Quick Navigation

- Report Overview

- Key Takeaways

- Offering Type Analysis

- Component Analysis

- Technology Analysis

- Crop Type Analysis

- Greenhouse Type Analysis

- Automation Level Analysis

- Application Analysis

- Key Market Segments

- Challenges

- Opportunity

- Drivers

- Restraints

- Geopolitical Impact Analysis

- Regional Analysis

- Key Players Analysis

- Key Development

- Report Scope

Report Overview

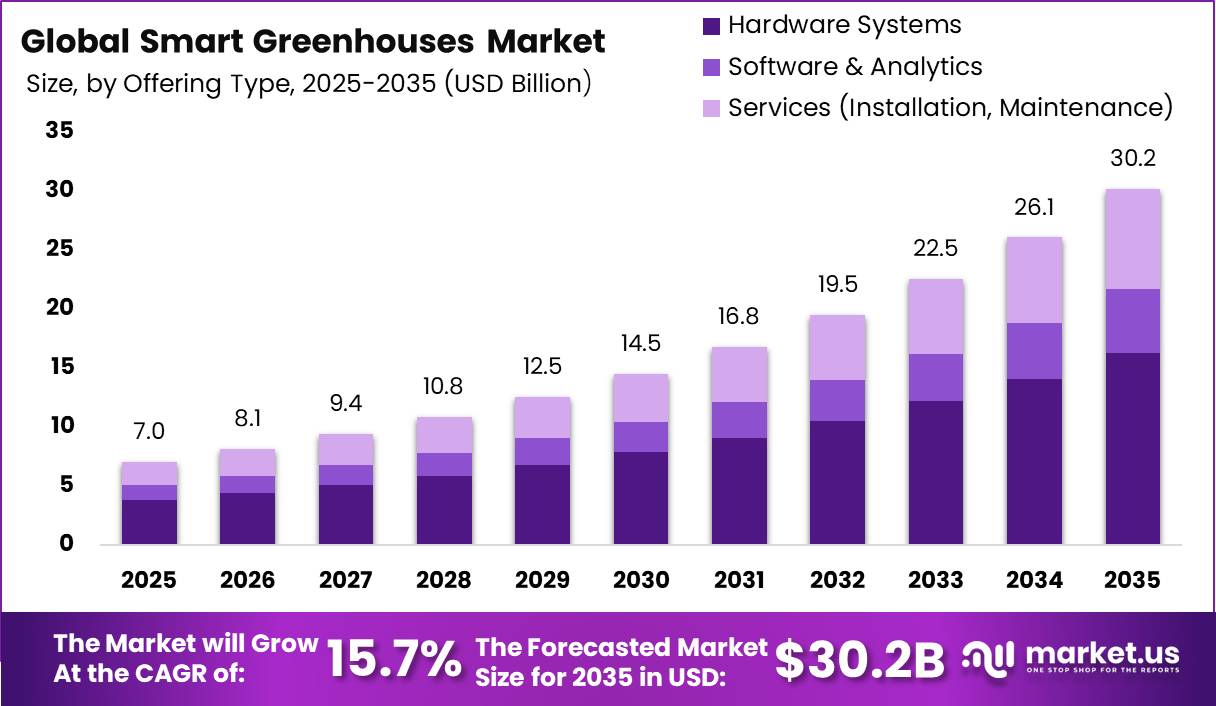

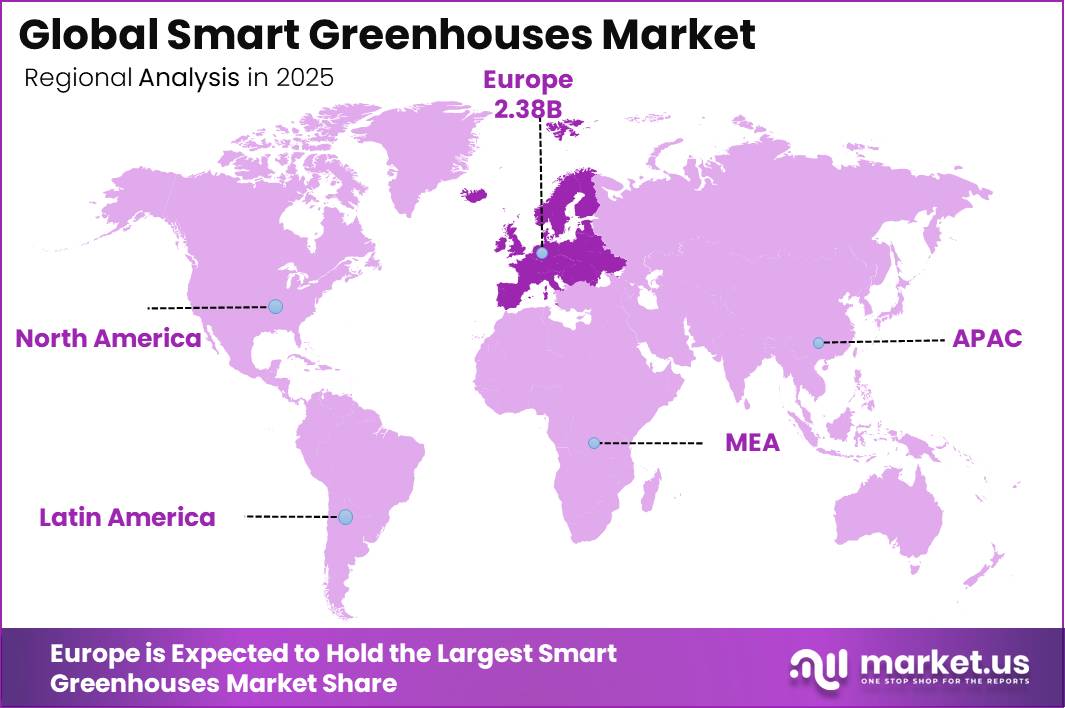

The Global Smart Greenhouses Market was valued at USD 7.0 billion in 2025, and between 2026 and 2035, this market is estimated to register a CAGR of 15.7%, reaching about USD 30.2 billion by 2035. Europe held a dominant market position, capturing more than 34% share and generating USD 2.38 billion in revenue.

The smart greenhouse market supports year-round crop production through automation and precision farming. IoT sensors, artificial intelligence, climate-control systems and computerized irrigation help farmers improve yields despite climate change, urbanization and declining arable land. LoRa-based monitoring systems can transmit greenhouse data over distances of up to 1 kilometre in open-field conditions.

- Automated irrigation is becoming a key part of smart greenhouse operations. Drip irrigation systems can reduce water consumption by approximately 30–50% compared with conventional irrigation methods while maintaining crop productivity. These systems monitor soil moisture and provide crops with the required amount of water at the correct time.

Energy-efficient lighting and crop-management technologies are also strengthening market adoption. Modern greenhouse LED systems provide photosynthetic photon efficacy of around 3.5–4.1 µmol/J, reducing electricity use for crop lighting. Europe remains a major adoption region, while Asia-Pacific is expanding rapidly through agricultural modernization, vertical farming and automated crop production.

Key Takeaways

- The global Smart Greenhouses market was valued at USD 7.0 billion in 2025.

- The global Smart Greenhouses market is projected to grow at a CAGR of 15.7% and is estimated to reach USD 30.2 billion by 2035.

- Based on the offering type, hardware systems dominated the global smart greenhouse market, accounting for 54% of the total market share.

- Based on the component, control systems & sensors led the market, comprising approximately 24% of the overall market share.

- Based on the technology, hydroponics emerged as the dominant segment, accounting for nearly 38% of the total market revenue.

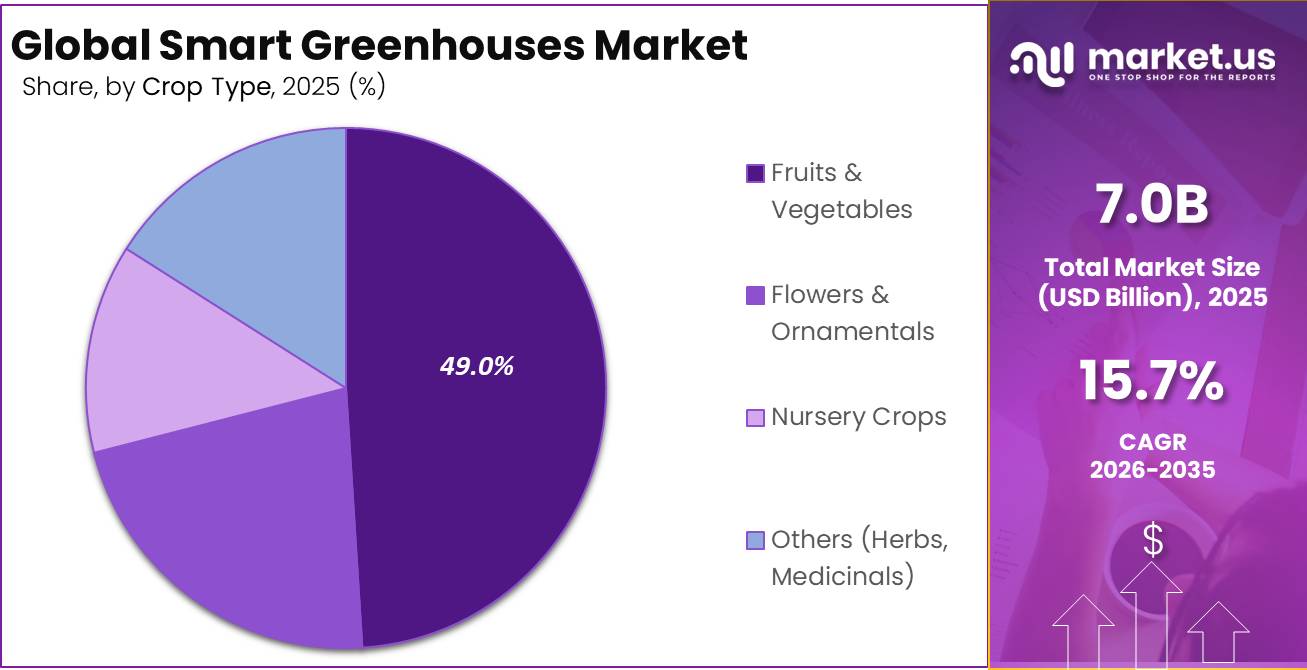

- Among the crop types, fruits & vegetables held the largest share in the smart greenhouse market, contributing around 49% of the total market share.

- Based on greenhouse type, glass greenhouses dominated the market, representing approximately 41% of the global market share.

- Among the automation levels, fully automated smart greenhouses accounted for the highest share, contributing nearly 46% of the total revenue.

- Based on application, commercial farming emerged as the leading segment, holding approximately 58% of the global smart greenhouse market share.

- In 2025, Europe dominated the regional smart greenhouse market, accounting for nearly 34% of the total global market share.

Offering Type Analysis

Hardware Systems represent the dominant Segment in the Market.

Hardware Systems represent the dominant segment in the Smart Greenhouses market, accounting for 54% share. This dominance is due to high market demand for physical products and indicates that customers interact with the company largely through real, product-driven solutions.

The domination of hardware systems is further backed by increased expenditures in greenhouse automation, climate control technology, LED lighting systems, and precision irrigation infrastructure in commercial farming operations around the world. Furthermore, the increased adoption of smart farming practices and need for high-yield crop production reinforce the need for modern greenhouse equipment and integrated hardware solutions.

Software & Analytics segment encompasses the data platforms, dashboards, monitoring tools, and analytics engines that sit on top of deployed hardware infrastructure. Customers who have already invested in hardware systems are naturally incentivized to adopt complementary software to maximize their return on that investment, making cross-sell conversion rates in this segment typically high. That’s where AI, machine learning, cloud computing, and real-time analytics step in.

Component Analysis

HVAC Systems a significant Component.

HVAC Systems dominate the worldwide greenhouse market component landscape, accounting for 22.50%, emphasizing the importance of climate control in modern controlled environment agriculture. Precise temperature, humidity, and air circulation management are critical for crop yield optimization, disease avoidance, and year-round cultivation, making HVAC an essential investment in any greenhouse setup.

As greenhouse operators seek automation and climatic precision, HVAC systems are likely to maintain their leadership position, with next-generation heat pumps and geothermal-integrated systems supporting the segment’s continuous progress. This dominance is further supported by the growing usage of large-scale commercial greenhouses in Europe, North America and Asia-Pacific, where energy-efficient HVAC solutions are required by both operational necessity and regulatory requirements.

LED grow lights have gained popularity as technological costs have decreased, making full-spectrum lighting more affordable and enhancing photosynthesis efficiency and crop output. Irrigation systems, particularly precision drip and fertigation technologies, enable solving water scarcity while maximizing fertilizer use and lowering operating waste.

Technology Analysis

Hydroponics Are the Most Widely Used Technologies.

Hydroponics has the biggest share of the worldwide greenhouse technology segment, 38%, establishing itself as the preferred soilless growing method for commercial and large-scale greenhouse operations. Its supremacy is credited to improved water efficiency, shorter crop growth cycles, and higher yield density compared to conventional farming, making it the preferred method for year-round, high-value crop production.

The technology’s scalability across a variety of habitats, from urban vertical farms to large controlled-environment facilities, broadens its commercial applicability. Continued developments in nutrient delivery systems, automation integration, and vertical farming acceptance are projected to reinforce Hydroponics‘ leadership position in global greenhouse markets.

Aeroponics is redefining the boundaries of soilless farming by delivering nutrients directly to plant root systems suspended in air through a fine, high-pressure mist. Because the roots are exposed to both oxygen and nutrients simultaneously, plants tend to absorb what they need far more efficiently than in traditional soil or even hydroponic setups, translating into remarkably faster growth rates and healthier yields.

Crop Type Analysis

Fruit and Vegetables Held a Major Share of the Smart Greenhouses Market.

Fruit and vegetables lead the global smart greenhouse market, accounting for over 49% of total market share. One of the primary drivers of this segment’s global expansion is the high need for fresh, healthy, year-round food supply. Greenhouse cultivation of crops including tomatoes, cucumbers, peppers, lettuce, strawberries, and other berries helps farmers to increase output, improve harvest quality, and extend shelf life as compared to traditional farming methods.

Furthermore, greenhouse farming decreases reliance on seasonal weather and cuts pesticide use, making products safer and more sustainable. Rising urbanization, dwindling arable land, shifting consumer dietary choices, and increased investment in controlled environment agriculture are all likely to bolster the segment’s global dominance.

Greenhouse Type Analysis

Glass Greenhouses Are Widely Utilized in Commercial Smart Farming Operations

Glass greenhouses make up the largest part of the global smart greenhouse market, holding around 41% of the share. This strong position comes from their better durability, higher efficiency in letting in light, and superior ability to control the climate compared to other types of greenhouses. Growers who sell crops commercially often choose glass greenhouses for growing high-value plants like tomatoes, cucumbers, peppers, flowers, and rare fruits.

This is because glass greenhouses allow for farming all year round, leading to better quality and higher production of crops. They are also able to withstand bad weather and last longer, which makes them the top choice for big greenhouse projects, especially in advanced agricultural areas like Europe and North America.

Rigid panel greenhouses are emerging as the fastest-growing structural format in the controlled environment agriculture space, and the momentum behind them is well-founded. Rigid panel greenhouses, typically constructed using twin-wall or multi-wall polycarbonate panels, strike a compelling balance between durability, thermal performance, and cost-effectiveness.

Automation Level Analysis

Fully automated smart greenhouses hold the largest share.

Fully automated smart greenhouses hold the largest share in the global market at nearly 46%, and are also growing faster than any other automation segment. This strong performance is largely because farmers and commercial growers are facing increasing labour shortages, rising production costs, and growing pressure to produce more food using fewer resources.

They automatically maintain the right temperature, humidity, lighting, and nutrient levels throughout the day, resulting in better crop quality, less water and fertilizer waste, and higher yields across all seasons. Commercial growers are increasingly choosing fully automated greenhouses because they cut labour costs, improve efficiency, and support more sustainable farming practices through smarter, data-backed decision-making.

Semi-automated greenhouses also have a significant market presence, particularly among medium-sized farming businesses looking for a compromise between cost and technological efficiency. These systems combine manual supervision with automatic features like watering or temperature management.

Application Analysis

Commercial farming is currently the biggest part of the global smart greenhouse market, holding about 58% of the total share. It’s also growing the fastest, thanks to increasing food demand worldwide, more people using precision agriculture techniques, and the need for reliable, high-yield crop production all year round.

Large greenhouse operators are investing more in automated systems for climate control, smart irrigation, LED grow lights, and AI tools for monitoring crops. These technologies help increase productivity while using less water, fewer fertilizers, and less labour.

This leads to better crop quality, lower costs, and more predictable harvests that match the needs of today’s retail and food supply chains. The increasing interest in controlled environment farming and sustainable agricultural practices is bringing in more investment, which strengthens commercial farming’s role as the main driver of growth in the smart greenhouse market.

Key Market Segments

By Offering Type

- Hardware Systems

- Software & Analytics

- Services (Installation, Maintenance)

By Component

- HVAC Systems

- LED Grow Lights

- Irrigation Systems

- Control Systems & Sensors

- Others

By Technology

- Hydroponics

- Aeroponics

- Aquaponics

- Soil-based Smart Farming

By Crop Type

- Fruits & Vegetables

- Flowers & Ornamentals

- Nursery Crops

- Others (Herbs, Medicinals)

By Greenhouse Type

- Glass Greenhouses

- Plastic Greenhouses

- Rigid Panel Greenhouses

By Automation Level

- Fully Automated

- Semi-Automated

- Manual/Assisted

By Application

- Commercial Farming

- Research & Education

- Retail & Urban Farming

- Residential/Small-scale

Challenges

Energy price volatility remains a major operational challenge for smart greenhouses, with energy accounting for 25–40% of operating costs in heated facilities and reaching 50–60 kWh per kg of high-value crops in colder climates. Wholesale electricity price swings of 30–80% can increase production costs by 0.15–0.25 per kg, while peak-demand tariffs may add 10–20% to monthly energy bills, reducing project IRRs by 200–300 basis points and lowering achievable market CAGR by around 1% point.

To limit these impacts, operators are optimizing energy strategies by reducing peak electricity demand by 5–10%, installing 0.5–2 MW solar-plus-battery systems, and securing 3–5-year power purchase agreements that can reduce price volatility by 20–30%. These measures improve cost predictability but require additional capital investment of 15–25% of the original greenhouse project value.

Advanced energy management is becoming a key competitive strategy, with facilities deploying 50–200 sub-meters per site, AI-based climate optimization that cuts energy use by 10–18% without reducing yields, and heat pump systems achieving seasonal performance factors above 3.0. Industry-wide adoption of these solutions is expected to mature over the next 2–4 years, improving resilience against energy cost fluctuations.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Volatile energy intensity | -1.0% | Europe, North Asia, North America | Medium term (2–4 years) |

| Complex IoT-OT integration | -0.8% | North America, EU, advanced APAC | Medium term (2–4 years) |

| Data, connectivity gaps | -0.5% | Emerging APAC, LatAm, MENA | Long term (≥ 4 years) |

| Agri-tech talent shortfall | -0.6% | Global, esp. EU & APAC | Long term (≥ 4 years) |

| Sensor & controls supply risk | -0.4% | Europe, North America, APAC hubs | Short term (≤ 2 years) |

| Project finance sophistication gap | -0.7% | Emerging markets, peri-urban hubs | Medium term (2–4 years) |

Opportunity

CEA-as-a-Service (CEAaaS) and outcome-based contracts are emerging as a major growth opportunity because 80%+ of smart greenhouse vendor revenue still comes from one-off capex sales. The model targets growers who lack upfront capital but are willing to pay predictable operating fees tied to production outcomes instead of making large initial investments.

Under these models, vendors could generate US$20–60 per m² annually through “yield-per-square-meter” or “cost-per-kg” contracts, with potential EBITDA margins 5–10% points higher than traditional hardware sales. The approach is particularly attractive in North America, Europe, the GCC, and East Asia, where labour constraints and demand for stable production are increasing.

If 10–15% of new smart greenhouse deployments between 2028 and 2035 transition to CEAaaS models, the recurring revenue stream could add around 2% points to market CAGR, increase lifetime value per site by 30–50%, and improve lender confidence through more predictable cash flows. The opportunity remains in its early stages as financing models, risk-sharing contracts, and long-term performance data continue to mature.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| CEA-as-a-Service & outcome contracts | +2.0% | North America, EU, GCC, East Asia | Medium term (2–4 years) |

| Integrated urban CEA hubs with retail tie-ins | +1.8% | North America core, EU, APAC Tier-1 cities | Medium term (2–4 years) |

| Low-cost modular smart greenhouses for emerging markets | +2.5% | APAC emerging, Latin America, Africa | Long term (≥ 4 years) |

| AI-driven autonomous operations platforms | +1.5% | North America, EU, Japan, South Korea | Short term (≤ 2 years) |

| Cross-value-chain M&A roll-ups in CEA | +1.2% | North America, EU, APAC developed | Medium term (2–4 years) |

| Climate-resilient specialty crops & high-margin categories | +1.7% | EU, North America, high-income Asia | Long term (≥ 4 years) |

Drivers

Water scarcity and the need for stable crop production are major structural growth drivers for smart greenhouses, as controlled-environment systems can reduce water consumption by 53–98% compared with open-field farming, depending on the system design and crop type. This makes precision agriculture increasingly attractive in water-stressed regions.

The trend is estimated to contribute around 1.3% points to market CAGR, driven by the adoption of irrigation optimization, closed-loop fertigation, and sensor-based moisture management. These technologies improve water-use efficiency while maintaining consistent crop yields.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-cost pressure driving climate control automation | +1.6% | EU core, North America core, APAC industrial corridors | Short term (≤ 2 years) |

| Labor scarcity accelerating automation and remote ops | +1.4% | North America core, EU core, Japan, South Korea, Gulf | Short term (≤ 2 years) |

| Water-stress and yield-security demand | +1.3% | Middle East, India, China north, North Africa, Australia | Medium term (2–4 years) |

| Policy support for climate-smart agriculture and CEA | +1.5% | EU, North America, China, India, GCC, selected LATAM | Medium term (2–4 years) |

| AI, IoT, and edge analytics improving unit economics | +1.8% | Global, with strongest pull in EU, North America, APAC | Short term (≤ 2 years) |

| Retail traceability and premium local-produce demand | +0.9% | North America, EU, Japan, urban APAC | Medium term (2–4 years) |

Restraints

High upfront capital costs remain the biggest restraint on smart greenhouse adoption, with fully automated facilities requiring 40–70% higher initial investment than conventional greenhouses. Typical 2–5 hectare projects cost US$2–5 mn, extending payback periods from 6–7 years for traditional glasshouses to 9–12 years for smart greenhouse systems.

Higher interest rates, remaining 200–300 basis points above 2015–2019 averages in many markets, have increased financing costs and raised lender equity requirements from 15–20% to 30–40%. In addition, depreciation of 8–10% of revenue and annual software subscription fees of US$20,000–40,000 reduce early-stage EBITDA margins by 300–500 basis points unless yields improve by 20–25% and input costs fall by 10–15%.

These financial challenges make many small and mid-sized growers delay investments, particularly where contract farming penetration remains below 30–40%. As a result, high capex and financing constraints reduce projected market CAGR by around 2.3% points, encouraging vendors to expand leasing, greenhouse-as-a-service, and revenue-sharing models to improve affordability.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex & payback risk | -2.3% | North America core, EU, East Asia | Short–Medium term |

| Volatile energy & heating costs | -1.6% | EU, UK, North America, MENA | Short term |

| Connectivity & digital infra gaps | -1.2% | APAC corridors, Latin America, Africa | Medium–Long term |

| Control system & sensor costs | -1.0% | Global, more acute in emerging markets | Medium term |

| Regulatory & data-compliance friction | -0.9% | EU, North America, selected APAC | Medium–Long term |

| Skilled labour & integration bottlenecks | -0.8% | EU, North America, developed APAC | Short–Medium term |

Geopolitical Impact Analysis

Geopolitical Dynamics and Their Impact on the Global Smart Greenhouse Market.

Geopolitical tensions and changing global trade policies are increasingly influencing the global smart greenhouse market, especially in the supply of important components such as semiconductors, sensors, LED lighting systems, and automation equipment.

Ongoing trade conflicts between major economies like the United States and China have created uncertainty regarding tariffs, technology exports, and equipment sourcing, forcing greenhouse operators and technology providers to diversify supply chains and rely more on regional manufacturing. As a result, many countries are investing in domestic agricultural technology production to reduce dependence on foreign suppliers and improve supply chain stability.

At the same time, geopolitical instability, regional conflicts, and climate-related disruptions are increasing concerns about food security worldwide. Countries that heavily depend on food imports, particularly across the Middle East, Southeast Asia, and parts of Europe, are increasingly investing in smart greenhouse infrastructure to strengthen domestic food production.

Governments are also supporting controlled environment agriculture through subsidies, funding programs, and public-private partnerships, recognizing smart greenhouses as an important solution for ensuring stable and sustainable food supplies in an uncertain global trade environment.

Regional Analysis

Europe Held the Largest Share of the Global Smart Greenhouses Market.

Europe firmly leads the global smart greenhouse market, holding nearly 34% of total market share, a position built on decades of investment in advanced greenhouse infrastructure, precision agriculture, and sustainable farming practices.

Countries like the Netherlands, Spain, Germany, and France drive this leadership through large-scale commercial greenhouse operations, strong government backing for climate-smart agriculture, and widespread adoption of technologies including AI-based climate control, LED grow lights, smart irrigation, and IoT monitoring systems.

The Netherlands stands out globally as a benchmark for greenhouse farming excellence, renowned for its highly efficient and technologically sophisticated horticulture ecosystem. Growing concerns around food security, water conservation, and energy-efficient farming continue to reinforce Europe’s dominant regional position.

Asia-Pacific is emerging as the fastest-growing market in the area, as a result of rapid urbanization, expanding population, declining arable land, and increased investment by authorities in new agricultural technologies in China, Japan, India, and South Korea.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global smart greenhouse market operates in a moderately consolidated competitive environment, where companies differentiate themselves primarily through technological innovation, automation capabilities, energy-efficient solutions, and integrated greenhouse management platforms. Leading players are actively expanding their product offerings across advanced climate control technologies, AI-driven crop monitoring, smart irrigation, LED grow lighting, and precision farming systems, continuously raising the performance bar for the broader industry.

Sustained investment in research and development remains a central priority, as companies seek to improve operational efficiency, enhance crop productivity, and align their solutions with the growing global emphasis on sustainable greenhouse farming practices.

Beyond product innovation, strategic partnerships, mergers, acquisitions, and collaborations with agricultural technology providers, commercial growers, and research institutions are serving as key competitive levers across the market. Companies are simultaneously expanding manufacturing facilities, strengthening regional distribution networks, and scaling smart farming infrastructure to broaden their global footprint and better serve diverse market needs. The intensifying industry focus on sustainable agriculture, water-efficient farming, renewable energy integration, and fully automated crop management is further sharpening competition, compelling market participants to continuously evolve their capabilities and deliver more comprehensive, future-ready greenhouse solutions to an increasingly sophisticated global customer base.

The Major Players in the Industry

- Richel Group

- Hoogendoorn Growth Management

- Priva

- Netafim

- Certhon

- Heliospectra

- Argus Controls

- Signify (Philips Horticulture)

- Rough Brothers Inc.

- GreenTech Agro LLC

- Sensaphone

- Gibraltar Industries

- Agra Tech Inc.

- LumiGrow

- AgriTech startup ecosystem (various)

Key Development

- In February 2024, Signify Holding introduced energy-efficient LED grow lighting solutions to improve crop productivity and reduce greenhouse energy consumption. The development supports sustainable and high-efficiency greenhouse farming practices.

- In January 2024, Netafim expanded its smart irrigation and precision greenhouse solutions to improve water efficiency and automated crop management. The initiative highlights growing adoption of precision agriculture technologies in controlled environment farming.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 7.0 Bn |

| Forecast Revenue (2035) | USD 30.2 Bn |

| CAGR (2026–2035) | 15.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020–2024 |

| Forecast Period | 2026–2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Offering Type (Hardware Systems, Software & Analytics, and Services (Installation, Maintenance)), By Component (HVAC Systems, LED Grow Lights, Irrigation Systems, Control Systems & Sensors, and Others), By Technology (Hydroponics, Aeroponics, Aquaponics, and Soil-based Smart Farming), By Crop Type (Fruits & Vegetables, Flowers & Ornamentals, Nursery Crops, and Others (Herbs, Medicinals)), By Greenhouse Type (Glass Greenhouses, Plastic Greenhouses, and Rigid Panel Greenhouses), By Automation Level (Fully Automated, Semi-Automated, and Manual/Assisted), By Application (Commercial Farming, Research & Education, Retail & Urban Farming, and Residential/Small-scale) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC- China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America- Brazil, Mexico & Rest of Latin America; Middle East & Africa- GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Richel Group, Hoogendoorn Growth Management, Priva, Netafim, Certhon, Heliospectra, Argus Controls, Signify (Philips Horticulture), Rough Brothers Inc., GreenTech Agro LLC, Sensaphone, Gibraltar Industries, Agra Tech Inc., LumiGrow, AgriTech startup ecosystem (various), and other key players. |

| Customization Scope | Customization for segments and region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |