Quick Navigation

- Report Overview

- Key Takeaways

- Asia-Pacific Outdoor Power Equipment Market

- By Equipment Type Analysis

- By Power Source Analysis

- By Capability Analysis

- By End-Use Analysis

- By Sales Channel Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

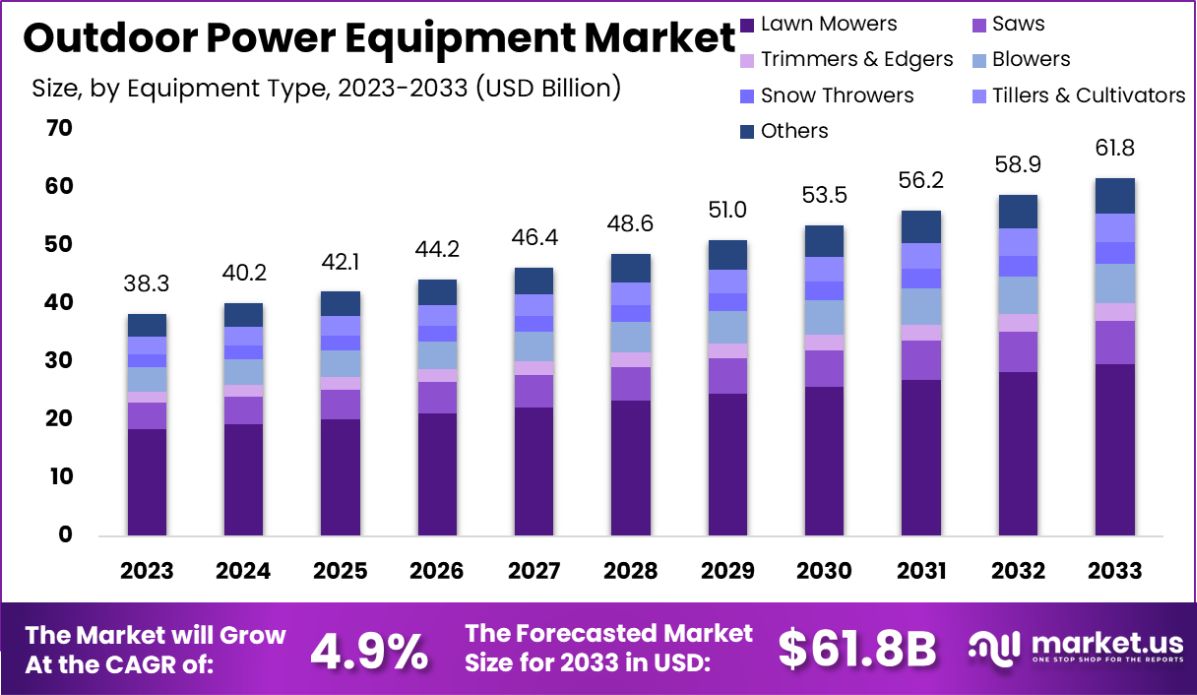

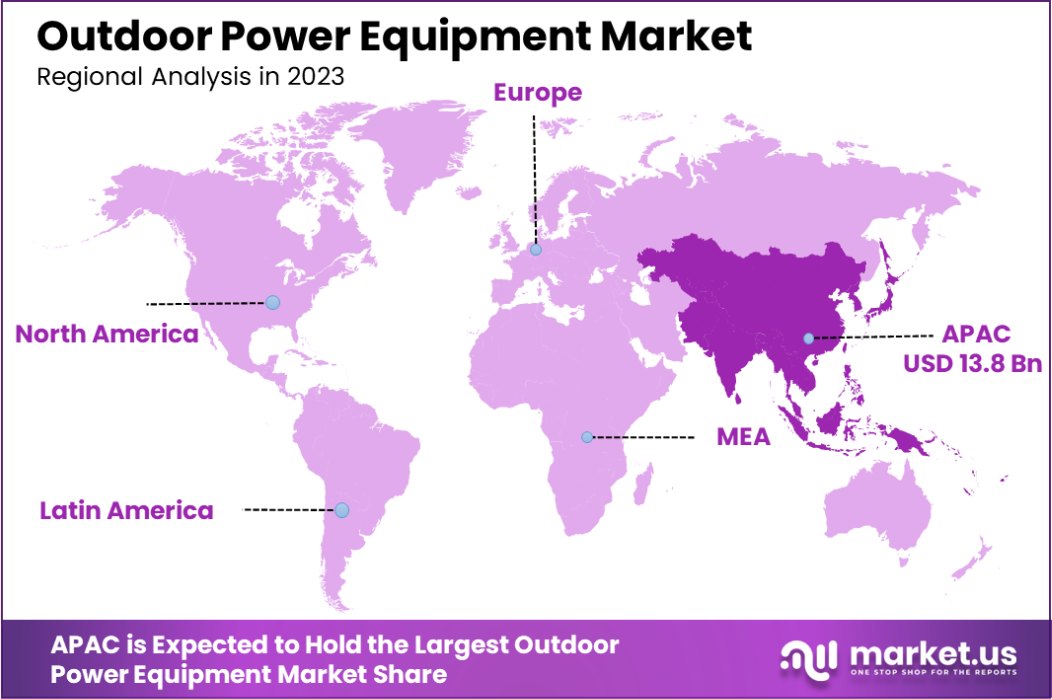

The Global Outdoor Power Equipment Market is expected to be worth around USD 61.8 Billion by 2033, up from USD 38.3 Billion in 2023, and grow at a CAGR of 4.9% from 2024 to 2033. The Asia-Pacific outdoor power equipment market holds 36.9%, valued at USD 13.8 billion.

Outdoor Power Equipment (OPE) refers to machines and tools used for outdoor tasks such as lawn care, gardening, landscaping, and snow removal. This includes lawnmowers, chainsaws, trimmers, leaf blowers, and snow throwers. These products are powered by gasoline, electricity, or batteries and are essential for residential and commercial outdoor maintenance.

The Outdoor Power Equipment Market is driven by factors such as the rising demand for DIY home improvement projects, increased landscaping needs, and a growing focus on environmental sustainability. Technological advancements, like the shift toward battery-powered equipment, are also fueling market growth, offering quieter, more efficient alternatives to traditional gas-powered models.

Demand for outdoor power equipment is especially high in residential areas, as more homeowners invest in maintaining their lawns and gardens. Additionally, the commercial sector, including landscaping and agricultural businesses, is contributing to the market’s expansion.

Opportunities in the market are seen in the growing trend towards eco-friendly solutions and automation. Battery-powered and robotic equipment are becoming more popular as consumers and businesses focus on reducing their carbon footprint and improving efficiency.

The Outdoor Power Equipment market, encompassing tools such as lawn mowers, trimmers, and blowers, is at a critical juncture due to its significant environmental impact and the evolving regulatory landscape. As the market adapts to increasing environmental awareness, the demand for innovative, eco-friendly solutions is on the rise.

In 2020, lawn and garden equipment in the U.S. was responsible for emissions that paint a stark picture of its environmental footprint. According to data from the Maryland General Assembly website, this equipment emitted over 30 million tons of carbon dioxide—surpassing the total smart greenhouse gas emissions of Los Angeles.

The same year saw these tools emit more than 68,000 tons of nitrogen oxide (equivalent to the emissions from 30 million typical cars) and over 350,000 tons of volatile organic compounds. Moreover, the particulate emissions were notably high, with more than 21,800 tons of fine particulates (PM2.5), comparable to the emissions from 234 million typical cars.

This considerable environmental impact is compounded by the operational inefficiencies of gas-powered tools. For instance, gas-powered lawn mowers release as much pollution in one hour as a new car driving 45 miles, and collectively, garden equipment engines contribute to up to 5% of national air pollution. Furthermore, the routine activity of refueling these tools leads to over 17 million gallons of spilled gasoline annually, as noted by the Environmental Protection Agency (EPA).

Historically, in 2011, gasoline-powered lawn and garden equipment accounted for 24%-45% of all nonroad gasoline emissions, including 43% of VOCs and about 50% of PM2.5 emissions from this equipment category. These figures underscore the urgent need for market transformation towards more sustainable practices and technologies.

Key Takeaways

- The Global Outdoor Power Equipment Market is expected to be worth around USD 61.8 Billion by 2033, up from USD 38.3 Billion in 2023, and grow at a CAGR of 4.9% from 2024 to 2033.

- Lawn mowers account for 48.2% of the outdoor power equipment market share globally, driving growth.

- Fuel-based power sources dominate with 45.2% market share, reflecting demand for robust equipment.

- Self-propelled mowers represent 34.4% of sales, highlighting consumer preference for convenience and efficiency.

- Residential applications lead the market at 57.5%, showing strong demand from homeowners for outdoor equipment.

- Retail sales channels contribute 47.5%, indicating a significant portion of market transactions occur through physical stores.

- The Asia-Pacific outdoor power equipment market holds 36.9%, valued at USD 13.8 billion.

Asia-Pacific Outdoor Power Equipment Market

The Asia-Pacific outdoor power equipment market is influenced by various energy initiatives and market dynamics. The USAID Southeast Asia’s Smart Power Program (SPP) aims to enhance energy security in Southeast Asia by promoting energy trade and transforming the energy sector with a focus on increasing the market penetration of energy-efficient technologies like super-efficient air conditioners and lighting. This initiative plans to increase the supply of non-hydro renewable energy to meet 23% of the region’s primary energy demand by 2025.

Furthermore, significant efforts are underway to advance economic growth and development in the region through secure, market-driven energy sectors. The SPP has set core targets to deploy 2,000 MW of advanced energy systems, mobilize $2 billion in financing, and increase regional power trade by 5%.

These actions emphasize the shift towards more sustainable and efficient energy use in the region, which is expected to have a knock-on effect on the demand and innovation in the outdoor power equipment sector, particularly in tools and machinery that are energy-efficient and can operate on alternative energy sources.

Additionally, the U.S. Energy Information Administration (EIA) projects a shift towards renewable energy sources in the Asia-Pacific region, driven by energy security concerns and regional resources. This transition is expected to influence the outdoor power equipment market as tools and technologies evolve to align with new energy infrastructures.

These initiatives and projections indicate a dynamic shift in the Asia-Pacific region towards more sustainable energy practices, potentially reshaping the outdoor power equipment market to favor more energy-efficient and environmentally friendly solutions.

By Equipment Type Analysis

The Outdoor Power Equipment market is dominated by lawn mowers, holding a significant 48.2% market share globally.

In 2023, Lawn Mowers held a dominant market position in the By Equipment Type segment of the Outdoor Power Equipment market, commanding a significant 48.2% share. This strong market presence can be attributed to the widespread use of lawn mowers for residential, commercial, and municipal purposes.

As the most commonly used equipment for lawn maintenance, their high demand is driven by factors such as the growing preference for well-maintained outdoor spaces and advancements in mower technology, including electric and robotic models.

Following Lawn Mowers, Saws accounted for a notable share of the market, driven by their utility in both professional landscaping and personal use. Saws are essential for tasks such as tree cutting, pruning, and branch removal, making them indispensable in outdoor maintenance.

Trimmers & Edgers also captured a significant portion of the market, contributing to the growing demand for precision tools for lawn care. These tools are increasingly favored for their ability to provide clean, well-defined edges around gardens and driveways, enhancing the aesthetic appeal of outdoor spaces.

Blowers and Snow Throwers have shown increased demand, particularly in regions with seasonal weather variations. These tools provide essential functions for clearing debris and snow, respectively, supporting their steady market growth.

Finally, Tillers & Cultivators play a crucial role in soil preparation for planting, with demand influenced by the rising trend of home gardening and agriculture.

By Power Source Analysis

Fuel-based power sources account for 45.2% of the Outdoor Power Equipment market, driven by high demand.

In 2023, Fuel-based power sources held a dominant market position in the By Power Source segment of the Outdoor Power Equipment market, with a 45.2% share. This dominance is largely driven by the continued preference for gasoline-powered equipment, which offers high power output and reliability for heavy-duty tasks.

Fuel-based outdoor power equipment is particularly favored in commercial landscaping and large residential properties where greater mobility and long-lasting performance are crucial. Additionally, the widespread availability of fuel and established infrastructure supports the continued use of fuel-powered equipment in many regions.

On the other hand, Electric power sources are experiencing significant growth, capturing a growing share of the market. The shift toward electric equipment is driven by environmental concerns, as well as advancements in battery technology, which have improved the performance and runtime of electric tools.

The growing demand for quieter, low-maintenance alternatives has made electric outdoor power equipment increasingly attractive to residential users and environmentally conscious consumers. The availability of corded and cordless models has expanded the electric segment’s reach, offering flexibility for a range of tasks from lawn mowing to trimming.

Despite the growth of electric models, fuel-based equipment remains preferred in many commercial and heavy-duty applications, ensuring its continued market leadership for the foreseeable future.

By Capability Analysis

Self-propelled mowers are highly popular in the market, comprising 34.4% of total Outdoor Power Equipment sales.

In 2023, Self-Propelled Mower held a dominant market position in the By Capability segment of the Outdoor Power Equipment market, with a 34.4% share. This growth can be attributed to the convenience and efficiency these mowers offer.

Self-propelled models provide users with reduced physical effort, making them a popular choice among homeowners with medium to large lawns. The ability to adjust the speed and navigate various terrains adds to their versatility, further driving demand across both residential and commercial markets.

Following self-propelled mowers, Riding Lawn Mowers captured a substantial share, particularly in the commercial and large residential segments. These mowers are preferred for their ability to cover large areas quickly and efficiently, with some models offering additional features such as cutting deck adjustments and mulching capabilities.

Automatic Lawn Mowers also demonstrated growing popularity, driven by the increasing consumer demand for smart, automated solutions. These mowers, often equipped with sensors and GPS technology, require minimal human intervention and provide an optimal balance of convenience and precision.

Push Lawn Mowers, while holding a smaller market share, continue to serve as a cost-effective solution for homeowners with smaller lawns. These mowers remain a preferred choice for those looking for lightweight, simple-to-use equipment at an affordable price point.

By End-Use Analysis

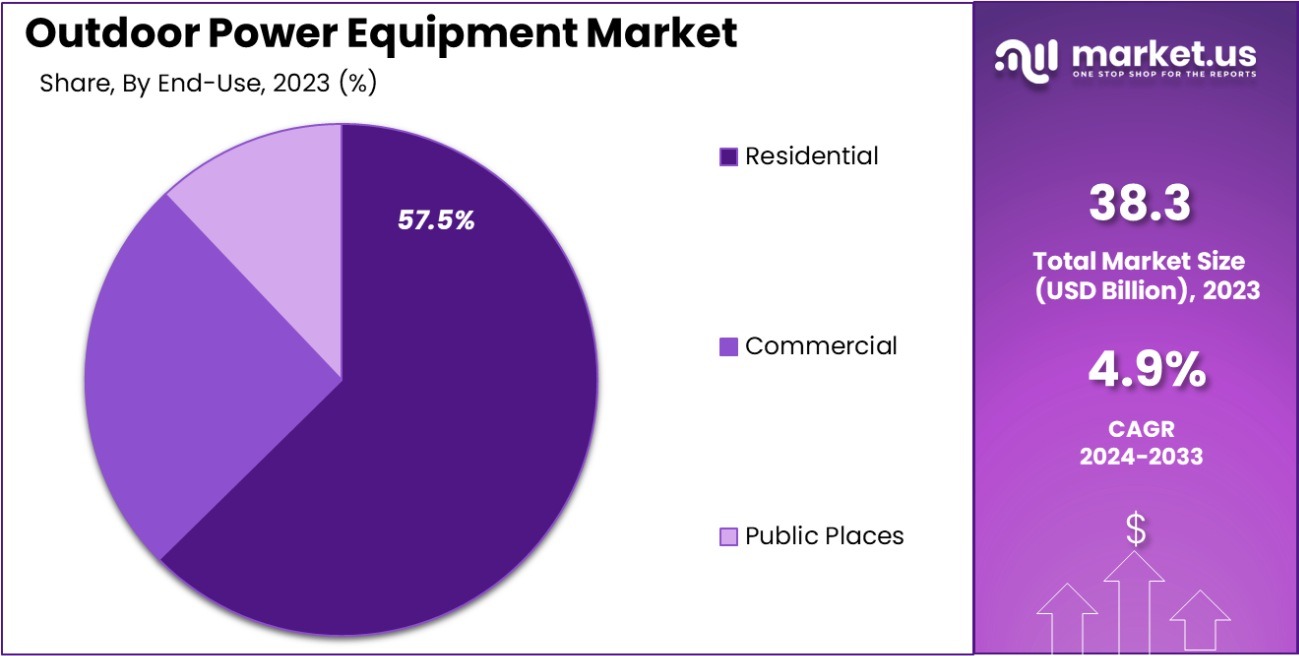

Residential end-use applications lead the Outdoor Power Equipment market, representing a significant 57.5% of the demand.

In 2023, Residential held a dominant market position in the By End-Use segment of the Outdoor Power Equipment market, capturing a 57.5% share. The continued preference for outdoor maintenance among homeowners has driven significant demand for a variety of equipment, including lawn mowers, trimmers, blowers, and snow throwers.

As consumers increasingly invest in well-maintained outdoor spaces, residential demand for efficient and user-friendly tools has surged. The growing trend of home gardening and landscape improvement, alongside the availability of cordless and electric models, has further propelled market growth in this segment.

Commercial users accounted for a substantial portion of the market, with demand driven by landscaping businesses, golf courses, and other professional services requiring high-performance, durable equipment for large-scale maintenance tasks. Commercial buyers typically favor more robust, fuel-based equipment that offers power and efficiency for extended usage.

The Public Places segment also experienced steady demand, although it remains a smaller portion of the market. Public parks, municipal spaces, and government buildings require outdoor power equipment for landscaping and maintenance. This segment is expected to grow moderately, as municipalities increasingly adopt eco-friendly and cost-effective solutions to maintain public outdoor spaces, often opting for equipment that meets sustainability goals.

Overall, residential demand remains the primary driver of market growth, supported by increasing consumer investment in outdoor aesthetics and functionality.

By Sales Channel Analysis

Retail channels dominate sales, with 47.5% of Outdoor Power Equipment purchased through various retail outlets worldwide.

In 2023, Retail held a dominant market position in the By Sales Channel segment of the Outdoor Power Equipment market, with a 47.5% share. This is largely due to the strong presence of brick-and-mortar stores such as home improvement centers, hardware stores, and specialized outdoor equipment retailers.

Consumers continue to value the in-person shopping experience, where they can inspect products, compare features, and receive immediate customer support. Retail stores also offer the advantage of providing a wide range of products, allowing customers to choose from various brands and models, further contributing to retail’s dominant market share.

Distributor channels accounted for a significant portion of sales, driven by their essential role in providing outdoor power equipment to businesses and commercial users. Distributors typically supply products in bulk to landscapers, construction companies, and other professional end-users who require durable and high-performance equipment for large-scale operations. These channels often offer competitive pricing and exclusive products, making them a preferred choice for commercial buyers.

The Online sales channel, while growing rapidly, represented a smaller but expanding segment in 2023. E-commerce platforms, including major websites and direct-to-consumer brands, have become increasingly popular for residential buyers seeking convenience, competitive pricing, and home delivery. As consumers become more comfortable purchasing large outdoor equipment online, the online channel is expected to experience further growth in the coming years.

Key Market Segments

By Equipment Type

- Lawn Mowers

- Saws

- Trimmers & Edgers

- Blowers

- Snow Throwers

- Tillers & Cultivators

- Others

By Power Source

- Fuel-based

- Electric

By Capability

- Self-Propelled Mower

- Riding Lawn Mower

- Automatic Lawn Mower

- Push Lawn Mower

- Others

By End-Use

- Residential

- Commercial

- Public Places

By Sales Channel

- Retail

- Distributor

- Online

Driving Factors

Growing Demand for Battery-Powered Tools

The outdoor power equipment market is seeing a significant shift towards battery-powered tools. As environmental concerns rise and technology improves, more consumers and professionals opt for eco-friendly alternatives to gas-powered equipment.

Recent data shows that the battery-powered segment is projected to grow at a compound annual growth rate (CAGR) of 7.6% through 2025. This trend is driven by the tools’ lower emissions, reduced noise levels, and advancements in battery life and performance, making them an increasingly popular choice in residential and commercial settings.

Expansion of Residential and Commercial Landscaping Services

Landscaping services are expanding rapidly due to increased interest in residential beautification and commercial property maintenance. This growth fuels demand for outdoor power equipment, as more homeowners and businesses invest in maintaining their outdoor spaces.

Industry reports indicate that the market for landscaping services is expected to increase by 4.5% annually over the next five years. This expansion directly impacts the sales of lawn mowers, trimmers, and other related equipment, as these tools are essential for efficient landscaping and upkeep.

Innovation and Product Advancement

Manufacturers in the outdoor power equipment market are constantly innovating to meet consumer demands for efficiency and convenience. There is a notable increase in the introduction of multi-functional products that offer more versatility and improved performance.

For instance, equipment combining blowing, mulching, and vacuuming capabilities is becoming more popular. This innovation not only caters to the need for space-saving solutions but also appeals to users looking for higher value from their purchases. As a result, such advancements are expected to drive market growth significantly in the coming years.

Restraining Factors

High Initial Cost of Advanced Equipment

One of the main hurdles in the outdoor power equipment market is the high initial cost of advanced tools. For many potential buyers, especially small businesses and homeowners, the upfront investment in newer, high-tech equipment like robotic mowers can be prohibitive.

For example, the cost of advanced battery-powered models can be twice that of traditional gas-powered equipment. This price barrier often discourages the initial purchase, impacting market growth despite the long-term savings and environmental benefits these tools offer.

Stringent Environmental Regulations

Tightening environmental regulations are significantly impacting the outdoor power equipment market. Many regions are introducing stricter emission standards that phase out the use of traditional gas-powered tools, which are known for their high emissions and noise levels.

While this shift aims to reduce environmental impact, it poses a challenge for manufacturers and users alike. The transition to compliant equipment requires redesigning products and sometimes, a complete overhaul of existing models, adding to costs and complicating compliance efforts. This can slow down market growth as both parties adjust to these new norms.

Market Saturation in Developed Regions

In many developed regions, the market for outdoor power equipment is nearing saturation, which limits new sales opportunities. As most households and businesses already own some form of outdoor power equipment, the primary market drivers become replacements and upgrades rather than new purchases.

This saturation results in a slower growth rate compared to emerging markets. For instance, in places like the United States and Western Europe, market growth is forecasted to hover around a modest 1% to 2% annually, as the potential for new customer acquisition diminishes.

Growth Opportunity

Rising Popularity of Smart Gardening Technologies

Smart gardening technologies are revolutionizing how people manage their outdoor spaces, presenting a significant growth opportunity in the outdoor power equipment market. These technologies, which include robotic lawn mowers and app-controlled irrigation systems, are gaining traction for their convenience and efficiency.

Market analysts predict a surge in consumer investment in these smart tools, with expected growth rates increasing by 15% annually over the next decade. This trend offers manufacturers a chance to innovate and expand their product lines to include more IoT-enabled devices, tapping into the tech-savvy consumer segment.

Expansion into Emerging Markets

Emerging markets offer fresh terrain for the outdoor power equipment industry, with substantial growth potential. As economic conditions improve in regions such as Asia-Pacific and Latin America, there is a growing middle class ready to invest in gardening and landscaping equipment.

These markets are relatively untapped compared to saturated Western markets, and they present opportunities for double-digit growth. Companies that can navigate the local consumer preferences and economic conditions in these areas could see significant returns, especially with products tailored to regional needs and price points.

Eco-Friendly Equipment Driving New Sales

Environmental concerns are not just shaping regulations; they are also influencing consumer behavior. There is a rising demand for eco-friendly outdoor power equipment, such as electric and solar-powered tools. This shift is seen not only in residential but also in commercial sectors, where sustainable practices are becoming a priority.

The global push towards sustainability is expected to increase sales of green equipment by over 10% annually. Manufacturers that focus on developing and marketing cleaner, quieter, and more energy-efficient models are likely to capture new customers and gain a competitive edge in this growing segment.

Latest Trends

Integration of Robotics and Automation in Equipment

The integration of robotics and automation into outdoor power equipment is a leading trend, reshaping how tasks like mowing and cleaning are done. Robotic lawn mowers and automated leaf blowers are becoming increasingly popular for their efficiency and minimal human intervention.

The market for these automated tools is expected to grow by approximately 12% annually over the next five years. This trend is driven by advancements in technology and a growing preference for convenience and time-saving solutions among users.

Surge in DIY Landscaping Projects

The DIY trend is booming, with more homeowners taking on landscaping projects themselves, spurred by online tutorials and home improvement shows. This shift has increased the demand for versatile, user-friendly outdoor power equipment suited to occasional use without professional expertise.

Retailers are noting a significant uptick in sales of compact, easy-to-use models designed for the average consumer, with sales expected to rise by 8% annually. This trend is enhancing user engagement and broadening the customer base for outdoor power tools.

Focus on Eco-Friendly and Energy-Efficient Products

There’s a strong movement towards eco-friendly and energy-efficient outdoor power equipment, driven by consumer awareness and tightening environmental regulations. Electric models, which are quieter and emit no direct emissions, are seeing a rise in popularity, particularly in urban areas where noise and pollution regulations are stricter.

The market for these green products is forecasted to expand by over 10% annually. Manufacturers who prioritize sustainability in their product development are well-positioned to attract environmentally conscious consumers, providing a significant growth opportunity in the industry.

Regional Analysis

The Asia-Pacific outdoor power equipment market holds a 36.9% share, valued at USD 13.8 billion.

The outdoor power equipment market is segmented into several key regions: North America, Europe, Asia-Pacific, Middle East & Africa, and Latin America, each exhibiting unique growth dynamics.

Dominating the market, Asia-Pacific holds a significant share of 36.9%, with a valuation of USD 13.8 billion, driven by rapid urbanization and increased spending on landscaping services in countries like China and Japan.

North America follows, characterized by high adoption rates of technologically advanced equipment, particularly for residential lawn care and municipal applications. The region’s focus on sustainable and eco-friendly tools continues to shape market offerings, aligning with environmental regulations.

Europe, with its stringent noise and emissions regulations, has seen a shift towards electric and battery-powered equipment. This shift is further propelled by the growing presence of robotic lawn mowers and other autonomous maintenance devices.

The Middle East & Africa region, although smaller in comparison, is experiencing gradual growth, fueled by increasing commercial construction and public space beautification initiatives.

Lastly, Latin America is emerging as a potential growth area, with increasing urban development and a rising middle class investing more in home and garden maintenance. Together, these regional markets create a diverse and evolving landscape for outdoor power equipment, driven by both technological advancements and changing consumer preferences.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2023, the global outdoor power equipment market will see prominent contributions from several key players, each leveraging their strengths in technology and market presence to shape industry dynamics.

Notably, companies like ANDREAS STIHL, Husqvarna Group, and Honda Motors Co. Ltd are at the forefront, offering a broad range of products that emphasize innovation, sustainability, and user efficiency.

ANDREAS STIHL continues to dominate with its strong portfolio in both electric and gasoline-powered tools. Stihl’s commitment to research and development is evident in its latest product launches, which are designed to meet both the rigorous demands of professional landscapers and the convenience needs of casual gardeners. Their advancements in battery technology and ergonomics make them a continued favorite in the market.

Husqvarna Group is another major player that stands out for its integration of smart technology in products. As a pioneer in robotic lawn mowers, Husqvarna emphasizes sustainability through reduced carbon footprints and noise pollution, aligning with global environmental concerns. Their approach not only strengthens their market position in Europe but also garners significant interest in North American and Asian markets.

Honda Motors, known for its engine manufacturing prowess, enhances the market with high-quality, durable products that are trusted worldwide. Honda’s focus on fuel efficiency and lower emissions engines in their mowers and trimmers cater to an increasingly eco-conscious consumer base.

Other significant players like Bosch, Deere & Company, and The Toro Company are equally important, pushing the envelope with innovative features that improve user safety and productivity. Bosch, for instance, leverages its expertise in power tool design to enhance the usability and performance of its garden equipment.

Collectively, these companies are not just competing on product features but are also deeply involved in shaping the regulatory and consumer landscapes. Their continued investment in technology and global expansion strategies are pivotal in driving the outdoor power equipment market forward, making it a highly competitive and dynamic sector.

Top Key Players in the Market

- AG & Co. KG

- AL-KO Kober Group

- ANDREAS STIHL

- Andreas Stihl AG & Company KG

- Ariens Company

- Bosch

- Briggs & Stratton Corp.

- CHERVON (China) Trading Co., Ltd

- Cub Cadet

- Deere & Company

- Hikoki

- Honda

- Honda Motors Co. Ltd

- Husqvarna AB

- Husqvarna Group

- Jonsered

- Kaercher

- Makita Corporation

- Maruyama U.S., Inc.

- MTD Holdings Inc.

- Robert Bosch

- Stanley Black and Decker Inc.

- Techtronic Industries

- The Toro Company

- Troy Blit LLC

- Vb Emak

- YAMABIKO Corporation

- Yamabiko Manufactures

Recent Developments

- In 2023, Bosch Power Tools emphasized sustainability in their product range, integrating recycled materials and eco-friendly components, and expanded their battery systems and multi-brand collaborations to enhance market presence and environmental responsibility.

- In 2023, Briggs & Stratton Corp., headquartered in Milwaukee, is a leading producer of outdoor power equipment engines and innovative power solutions like lithium-ion batteries and generators. Serving both residential and commercial sectors globally, they focus on durability and environmental standards.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 38.3 Billion |

| Forecast Revenue (2033) | USD 61.8 Billion |

| CAGR (2024-2033) | 4.9% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Equipment Type (Lawn Mowers, Saws, Trimmers and Edgers, Blowers, Snow Throwers, Tillers and Cultivators, Others), By Power Source (Fuel-based, Electric), By Capability (Self-Propelled Mower, Riding Lawn Mower, Automatic Lawn Mower, Push Lawn Mower, Others), By End-Use (Residential, Commercial, Public Places), By Sales Channel (Retail, Distributor, Online) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | AG & Co. KG, AL-KO Kober Group, ANDREAS STIHL, Andreas Stihl AG & Company KG, Ariens Company, Bosch, Briggs & Stratton Corp., CHERVON (China) Trading Co., Ltd, Cub Cadet, Deere & Company, Hikoki, Honda, Honda Motors Co. Ltd, Husqvarna AB, Husqvarna Group, Jonsered, Kaercher, Makita Corporation, Maruyama U.S., Inc., MTD Holdings Inc., Robert Bosch, Stanley Black and Decker Inc., Techtronic Industries, The Toro Company, Troy Blit LLC, Vb Emak, YAMABIKO Corporation, Yamabiko Manufactures |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |