Quick Navigation

Report Overview

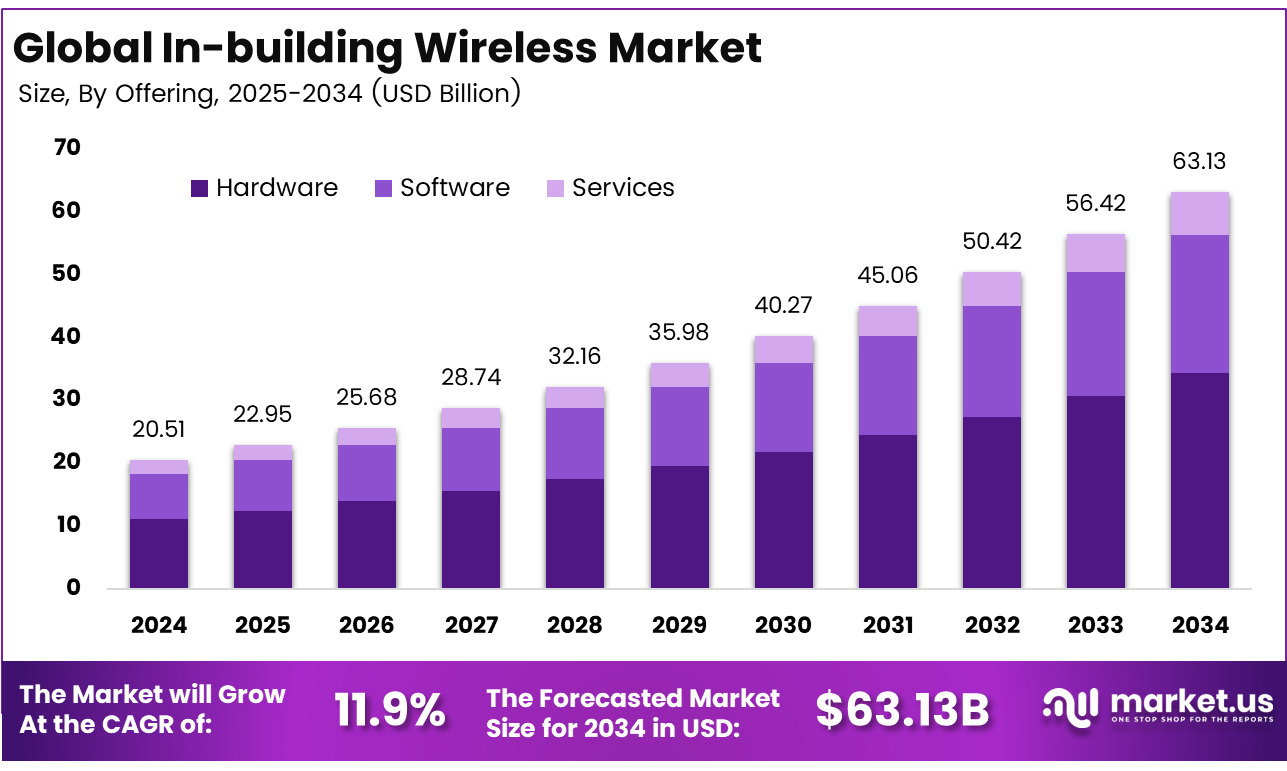

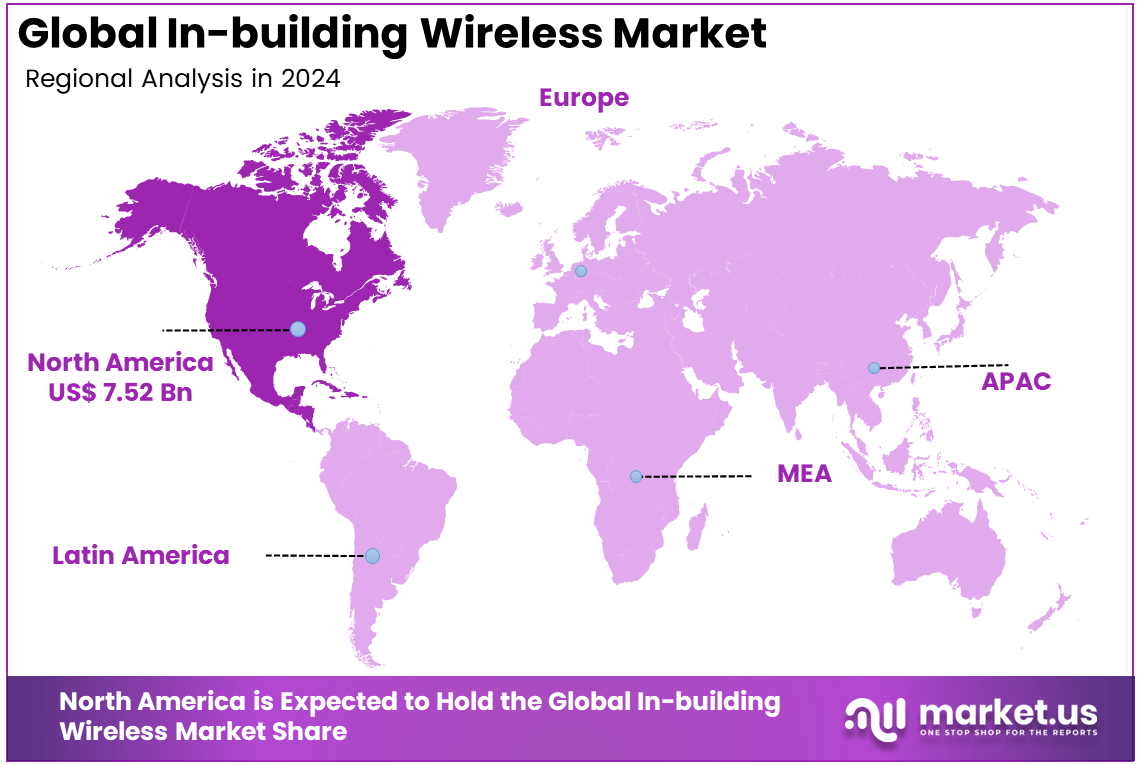

The Global In-building Wireless Market size is expected to be worth around USD 63.13 billion by 2034, from USD 20.51 billion in 2024, growing at a CAGR of 11.9% during the forecast period from 2025 to 2034. North America held a dominant market position, capturing more than a 36.7% share, holding USD 7.52 billion in revenue.

The market for in-building wireless is primarily driven by the growing demand for seamless, high-speed connectivity within buildings. The rise of mobile data usage, the expansion of 5G networks, and the increasing integration of IoT devices in smart buildings are key factors fueling this growth. As businesses and consumers demand more reliable and faster wireless services, especially in high-density environments like offices, malls, and airports, the need for advanced in-building wireless solutions continues to escalate, ensuring consistent and efficient coverage across diverse indoor spaces.

For instance, in May 2023, Strategic Venue Partners expanded its leadership team to address the growing demand for wireless connectivity and in-building infrastructure. The company’s move to strengthen its team highlights the increasing need for advanced in-building wireless solutions in venues, commercial spaces, and large buildings.

Scope and Forecast

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 20.51 Billion |

| Forecast Revenue (2034) | USD 63.13 Billion |

| CAGR (2025-2034) | 11.9% |

| Largest market in 2024 | North America [36.7% market share] |

Key Takeaway

- In 2024, the Hardware segment held a dominant market position, capturing a 54.3% share of the Global In-building Wireless Market.

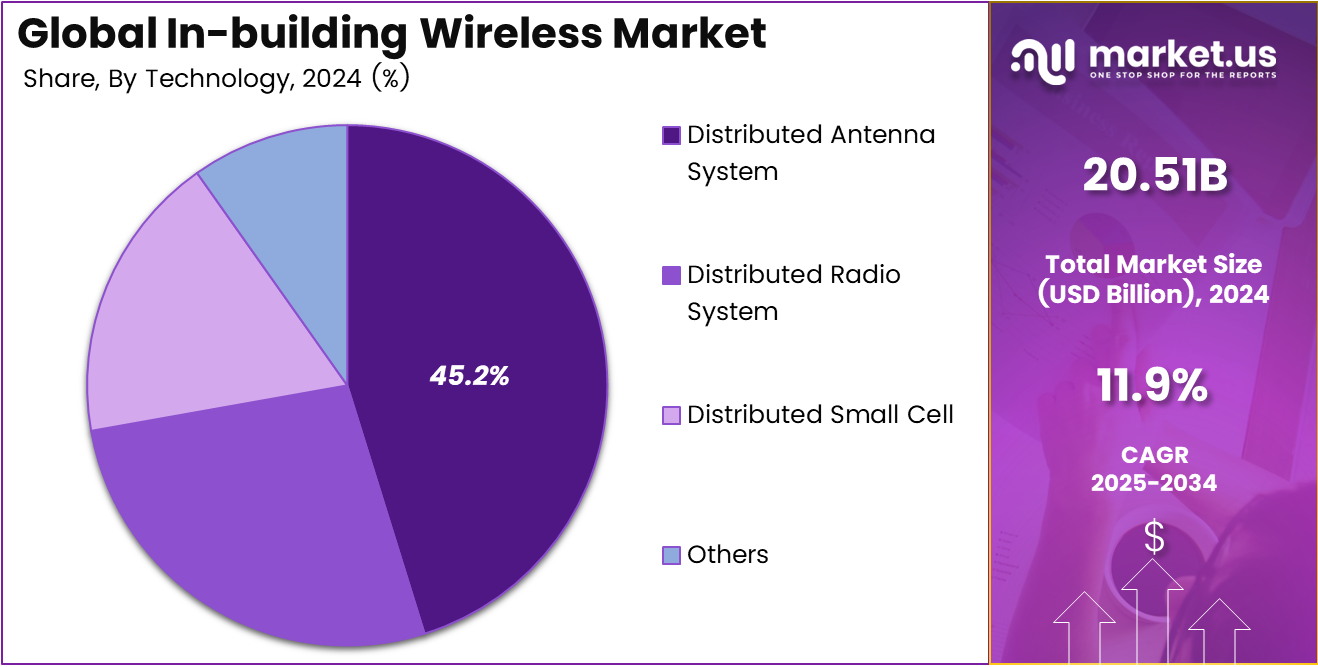

- In 2024, the Distributed Antenna System (DAS) segment held a dominant market position, capturing a 45.2% share of the Global In-building Wireless Market.

- In 2024, the Service Providers segment held a dominant market position, capturing a 47.4% share of the Global In-building Wireless Market.

- In 2024, the Large Buildings segment held a dominant market position, capturing a 63.1% share of the Global In-building Wireless Market.

- In 2024, the Public Network segment held a dominant market position, capturing a 58% share of the Global In-building Wireless Market.

- In 2024, the Commercial Campuses segment held a dominant market position, capturing a 21.8% share of the Global In-building Wireless Market.

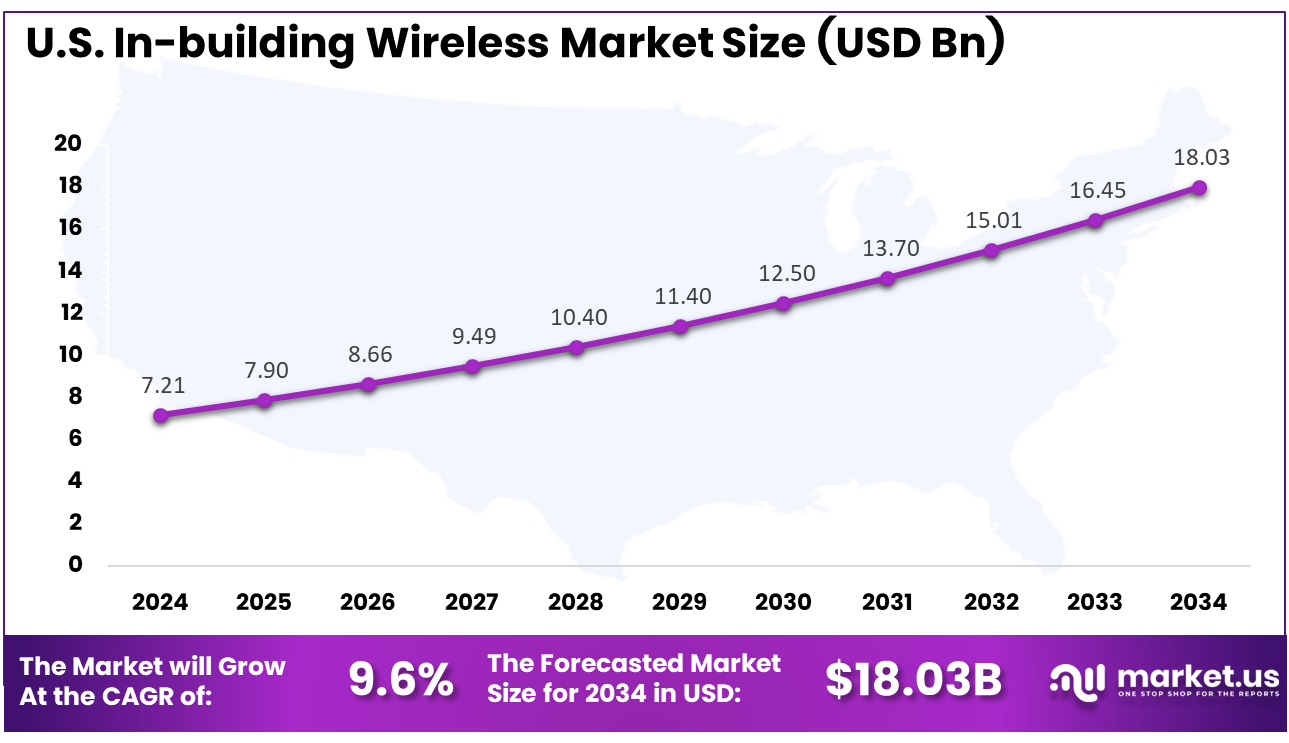

- The U.S. In-building Wireless Market was valued at USD 7.21 billion in 2024, with a robust CAGR of 9.6%.

- In 2024, North America held a dominant market position in the Global In-building Wireless Market, capturing more than a 36.7% share.

Regional Analysis

In 2024, North America held a dominant market position in the Global In-building Wireless Market, capturing more than a 36.7% share, holding USD 7.52 billion in revenue. The dominance is due to the rapid adoption of advanced technologies like 5G and IoT. The region’s strong infrastructure, high demand for seamless connectivity in commercial and residential buildings, and widespread smart building initiatives by the government further fueled growth. Additionally, the shift to hybrid work models and mobile-first environments in the U.S. and Canada increased the need for reliable in-building wireless solutions, strengthening the region’s leadership in the market.

For instance, in February 2023, Ericsson launched new solutions to boost indoor 5G capacity and precise location services, further solidifying North America’s dominance in the in-building wireless market. These innovations aim to enhance wireless coverage and improve the accuracy of indoor location-based services across various industries.

U.S. In-Building Wireless Market Size

The market for In-building Wireless within the U.S. is growing tremendously and is currently valued at USD 7.21 billion. The market has a projected CAGR of 9.6%. The market is expanding rapidly due to the rising demand for fast, reliable connectivity in both commercial and residential areas. The nationwide deployment of 5G, combined with the growth of smart buildings and IoT devices, has increased the need for advanced wireless infrastructure. The shift to remote work and mobile-first environments also drives the demand for strong wireless coverage in offices and public spaces. Partnerships between telecom providers and building owners are further accelerating this growth, enhancing operational efficiency and user experience.

For instance, in March 2025, Connectivity Wireless secured $200 million in capital from First Citizens Bank and Post Road Group to accelerate its growth in the U.S. in-building wireless market. This strategic funding will help the company expand its portfolio of advanced wireless solutions, including Distributed Antenna Systems (DAS) and small cells, addressing the rising demand for reliable and high-speed connectivity in commercial and residential buildings.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Offering Analysis

In 2024, the Hardware segment held a dominant market position, capturing a 54.3% share of the Global In-building Wireless Market. The dominance is due to the critical role of hardware components like antennas, distributed antenna systems (DAS), and small cells in providing reliable, high-speed connectivity within buildings. As the demand for seamless wireless coverage in commercial and residential spaces rises, the need for advanced hardware solutions grows. The widespread adoption of 5G, IoT devices, and smart building technologies further fuels the need for scalable hardware.

For instance, in October 2024, ADRF launched its first Part-20 SDRC Series Repeater, designed to deliver instant indoor wireless connectivity. This advanced hardware solution, incorporating high-performance antennas, ensures seamless coverage within buildings by amplifying wireless signals. The repeater is a key component in enhancing in-building wireless systems, enabling reliable and fast connectivity across commercial and residential spaces.

Technology Analysis

In 2024, the Distributed Antenna System (DAS) segment held a dominant market position, capturing a 45.2% share of the Global In-building Wireless Market. The demand has been primarily driven by the need for enhanced wireless coverage and capacity in large, complex environments such as commercial buildings, stadiums, and airports. DAS solutions ensure reliable connectivity by distributing signals evenly across indoor spaces, addressing issues like signal degradation caused by building materials, and supporting the growing demand for high-speed data and mobile communication.

For instance, in April 2025, Airspan completed the acquisition of Corning’s wireless business, which includes a significant portfolio of Distributed Antenna System (DAS) technologies. This strategic acquisition enhances Airspan’s ability to provide advanced in-building wireless solutions, particularly in high-demand environments like stadiums, office buildings, and large public spaces.

Business Model Analysis

In 2024, the Service Providers segment held a dominant market position, capturing a 47.4% share of the Global In-building Wireless Market. This dominance is primarily due to the critical role service providers play in delivering reliable and high-speed wireless connectivity. They are key players in deploying and managing in-building wireless solutions, including DAS and small cells, to ensure seamless coverage for businesses and residential areas. Their ability to integrate cutting-edge technologies like 5G and IoT further boosts their market leadership and customer demand.

For instance, in May 2025, Airspan outlined its vision for purpose-built in-building wireless solutions, emphasizing the growing role of service providers in delivering customized wireless coverage. Airspan’s approach focuses on creating tailored solutions that meet the unique connectivity needs of various industries, including commercial spaces, healthcare, and large public venues.

Building Size Analysis

In 2024, the Large Buildings segment held a dominant market position, capturing a 63.1% share of the Global In-building Wireless Market. This dominance is due to the high demand for reliable wireless connectivity in large-scale environments such as office towers, shopping malls, and stadiums. These buildings require robust in-building wireless solutions like DAS and small cells to ensure seamless coverage across expansive areas. The growing need for high-speed data, especially with the rise of 5G and IoT devices, further supports the demand in this segment.

For instance, in June 2025, Cenomi Centers partnered with TAWAL to enhance indoor mobile coverage across its malls. This collaboration focuses on deploying advanced in-building wireless solutions to ensure seamless connectivity for shoppers and retailers. By improving mobile coverage, the partnership aims to provide better user experiences, enabling efficient use of mobile apps, e-commerce, and IoT devices within the mall environment.

Network Type Analysis

In 2024, the Public Network segment held a dominant market position, capturing a 58% share of the Global In-building Wireless Market. This dominance is due to the widespread reliance on public networks for mobile connectivity in urban areas, commercial spaces, and public venues. Public networks, supported by major telecom operators, provide extensive coverage and scalability, catering to the growing demand for seamless wireless experiences. The expansion of 5G networks and increased mobile data usage further strengthen the role of public networks in in-building wireless solutions.

For instance, in May 2025, Wilson Connectivity launched the WilsonPro Enterprise 5143U in-building cellular repeater in the UK market, targeting enhanced mobile coverage for public networks in commercial buildings. The repeater amplifies cellular signals, ensuring seamless connectivity for users within large buildings, such as offices and shopping centers.

End-User Analysis

In 2024, the Commercial Campuses segment held a dominant market position, capturing a 21.8% share of the Global In-building Wireless Market. This dominance is due to the increasing need for robust wireless connectivity in large office buildings, corporate campuses, and mixed-use developments. As businesses adopt digital transformation, the demand for seamless communication, high-speed data transfer, and IoT integration within these spaces grows. In-building wireless solutions, such as DAS and small cells, are essential for maintaining reliable coverage and enhancing operational efficiency in commercial campuses.

For instance, in June 2025, Nokia and Andorix partnered to enhance private 5G solutions for commercial campuses, focusing on advanced in-building wireless connectivity. This collaboration aims to provide secure, high-performance wireless networks tailored to the unique needs of commercial environments, enabling efficient communication and seamless integration of IoT devices.

Key Market Segments

By Offering

- Hardware

- Head End Units

- Remote Units

- Repeaters

- Antennas

- Femtocells

- Others

- Software

- Network Planning & Design

- Network Management

- Others

- Services

- Professional Services

- Network Design

- Integration & Deployment

- Training, Support, & Maintenance

- Managed Services

- Professional Services

By Technology

- Distributed Antenna System

- Distributed Radio System

- Distributed Small Cell

- Others

By Business Model

- Service Providers

- Enterprises

- Neutral Host Operators

By Building Size

- Large Buildings

- Small & Medium-sized Buildings

By Network Type

- Public Network

- Private Network

By End-User

- Commercial Campuses

- Government

- Transportation & Logistics

- Hospitality

- Industrial & Manufacturing

- Entertainment & Sports Venues

- Education

- Healthcare

- Others

Latest Trends

The adoption of neutral host models is becoming a key trend in the in-building wireless market. This approach allows multiple wireless carriers to share a single infrastructure, significantly reducing deployment costs and improving coverage efficiency. By consolidating resources, building owners can offer seamless connectivity to various carriers without the need for separate installations. This model is especially beneficial in high-traffic locations like shopping malls, airports, and office buildings, where efficient and cost-effective wireless coverage is crucial for user satisfaction and business operations.

For instance, in July 2025, Nokia, CST, and their partners launched a 4.0 GHz neutral host network in Saudi Arabia, marking a significant step forward in the region’s connectivity landscape. This new network model allows multiple mobile network operators to share the same infrastructure, reducing deployment costs and enhancing network efficiency.

Market Dynamics

Drivers - IoT and Smart Building Integration

The increasing integration of IoT devices in buildings, such as smart thermostats, lighting systems, and security cameras, is fueling the demand for robust in-building wireless networks. These devices require continuous, high-speed connectivity for efficient operation, leading to a greater need for reliable wireless infrastructure. As buildings become smarter, ensuring seamless communication between connected devices is essential, driving the adoption of advanced wireless technologies that can support the growing IoT ecosystem.

For instance, in July 2025, Siemens and Microsoft teamed up to enable open-standard IoT for smart buildings, a significant development in the integration of IoT and in-building wireless systems. Their collaboration aims to provide seamless connectivity and interoperability for smart building technologies, including lighting, HVAC, and security systems.

Restraint - High Initial Installation Costs

Deploying advanced in-building wireless systems comes with high upfront costs, including the installation of infrastructure and the purchase of necessary equipment. For small and medium-sized businesses, this high initial investment can be a major barrier to adoption. The expense of retrofitting older buildings with modern wireless solutions adds another layer of complexity and cost, slowing down widespread adoption. Without a clear, immediate ROI, some businesses may hesitate to make the necessary financial commitment for in-building wireless systems.

For instance, in December 2024, SOLID secured a $27.68 million grant to advance Open RAN for in-building 5G, showcasing the ongoing challenges of high initial installation costs in the in-building wireless market. Despite the significant investment required for deploying advanced infrastructure, the grant will help reduce costs by leveraging Open RAN technology, which offers a more flexible and cost-effective approach to network deployment.

Opportunities - Expansion of 5G Networks

The global rollout of 5G networks offers a significant opportunity to enhance in-building wireless systems. 5G promises faster data speeds, lower latency, and the ability to support a greater number of connected devices, making it ideal for businesses and consumers alike. This expansion enables the deployment of more reliable, efficient, and high-performance wireless networks within buildings, enhancing user experience and driving the need for advanced in-building solutions to support emerging technologies like augmented reality and smart environments.

For instance, in March 2025, Fujitsu announced the launch of its advanced 5G in-building wireless solution, designed to provide enhanced connectivity for businesses and public spaces. The new system integrates cutting-edge technology to ensure high-speed, low-latency communication across complex indoor environments. This solution is part of Fujitsu’s broader efforts to support the growing demand for seamless 5G coverage in commercial buildings and urban areas.

Challenges - Competition Among Providers

The in-building wireless market is highly competitive, with numerous players offering similar solutions. Companies are constantly striving to differentiate themselves through innovation, pricing, and service offerings. With various technologies like DAS, Wi-Fi, and small cells available, distinguishing one’s product from competitors becomes increasingly difficult. As new entrants continue to emerge, companies must focus on building strong value propositions, offering tailored solutions, and improving customer experience to capture and retain market share in this crowded space.

For instance, in January 2025, Freshwave deployed all-operator 4G in-building connectivity across the City of London, showcasing the increasing competition among providers in the in-building wireless market. By enabling seamless connectivity for all mobile network operators within one infrastructure, Freshwave aims to enhance service quality and coverage in the heart of London’s business district.

Key Players Analysis

One of the leading players in the market, in October 2024, CommScope announced a partnership with the Cleveland Cavaliers to enhance the in-building wireless connectivity at Rocket Mortgage FieldHouse, home to the team. The collaboration focuses on upgrading the venue’s wireless infrastructure, ensuring seamless connectivity for fans, staff, and visitors. By deploying advanced Distributed Antenna Systems (DAS) and other cutting-edge wireless solutions, CommScope aims to provide high-speed, reliable coverage, improving the overall fan experience during events and supporting the increasing demand for mobile data in large public venues.

Top Key Players in the Market

- CommScope Holding Co.

- Cisco Systems Inc.

- Corning Inc.

- Ericsson AB

- Nokia Corp.

- AT&T Inc.

- Verizon Communications Inc.

- Pierson Wireless Corp.

- Cobham PLC

- Cambium Networks

- TE Connectivity Ltd.

- Dali Wireless Inc.

- Airspan Networks

- American Tower Corp.

- Boingo Wireless Inc.

- Extreme Networks Inc.

- Juniper Networks Inc.

- HPE (Aruba Networks)

- Samsung Electronics (Co. Networks)

- Huawei Technologies Co. Ltd.

- Others

Recent Developments

- In March 2025, Corning showcased new AI solutions at the 2025 Optical Fiber Communication Conference and Exposition, aimed at helping operators build dense optical networks and enable interconnected data centers. These innovations support the increasing need for high-performance in-building wireless infrastructure.

- In May 2025, Juniper Networks introduced advancements in wireless networking at the Smart City Expo US 2025, focusing on solutions that support in-building wireless infrastructure in urban environments.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 20.51 Billion |

| Forecast Revenue (2034) | USD 63.13 Billion |

| CAGR (2025-2034) | 11.9% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Offering (Hardware, Software, Services), By Technology (Distributed Antenna System, Distributed Radio System, Distributed Small Cell, Others), By Business Model (Service Providers, Enterprises, Neutral Host Operators), By Building Size (Large Buildings, Small & Medium sized Buildings), By Network Type (Public Network, Private Network), By End-User (Commercial Campuses, Government, Transportation & Logistics, Hospitality, Industrial & Manufacturing, Entertainment & Sports Venues, Education, Healthcare, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | CommScope Holding Co., Cisco Systems Inc., Corning Inc., Ericsson AB, Nokia Corp., AT&T Inc., Verizon Communications Inc., Pierson Wireless Corp., Cobham PLC, Cambium Networks, TE Connectivity Ltd., Dali Wireless Inc., Airspan Networks, American Tower Corp., Boingo Wireless Inc., Extreme Networks Inc., Juniper Networks Inc., HPE (Aruba Networks), Samsung Electronics (Co. Networks), Huawei Technologies Co. Ltd., Others |

| Customization Scope | Customization at the segment and region/country levels will be provided. Moreover, customization can be tailored to the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |