Quick Navigation

Report Overview

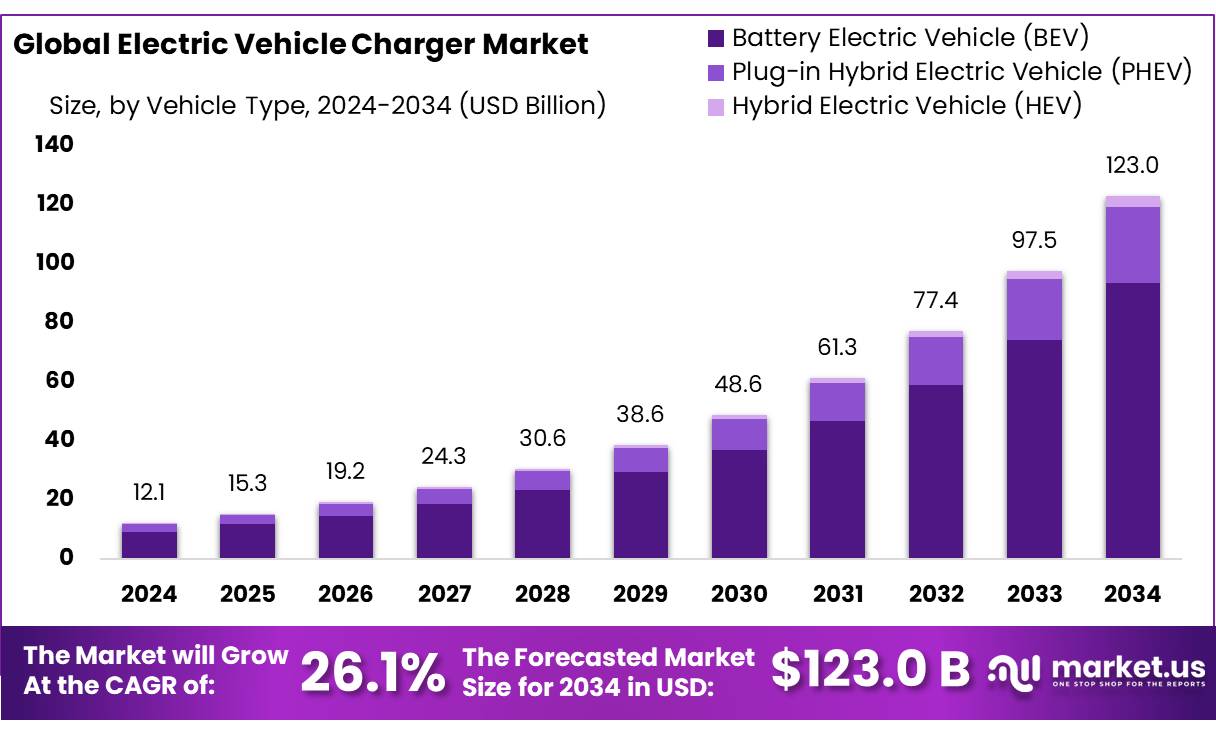

The Global Electric Vehicle Charger Market size is expected to be worth around USD 123.0 Billion by 2034, from USD 12.1 Billion in 2024, growing at a CAGR of 26.1% during the forecast period from 2025 to 2034.

The electric vehicle (EV) charging infrastructure sector in India is experiencing significant growth, driven by robust policy support, increasing EV adoption, and strategic investments in public and private charging networks. This expansion is integral to India’s broader objectives of reducing carbon emissions and achieving sustainable transportation.

Under the Faster Adoption and Manufacturing of Hybrid and Electric Vehicles (FAME) II scheme, the Indian government allocated ₹1,000 crore to develop EV charging infrastructure. This funding facilitated the sanctioning of 2,636 charging stations across 62 cities in 24 states and union territories, along with 1,544 stations along highways. The Ministry of Power’s guidelines mandate the installation of at least one public charging station within every 3 km x 3 km grid in urban areas and every 25 km on both sides of highways.

State governments are also implementing initiatives to enhance EV infrastructure. Delhi’s new EV policy aims to establish affordable, fast-charging stations every 5 km, particularly along the Outer Ring Road, and plans to create at least 20,000 new jobs through the expansion of the EV charging ecosystem. Maharashtra has announced a five-year toll exemption for EVs on major expressways and plans to install charging stations every 25 km on state and national highways.

The central government is further supporting EV adoption through the PM E-DRIVE scheme, which allocates ₹10,900 crore for subsidies on various electric vehicles, including two-wheelers, three-wheelers, ambulances, and trucks.

Key Takeaways

- Electric Vehicle Charger Market size is expected to be worth around USD 123.0 Billion by 2034, from USD 12.1 Billion in 2024, growing at a CAGR of 26.1%.

- Battery Electric Vehicle (BEV) held a dominant market position, capturing more than a 76.2% share in the electric vehicle charger market.

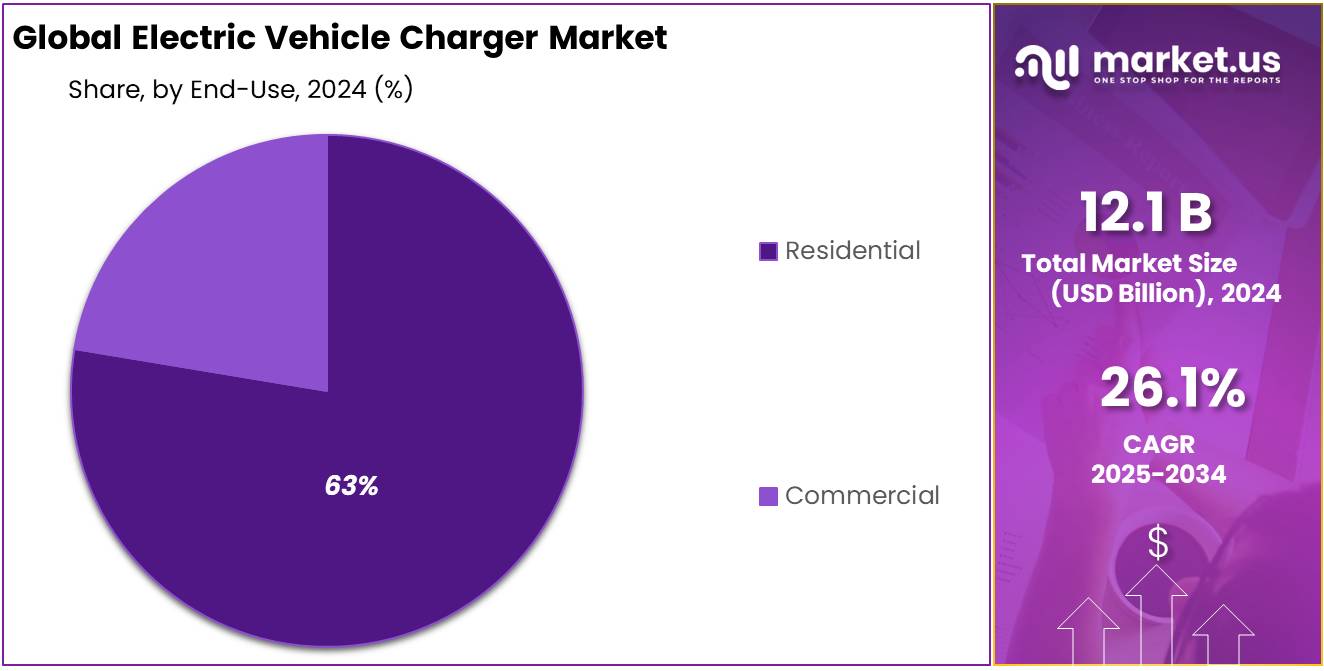

- Residential held a dominant market position, capturing more than a 62.8% share in the electric vehicle charger market.

- Off-board Chargers held a dominant market position, capturing more than a 72.4% share in the electric vehicle charger market.

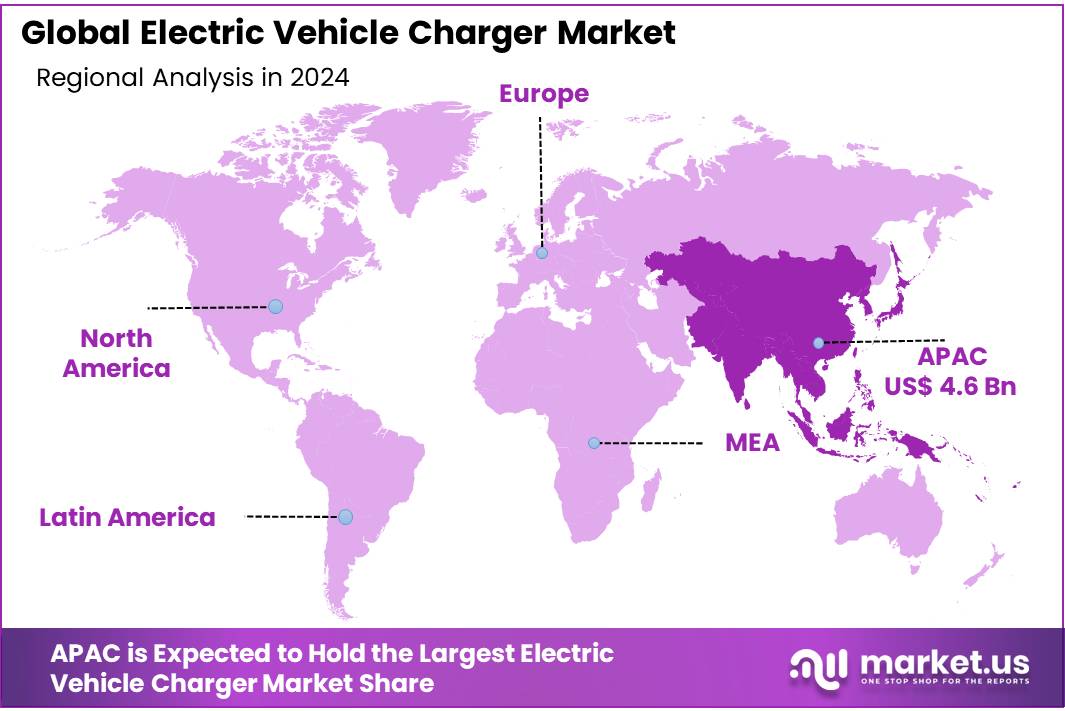

- Asia-Pacific (APAC) region held a dominant position in the global electric vehicle (EV) charger market, capturing 38.40% of the total market share, which translated to a valuation of approximately USD 4.6 billion.

By Vehicle Type

Battery Electric Vehicle (BEV) dominates with 76.2% share in 2024 due to rising demand for zero-emission mobility.

In 2024, Battery Electric Vehicle (BEV) held a dominant market position, capturing more than a 76.2% share in the electric vehicle charger market by vehicle type. This significant lead is largely driven by strong policy incentives for cleaner transportation, expanding charging infrastructure, and growing consumer preference for zero-emission vehicles.

BEVs benefit from higher energy efficiency and lower operating costs compared to hybrid alternatives, which further attracts fleet operators and individual buyers. With national and state-level subsidies continuing through 2024 and the steady decline in battery costs, BEV adoption is rising sharply. As a result, the demand for compatible EV chargers—particularly fast-charging stations—has grown in parallel, reinforcing the segment’s leadership within the charger market.

By End User

Residential segment dominates with 62.8% in 2024 as home charging becomes the preferred choice for EV users.

In 2024, Residential held a dominant market position, capturing more than a 62.8% share in the electric vehicle charger market by end user. This strong presence is primarily driven by the rising number of personal electric vehicle purchases, particularly in urban and suburban regions where users prefer the convenience of overnight home charging.

As more homeowners install Level 1 and Level 2 chargers, often supported by local utility rebates and tax incentives, the adoption curve continues to rise. The residential segment is further supported by smart home integration features and user-friendly mobile apps, making charging management easier and more efficient. With EV ownership steadily increasing in 2024 and charger installation becoming more affordable, the residential segment remains the backbone of EV charging demand.

By Charging Type

Off-board Chargers dominate with 72.4% share in 2024 due to their faster charging and widespread public use.

In 2024, Off-board Chargers held a dominant market position, capturing more than a 72.4% share in the electric vehicle charger market by charging type. These chargers are widely used in public and commercial spaces, offering higher power output and faster charging times compared to on-board systems. Their popularity is especially strong among fleet operators, highway service stations, and urban public charging networks, where quick turnaround is essential.

As electric vehicle adoption continues to rise and long-distance travel becomes more common, the need for rapid, high-capacity charging infrastructure has made off-board systems the preferred solution. The government’s support for DC fast-charging installations and the increasing number of high-powered EV models in 2024 have further strengthened the demand for off-board chargers, securing their lead in the market.

Key Market Segments

By Vehicle Type

- Battery Electric Vehicle (BEV)

- Plug-in Hybrid Electric Vehicle (PHEV)

- Hybrid Electric Vehicle (HEV)

By End User

- Residential

- Commercial

By Charging Type

- On-board Chargers

- Off-board Chargers

Drivers

Government Initiatives Fueling EV Charger Market Growth

One of the key drivers propelling the electric vehicle (EV) charger market is the Indian government’s robust policy support aimed at expanding charging infrastructure. Recognizing the pivotal role of accessible charging stations in accelerating EV adoption, several initiatives have been launched to address infrastructure gaps.

State governments have also introduced policies to bolster EV infrastructure. For instance, the Delhi government’s new EV policy aims to establish affordable, fast-charging stations every 5 km, particularly along the Outer Ring Road, and plans to create at least 20,000 new jobs through the expansion of the EV charging ecosystem. Similarly, Maharashtra has announced a five-year toll exemption for EVs on major expressways and plans to install charging stations every 25 km on state and national highways.

Furthermore, the central government’s PM E-DRIVE scheme allocates ₹10,900 crore ($1.3 billion) for subsidies on various electric vehicles, including two-wheelers, three-wheelers, ambulances, and trucks. This includes ₹5,000 crore specifically for e-ambulances and ₹5,000 crore for incentivizing the replacement of polluting trucks with e-trucks.

Restraints

Grid Limitations Pose Challenges to EV Charger Expansion

One significant challenge facing the electric vehicle (EV) charger market in India is the strain on the existing power grid infrastructure. As the adoption of EVs accelerates, the demand for electricity to power charging stations increases correspondingly. However, the current grid infrastructure, particularly at the distribution level, is not uniformly equipped to handle this additional load.

According to a report by NITI Aayog, the integration of EV charging infrastructure with the distribution grid presents several challenges, including the need for substantial upgrades to existing systems to accommodate the increased load and ensure reliable power supply to charging stations. The report emphasizes the importance of strategic planning and investment in grid infrastructure to support the growing EV ecosystem.

Furthermore, the report highlights that without proper integration and planning, the increased load from EV charging could lead to grid instability, voltage fluctuations, and potential power outages. This underscores the necessity for coordinated efforts between various stakeholders, including government agencies, power distribution companies, and private sector participants, to develop and implement comprehensive strategies for grid enhancement and EV charger deployment.

Opportunity

Expanding Public Charging Infrastructure

India’s electric vehicle (EV) sector is witnessing rapid growth, with a significant emphasis on enhancing public charging infrastructure to support this expansion. As of December 2024, the country had established 25,202 public charging stations, a substantial increase from previous years. This development is crucial in addressing range anxiety and promoting the adoption of EVs across the nation.

The government’s commitment to this cause is evident through initiatives like the PM E-DRIVE scheme, which allocated ₹2,000 crore specifically for the development of public charging stations. This funding aims to accelerate the deployment of charging infrastructure, ensuring that EV users have convenient access to charging facilities.

State governments are also playing a pivotal role. For instance, Maharashtra’s Electric Vehicle Policy 2025 includes plans to install EV charging stations every 25 km on state and national highways, facilitating long-distance travel for EV users. Similarly, Uttar Pradesh inaugurated its first solar-powered EV charging station in Banthra, highlighting a move towards sustainable energy sources for charging infrastructure.

These concerted efforts by both central and state governments, coupled with private sector participation, are creating a robust ecosystem for EV charging infrastructure. The expansion of public charging stations not only supports the growing number of EVs on the road but also contributes to environmental goals by promoting cleaner transportation options.

Trends

Integration of Renewable Energy into EV Charging Infrastructure

A significant trend shaping India’s electric vehicle (EV) charger market is the integration of renewable energy sources, particularly solar power, into charging infrastructure. This approach not only addresses environmental concerns but also enhances the sustainability and resilience of the EV ecosystem.

In a notable development, Uttar Pradesh inaugurated its first solar-powered EV charging station in Banthra, Sarojininagar constituency. This initiative aligns with the state’s broader goal of expanding its solar energy capacity from 288 MW in 2017 to 22,000 MW by 2030, as part of its commitment to sustainable energy solutions. The integration of solar power into EV charging stations is seen as a strategic move to reduce dependence on conventional energy sources and lower carbon emissions.

The central government is also actively promoting the use of renewable energy in EV infrastructure. Under the Faster Adoption and Manufacturing of Hybrid and Electric Vehicles (FAME) II scheme, the government has allocated substantial funds to support the development of charging stations powered by renewable sources. This initiative aims to create a robust and green charging network across the country, facilitating the transition to electric mobility.

Furthermore, the integration of renewable energy into EV charging infrastructure is expected to alleviate the load on the national grid, especially during peak hours. By harnessing solar power, charging stations can operate independently, ensuring uninterrupted service and reducing the risk of grid overloads.

Regional Analysis

APAC Leads the Global Electric Vehicle Charger Market with 38.40% Share in 2024

In 2024, the Asia-Pacific (APAC) region held a dominant position in the global electric vehicle (EV) charger market, capturing 38.40% of the total market share, which translated to a valuation of approximately USD 4.6 billion. This dominance is largely driven by the aggressive electrification policies and manufacturing scale of key countries such as China, Japan, South Korea, and India.

According to the China Electric Vehicle Charging Infrastructure Promotion Alliance (EVCIPA), China had deployed more than 2.2 million public chargers as of late 2023, with consistent monthly additions exceeding 60,000 units.

Government initiatives have significantly accelerated the deployment of charging infrastructure. For instance, India’s FAME II scheme allocated ₹1,000 crore towards establishing over 4,000 charging stations across urban centers and highways. Japan and South Korea are also expanding their ultra-fast charging networks in sync with EV sales growth and automaker targets.

APAC’s lead is also attributed to strong local demand, rising fuel prices, and ambitious carbon neutrality goals. With regional automakers introducing a wider range of EV models and supportive infrastructure expanding rapidly, the region continues to be the engine of global EV adoption. The synergy between policy frameworks, industrial backing, and consumer readiness is expected to reinforce APAC’s leadership in the EV charger market through 2025 and beyond.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

ABB Ltd. stands out as a global leader in electric vehicle (EV) charging solutions, offering a broad portfolio of fast-charging systems, including DC chargers and high-power charging networks. The company has deployed more than 50,000 DC fast chargers across 85 countries as of 2024. Its Terra series is widely adopted in commercial fleets and urban infrastructure. ABB actively supports grid integration technologies and has partnered with governments to expand public EV charging in APAC and Europe.

Aerovironment Inc., now operating its EV charging business under Webasto, is known for its residential and workplace charging systems. Its flagship product line, TurboCord, provides portable Level 1 and Level 2 charging for individual EV owners. The company focuses on compact design, energy efficiency, and ease of use. With a strong presence in the U.S. market, Aerovironment has installed tens of thousands of chargers and continues to partner with utility companies for grid-aware charger deployment.

Chargemaster PLC, a BP-owned company under the BP Pulse brand, plays a key role in the UK’s public and private EV charging infrastructure. As of 2024, it operates over 9,000 public charging points across the UK. The company offers a complete ecosystem of charging solutions, including home units, commercial charging, and rapid public stations. Chargemaster’s integration with BP’s energy network allows for enhanced reliability, smart grid features, and renewable energy use.

Top Key Players in the Market

- ABB Ltd.

- Aerovironment Inc.

- Chargemaster PLC

- ChargePoint, Inc.

- Chroma ATE Inc.

- Delphi Technologies PLC

- Pod Point

- Robert Bosch GmbH.

- Schaffner Holdings AG

- Siemens AG

- Silicon Laboratories

Recent Developments

In 2024, ABB Ltd. solidified its position as a global leader in the electric vehicle (EV) charger market by expanding its product portfolio and deploying advanced charging solutions worldwide. The company introduced the A400 All-in-One charger, capable of delivering up to 400 kW, designed to enhance user experience with a 99% charging success rate and 97% uptime, addressing common challenges in EV charging reliability.

In 2024, Chargemaster PLC, operating under the BP Pulse brand, maintained its position as a leading electric vehicle (EV) charging provider in the UK. The company managed over 9,000 public charging points, including more than 3,000 rapid and ultra-fast chargers, catering to the growing demand for efficient EV charging solutions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 12.1 Bn |

| Forecast Revenue (2034) | USD 123.0 Bn |

| CAGR (2025-2034) | 26.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Vehicle Type (Battery Electric Vehicle (BEV), Plug-in Hybrid Electric Vehicle (PHEV), Hybrid Electric Vehicle (HEV)), By End User (Residential, Commercial), By Charging Type (On-board Chargers, Off-board Chargers) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | ABB Ltd., Aerovironment Inc., Chargemaster PLC, ChargePoint, Inc., Chroma ATE Inc., Delphi Technologies PLC, Pod Point, Robert Bosch GmbH., Schaffner Holdings AG, Siemens AG, Silicon Laboratories |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |