Quick Navigation

Report Overview

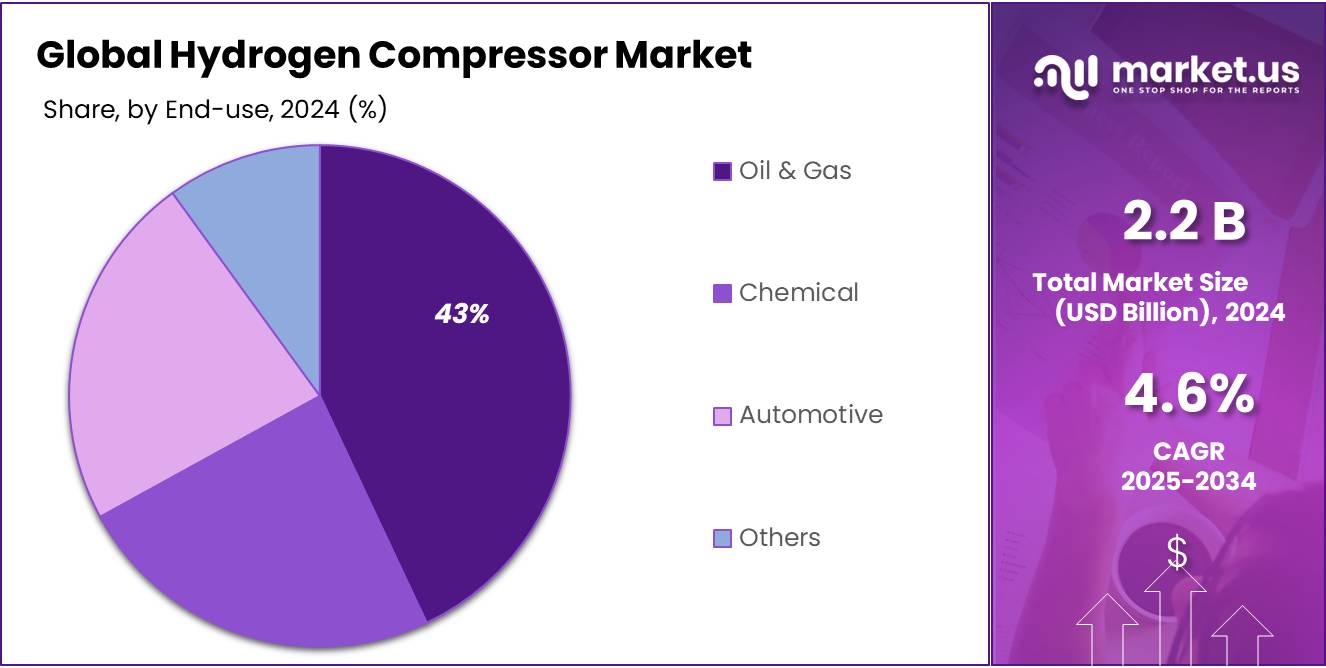

The Global Hydrogen Compressor Market size is expected to be worth around USD 3.4 Bn by 2034, from USD 2.2 Bn in 2024, growing at a CAGR of 4.6% during the forecast period from 2025 to 2034.

The hydrogen compressor industry is a critical component of the hydrogen energy sector, facilitating the efficient storage and transport of hydrogen gas. These compressors are designed to increase the pressure of hydrogen to desired levels, making it suitable for various applications including fuel cells, industrial processes, and energy storage.

Several key factors are propelling the growth of the hydrogen compressor market. Firstly, the global push towards decarbonization has led to an increased focus on clean energy technologies, with hydrogen playing a pivotal role as a green energy carrier. Government initiatives such as the European Union’s Hydrogen Strategy, which aims to achieve 40 gigawatts of renewable hydrogen electrolyzers by 2030, underscore the commitment to integrating hydrogen into the energy system.

Secondly, the automotive industry’s shift towards hydrogen fuel cell vehicles (FCVs) significantly contributes to the demand for hydrogen compressors. Governments are supporting this transition through subsidies and tax incentives. For instance, Germany has allocated over EUR 8 billion towards hydrogen projects, including the development of refueling stations that rely on hydrogen compressors.

In the face of pandemic-related challenges, governments around the world have remained steadfast in advancing clean energy efforts, particularly through investments in hydrogen infrastructure. Aiming for net zero emissions, many countries are accelerating hydrogen development. According Hydrogen Council highlights that 131 new hydrogen projects have been launched globally, bringing the total to 359. These initiatives represent a projected investment of nearly USD 500 billion across the full hydrogen value chain by 2030. This surge in activity is expected to play a key role in propelling the growth of the hydrogen compressor market.

Key Takeaways

- The Hydrogen Compressor market is projected to grow from USD 2.2 billion in 2024 to approximately USD 3.4 billion by 2034, achieving a (CAGR) of 4.6%.

- Mechanical Compressors are predominant in the Hydrogen Compressor market, holding an impressive 87.2% share.

- Oil-based compressors lead in the market, accounting for 63.4% of the market share.

- Compressors with a discharge capacity of up to 10,000 psig are leading the market, representing a 46.5% share in 2024.

- The Oil & Gas sector is a significant user of hydrogen compressors, comprising 43.5% of the market.

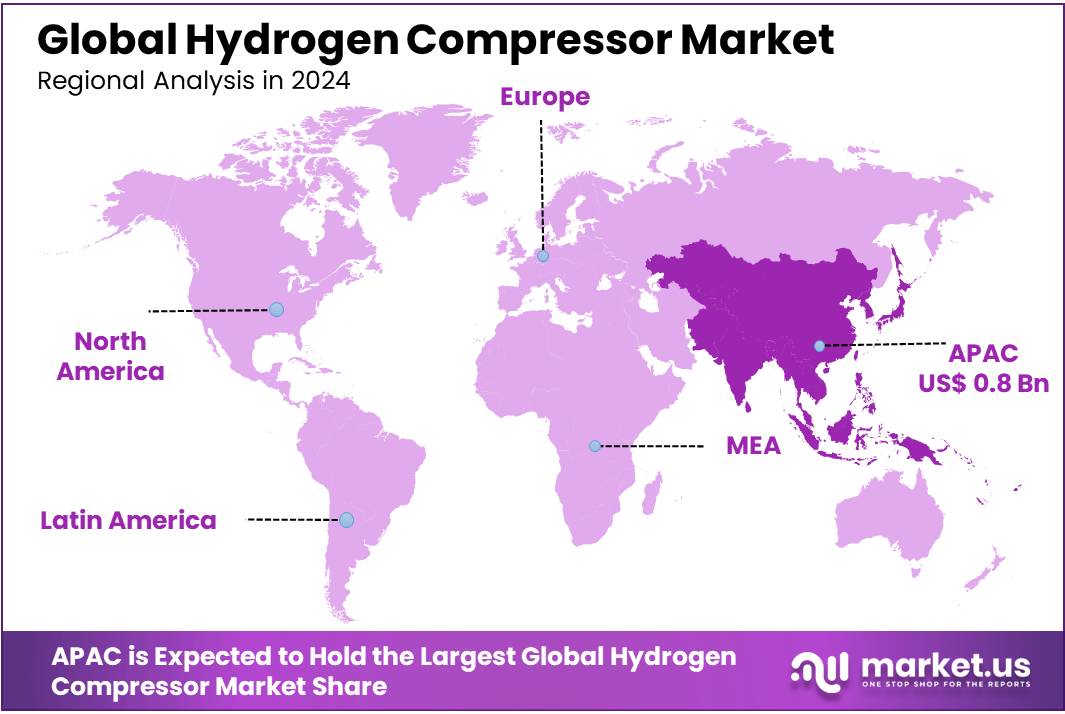

- The Asia-Pacific (APAC) region is becoming a significant player, holding a 36.5% market share, which equates to a market valuation of around USD 0.8 billion.

Analysts’ Viewpoint

From an investment perspective, the Hydrogen Compressor market presents significant opportunities as industries lean towards cleaner energy solutions. The demand for hydrogen compressors is set to increase, particularly in sectors like manufacturing, oil & gas, and renewable energy, where hydrogen plays a pivotal role in clean energy transitions.

The regulatory landscape for hydrogen compressors is tightening, with governments worldwide setting stringent emissions standards and supporting hydrogen technologies through subsidies and incentives. For instance, the European Union has earmarked substantial funds to support hydrogen projects, which could ease financial burdens associated with adopting hydrogen technologies. Such initiatives are expected to drive the adoption of hydrogen compressors further, especially in regions committed to cutting emissions.

Impact of US Tariffs

The recent US tariff actions implemented in April 2025 have significantly impacted the hydrogen compressor industry, particularly concerning raw material costs and supply chain continuity. According to industry reports, tariffs have affected imports of critical components used in compressor systems, such as high-strength alloys and specialized seals. These tariffs, some exceeding 100 percent, have substantially increased the cost base for US manufacturers.

The companies are accelerating shifts toward domestic and alternative regional suppliers, aiming to enhance long-term supply security. Retaliatory trade measures by partner countries have restricted access to certain specialty inputs, prompting firms to explore new trade partnerships, particularly in Southeast Asia and Latin America.

By Technology Type

Mechanical Compressors Dominate with 87.2% Share Due to High Efficiency and Reliability

In 2024, Mechanical Compressors held a dominant market position in the Hydrogen Compressor market, capturing more than an 87.2% share. This significant market share is attributed to their reliability and efficiency in various industrial applications. Mechanical compressors are favored in sectors that demand high-pressure hydrogen for processes such as hydrogen refueling stations and industrial gas production. Their robust design and advanced technology allow for sustained performance under high-demand conditions, making them indispensable in settings that require continuous, high-volume hydrogen compression. This dominance is expected to continue as industries increasingly prioritize energy efficiency and system reliability in their operations.

By Lubrication Type

Oil-Based Compressors Lead with 63.4% Share for Enhanced Performance and Durability

In 2024, oil-based compressors maintained a dominant position in the Hydrogen Compressor market, securing a significant 63.4% share. This preference stems from their enhanced performance capabilities and the durability they offer in high-pressure environments. Oil-based compressors are particularly valued for their ability to provide a stable and consistent compression service, which is crucial in applications involving the production and transportation of hydrogen. The lubrication provided by oil minimizes wear and tear on compressor components, thus extending their operational lifespan and reducing maintenance costs. Their continued dominance is driven by these practical benefits, which are essential in industrial settings where reliability and efficiency are paramount.

By Discharge Pressure

Compressors Up to 10,000 psig Dominate with 46.5% Share for Versatile High-Pressure Applications

In 2024, compressors capable of discharging up to 10,000 psig held a dominant market position, capturing more than a 46.5% share of the Hydrogen Compressor market. This segment’s prominence is largely due to the versatility these compressors offer in handling high-pressure requirements across various industries, including energy, manufacturing, and chemical processing. Their ability to operate efficiently at such high pressures makes them ideal for applications that require robust, reliable hydrogen compression solutions. This category’s significant market share reflects its critical role in meeting the demanding specifications for hydrogen infrastructure projects and high-pressure hydrogen storage and distribution systems.

By End use

Oil & Gas Sector Leads with 43.5% Share, Driven by High Demand for Hydrogen Compression

In 2024, the Oil & Gas sector held a dominant market position in the Hydrogen Compressor market, securing a 43.5% share. This leadership is primarily due to the critical role of hydrogen compressors in oil and gas operations, where they are essential for hydrogen processing and refinery activities. The high demand for hydrogen in processes such as hydrocracking and hydrogenation underlines the importance of reliable and efficient hydrogen compressors. The sector’s substantial share underscores its reliance on advanced compression technologies to enhance operational efficiency and meet stringent environmental regulations regarding emissions.

Key Market Segments

By Technology Type

- Mechanical Compressors

- Non-Mechanical Compressors

By Lubrication Type

- Oil-based

- Oil-free

By Discharge Pressure

- Upto 10,000 psig

- 10,000 psig to 15,000 psig

- Above 15,000 psig

By End use

- Oil & Gas

- Chemical

- Automotive

- Others

Drivers

Accelerated Transition to Clean Energy Spurs Demand for Hydrogen Compressors

One major driving factor for the hydrogen compressor market is the global shift towards clean energy sources. Governments worldwide are implementing stringent environmental regulations to reduce carbon emissions, which has significantly boosted the demand for renewable energy sources, including hydrogen. This transition is largely driven by the need to address climate change concerns and reduce dependency on fossil fuels.

For instance, the European Union has committed to reducing greenhouse gas emissions by at least 55% by 2030, compared to 1990 levels, under the “Fit for 55” legislative package. This initiative directly impacts the hydrogen market as the EU aims to expand hydrogen production primarily from renewable sources. Hydrogen compressors are essential in this context because they enable the effective storage and transportation of hydrogen, making them crucial for the infrastructure required for a hydrogen economy.

Furthermore, the U.S. Department of Energy (DOE) has launched several initiatives to support hydrogen technologies. In 2024, the DOE announced funding of $100 million to support research and development in hydrogen energy systems, including advancements in hydrogen compressors. These compressors are vital for increasing the efficiency and viability of hydrogen as a clean energy carrier.

Restraints

High Initial Investment Costs Limit Hydrogen Compressor Adoption

A significant restraining factor for the hydrogen compressor market is the high initial investment required for deployment. These compressors are technologically advanced and crucial for hydrogen storage and transportation, but their high cost poses a substantial barrier, especially for emerging markets and small-scale operators.

The capital-intensive nature of hydrogen compressors can deter their adoption despite the potential long-term benefits in reducing operational costs and carbon footprints. For instance, the setup cost for hydrogen compression systems for fuel stations can run into millions of dollars, depending on the capacity and technology used. This financial hurdle is particularly challenging for small enterprises or regions with limited access to funding.

Government initiatives do exist to help mitigate these costs. For example, the European Union has allocated funds through the Clean Hydrogen Partnership, aiming to co-finance projects that reduce the cost of hydrogen technologies, including compressors. Similarly, in the United States, the Infrastructure Investment and Jobs Act provides funding for clean hydrogen initiatives, which can include compressor technology.

Opportunity

Expanding Hydrogen Economy Offers Growth Opportunities for Compressor Manufacturers

A major growth opportunity for the hydrogen compressor market is the expanding global hydrogen economy, which is set to transform energy systems worldwide. As countries and industries commit to decarbonization targets, the demand for hydrogen as a clean energy source is projected to surge, thereby driving the need for reliable and efficient hydrogen compression solutions.

The International Energy Agency (IEA) highlights that the global demand for hydrogen, which stood at around 70 million tons in 2020, is expected to increase significantly by 2030. Hydrogen compressors are crucial in this growth, as they are needed to pressurize hydrogen for storage and transport, making them essential for the scaling of hydrogen infrastructure.

Government initiatives across the globe are also accelerating this growth. For instance, the European Green Deal includes the aim to install at least 40 gigawatts of renewable hydrogen electrolyzers in the EU by 2030 and an additional 40 gigawatts in neighboring countries. This massive increase in hydrogen production capacity will require extensive and efficient hydrogen compression systems.

Furthermore, in Asia, Japan’s Green Growth Strategy under its broader 2050 Carbon Neutral goal, plans to increase the annual hydrogen demand from 2 million tons in 2030 to about 20 million tons by 2050. The strategy includes substantial investments in hydrogen technology and infrastructure, emphasizing the need for high-performance hydrogen compressors.

Trends

Integration of IoT and AI in Hydrogen Compressors Marks a Trending Shift

A significant trend emerging in the hydrogen compressor market is the integration of Internet of Things (IoT) and Artificial Intelligence (AI) technologies. This advancement is transforming how hydrogen compressors are monitored, maintained, and operated, leading to increased efficiency, predictive maintenance, and enhanced safety measures.

The adoption of IoT devices allows for real-time monitoring of compressor conditions, such as temperature, pressure, and flow rates. This data can be analyzed using AI algorithms to predict potential failures before they occur, thus preventing downtime and reducing maintenance costs. For example, a leading compressor manufacturer reported a 30% reduction in maintenance costs after implementing IoT-based predictive maintenance systems.

Governments are also supporting the digital transformation of industrial equipment through various initiatives. The U.S. Department of Energy, for instance, has funded projects that explore the use of advanced digital tools in energy systems, including hydrogen compressors. These projects aim to improve the operational efficiency and resilience of hydrogen infrastructure.

Moreover, the push towards smart factories and Industry 4.0 technologies is encouraging the use of smart compressors. In Europe, the Horizon 2020 program has invested in research and development projects that integrate digital technologies in energy systems, recognizing the potential of IoT and AI to revolutionize the hydrogen economy.

Geopolitical Impact Analysis

The hydrogen compressor sector in 2025 is influenced by a dynamic macroeconomic and geopolitical landscape. Ongoing geopolitical tensions, particularly in Eastern Europe and the Middle East, continue to disrupt global trade routes and logistics networks, affecting the availability and movement of essential components for hydrogen compression systems. Commodity price volatility, especially for key materials like steel and rare earth metals, remains high due to climatic fluctuations and export restrictions from major producers.

These challenges are prompting strategic reassessments across the industry. Governments and private entities are increasingly investing in localized and alternative sourcing solutions to mitigate risks associated with global supply chain disruptions. Stricter international standards on energy infrastructure and environmental impact are driving innovation in compressor design and manufacturing processes.

The adoption of advanced technologies, such as digital monitoring and predictive maintenance, is also rising, aiding operators in managing risk and improving operational efficiency. Despite the uncertainty, the sector is demonstrating operational adaptability through diversification, enhanced traceability, and local capacity building.

Regional Analysis

Hydrogen Compressor Market Flourishes in APAC with a 36.5% Share

The Asia-Pacific (APAC) region is emerging as a powerhouse in the hydrogen compressor market, capturing a notable 36.5% market share, which translates to a market value of approximately USD 0.8 billion. This dominance is primarily driven by several factors including the region’s robust industrial growth, aggressive clean energy targets, and significant governmental backing.

Similarly, Japan’s Basic Hydrogen Strategy outlines extensive hydrogen infrastructure development, aiming to become a hydrogen-led society by 2050. This strategy supports the establishment of a complete domestic supply chain for hydrogen, which naturally boosts the demand for hydrogen compressors in the country.

South Korea isn’t far behind, with its Hydrogen Economy Roadmap targeting the production of over 6.2 million fuel cell vehicles and the establishment of 1,200 refueling stations by 2040. The roadmap underscores the need for reliable hydrogen compression solutions to manage the anticipated increase in hydrogen production and utilization effectively.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Air Products and Chemicals, Inc. stands as a leader in the hydrogen compressor market, renowned for its innovative solutions in gas and chemical manufacturing. The company specializes in providing a range of hydrogen compressors that cater to various industries including refining, chemical, and general industrial applications. With a strong focus on sustainable technology solutions, Air Products continues to expand its influence by engaging in key international projects that aim to enhance the hydrogen infrastructure globally.

Ariel Corporation excels in the manufacture of gas compressors, including those used for hydrogen compression. As the world’s largest manufacturer of reciprocating gas compressors, Ariel’s products are pivotal in applications ranging from gas processing and petrochemicals to general industry operations. The company’s commitment to reliability and innovation allows it to support the growing demand for efficient hydrogen energy solutions.

Atlas Copco Group, a global industrial group, provides highly efficient and reliable hydrogen compressors, essential for various sectors such as renewable energy, manufacturing, and utilities. Their extensive portfolio includes advanced technology that ensures performance and sustainability. Atlas Copco’s ongoing commitment to innovation is evident in their continuous development of energy-efficient systems, supporting the transition to greener energy solutions.

Top Key Players in the Market

- Air Products and Chemicals, Inc.

- Ariel Corporation

- Atlas Copco Group

- Burckhardt Compression Holding AG

- Chart Industries, Inc. (Howden Group)

- Corken Inc.

- Fluitron Inc.

- Haug Kompressoren AG

- Hitachi Ltd.

- Hydro-Pac Inc.

- IDEX CORPORATION

- Indian Compressors Ltd

- Ingersoll Rand Inc.

- KOBE STEEL, LTD.

- Linde plc

- Mitsubishi Heavy Industries Ltd.

- NEL ASA

- Siemens Energy

- Sundyne Corp

Recent Developments

In 2024, Air Products and Chemicals, Inc. continued to strengthen its position in the hydrogen compressor sector, reporting annual sales of $12.1 billion across its global operations in approximately 50 countries . The company is actively involved in developing and operating some of the world’s largest clean hydrogen projects, which are essential for the transition to low- and zero-carbon energy in industrial and transportation sectors.

In 2024, Ariel Corporation, a prominent U.S.-based manufacturer of reciprocating gas compressors, achieved a significant milestone by delivering its 70,000th compressor since its inception in 1966. This landmark unit, the KBH hydrogen compressor, is tailored for hydrogen mobility applications and is capable of compressing hydrogen gas to pressures up to 7,250 psig (500 barg), handling over 250 kg/hr, making it suitable for trailer filling and hydrogen refueling stations.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 2.2 Bn |

| Forecast Revenue (2034) | USD 3.4 Bn |

| CAGR (2025-2034) | 4.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Technology Type (Mechanical Compressors, Non-Mechanical Compressors), By Lubrication Type (Oil-based, Oil-free), By Discharge Pressure (Upto 10,000 psig, 10,000 psig to 15,000 psig, Above 15,000 psig), By End use (Oil and Gas, Chemical, Automotive, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Air Products and Chemicals, Inc., Ariel Corporation, Atlas Copco Group, Burckhardt Compression Holding AG, Chart Industries, Inc. (Howden Group), Corken Inc., Fluitron Inc., Haug Kompressoren AG, Hitachi Ltd., Hydro-Pac Inc., IDEX CORPORATION, Indian Compressors Ltd, Ingersoll Rand Inc., KOBE STEEL, LTD., Linde plc, Mitsubishi Heavy Industries Ltd., NEL ASA, Siemens Energy, Sundyne Corp |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |