Quick Navigation

Report Overview

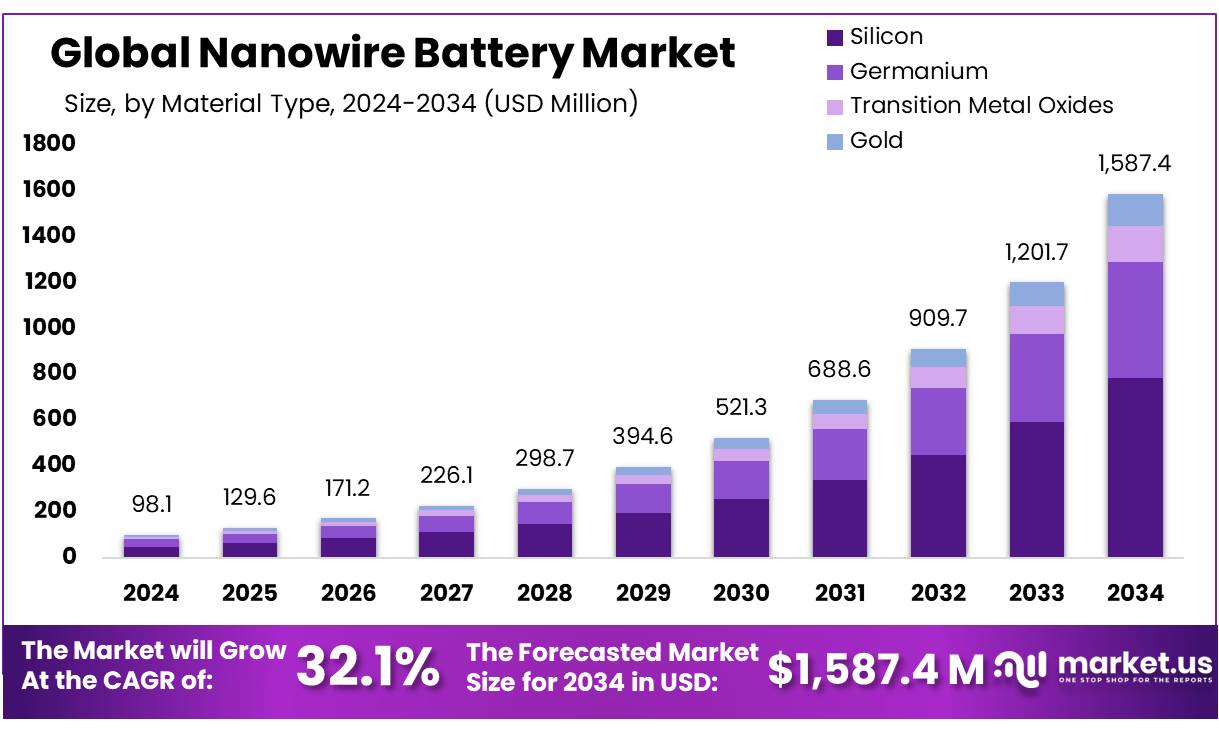

The Global Nanowire Battery Market size is expected to be worth around USD 1587.4 Million by 2034, from USD 98.1 Million in 2024, growing at a CAGR of 32.1% during the forecast period from 2025 to 2034.

Nanowire batteries represent a significant advancement in energy storage technology, characterized by their utilization of nanostructured materials such as silicon, germanium, and transition metal oxides. These materials offer enhanced surface area and superior electrochemical properties, leading to higher energy densities, faster charging capabilities, and extended cycle life compared to traditional lithium-ion batteries.

The nanowire batteries is rapidly evolving, driven by the growing demand for efficient energy storage solutions in electric vehicles (EVs), consumer electronics, and renewable energy systems. In the United States, the Department of Energy (DOE) has initiated substantial funding programs to bolster domestic battery production. Notably, over $3 billion has been allocated to support 25 projects across 14 states, aiming to enhance the manufacturing of advanced batteries and battery materials.

Silicon nanowires are at the forefront of this technological evolution, offering a theoretical charge retention capacity of 4,200 mAh/g, which is ten times greater than traditional graphite anodes. This substantial improvement in energy density makes silicon nanowire batteries highly attractive for applications requiring long-lasting and fast-charging power sources.

Government initiatives play a crucial role in fostering the development and adoption of nanowire battery technologies. In the United States, the Department of Energy allocated USD 3.1 billion in 2022 to enhance domestic battery manufacturing capabilities.

Similarly, China’s aggressive push towards electrification has resulted in the country accounting for 95% of global electric bus deployments and achieving 6.1 million EV sales in 2022. These governmental efforts underscore the strategic importance of advanced battery technologies in achieving energy security and environmental sustainability goals.

The National Nanotechnology Initiative (NNI), a U.S. government program, coordinates nanoscale research and development across federal agencies. As of fiscal year 2025, the NNI has invested approximately USD 45 billion in nanotechnology research, with a focus on areas including batteries and energy storage. This concerted effort aims to maintain the United States’ leadership in nanotechnology and facilitate the commercialization of innovative applications such as nanowire batteries.

Additionally, the DOE’s Battery Manufacturing and Recycling Grants Program, funded by the Bipartisan Infrastructure Law, allocates USD 3 billion to support the construction and retrofitting of facilities for battery component manufacturing and recycling. These initiatives aim to strengthen the U.S. battery supply chain and reduce dependence on foreign sources.

Key Takeaways

- Nanowire Battery Market size is expected to be worth around USD 1587.4 Million by 2034, from USD 98.1 Million in 2024, growing at a CAGR of 32.1%.

- Silicon held a dominant market position, capturing more than a 49.3% share in the global nanowire battery market.

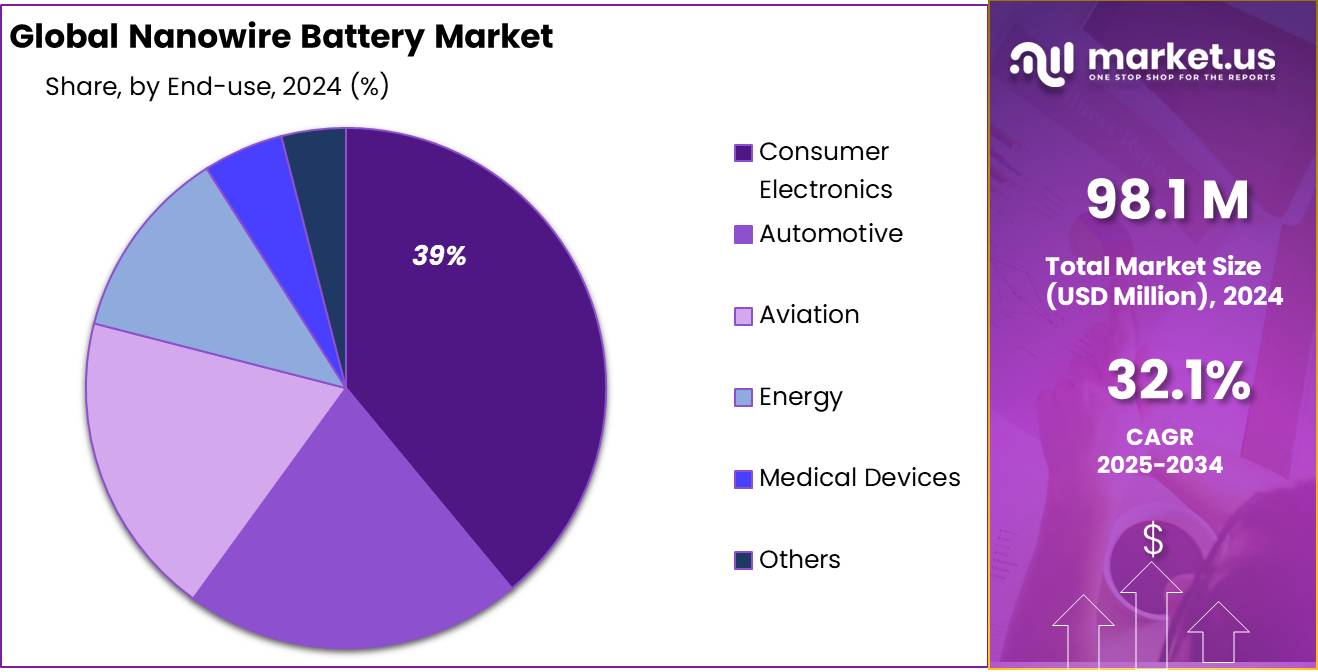

- Consumer Electronics held a dominant market position, capturing more than a 39.9% share of the nanowire battery market.

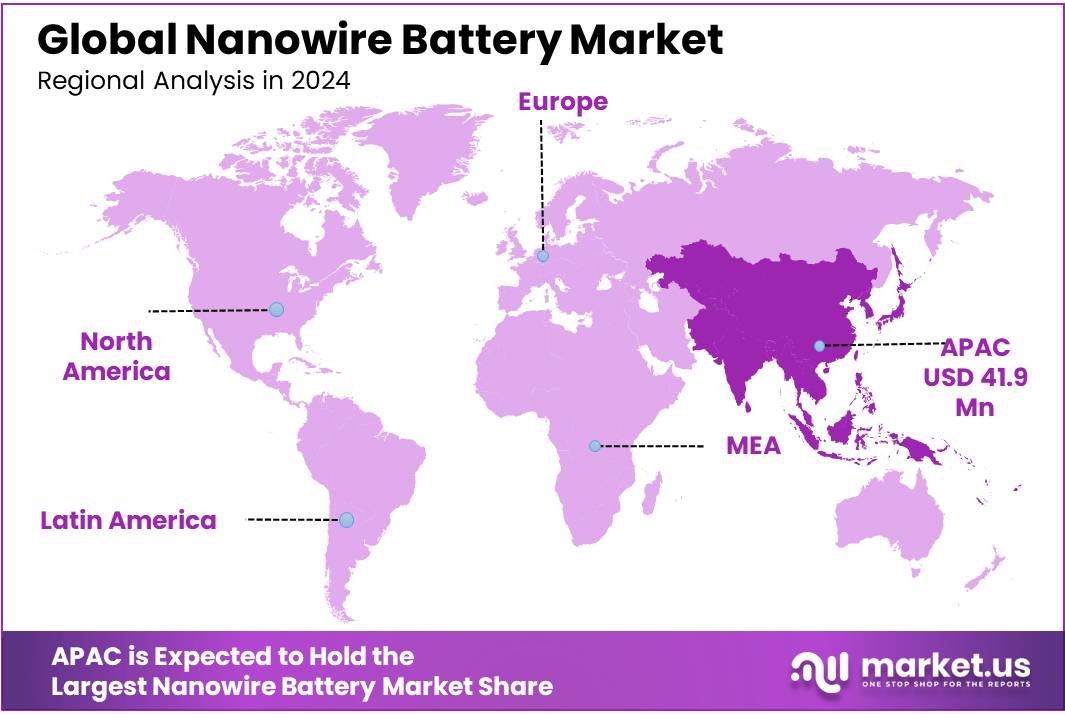

- Asia-Pacific (APAC) region secured a dominant position in the global nanowire battery market, capturing approximately 42.8% of the total market share, equating to a valuation of USD 41.9 million.

By Material Type

Silicon dominates Nanowire Battery Market with 49.3% share in 2024, driven by its high energy capacity and proven compatibility with lithium-ion systems.

In 2024, Silicon held a dominant market position, capturing more than a 49.3% share in the global nanowire battery market. This strong position is mainly due to silicon’s ability to store about ten times more lithium ions than traditional graphite-based anodes. As a material, silicon has emerged as a preferred choice for nanowire applications because of its abundance, light weight, and exceptional theoretical capacity nearing 4,200 mAh/g. Moreover, recent improvements in silicon nanowire engineering have helped overcome key challenges such as volume expansion during charging cycles, which previously led to electrode degradation.

By End-use

Consumer Electronics leads Nanowire Battery Market with 39.9% share in 2024, fueled by rising demand for longer battery life in portable devices.

In 2024, Consumer Electronics held a dominant market position, capturing more than a 39.9% share of the nanowire battery market. This leadership comes from the growing need for compact, lightweight, and high-capacity batteries in everyday gadgets such as smartphones, tablets, smartwatches, and wireless earphones. Consumers increasingly expect devices to charge faster and last longer, which has made nanowire batteries — especially those using silicon — a practical solution for tech manufacturers seeking performance upgrades.

Key Market Segments

By Material Type

- Silicon

- Germanium

- Transition Metal Oxides

- Gold

By End-use

- Consumer Electronics

- Automotive

- Aviation

- Energy

- Medical Devices

- Others

Drivers

Government Support and EV Demand Drive Nanowire Battery Market Growth

One major factor fueling the growth of the nanowire battery market is the increasing demand for high-capacity, fast-charging batteries in electric vehicles (EVs) and portable electronics. Nanowire batteries offer superior energy density and faster charging capabilities, addressing the performance limitations of traditional lithium-ion batteries. As the world shifts toward electric mobility and renewable energy integration, the need for efficient, durable, and scalable battery solutions is growing.

In 2023, the silicon segment dominated the nanowire battery market with a 48.7% share and is expected to grow the fastest from 2024 to 2032. This increase is attributed to silicon’s high energy density per unit weight, ready availability, and compatibility with current lithium-ion architectures. High surface area and charge retention, along with volume expansion during charging, provide longer battery life and better efficiency in devices like EVs and portable devices.

Government initiatives are also playing a significant role in promoting the adoption of nanowire batteries. For instance, the U.S. Department of Energy has been investing in advanced battery research to support the development of next-generation energy storage solutions. These efforts aim to enhance the performance and reduce the cost of batteries, making them more accessible for widespread use in various applications.

As a result of these factors, the nanowire battery market is projected to experience significant growth in the coming years. With ongoing research and development, coupled with supportive government policies and increasing demand from the EV and electronics sectors, nanowire batteries are poised to become a key component in the future of energy storage.

Restraints

High Production Costs and Manufacturing Complexity Hinder Nanowire Battery Market Growth

Nanowire batteries, especially those utilizing silicon nanowires, promise significant advancements in energy storage due to their high energy density and rapid charging capabilities. However, the intricate and specialized manufacturing processes required for these batteries present substantial challenges. The production involves precise control over nanowire synthesis, alignment, and integration into battery architectures, necessitating advanced equipment and stringent quality control measures. These complexities lead to increased labor and equipment costs, making large-scale production economically challenging.

Furthermore, the materials used in nanowire batteries, such as high-purity silicon, contribute to the elevated production costs. The need for specialized facilities and the current lack of established large-scale manufacturing infrastructure further exacerbate these cost issues. As a result, despite the technological advantages, the commercialization and widespread adoption of nanowire batteries are hindered by these economic barriers.

In contrast, traditional lithium-ion batteries benefit from mature manufacturing processes and established supply chains, allowing for more cost-effective production. This economic disparity poses a significant obstacle for nanowire batteries to compete in the market, particularly in cost-sensitive applications.

Addressing these challenges requires concerted efforts in research and development to simplify manufacturing processes and reduce material costs. Government initiatives and industry collaborations could play a pivotal role in overcoming these barriers, facilitating the transition of nanowire batteries from laboratory research to commercial viability.

Opportunity

Government-Backed Giga-Scale Battery Manufacturing: A Catalyst for Nanowire Battery Market Growth

India’s ambitious push towards self-reliance in advanced battery technologies presents a significant opportunity for the nanowire battery market. The government’s focus on establishing giga-scale battery manufacturing facilities aims to meet the projected demand of approximately 260 GWh by 2030, driven by the accelerated adoption of electric vehicles (EVs) and the integration of renewable energy sources into the power grid.

To achieve this, the government has introduced the Production Linked Incentive (PLI) scheme, allocating ₹18,100 crore (approximately USD 2.4 billion) to support the development of Advanced Chemistry Cell (ACC) battery manufacturing in India. This initiative encourages both domestic and international investors to establish manufacturing units, fostering innovation and reducing reliance on imports.

The PLI scheme is technology-agnostic, allowing manufacturers to choose suitable technologies, including nanowire-based batteries, provided they meet performance criteria. This flexibility opens avenues for incorporating nanowire technology into large-scale production, leveraging its advantages such as higher energy density and faster charging capabilities.

Furthermore, the establishment of giga-scale manufacturing plants is expected to create economies of scale, reducing production costs and making advanced battery technologies more accessible. This development aligns with the government’s broader objectives of promoting sustainable energy solutions and positioning India as a global hub for battery manufacturing.

Trends

Integration of Nanowire Batteries in Renewable Energy Storage Systems

The global transition towards renewable energy sources has intensified the need for efficient and reliable energy storage solutions. Nanowire batteries, with their high energy density and rapid charge-discharge capabilities, are emerging as a promising technology to address this demand.

Governments worldwide are recognizing the potential of nanowire batteries in enhancing energy storage infrastructure. For instance, the United States Department of Energy (DOE) has allocated substantial funding towards battery research and development, aiming to support technologies that can facilitate the integration of renewable energy into the grid. Similarly, the European Union’s strategic initiatives focus on advancing battery technologies to meet sustainability goals.

In the Asia-Pacific region, countries like China and India are investing heavily in renewable energy projects. China, for example, accounted for a significant share of global electric bus sales and is rapidly expanding its renewable energy capacity. These developments underscore the growing need for efficient energy storage solutions, positioning nanowire batteries as a key component in achieving energy security and environmental objectives.

The integration of nanowire batteries into renewable energy systems offers the potential to enhance grid stability, reduce reliance on fossil fuels, and support the global shift towards sustainable energy. As technological advancements continue and production scales up, nanowire batteries are poised to play a crucial role in the future of energy storage.

Regional Analysis

In 2024, the Asia-Pacific (APAC) region secured a dominant position in the global nanowire battery market, capturing approximately 42.8% of the total market share, equating to a valuation of USD 41.9 million. This leadership is primarily attributed to the region’s rapid industrialization, substantial investments in renewable energy infrastructure, and a burgeoning consumer electronics industry. Countries such as China, Japan, and South Korea are at the forefront, driving innovation and adoption of nanowire battery technologies.

China, in particular, plays a pivotal role, accounting for a significant portion of the regional market. The nation’s aggressive push towards electric vehicle (EV) adoption and its status as a global manufacturing hub for consumer electronics have created a robust demand for advanced battery solutions. In 2022, China was responsible for approximately 95% of global electric bus sales and recorded 6.1 million EV sales, underscoring its commitment to sustainable transportation and the consequent need for high-performance batteries .

Japan and South Korea are also significant contributors, with companies like Panasonic and Samsung SDI investing heavily in research and development of nanowire battery technologies. These nations benefit from strong governmental support, fostering an environment conducive to innovation and commercialization of advanced energy storage solutions.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Nexeon, a UK-based company, specializes in silicon anode materials for lithium-ion batteries. Their NSP2™ technology replaces traditional graphite anodes, offering up to a 50% increase in energy density. This advancement enables smaller, lighter batteries without compromising performance. Nexeon’s materials are designed for mass production using cost-effective processes, aiming to reduce the carbon footprint of battery manufacturing.

Amprius Technologies, headquartered in Fremont, California, leads in silicon anode lithium-ion battery innovation. Their SiMaxx™ batteries deliver up to 450 Wh/kg and 1,150 Wh/L, with third-party validations reaching 500 Wh/kg and 1,300 Wh/L. These high-energy-density batteries are utilized in various sectors, including unmanned and manned aviation, electric vehicles, and defense applications.

LG Chem, based in South Korea, is a global leader in battery materials, including cathode and anode components for lithium-ion batteries. The company reported sales of KRW 48.92 trillion in 2024 and aims to achieve over KRW 60 trillion by 2030. LG Chem’s advanced materials are integral to electric vehicles and energy storage systems, driving innovation in battery technology.

Top Key Players in the Market

- Nexeon

- Amprius

- OneD Material

- LG Chem

- ACS Materials

- Novarials Corporation

Recent Developments

In 2024, LG Chem made significant progress in the nanowire battery sector by unveiling a silicon-based nanowire battery prototype that offers a 30% increase in energy density compared to conventional lithium-ion batteries.

In 2024, Nexeon, a UK-based developer of silicon anode materials for lithium-ion batteries, achieved a significant milestone by commencing construction of its first commercial-scale production facility in Gunsan, South Korea.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 98.1 Mn |

| Forecast Revenue (2034) | USD 1587.4 Mn |

| CAGR (2025-2034) | 32.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material Type (Silicon, Germanium, Transition Metal Oxides, Gold), By End-use (Consumer Electronics, Automotive, Aviation, Energy, Medical Devices, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Nexeon, Amprius, OneD Material, LG Chem, ACS Materials, Novarials Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |