Quick Navigation

- Report Overview

- Key Takeaways:

- U.S. Wireless Infrastructure Market Size

- Technology Segment Analysis

- Enterprise Size Segment Analysis

- End Use Industry Segment Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunities

- Challenging Factors

- Growth Factors

- Latest Trends

- Key Regions and Countries

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

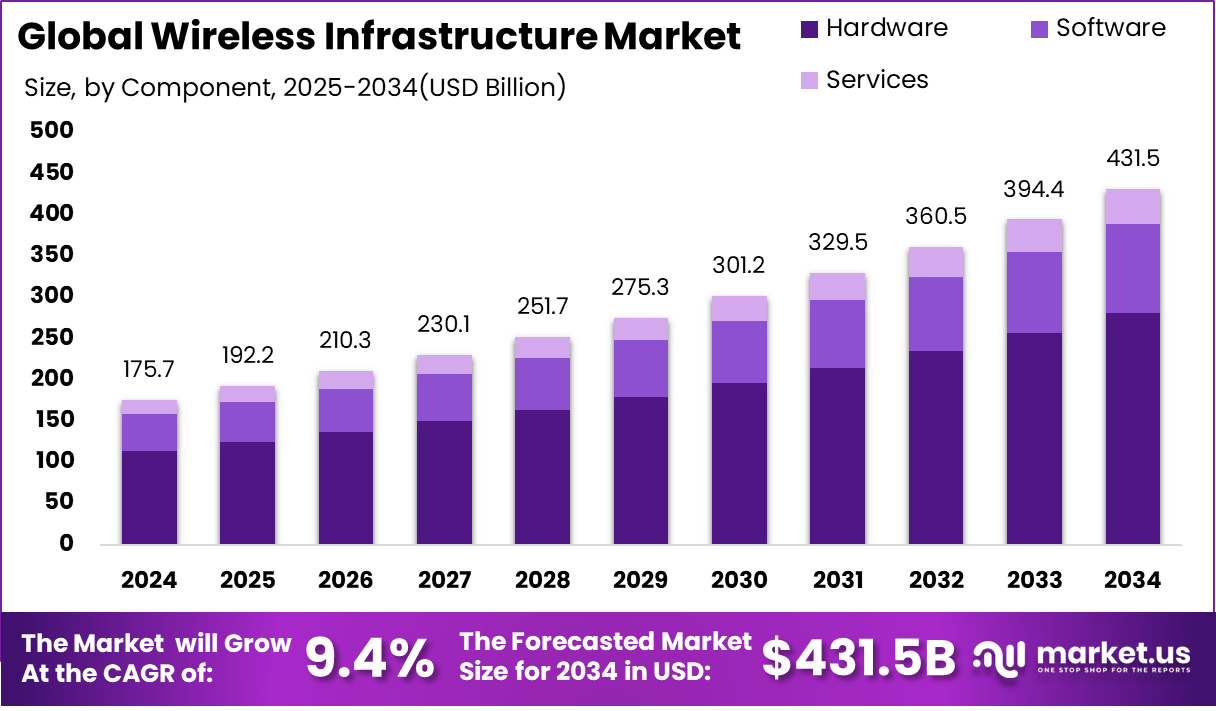

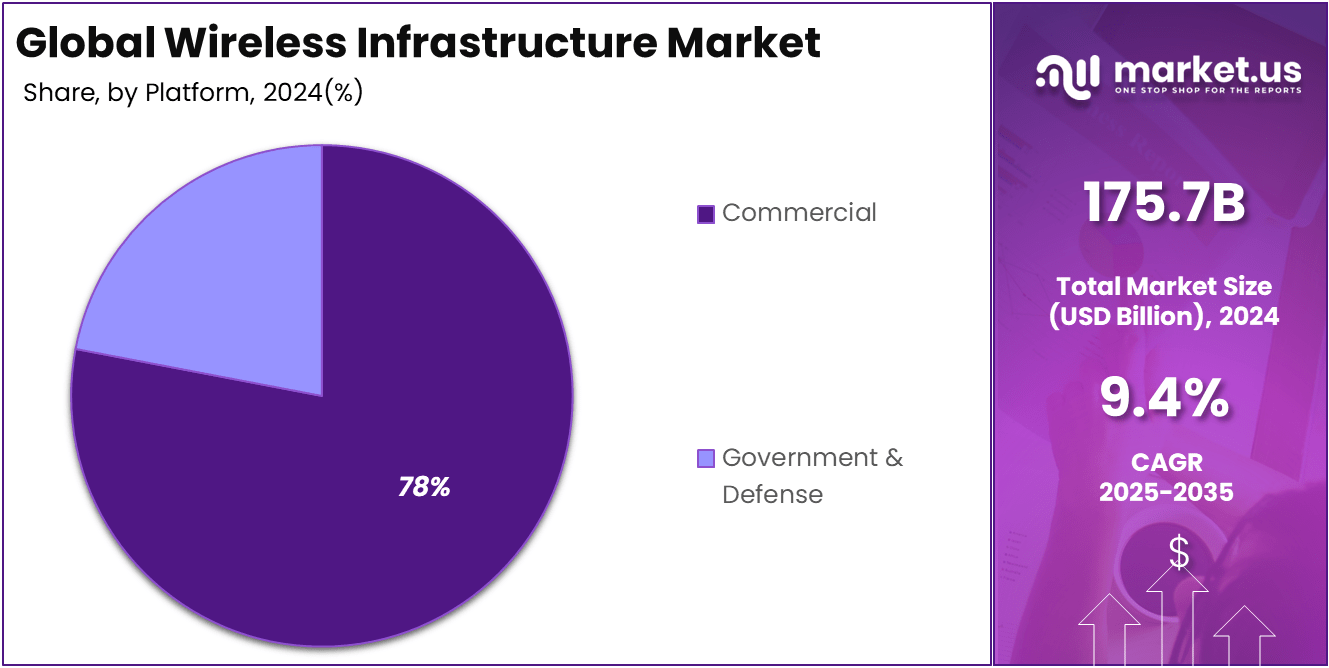

The Global Wireless Infrastructure Market size is expected to be worth around USD 431.5 billion by 2034, from USD 175.7 billion in 2024, growing at a CAGR of 9.4% during the forecast period from 2024 to 2033.

Wireless infrastructure refers to a collection of various connectivity solutions that operate together to offer a wireless network. Some of these include wireless local area networks (WLANs), cell phone networks, satellite communication networks, wireless sensor networks, and terrestrial microwave networks.

The market for wireless infrastructure is growing rapidly due to the growing demand for high-speed connectivity and advancements. Moreover, the increasing popularity of fast internet connection and the widespread adoption of smartphones as well as IoT devices have also contributed to the market growth. For instance, according to ITA, as of mid-2024, there are over 650 million smartphone users, and internet subscribers have surpassed 950 million.

Additionally, the ongoing trend of 5G technology has also reshaped the market. 5G provides a fast data speed, minimal delay, and a higher bandwidth to the customers. This has increased its adoption in the market, thus necessitating reliable wireless infrastructure including base stations, backhaul networks, core network equipment, and others.

Key Takeaways:

- In 2024, the Hardware segment held a dominant market position, capturing more than a 65% share of the Global Wireless Infrastructure Market.

- In 2024, the 4G and LTE segment held a dominant market position, capturing more than a 40% share of the Global Wireless Infrastructure Market.

- In 2024, the commercial segment held a dominant market position, capturing more than a 78% share of the Global Wireless Infrastructure Market.

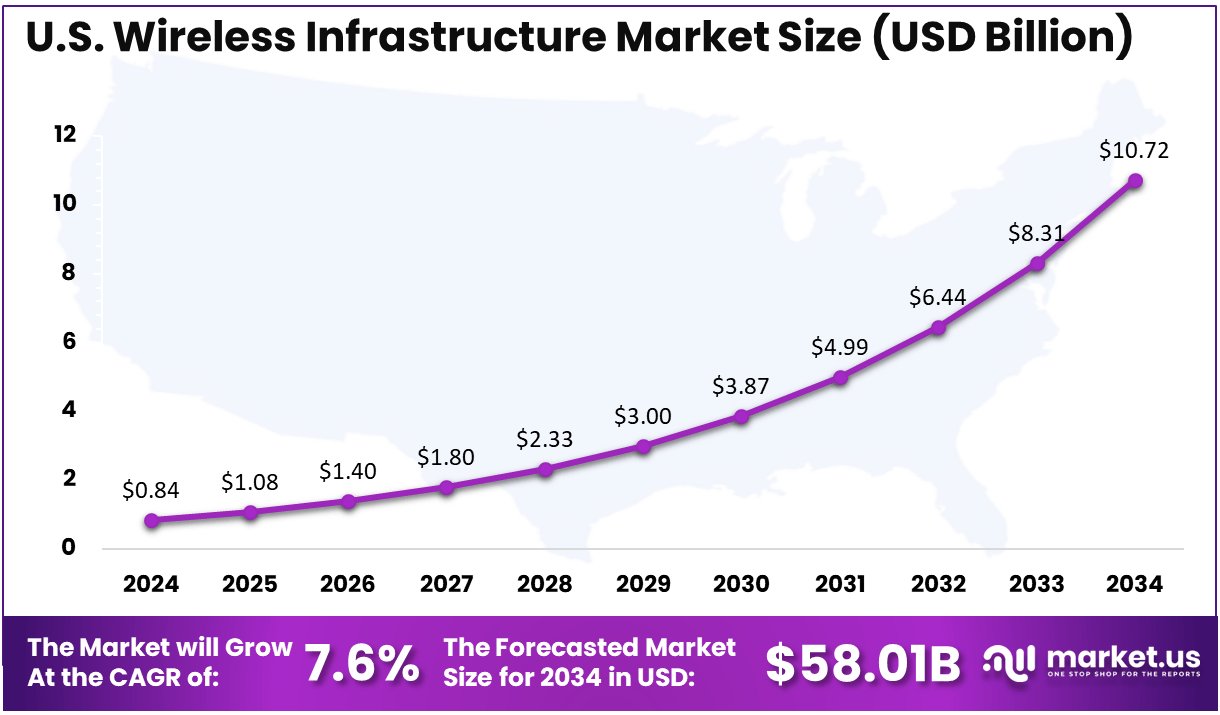

- The US Wireless Infrastructure Market was valued at USD 58.01 billion in 2024, with a robust CAGR of 6%.

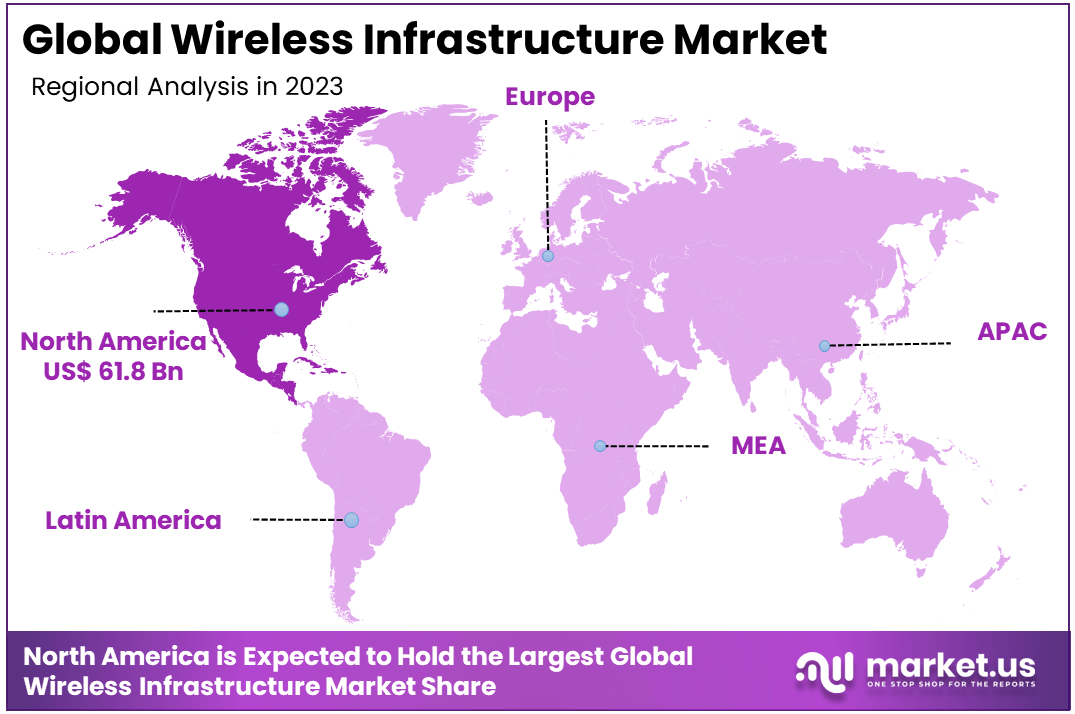

- In 2023, North America held a dominant market position in the global Wireless Infrastructure Market, capturing more than a 35.2% share.

- According to ISID, as of 2022, nearly 96% of internet access in India is wireless.

- According to WIA, The U.S. wireless & mobile industry spent USD 11.9 billion building additional capacity and coverage into the nation’s wireless networks.

U.S. Wireless Infrastructure Market Size

The US Wireless Infrastructure Market was valued at USD 58.01 billion in 2024, with a robust CAGR of 7.6%. This is majorly due to the presence of various technological companies like Qualcomm, Ericsson, and Cisco in the U.S., which play a crucial role in advancing wireless infrastructure.

Furthermore, both the federal and state governments are increasingly investing in digital transformation initiatives that tend to support the deployment of advanced wireless networks. For instance, the State of California has launched the California Broadband for All initiative, which aims to provide high-speed internet access to all residents. This initiative includes funding for infrastructure development, public-private partnerships, and regulatory support to ensure the deployment of advanced wireless networks across the state.

In 2023, North America held a dominant market position in the global Wireless Infrastructure Market, capturing more than a 35.2% share. This is majorly due to the high investment of telecom giants such as AT&T, T-Mobile, and Verizon in upgrading their networks, especially with the trend of 5G.

There is also a growing demand for advanced wireless services in North America due to the widespread use of connected devices, smart homes, and IoT applications. Additionally, the presence of robust and extensive telecom infrastructure makes it easier to deploy new technologies in the region.

Technology Segment Analysis

In 2024, the Hardware segment held a dominant market position, capturing more than a 65% share of the Global Wireless Infrastructure Market. This is majorly due to the increasing need to ensure higher reliability and performance of wireless infrastructure, where hardware plays a crucial role.

Hardware tends to form the backbone of wireless infrastructure, including the antennas, transceivers, and backhaul equipment. These elements are crucial for establishing and maintaining wireless communication networks.

Moreover, cutting-edge designs such as modular hardware components also allow for easy upgrades and maintenance of wireless infrastructure, thus reducing downtime and operational costs.

Enterprise Size Segment Analysis

In 2024, the 4G and LTE segment held a dominant market position, capturing more than a 40% share of the Global Wireless Infrastructure Market. This is due to the higher data transfer rates offered by the 4G and LTE networks. This makes them ideal for bandwidth-intensive applications such as online gaming, video conferencing, and video streaming.

Moreover, 4G and LTE networks offer a better network capacity, thus allowing users to connect simultaneously without compromising on performance or speed. It also supports advanced applications including smart cities and autonomous vehicles.

Additionally, 4G and LTE combine multiple frequency bands to increase the data speed and improve the overall networks. It also enables high-definition voice calls, thus offering better call quality and networking.

End Use Industry Segment Analysis

In 2024, the commercial segment held a dominant market position, capturing more than a 78% share of the Global Wireless Infrastructure Market. This is due to the need for high-speed connectivity for commercial aspects such as video conferencing, cloud services, and online transactions.

Moreover, the proliferation of IoT devices in commercial settings such as smart factories, retail environments, and logistics, increases the need for extensive wireless infrastructure to ensure seamless connectivity.

There is also a constant push to increase the mobile and broadband services in the rural and urban areas. This drives the need for extensive wireless infrastructure in commercial areas.

Key Market Segments

By Component

- Hardware

- Small Cells

- Radio Access Network (RAN)

- Macro Cells

- Backhaul

- Mobile Core

- SATCOM

- Others

- Software

- Network Management Tools

- Optimization Solutions

- Services

- Installation & Deployment

- Maintenance & Support

- Consulting & Integration

By Type

- Satellite

- 2G and 3G

- 4G and LTE

- 5G

By Platform

- Commercial

- Government & Defense

Driving Factors

Growth of IoT devices

IoT devices are being increasingly used in homes and offices. This drives the market as it relies on wireless connectivity to function and communicate. With the increase in the number of these devices, the demand for reliable and robust wireless networks would also increase.

Additionally, IoT devices generate a vast amount of data. For instance, a smart factory could have thousands of sensors that continuously transmit data about machinery performance. This demands an advanced wireless infrastructure that is capable of handling high bandwidth.

Restraining Factors

Higher capital investment

High capital investment significantly restraints the wireless infrastructure market. Setting up wireless infrastructure, including cell towers, fiber optic cables, and base stations, need a substantial financial resource. This could be a barrier to the new entrants as well as the small companies operating in the market.

Furthermore, the ongoing maintenance and regular upgrades of the infrastructure also demand significant investments. These costs could strain the budget of the network operators.

Growth Opportunities

Integration of edge computing

The integration of edge computing presents a crucial opportunity for the market. Edge computing processes the data closer to the source, thus reducing the time it takes to send the data to a central server and back. This is crucial for real-time applications, such as autonomous vehicles, industrial automation, and remote healthcare management.

Furthermore, edge computing processes data locally and reduces the amount of data that needs to be transmitted over the network, thus freeing up bandwidth for other users and improving the overall network efficiency.

Challenging Factors

Managing interference and congestion in densely populated areas

Managing interference and congestion in densely populated areas presents a challenge for the wireless infrastructure market. In urban environments, several devices and wireless networks are operating nearby. This can cause significant signal interference and degrade the quality of wireless connections.

Further, there are various physical obstructions such as buildings and others in urban areas, obstructing the wireless signals. Moreover, the high density of users and devices in urban areas can overwhelm wireless networks, thus leading to congestion.

Growth Factors

Various innovations in wireless technology such as small cells, massive MIMO, and edge computing are enhancing the network performance and efficiency, thus driving the market growth.

Furthermore, businesses are increasingly adopting digital solutions and cloud services, that need reliable wireless connectivity to support operations and improve efficiency. Consumers are also demanding seamless connectivity in both personal and professional environments, driving the need for wireless infrastructure.

Latest Trends

AI and machine learning are being integrated into the wireless infrastructure to optimize network performance, predict maintenance needs, and enhance security. This trend is reshaping the market.

Moreover, network operators are also deploying more small cells and distributed antenna systems to densify the networks, particularly in urban areas. This could promote the adoption of wireless infrastructures.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

One of the leading players in the market is Huawei Technologies, which offers a comprehensive range of wireless infrastructure solutions, specially designed to meet the diverse needs of modern networks. Another prominent player in the market is Capgeminwhichat provides a portfolio of over 70 software frameworks for wireless technologies, designed to accelerate innovation.

Top Key Players in the Market

- Huawei Technologies Co., Ltd.

- NXP Semiconductors

- Capgemini

- Qualcomm Technologies Inc.

- NEC Corporation

- Cisco Systems, Inc.

- D-Link Corporation

- Fujitsu Ltd.

- Ciena Corporation

- ZTE Corporation

- Telefonaktiebolaget LM Ericsson

- Juniper Networks

- Mavenir Systems Inc.

- Capgemini SE

- Other Key Players

Recent Developments

- In October 2024, Qualcomm Launches New Wireless Networking Platform With AI. This uses the latest Wi-Fi 7 technology and any connected devices are empowered with powerful and centralized generative AI processing capabilities.

- In September 2024, NVIDIA launched its AI Aerial which is a suite of accelerated computing software and hardware for designing, simulating, training, ing and deploying AI radio access network technology (AI-RAN) for wireless networks in the AI era.

- In July 2024, Guerrilla RF, Inc. announced the release of its new GRF5112, a highly linear, broadband power amplifier that excels in delivering excellent compression performance over large fractional bandwidths of up to 40 percent. The GRF5112’s broad, single-tuned responses enable multicarrier base stations to simultaneously transmit across two or more cellular bands using a single RF lineup.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 175.7 billion |

| Forecast Revenue (2034) | USD 431.5 billion |

| CAGR (2025-2034) | 9.4% |

| Largest Market | North America |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Hardware (Small Cells, Radio Access Network (RAN), Macro Cells, Backhaul, Mobile Core, SATCOM, Others), Software (Network Management Tools, Optimization Solutions), Services (Installation & Deployment, Maintenance & Support, Consulting & Integration), By Type (Satellite, 2G and 3G, 4G and LTE, 5G), By Platform (Government & Defense, Commercial), Region |

| Regional Analysis | North America (US, Canada), Europe (Germany, UK, Spain, Austria, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of Asia-Pacific), Latin America (Brazil), Middle East & Africa(South Africa, Saudi Arabia, United Arab Emirates) |

| Competitive Landscape | Huawei Technologies Co., Ltd., NXP Semiconductors, Capgemini, Qualcomm Technologies Inc., NEC Corporation, Cisco Systems, Inc., D-Link Corporation, Fujitsu Ltd., Ciena Corporation, ZTE Corporation, Telefonaktiebolaget LM Ericsson, Juniper Networks, Mavenir Systems Inc., Capgemini SE, Other Key Players |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |