion or direct flame heating, making them suitable for the storage and processing of gases and liquids under pressure without the added complexity of heat integration.

Their structural simplicity, lower operational risks, and compliance with safety standards have made them a preferred choice across industries. The high adoption rate is also driven by their cost-effectiveness in terms of manufacturing and maintenance. Unfired pressure vessels are commonly deployed in chemical processing, water treatment, and oil refining systems, where controlled environments are crucial.

Their design flexibility allows easy customization based on pressure ratings and volume needs, making them versatile in multiple engineering setups. In 2024, the strong reliance on process containment, storage, and safety in critical sectors further strengthened the demand for unfired vessels.

By Application Analysis

Processing Vessels led application segment, capturing 57.2% share in the global market.

In 2024, Processing Vessels held a dominant market position in the By Application segment of the Pressure Vessels Market, with a 78.1% share. This strong market presence highlights the essential role of processing vessels in handling chemical reactions, mixing, and intermediate containment in industrial processes. Their high-pressure resistance and robust construction make them ideal for continuous processing environments, where maintaining consistent operating conditions is critical.

Industries such as oil refining, chemical manufacturing, and food processing rely heavily on these vessels to ensure product quality, safety, and efficiency. The 78.1% share demonstrates the widespread dependence on processing vessels to support large-scale operations that demand precise control over temperature and pressure. Their adaptability to various sizes and configurations adds to their appeal, enabling deployment across both batch and continuous production lines.

In 2024, the consistent growth in industrial activity and rising demand for controlled production environments significantly boosted the use of processing vessels. Their ability to enhance throughput while maintaining safety and quality standards played a key role in cementing their dominant position within the application segment of the pressure vessels market.

By End-user Analysis

The oil and Gas industry accounted for a 36.4% share in the end-user segment.

In 2024, Oil and Gas held a dominant market position in the By End-user segment of the Pressure Vessels Market, with a 36.4% share. This leadership is driven by the sector’s continuous demand for reliable equipment capable of handling high-pressure fluids and gases during extraction, refining, and transportation processes.

Pressure vessels are integral in various stages of oil and gas operations, including separation, gas treatment, and chemical injection, where maintaining pressure integrity is vital. The 36.4% share reflects the industry’s heavy reliance on such vessels for operational safety, regulatory compliance, and efficiency in both upstream and downstream activities. In 2024, ongoing exploration projects and refinery expansions further supported the increased adoption of pressure vessels across the oil and gas landscape.

Their proven performance in harsh and high-risk environments reinforces their value in maintaining production continuity and minimizing downtime. The focus on optimizing process safety and extending asset life also contributed to greater investment in pressure vessel systems.

Key Market Segments

By Material

- Titanium

- Nickel and Nickel Alloys

- Tantalum

- Steel

- Carbon Steel

- Stainless Steel

- Others

By Heat Source

- Fired Pressure Vessels

- Unfired Pressure Vessels

By Application

- Storage Vessels

- Processing Vessels

By End-user

- Oil and Gas

- Power

- Food and Beverages

- Pharmaceuticals

- Chemicals

Driving Factors

Growing Energy Demand Driving Equipment Installations Globally

As global energy demand keeps rising, pressure vessels are needed more than ever. Power plants, oil refineries, and industrial facilities rely on these vessels to store and handle pressurized gases and liquids safely. With countries investing in new thermal and nuclear power stations, the need for robust and durable vessels has increased. These vessels ensure safety and smooth operations, especially in high-pressure environments.

Developing economies are expanding their energy infrastructure, while advanced nations are upgrading old systems. This leads to steady pressure vessel installations worldwide. Whether for gas storage, steam generation, or chemical processing, the growing need for reliable energy drives pressure vessel usage. It continues to be a key factor behind the market’s growth.

Restraining Factors

Strict Safety Rules Increase Design and Cost

Pressure vessels must follow very strict safety rules and design standards. These rules are important because any failure can lead to explosions or serious accidents. But following all the safety codes makes the design process very complex and expensive. Every vessel needs to pass many tests and approvals before it can be used.

This increases the cost and time needed to manufacture and install them. Smaller manufacturers may struggle to keep up with these demands. Also, updating existing systems to meet new regulations can be costly. These strict rules, while necessary for safety, slow down production and make it harder for companies to quickly expand or offer cheaper pressure vessels in the market.

Growth Opportunity

Hydrogen Storage Offers High‑Growth Future Potential

As industries shift toward clean energy, storing hydrogen safely becomes essential, and that needs advanced pressure vessels. Hydrogen must be kept under high pressure, requiring vessels that are strong, leak-proof, and lightweight. This creates a big opportunity for manufacturers to innovate with new materials and designs tailored for hydrogen use.

With global efforts to decarbonize and support hydrogen-powered transportation, industrial energy, and power generation, demand for these specialized vessels is expected to grow significantly. Companies that can deliver reliable, cost-effective hydrogen storage solutions stand to capture this expanding market.

Latest Trends

Smart Monitoring Systems Now Used in Vessels

One of the latest trends in the pressure vessels market is the use of smart monitoring systems. These systems include sensors that track temperature, pressure, and stress in real time. They help detect early signs of wear, corrosion, or leakage before major problems occur. This reduces downtime and improves safety. Operators can view live data on screens or mobile devices, making it easier to manage vessel performance remotely.

Industries are adopting these technologies to avoid accidents, lower maintenance costs, and extend equipment life. As digital tools become more affordable, more companies are adding smart features to their pressure vessels. This trend shows how the market is moving toward safer, data-driven, and more efficient industrial systems.

Regional Analysis

Asia-Pacific led the pressure vessels market with 43.8% share, valued at USD 23.2 Bn.

In 2024, Asia-Pacific held a dominant position in the global Pressure Vessels Market, accounting for 43.8% of the total share and reaching a value of USD 23.2 billion. This leading position is primarily driven by large-scale industrialization, rising energy consumption, and expanding petrochemical infrastructure across major countries in the region. Nations such as China, India, South Korea, and Japan continue to invest in power generation and oil refining, increasing the deployment of pressure vessels in these sectors.

North America and Europe followed, supported by the presence of established process industries and the ongoing modernization of energy infrastructure. However, their share remained below Asia-Pacific. Meanwhile, the Middle East & Africa and Latin America showed steady demand, particularly from oil-rich economies and developing industrial zones. These regions contribute to the global market with growing applications in gas storage, thermal power, and water treatment facilities.

Although their current market value is relatively lower compared to other regions, the presence of untapped industrial potential suggests future growth. Overall, the dominance of Asia-Pacific reflects its strong manufacturing base and investment momentum, solidifying its role as the central hub of global pressure vessel demand in 2024.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, IHI Corporation maintained a strong presence in the global pressure vessels market, leveraging its engineering depth and large-scale project capabilities. Known for its high-pressure solutions across power generation and process industries, IHI focused on supplying pressure vessels suited for advanced applications such as liquefied gas storage and energy infrastructure. Its ability to manufacture large, custom-designed vessels aligned well with the demand for reliability and performance in the energy and petrochemical sectors.

Babcock & Wilcox Enterprises, Inc. remained a notable player in 2024, particularly in markets focused on clean energy and utility-scale boilers. Their pressure vessel offerings are integrated within thermal and waste-to-energy systems, making them well-positioned to serve the needs of power producers aiming for efficiency and environmental compliance. Their U.S.-based manufacturing base and experience with high-pressure steam systems provided a competitive edge in North America and selected overseas projects.

Pressure Vessels (India) demonstrated significant growth potential in 2024, benefiting from increasing industrialization and infrastructure development across Asia. The company’s focus on cost-effective, high-quality fabrication positioned it well in price-sensitive markets. With India expanding its refining and chemical processing sectors, the company capitalized on local demand and slowly increased visibility in export markets.

Top Key Players in the Market

- IHI Corporation

- Babcock & Wilcox Enterprises, Inc.

- Pressure Vessels (India)

- MITSUBISHI HEAVY INDUSTRIES, LTD.

- Samuel, Son & Co.

- Alloy Products Corp.

- Abbott Pressure Vessels

- Doosan Corporation

- Bharat Heavy Electricals Limited

- LARSEN & TOUBRO LIMITED

- MERSEN PROPERTY

- Xylem

- Tinita Engg Pvt. Ltd

Recent Developments

- In April 2024, Babcock & Wilcox’s Renewable Service division received a contract worth over USD 7 million to upgrade three municipal and commercial waste‑to‑energy boilers in Southeast Asia.

- By March 2024, IHI had advanced its welding and fabrication technology for the reactor pressure vessels in the NuScale VOYGR small modular reactor (SMR). This includes lightweight yet robust containment vessels—the core of SMR design—and improvements like laser and arc welding to meet stringent safety standards.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 53.1 Billion |

| Forecast Revenue (2034) | USD 79.4 Billion |

| CAGR (2025-2034) | 4.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material (Titanium, Nickel and Nickel Alloys, Tantalum, Steel, (Carbon Steel, Stainless Steel), Others), By Heat Source (Fired Pressure Vessels, Unfired Pressure Vessels), By Application (Storage Vessels, Processing Vessels), By End-user (Oil and Gas, Power, Food and Beverages, Pharmaceuticals, Chemicals) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | IHI Corporation, Babcock & Wilcox Enterprises, Inc., Pressure Vessels (India), MITSUBISHI HEAVY INDUSTRIES, LTD., Samuel, Son & Co., Alloy Products Corp., Abbott Pressure Vessels, Doosan Corporation, Bharat Heavy Electricals Limited, LARSEN & TOUBRO LIMITED, MERSEN PROPERTY, Xylem, Tinita Engg Pvt. Ltd |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |