Quick Navigation

- Report Overview

- Key Takeaways

- By Coating Type Analysis

- By Coating Technique Analysis

- By Coating Type Analysis

- By Electrical Steel Type Analysis

- By Application Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

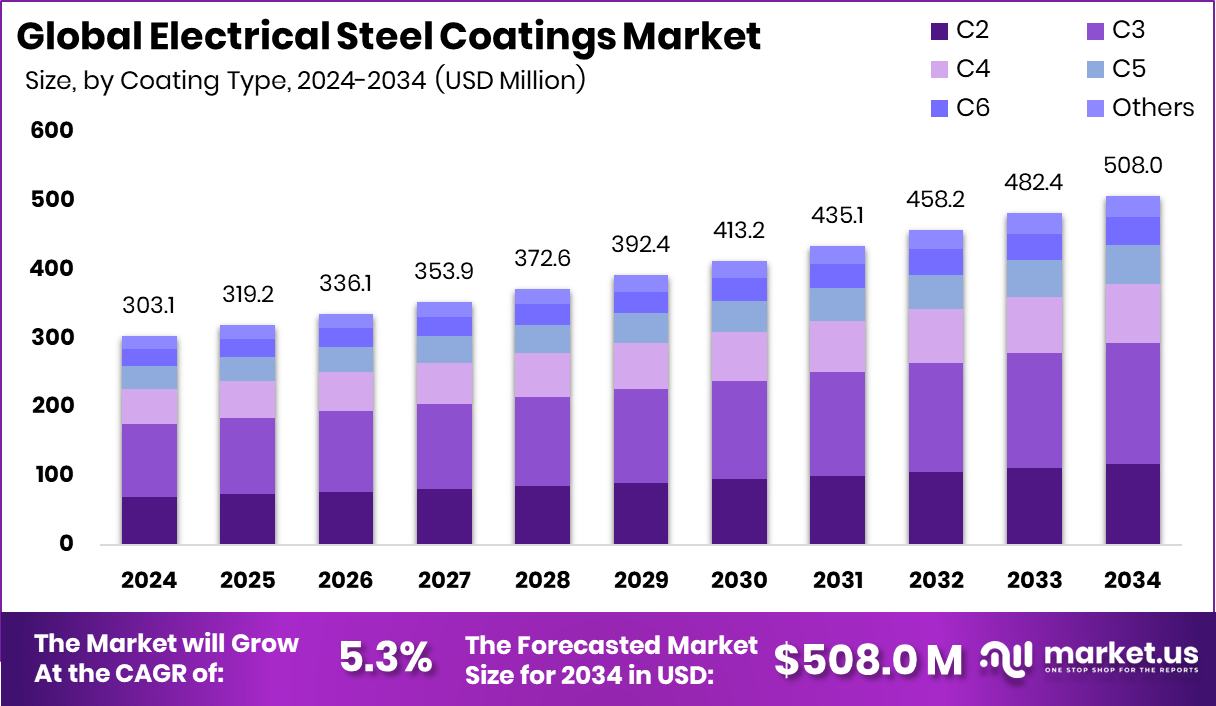

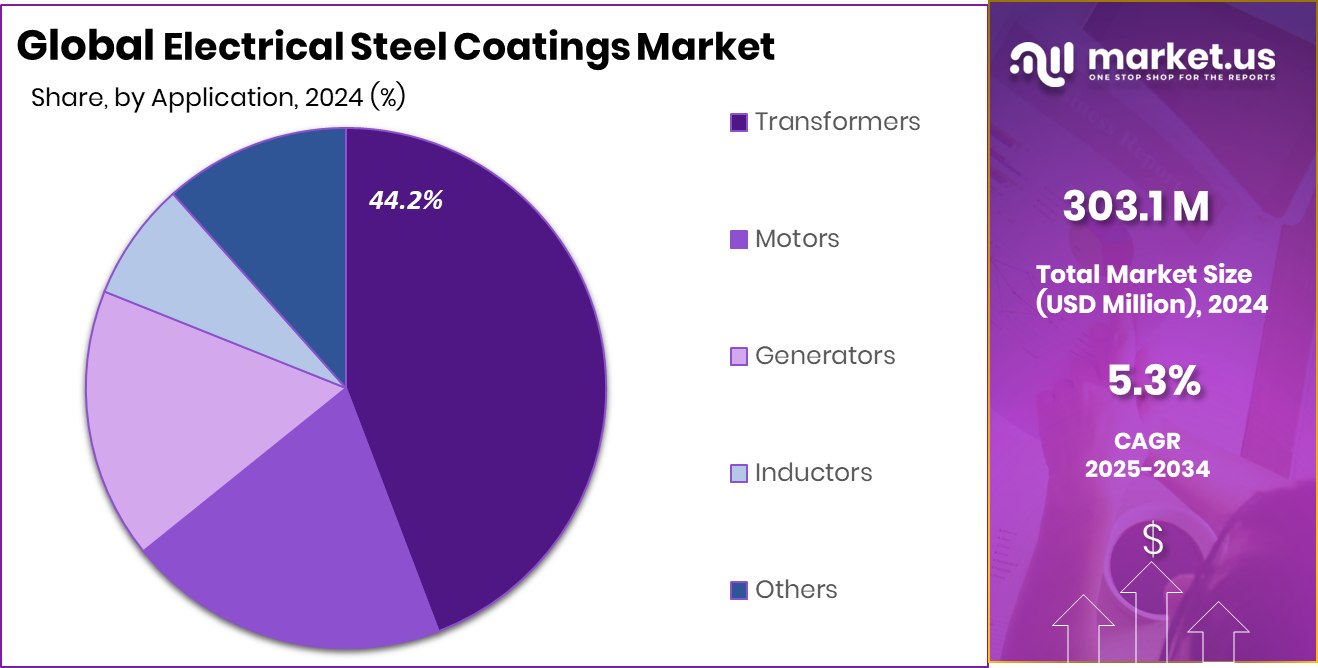

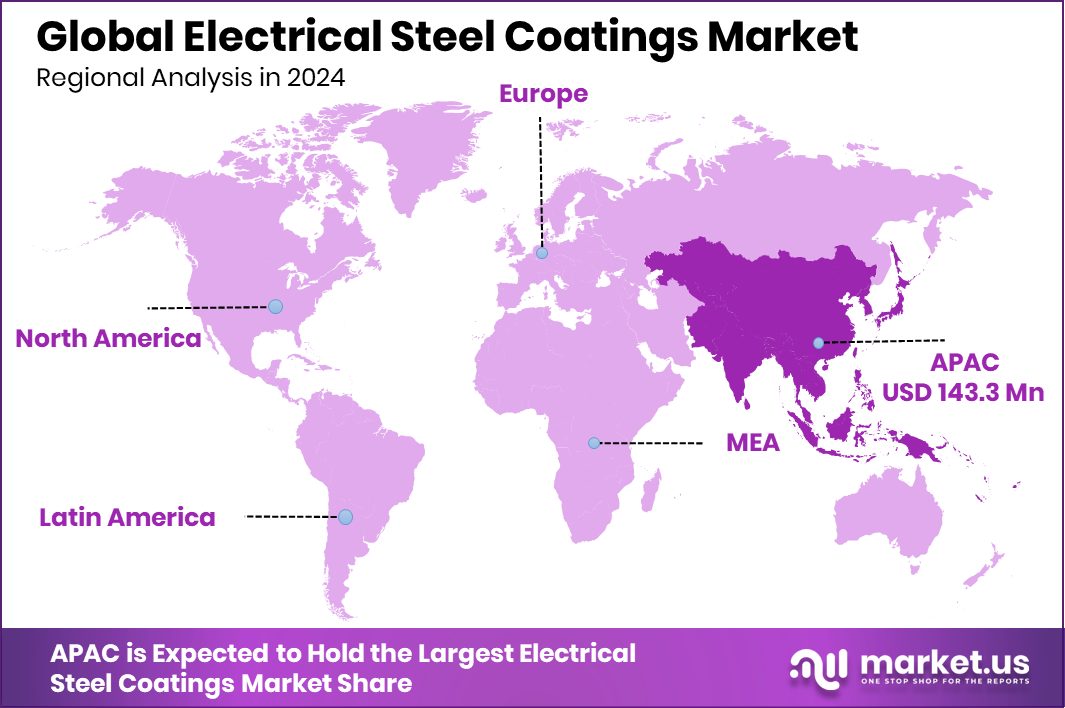

Global Electrical Steel Coatings Market is expected to be worth around USD 508.0 million by 2034, up from USD 303.1 million in 2024, and grow at a CAGR of 5.3% from 2025 to 2034. Asia-Pacific led demand for coated steel, holding a 47.3% regional market share.

Electrical steel coatings are specially formulated insulating layers applied to electrical steel sheets used in transformers, motors, and generators. These coatings prevent eddy current losses by insulating individual laminations, improve corrosion resistance, and reduce noise and wear caused by vibration. They also enhance the thermal stability of electrical components, making them essential for high-efficiency energy equipment.

The electrical steel coatings market revolves around the supply and demand of insulation coatings used on non-grain-oriented and grain-oriented electrical steel. This market supports key industries like automotive, energy, and appliances, which rely on efficient electromagnetic performance. It includes various coating types, such as inorganic, organic, and hybrid coatings, tailored for different operational environments and electrical applications.

A primary growth driver is the global push for energy-efficient systems. With rising electricity consumption and grid upgrades, coated electrical steels are vital for reducing transmission losses. Moreover, the growing use of electric motors in appliances, vehicles, and industrial equipment increases the demand for high-quality coated steel laminations.

The surge in electric vehicle production and the expansion of renewable energy installations have sharply increased the need for coated electrical steel. These applications require precise insulation to meet performance and safety standards, making the coatings indispensable. According to an industry report, in February 2025, ArcelorMittal revealed plans to invest $1.2 billion in building a new electrical steel production facility in Calvert, Alabama.

Key Takeaways

- Global Electrical Steel Coatings Market is expected to be worth around USD 508.0 million by 2034, up from USD 303.1 million in 2024, and grow at a CAGR of 5.3% from 2025 to 2034.

- C3 coatings hold 34.8% market share in the Electrical Steel Coatings Market by coating type.

- Physical Vapor Deposition technique dominates with a 45.1% share among all coating application methods globally.

- Epoxy coatings lead the market with a 53.3% share due to superior insulation and corrosion resistance.

- Grain-oriented electrical steel accounts for 58.9% share, driven by transformer and high-efficiency motor demand.

- Transformers remain the top application, holding 44.2% market share in electrical steel coatings usage.

- Strong transformer production in Asia-Pacific boosted market value to USD 143.3 million.

By Coating Type Analysis

C3 coating type leads the Electrical Steel Coatings Market with 34.8%.

In 2024, C3 held a dominant market position in the By Coating Type segment of the Electrical Steel Coatings Market, with a 34.8% share. This coating type is widely preferred due to its excellent insulation performance, heat resistance, and adaptability across various electrical applications. C3 coatings are typically used on both grain-oriented and non-grain-oriented electrical steels, making them suitable for transformers, electric motors, and generators where precise electrical insulation and operational efficiency are critical.

The demand for C3 coatings has been supported by the increasing need for advanced materials that can meet evolving performance standards in modern power and automotive systems. Their ability to maintain structural stability under high thermal and magnetic stresses has further solidified their position in high-voltage equipment and energy-efficient motors. In addition, C3 coatings offer good adhesion and corrosion resistance, making them a reliable choice for long-term use in humid or industrial environments.

Manufacturers continue to favor this coating type due to its balanced performance-to-cost ratio and compliance with stringent electrical insulation norms. With ongoing grid modernization and electrification initiatives worldwide, C3 coatings are expected to maintain their leadership in the coating type segment, driven by continued application in energy infrastructure and sustainable transportation systems.

By Coating Technique Analysis

Physical Vapor Deposition technique dominates coating processes, holding 45.1% market share.

In 2024, Physical Vapor Deposition held a dominant market position in the by-coating-technique segment of the Electrical Steel Coatings Market, with a 45.1% share. This technique is widely recognized for producing uniform, high-performance coatings with excellent adhesion and controlled thickness. Physical Vapor Deposition (PVD) is favored in the electrical steel industry due to its ability to create thin insulating layers that enhance magnetic properties while minimizing eddy current losses.

Its precise coating process makes it especially suitable for complex geometries and high-grade applications in motors and transformers. The technique supports the development of advanced insulation systems that meet the stringent performance standards required in next-generation electric motors, including those used in electric vehicles and high-efficiency industrial machinery. PVD also enables better environmental compliance, as it typically involves fewer hazardous chemicals compared to some traditional coating methods.

The method’s compatibility with automated and vacuum-based production lines has further encouraged its adoption across modern steel processing facilities. As manufacturers prioritize quality, consistency, and performance in electrical steel, Physical Vapor Deposition remains the preferred technique, supported by ongoing innovation in thin-film technologies and the rising need for durable and thermally stable coatings in power distribution and electrified transport systems.

By Coating Type Analysis

Epoxy coatings account for 53.3% of the electrical steel coatings market.

In 2024, Epoxy Coatings held a dominant market position in the By Coating Type segment of the Electrical Steel Coatings Market, with a 53.3% share. Known for their excellent dielectric properties, strong adhesion, and resistance to corrosion and moisture, epoxy coatings are widely used in applications requiring reliable electrical insulation and mechanical protection. Their high thermal stability makes them ideal for use in electrical steel components that operate under elevated temperatures, such as transformers, motors, and generators.

The dominance of epoxy coatings in the market is also attributed to their compatibility with various steel grades and ease of application through different techniques, including roll coating and spray systems. These coatings offer long-term durability and help minimize energy losses by effectively separating laminations, thereby reducing eddy currents and magnetic interference.

Moreover, epoxy coatings have gained widespread acceptance in both grain-oriented and non-grain-oriented electrical steels used in power distribution and rotating machinery. Their insulating capability not only enhances energy efficiency but also extends the service life of electrical components. As demand for energy-efficient and low-loss systems continues to grow across industrial, automotive, and power sectors, epoxy coatings remain the preferred choice, maintaining their leading position in the electrical steel coatings landscape.

By Electrical Steel Type Analysis

Grain-oriented electrical steel leads by type, contributing 58.9% market share.

In 2024, Grain-oriented held a dominant market position in the By Coating Type segment of the Electrical Steel Coatings Market, with a 58.9% share. This type of electrical steel is specially processed to align its grain structure, allowing for superior magnetic properties along the rolling direction. Coatings applied to grain-oriented electrical steel serve a critical function in providing insulation between laminations, which significantly reduces core losses and improves energy efficiency in static equipment such as transformers.

The widespread use of grain-oriented steel in power transformers, distribution transformers, and reactor cores has contributed to its dominant market share. Coated grain-oriented steel enables higher operational efficiency and reduced energy dissipation, which are key requirements in modern power grid applications. Its high permeability and low magnetostriction characteristics make it the preferred choice in high-voltage equipment.

Furthermore, the increasing global focus on minimizing transmission losses and enhancing grid stability has elevated the demand for high-performance coated grain-oriented steel. Its application is central to energy infrastructure projects, especially in regions modernizing or expanding their electricity distribution networks. With the continued transition toward more energy-efficient electrical systems, grain-oriented coated steel maintains its lead, driven by its proven reliability in mission-critical power equipment.

By Application Analysis

The transformers application segment holds a 44.2% share in the coatings market demand.

In 2024, Transformers held a dominant market position in the By Application segment of the Electrical Steel Coatings Market, with a 44.2% share. The critical role of transformers in power generation, transmission, and distribution systems has driven consistent demand for coated electrical steel, particularly grain-oriented variants. Electrical steel coatings used in transformers provide essential insulation between laminations, minimizing eddy current losses and heat generation while enhancing overall efficiency.

These coatings also improve corrosion resistance and mechanical durability, which are necessary for the long-term reliability of transformers operating under high loads and varying environmental conditions. As global energy demand continues to rise, especially in developing economies, investments in transmission infrastructure and grid expansion projects have increased. This directly boosts the need for efficient transformers equipped with high-performance coated steel.

Additionally, the transition toward smart grids and renewable energy integration has further supported the deployment of distribution and power transformers with advanced insulation solutions. The 44.2% share held by transformers underscores the importance of this segment in the broader electrical steel coatings market.

Key Market Segments

By Coating Type

- C2

- C3

- C4

- C5

- C6

- Others

By Coating Technique

- Electroless Plating

- Physical Vapor Deposition

- Chemical Vapor Deposition

By Coating Type

- Epoxy Coatings

- Polyester Coatings

- Phenolic Coatings

By Electrical Steel Type

- Grain-oriented

- Non-grain Oriented

- Non-oriented Semi-processed Electrical Steel

- Non-oriented Fully processed Electrical Steel

- Silicon Steel

By Application

- Transformers

- Motors

- Generators

- Inductors

- Others

Driving Factors

Rising Demand for Energy-Efficient Electrical Equipment

One of the main drivers of the electrical steel coatings market is the growing need for energy-efficient electrical equipment. As more countries focus on saving electricity and reducing energy loss, transformers, motors, and generators need to perform better. Coatings on electrical steel help reduce energy waste by lowering heat and magnetic losses.

This is especially important in power plants, electric vehicles, and factories where equipment runs constantly. Governments and industries are also pushing for smart grids and clean energy solutions, which need high-performance electrical components. These changes are making more companies use coated electrical steel in their products. As a result, the market for electrical steel coatings is expected to grow steadily over the coming years.

Restraining Factors

High Cost of Advanced Coating Techniques

A major challenge for the electrical steel coatings market is the high cost of advanced coating techniques. Methods like Physical Vapor Deposition (PVD) or other precision coatings offer better insulation and efficiency, but are expensive to install and operate. These costs increase the overall price of coated electrical steel, which can be a problem for manufacturers working with tight budgets.

Smaller companies or those in cost-sensitive markets may avoid using high-end coatings due to limited return on investment. Additionally, maintaining advanced coating equipment and ensuring quality control adds to the overall cost. This price barrier can slow down adoption, especially in regions with low infrastructure investment or limited demand for premium electrical equipment.

Growth Opportunity

Expanding Renewable Energy Infrastructure Drives Market Growth

The increasing global investment in renewable energy projects presents a significant opportunity for the electrical steel coatings market. As countries aim to reduce carbon emissions, there is a growing demand for efficient transformers and motors in wind and solar power systems. Electrical steel coatings enhance the performance and longevity of these components by providing superior insulation and reducing energy losses.

This trend is particularly notable in regions like Asia-Pacific, where rapid industrialization and supportive government policies are accelerating the adoption of renewable energy technologies. Consequently, the need for high-quality electrical steel coatings is expected to rise, offering substantial growth prospects for manufacturers in this sector.

Latest Trends

Shift Toward Eco-Friendly Insulation Coating Materials

A key trend in the electrical steel coatings market is the growing use of eco-friendly insulation materials. Manufacturers are moving away from traditional chemical-based coatings and exploring water-based or solvent-free alternatives that are safer for workers and the environment. This shift is driven by strict environmental rules and a global push to reduce harmful emissions during manufacturing.

These new coatings also offer improved performance in terms of thermal stability and electrical insulation. As industries and governments promote cleaner production methods, eco-friendly coatings are gaining popularity in electrical steel used for motors, transformers, and generators.

Regional Analysis

In 2024, Asia-Pacific dominated with a 47.3% share, valued at USD 143.3 million.

In 2024, Asia-Pacific held the dominant position in the global Electrical Steel Coatings Market, accounting for 47.3% of the total share and reaching a market value of USD 143.3 million. The region’s strong presence is primarily driven by the large-scale production of transformers, electric motors, and other electrical equipment in countries like China, Japan, and India.

Rapid industrialization, expanding renewable energy infrastructure, and growing investments in power transmission projects have supported the demand for coated electrical steel in the region.

North America and Europe followed, supported by technological advancements in energy systems and the increasing shift toward energy-efficient electrical infrastructure. Meanwhile, the Middle East & Africa and Latin America are witnessing gradual growth, fueled by grid modernization and electrification efforts in developing economies.

Although these regions currently represent a smaller portion of the global market, rising energy demand and infrastructure upgrades are expected to support future growth.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

AK Steel Holding Corporation continued to play a pivotal role in the North American market, leveraging its expertise in producing high-quality electrical steels. The company’s focus on developing advanced coatings that enhance the performance and efficiency of electrical components has solidified its position in the industry.

ArcelorMittal SA made notable strides by expanding its electrical steel production capacity. The inauguration of a new production unit in Mardyck, France, in 2024 tripled the company’s capacity for electrical steel production, demonstrating its commitment to meeting the growing demand for energy-efficient electrical components.

Axalta Coating Systems Ltd. showcased its innovation in the coatings segment by introducing environmentally friendly products like Voltatex® 7345 A ECO Wire Enamel. This product, recognized with the 2024 BIG Innovation Award, underscores Axalta’s commitment to sustainability and advancing electrification through efficient insulation solutions.

Top Key Players in the Market

- AK Steel Holding Corporation

- ArcelorMittal SA Baosteel

- Axalta Coatings Systems Ltd.

- Baosteel

- Chemetall GmbH

- Cogent Power Limited

- Dorf Ketal Chemicals

- JFE Steel Corporation

- Nippon Steel & Sumitomo Metal Corporation (NSSMC)

- Polaris Laser Laminations, LLC

- POSCO

- Rembrandtin Lack GmbH Nfg. KG

- Thyssenkrupp AG

Recent Developments

- In May 2025, Chemetall GmbH announced that its Langelsheim production facility in Germany now operates entirely on renewable electricity sourced from BASF Renewable Energy. This transition is expected to reduce approximately 620 tons of CO₂ emissions annually and marks a significant step towards Chemetall’s goal of utilizing 80% renewable energy across all its sites by 2025.

- In May 2024, Dorf Ketal Chemicals completed the acquisition of Impact Fluid Solutions, a Texas-based provider of downhole fluid additives utilized in various industrial drilling applications. This acquisition aims to enhance Dorf Ketal’s portfolio of solutions for the oil and gas production sector.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 303.1 Million |

| Forecast Revenue (2034) | USD 508.0 Million |

| CAGR (2025-2034) | 5.3% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Coating Type (C2, C3, C4, C5, C6, Others),By Coating Technique (Electroless Plating, Physical Vapor Deposition, Chemical Vapor Deposition), By Coating Type (Epoxy Coatings, Polyester Coatings, Phenolic Coatings), By Electrical Steel Type (Grain-oriented, Non-grain Oriented (Non-oriented Semi-processed Electrical Steel, Non-oriented Fully processed Electrical Steel), Silicon Steel), By Application (Transformers, Motors, Generators, Inductors, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | AK Steel Holding Corporation, ArcelorMittal SA Baosteel, Axalta Coatings Systems Ltd., Baosteel, Chemetall GmbH, Cogent Power Limited, Dorf Ketal Chemicals, JFE Steel Corporation, Nippon Steel & Sumitomo Metal Corporation (NSSMC), Polaris Laser Laminations, LLC, POSCO, Rembrandtin Lack GmbH Nfg. KG, Thyssenkrupp AG |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |