Quick Navigation

Report Overview

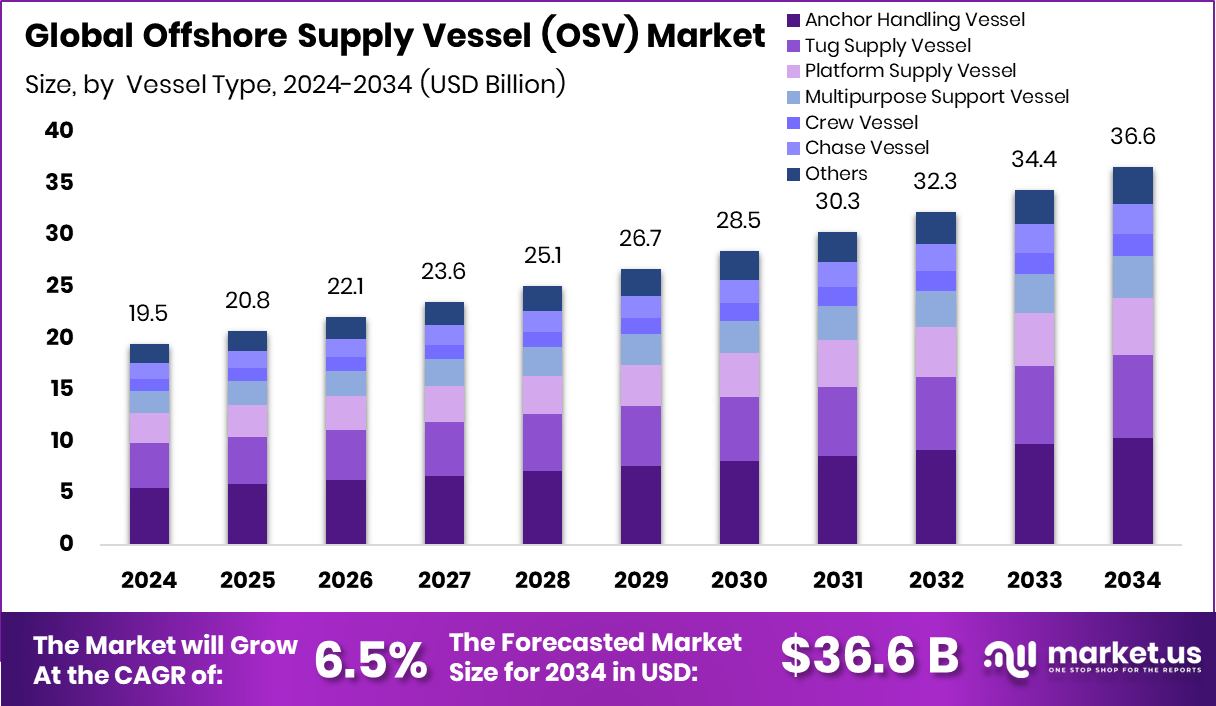

Global Offshore Supply Vessel (OSV) Market is expected to be worth around USD 36.6 billion by 2034, up from USD 19.5 billion in 2024, and grow at a CAGR of 6.5% from 2025 to 2034. Strong offshore drilling in Europe pushed OSV demand to 48.4% market dominance.

An Offshore Supply Vessel (OSV) is a type of ship designed to transport goods, supplies, equipment, and personnel to and from offshore oil and gas platforms. These vessels are built to handle heavy cargo, provide stability in rough seas, and often feature advanced navigation and dynamic positioning systems. OSVs play a crucial role in maintaining offshore operations by ensuring the timely delivery of tools, pipes, drilling fluids, fuel, and other critical items needed to keep offshore rigs functioning.

The Offshore Supply Vessel market refers to the global industry involved in designing, building, operating, and maintaining vessels that serve offshore oil and gas installations. It includes various types of OSVs like platform supply vessels (PSVs), anchor handling tug supply vessels (AHTS), and multi-purpose supply vessels.

This market supports energy production activities by ensuring offshore rigs have continuous logistical support. Demand for OSVs fluctuates based on offshore exploration projects, oil prices, and global energy consumption trends.

One of the biggest drivers for the OSV market is the steady growth in offshore oil and gas exploration activities. With maturing onshore oil fields and increasing demand for energy, companies are expanding into deepwater and ultra-deepwater zones. This growing reliance on offshore production creates a strong need for reliable logistics, directly fueling the demand for OSVs.

Many offshore vessels currently in service are over 20 years old, which increases maintenance costs and lowers efficiency. This aging fleet creates a demand for newer, technologically advanced vessels that can offer fuel efficiency, improved safety, and better performance. As companies aim to cut emissions and operating costs, replacing older vessels becomes a priority.

Key Takeaways

- Global Offshore Supply Vessel (OSV) Market is expected to be worth around USD 36.6 billion by 2034, up from USD 19.5 billion in 2024, and grow at a CAGR of 6.5% from 2025 to 2034.

- Anchor Handling Vessels held 28.4% market share due to their critical role in rig positioning.

- Shallow water operations accounted for 44.3% share due to cost-effective offshore exploration and development.

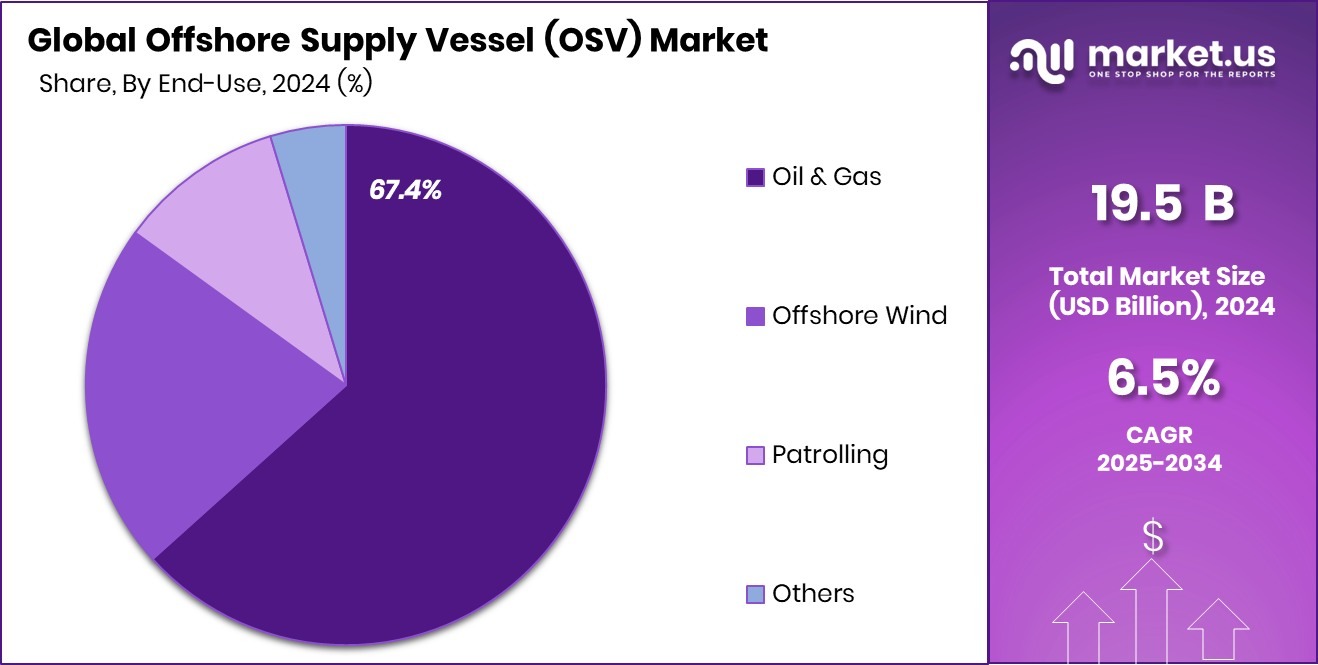

- Oil and gas industry dominated with a 67.4% share due to consistent offshore exploration and production activities.

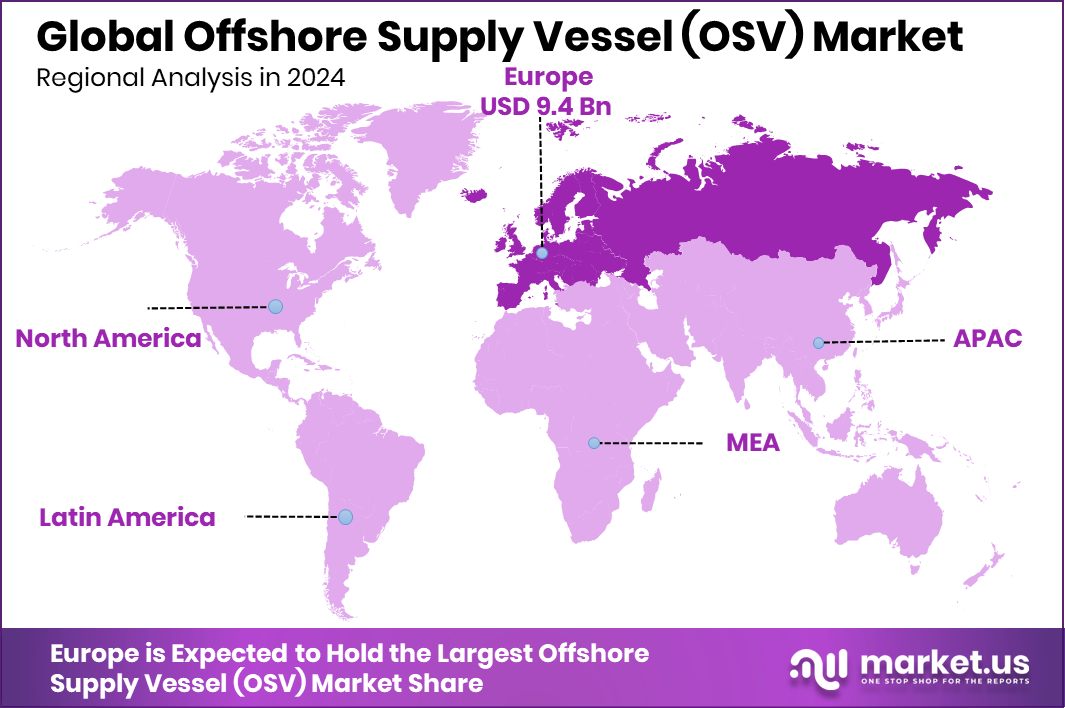

- Europe’s Offshore Supply Vessel market reached a total worth of USD 9.4 billion.

By Vessel Type Analysis

Anchor handling vessels dominate OSV fleet with 28.4% global market share.

In 2024, Anchor Handling Vessel held a dominant market position in the By Vessel Type segment of the Offshore Supply Vessel (OSV) Market, with a 28.4% share. These vessels played a critical role in offshore oil and gas operations, particularly in positioning and anchoring drilling rigs.

Their high demand stemmed from the increased offshore drilling activities and deepwater exploration projects, where heavy-duty anchor handling and towing capabilities are essential. The growing need to transport anchors, subsea equipment, and floating platforms further fueled the utilization of these vessels in both shallow and deepwater environments.

The segment’s growth was supported by operational flexibility and high bollard pull, making these vessels suitable for extreme weather and deepwater deployment. The steady demand from exploration and production companies continued to drive fleet expansions and retrofitting projects.

Additionally, technological advancements in dynamic positioning and fuel efficiency improved the performance of anchor handling vessels, strengthening their market presence. As offshore energy projects became more complex and capital-intensive, the need for reliable support vessels like anchor handling types remained strong.

By Water Depth Analysis

Shallow water operations accounted for 44.3% of OSV market in 2024.

In 2024, Shallow Water held a dominant market position in the by-water-depth segment of the Offshore Supply Vessel (OSV) Market, with a 44.3% share. This dominance was largely driven by the steady demand for OSVs in nearshore oil and gas fields, particularly in regions with mature shallow-water basins.

These operations typically require smaller, cost-effective vessels for transporting crew, equipment, and supplies to offshore platforms. Shallow water OSVs were preferred for their lower operating costs, simpler logistics, and faster turnaround times compared to deepwater alternatives.

The segment’s growth was further supported by ongoing maintenance and redevelopment activities in older offshore fields, especially in the Middle East, Southeast Asia, and parts of West Africa.

Many operators continued to prioritize cost optimization, making shallow water projects and supporting vessels more financially viable amid fluctuating oil prices. Additionally, regulatory approvals and shorter project lead times in shallow waters allowed faster deployment of OSVs.

By End-use Analysis

Oil and gas sector held 67.4% OSV market share in 2024.

In 2024, Oil and Gas held a dominant market position in the by-end-use segment of the Offshore Supply Vessel (OSV) Market, with a 67.4% share. This segment maintained its lead due to the continuous demand for logistical support in offshore exploration, drilling, and production activities.

OSVs are critical in transporting personnel, equipment, and supplies to offshore rigs, especially in remote locations where regular access is limited. The sector’s dominance reflects the high level of operational activity in offshore oil and gas blocks across regions like the Gulf of Mexico, the North Sea, the Middle East, and Asia-Pacific.

The market share also highlights the dependence of upstream offshore operations on specialized vessels such as platform supply vessels (PSVs), anchor handling tug supply vessels (AHTSVs), and emergency response vessels. These vessels remained essential to ensure the uninterrupted flow of operations, safety compliance, and supply chain continuity for oil and gas platforms.

Key Market Segments

By Vessel Type

- Anchor Handling Vessel

- Tug Supply Vessel

- Platform Supply Vessel

- Multipurpose Support Vessel

- Crew Vessel

- Chase Vessel

- Others

By Water Depth

- Shallow Water

- Deep Water

- Ultra Deep Water

By End-use

- Oil and Gas

- Offshore Wind

- Patrolling

- Others

Driving Factors

Rising Offshore Exploration Projects Boost OSV Demand

One of the key driving factors for the Offshore Supply Vessel (OSV) market is the rise in offshore oil and gas exploration projects. Many energy companies are expanding their operations in offshore areas to tap into untapped reserves, especially in regions like the North Sea, Middle East, and West Africa. These projects require constant transportation of equipment, personnel, and materials between the shore and offshore platforms.

As a result, demand for OSVs—particularly platform supply vessels and anchor handling tug vessels—has increased significantly. In 2024, this growing offshore activity directly pushed the need for a more reliable and versatile OSV fleet, making offshore exploration a major growth engine for the overall market.

Restraining Factors

High Operating and Maintenance Costs Limit Adoption

A major restraining factor in the Offshore Supply Vessel (OSV) market is the high cost of operations and maintenance. Running an OSV involves significant expenses related to fuel, crew salaries, repairs, insurance, and regulatory compliance.

These costs can rise sharply in harsh weather or remote offshore environments, where more robust and specialized vessels are required. For many smaller operators, such high expenses reduce profitability and make it harder to compete with larger companies.

Additionally, during periods of low oil prices, exploration budgets are cut, directly impacting OSV demand. In 2024, this challenge continued to affect vessel utilization rates and discouraged investment in new or upgraded OSVs, particularly in cost-sensitive or marginal offshore fields.

Growth Opportunity

Expanding Offshore Wind Projects Create New Opportunities

A major growth opportunity for the Offshore Supply Vessel (OSV) market lies in the rising number of offshore wind projects. As more countries invest in renewable energy, offshore wind farms are rapidly being developed, especially in Europe, Asia-Pacific, and the United States. These large-scale installations need support vessels for construction, transportation, and maintenance—similar to oil and gas operations.

OSVs can be modified or repurposed to serve wind energy needs, opening a fresh revenue stream for vessel operators. In 2024, the increase in offshore wind activity created strong demand for jack-up barges, crew transfer vessels, and multipurpose OSVs, offering new growth prospects for companies looking to diversify beyond traditional fossil fuel industries.

Latest Trends

Advanced Digital Technologies Transforming OSV Operations

A significant trend in the Offshore Supply Vessel (OSV) market is the adoption of advanced digital technologies to enhance operational efficiency and safety. In 2024, companies began integrating automation systems, dynamic positioning, and real-time monitoring tools into their vessels.

These technologies enable precise navigation and positioning, especially crucial in challenging offshore environments. The implementation of such systems reduces human error, lowers operational costs, and improves response times during critical operations. Additionally, the use of digital tools facilitates predictive maintenance, allowing operators to address potential issues before they escalate, thereby minimizing downtime.

As offshore projects become more complex, the reliance on digital solutions is expected to grow, positioning technologically advanced OSVs as preferred choices for operators seeking efficiency and reliability in their offshore endeavors.

Regional Analysis

In 2024, Europe led the OSV market with a 48.4% regional share value.

In 2024, Europe held a dominant position in the Offshore Supply Vessel (OSV) Market, accounting for 48.4% of the global share, valued at USD 9.4 billion. This leadership was driven by extensive offshore oil and gas operations in the North Sea and the rapid growth of offshore wind energy projects across the region.

The demand for various OSVs—such as platform supply vessels and anchor handling tug vessels—remained high due to complex offshore logistics and year-round operational requirements in European waters.

North America followed, supported by ongoing offshore drilling activities in the Gulf of Mexico. The Asia Pacific region also showed steady demand, particularly in Southeast Asia, where shallow-water exploration continues. The Middle East & Africa region maintained relevance due to strong offshore investments in countries like Saudi Arabia and Angola.

Meanwhile, Latin America’s OSV market remained moderate, backed by offshore activities in Brazil and Guyana. Across all these regions, Europe remained the clear leader in 2024, both in terms of share and market value, due to its combination of mature offshore infrastructure and a strong push toward renewable offshore energy.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, the global Offshore Supply Vessel (OSV) market is experiencing significant growth, driven by increased offshore exploration activities and the expansion of renewable energy projects. Key players such as Bass Marine Pty Ltd., BOURBON Maritime, and Damen Shipyards Group are strategically positioning themselves to capitalize on these trends.

Bass Marine Pty Ltd. continues to strengthen its presence in the OSV sector by offering specialized marine services tailored to offshore operations. Their focus on operational efficiency and safety has enabled them to maintain a competitive edge in servicing offshore oil and gas projects.

BOURBON Maritime, headquartered in France, has been proactive in modernizing its fleet to meet evolving industry demands. In 2024, BOURBON announced the renewal of its passenger transport fleet, aiming to reduce fuel consumption by 20%. This initiative includes the introduction of six new versatile “Surfers” designed for more efficient and sustainable navigation.

Damen Shipyards Group remains a pivotal player in the OSV market, leveraging its extensive shipbuilding expertise to deliver advanced vessels equipped with the latest technologies. Their emphasis on innovation and customization allows them to cater to a diverse range of offshore requirements, from traditional oil and gas support to emerging renewable energy projects.

Top Key Players in the Market

- Bass Marine Pty Ltd.

- BOURBON Maritime

- Damen Shipyards Group

- DP World

- Edison Chouest Offshore Co.

- Harren Shipping Services GmbH and Co. KG

- Harvey Gulf International Marine LLC

- Havila Shipping ASA

- Hornbeck Offshore Services Inc.

- Island Offshore Management AS

- Nam Cheong Ltd.

- Qatar Navigation QPSC

- Siem Offshore Inc.

- Vroon BV

- Wartsila Corp.

Recent Developments

- In March 2024, ECO partnered with Maersk Supply Service to provide wind turbine installation services in the U.S. offshore wind market. ECO will supply two tugs and two barges, enhancing the efficiency of offshore wind installations.

- In February 2023, Bourbon and Horizon Maritime formed a joint venture named Bourbon Horizon, based in Norway. This venture operates seven OSVs and aims to provide services in the North Sea and Canadian offshore markets, focusing on harsh environment operations.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 19.5 Billion |

| Forecast Revenue (2034) | USD 36.6 Billion |

| CAGR (2025-2034) | 6.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Vessel Type (Anchor Handling Vessel, Tug Supply Vessel, Platform Supply Vessel, Multipurpose Support Vessel, Crew Vessel, Chase Vessel, Others), By Water Depth (Shallow Water, Deep Water, Ultra Deep Water), By End-use (Oil and Gas, Offshore Wind, Patrolling, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Bass Marine Pty Ltd., BOURBON Maritime, Damen Shipyards Group, DP World, Edison Chouest Offshore Co., Harren Shipping Services GmbH and Co. KG, Harvey Gulf International Marine LLC, Havila Shipping ASA, Hornbeck Offshore Services Inc., Island Offshore Management AS, Nam Cheong Ltd., Qatar Navigation QPSC, Siem Offshore Inc., Vroon BV, Wartsila Corp. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Market")