Quick Navigation

Report Overview

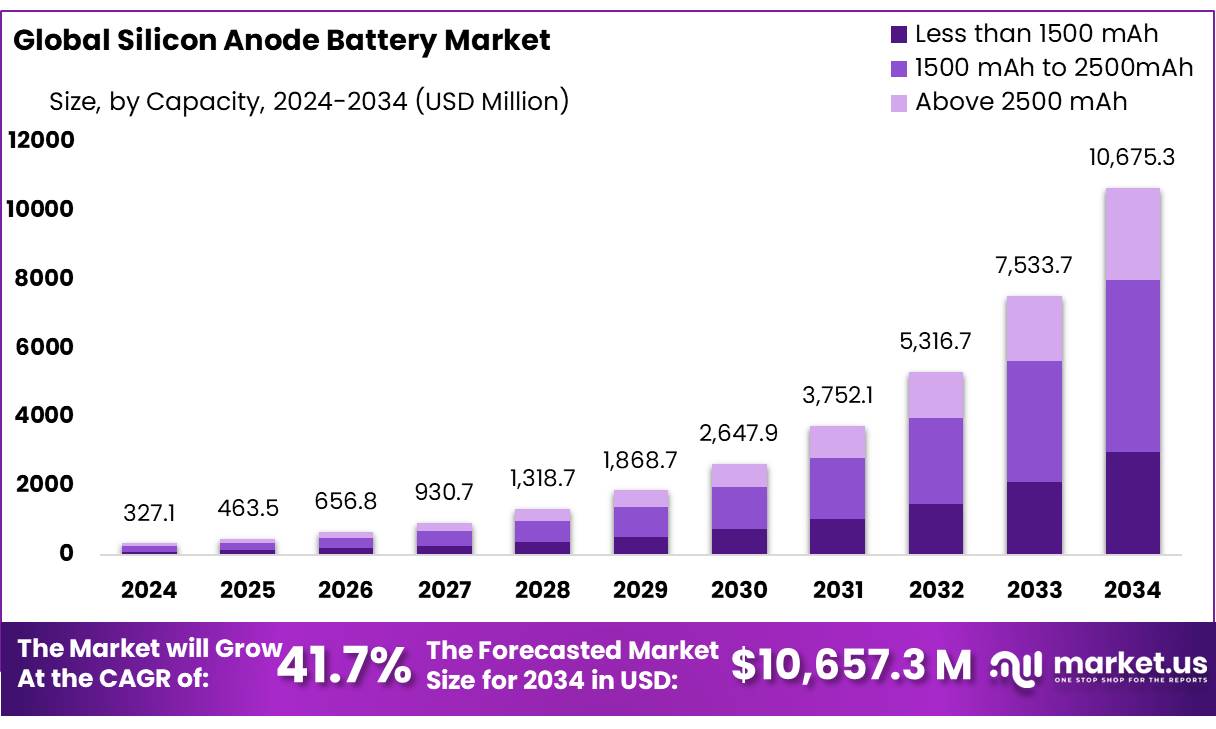

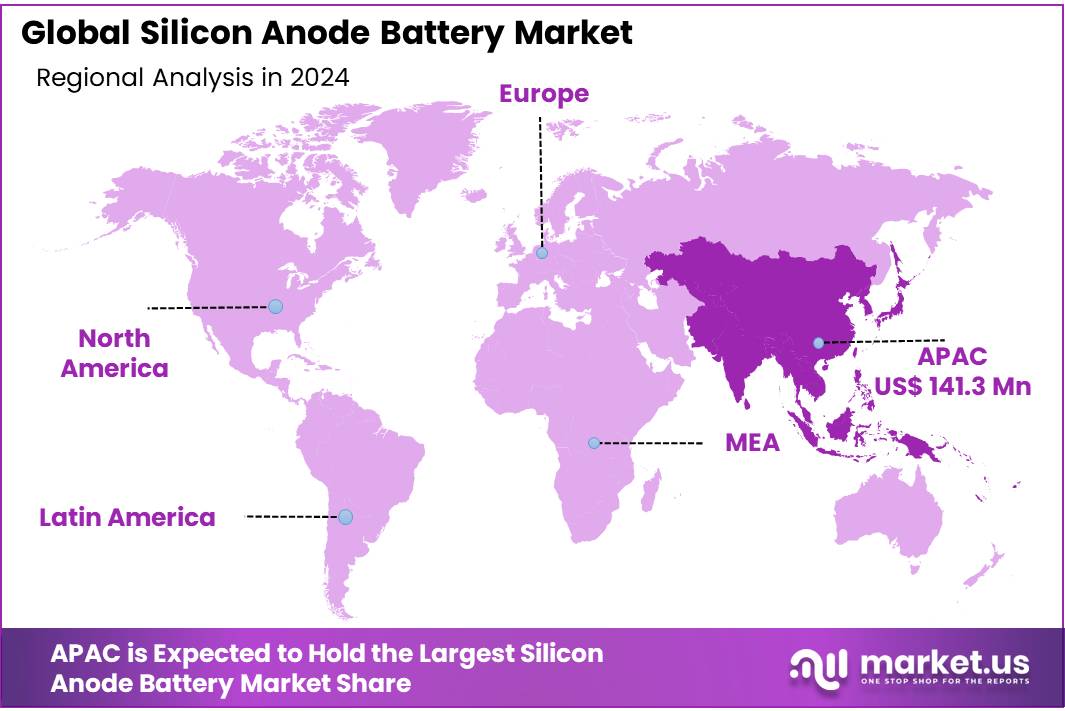

The Global Silicon Anode Battery Market size is expected to be worth around USD 10675.3 Million by 2034, from USD 327.1 Million in 2024, growing at a CAGR of 41.7% during the forecast period from 2025 to 2034. Asia-Pacific (APAC) held a dominant market position, capturing more than a 43.2% share, holding USD 141.3 Million revenue.

The silicon anode battery market is experiencing significant growth, driven by advancements in battery technology and increasing demand for high-performance energy storage solutions. Silicon anodes are emerging as a superior alternative to conventional graphite anodes in lithium-ion batteries, offering a higher capacity and longer lifecycle. Silicon’s theoretical capacity reaches approximately 4,200 mAh/g, nearly ten times that of graphite. This advancement is particularly crucial for electric vehicles (EVs), consumer electronics, and renewable energy storage systems, where enhanced performance and efficiency are paramount.

The global silicon anode battery market is experiencing rapid growth, driven by increasing demand across various sectors. In the United States, the Department of Energy (DOE) has launched initiatives to bolster domestic battery manufacturing. For instance, the DOE announced a funding opportunity to advance battery technologies, aiming to achieve carbon pollution-free electricity by 2035 and net-zero emissions by 2050. Additionally, the DOE has set goals to reduce the cost of electric vehicle battery packs to less than $100/kWh by 2028, enhancing the competitiveness of EVs in the market.

In Asia, countries like South Korea are investing in sustainable battery technologies. The South Korean government awarded NEO Battery Materials a role in a $20 million project focused on developing high-performance silicon anode materials using recycled silicon scrap from semiconductor manufacturing. This initiative underscores the emphasis on sustainability and resource efficiency in battery production.

Australia is also contributing to the advancement of silicon anode technology. The Australian Renewable Energy Agency (ARENA) committed $11.1 million to a three-year project aimed at commercializing AnteoTech’s proprietary silicon anode technology. The project’s goals include reducing battery storage costs and enabling longer driving ranges for EVs, highlighting the global effort to enhance battery performance.

From an investment perspective, silicon anode batteries are emerging as a promising frontier in energy storage. This surge is fueled by the demand for high-performance batteries in electric vehicles (EVs), consumer electronics, and renewable energy storage. Notably, companies like Group14 Technologies have developed materials such as SCC55™, which offers 50% more energy density and significantly reduces charging times . Such advancements are attracting substantial investments and partnerships, indicating a strong growth trajectory for the sector.

Key Takeaways

- Silicon Anode Battery Market size is expected to be worth around USD 10675.3 Mn by 2034, from USD 327.1 Mn in 2024, growing at a CAGR of 41.7%.

- 1500 mAh to 2500mAh capacity segment of the silicon anode battery market held a dominant position, capturing more than a 46.8% share.

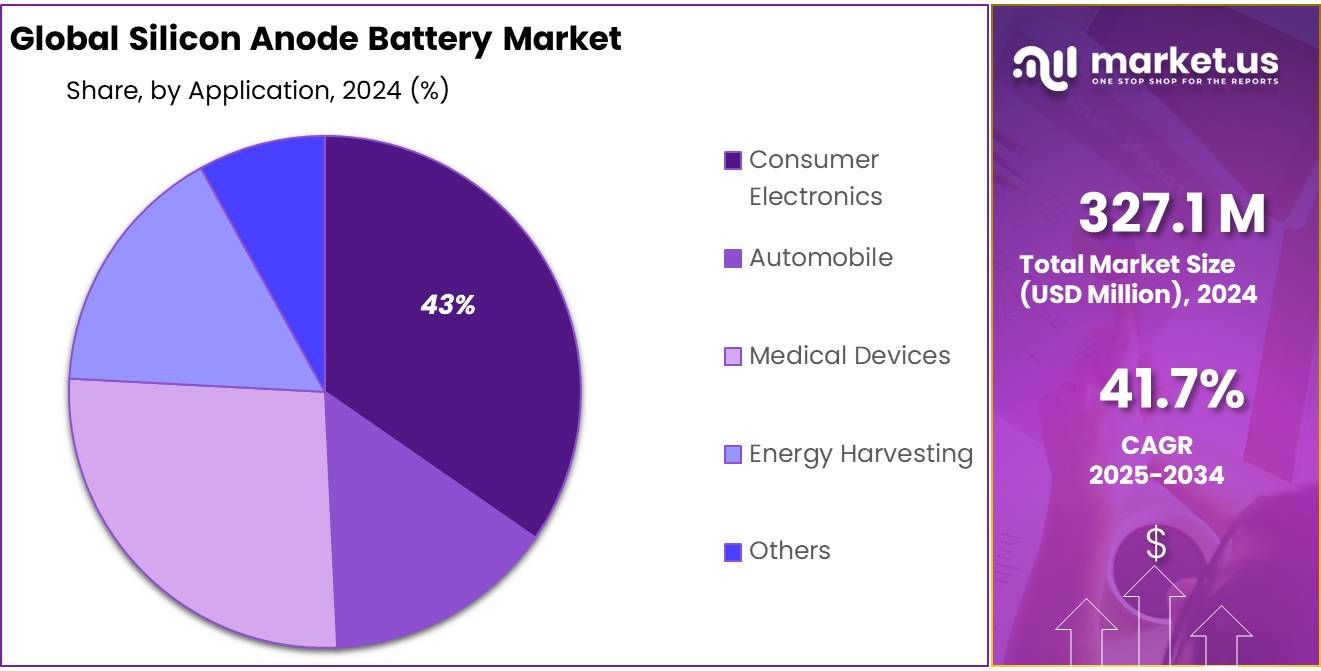

- Consumer Electronics segment held a dominant market position in the silicon anode battery market, capturing more than a 43.6% share.

- Asia-Pacific (APAC) region, the silicon anode battery market has established a strong foothold, demonstrating a significant market share of 43.2% and generating revenues amounting to USD 141.3 million.

US Tariff Impact Analysis

The recent imposition of U.S. tariffs on Chinese imports, including lithium-ion batteries and critical minerals, is significantly impacting the silicon anode battery market. As of April 2025, President Donald Trump initiated a national security probe into potential tariffs on all U.S. critical mineral imports, citing overreliance on foreign nations, especially China, for processed minerals vital to the U.S. economy . These tariffs have led to a sharp increase in battery costs, with Chinese battery cell imports now facing an effective 64.9% tariff, adding approximately $8 billion to costs for U.S. automakers and battery pack producers .

The global silicon anode battery market is experiencing rapid growth, driven by advancements in battery technology and increasing demand for high-energy-density solutions across electric vehicles (EVs), consumer electronics, and renewable energy storage. Silicon anodes offer significant advantages over traditional graphite anodes, including higher theoretical capacity and improved performance. Government initiatives, such as the U.S. Inflation Reduction Act, are accelerating the adoption of these technologies by providing substantial incentives for clean energy and battery manufacturing.

However, geopolitical tensions, particularly between the U.S. and China, pose challenges to the supply chain, as China dominates the production of critical materials like lithium and graphite . These tensions have led to export restrictions and trade barriers, potentially disrupting the availability and cost of essential components.

By Capacity

The 1500 mAh to 2500mAh segment leads with a 46.8% share, driven by high demand in consumer electronics.

In 2024, the 1500 mAh to 2500mAh capacity segment of the silicon anode battery market held a dominant position, capturing more than a 46.8% share. This range has proven particularly popular in the consumer electronics sector, where the demand for durable and efficient batteries is continuously increasing.

Devices such as smartphones, portable gaming systems, and tablets primarily drive this segment’s growth, as manufacturers aim to extend device usability while enhancing user experience. The enhanced capacity of silicon anode batteries not only meets these requirements but also offers a significantly longer lifespan compared to traditional lithium-ion counterparts.

By Application

Consumer Electronics leads with a 43.6% share, highlighting advanced battery needs.

In 2024, the Consumer Electronics segment held a dominant market position in the silicon anode battery market, capturing more than a 43.6% share. This substantial market share underscores the crucial role of advanced battery technologies in powering a wide array of consumer electronics. The segment benefits significantly from the continual miniaturization and enhanced functionality of consumer devices such as smartphones, laptops, and wearable technology, which require more powerful and longer-lasting batteries.

Silicon anode batteries are particularly suited to these applications due to their higher energy densities and efficiency compared to traditional lithium-ion batteries. This adaptation not only meets consumer demands for longer battery life and faster charging but also aligns with the ongoing trends towards more sustainable and efficient energy solutions in consumer electronics.

Key Market Segments

By Capacity

- Less than 1500 mAh

- 1500 mAh to 2500mAh

- Above 2500 mAh

By Application

- Consumer Electronics

- Automobile

- Medical Devices

- Energy Harvesting

- Others

Drivers

Government-backed EV initiatives boost silicon anode battery demand.

One of the major driving factors for the growth of the silicon anode battery market is the surging demand for electric vehicles (EVs) globally. Governments around the world are promoting the adoption of EVs through various incentives such as tax rebates, grants, and subsidies to reduce carbon emissions and mitigate climate change. For instance, the U.S. government has pledged significant investment into EV infrastructure, including charging stations and manufacturing hubs, as part of its broader environmental and energy policies.

The demand for EVs has directly impacted the need for more efficient and higher capacity batteries. Silicon anode batteries are particularly suited for this application due to their higher energy density compared to traditional lithium-ion batteries. This allows EVs to achieve greater range per charge, a key consumer requirement. For example, the incorporation of silicon anode technology can potentially increase battery efficiency by over 20%, significantly extending the driving range of EVs without increasing the physical size or weight of the battery pack.

Additionally, major automotive manufacturers are investing in battery research and development to decrease charging times and increase lifecycle, which are crucial for consumer acceptance and the broader adoption of electric vehicles. For instance, several leading automotive companies have formed partnerships with battery technology firms to integrate silicon anode batteries into their next-generation electric models.

Restraints

High production costs hinder widespread adoption of silicon anode technology.

A significant restraining factor in the silicon anode battery market is the high manufacturing cost associated with the production of silicon anode materials. Silicon anodes require more sophisticated and costly manufacturing processes compared to traditional graphite anodes. This is due to the complex nature of silicon, which expands and contracts significantly during charging cycles, necessitating additional engineering to maintain structural integrity and performance over time.

This high cost is a barrier for many battery manufacturers, particularly smaller players who may lack the financial resources to invest in necessary R&D and advanced production facilities. Moreover, the integration of silicon anodes into existing battery production lines often requires substantial modifications, adding further to the costs. For instance, specialized coatings and binders are needed to accommodate silicon’s expansive properties, which can double the production costs compared to conventional materials.

Despite these challenges, various government initiatives aim to reduce the impact of these costs. For example, the European Union’s Horizon 2020 program has funded projects that focus on improving the cost-effectiveness and scalability of advanced battery technologies, including silicon anode batteries. These efforts are crucial in making the technology more accessible and affordable for a broader range of manufacturers, potentially mitigating one of the key barriers to market expansion.

Opportunity

Silicon anode batteries key to enhancing renewable energy storage efficiency.

A significant growth opportunity for the silicon anode battery market lies in its expansion into renewable energy storage systems. As the global focus shifts towards sustainable energy, the demand for efficient storage solutions that can handle the intermittent nature of renewable sources like solar and wind is escalating. Silicon anode batteries, with their higher energy densities and efficiency, are perfectly suited to meet these demands.

Renewable energy systems require batteries that can store large amounts of energy during peak production times and then distribute it steadily, ensuring a reliable power supply despite variable weather conditions. Silicon anode batteries can significantly enhance the capacity and longevity of these storage systems compared to traditional batteries. For example, they are capable of providing up to three times the energy density of graphite-based lithium-ion batteries, which translates into longer storage periods and more reliable energy distribution.

Government initiatives across the globe support the integration of advanced battery technologies in renewable energy systems. The U.S. Department of Energy, for instance, has launched multiple programs under its Energy Storage Grand Challenge, aiming to accelerate the development and deployment of energy storage technologies, including those involving silicon anodes. These initiatives not only provide financial incentives but also foster research and collaboration between leading technology providers and energy sectors.

Trends

Silicon anode batteries: powering the next wave of IoT and smart devices.

One of the most prominent trends in the silicon anode battery market is the integration of these batteries into Internet of Things (IoT) devices and smart technology. As IoT devices proliferate, driven by the growing smart home, health, and automotive sectors, the demand for batteries that can operate efficiently under various conditions and last longer between charges is increasing. Silicon anode batteries are emerging as a top choice due to their higher energy density and longer lifespan compared to traditional lithium-ion counterparts.

This trend is amplified by the consumer’s shift towards smarter and more connected lifestyles, where devices are expected to perform with greater efficiency and reliability. Silicon anode batteries enable these devices to have a compact size while still maintaining the power and endurance needed for continuous data processing and connectivity. For instance, smartwatches, home automation systems, and health monitoring devices benefit greatly from extended battery life, as it enhances user convenience and device functionality.

Government and industry support for IoT development further fuels this trend. Initiatives like the European Union’s Digital Single Market strategy aim to integrate digital technologies across all economic sectors. This includes funding for research into technologies that enhance connectivity and sustainability of IoT devices, including advanced power solutions like silicon anode batteries.

Regional Analysis

APAC dominates with 43.2% market share, driven by tech innovation and strong governmental support.

In the Asia-Pacific (APAC) region, the silicon anode battery market has established a strong foothold, demonstrating a significant market share of 43.2% and generating revenues amounting to USD 141.3 million. This robust market position is driven by a combination of technological advancements, increasing investments in battery technology, and rising demand from key sectors such as consumer electronics and automotive.

APAC is home to several of the world’s leading economies like China, Japan, and South Korea, which are at the forefront of technological innovation in battery development. These countries house major tech companies and automotive manufacturers that are actively integrating silicon anode technologies to enhance battery performance and efficiency. The regional market is buoyed by strong governmental support through subsidies for electric vehicle (EV) manufacturing and renewable energy projects, which in turn stimulates demand for advanced battery technologies including silicon anode batteries.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Amprius Technologies focuses on high-energy silicon anode batteries designed for aviation, military, and wearable applications. The company’s proprietary silicon nanowire anode technology delivers energy densities exceeding 450 Wh/kg, enhancing performance for compact, high-demand devices. In 2024, Amprius announced expansion plans for its Colorado facility to meet growing demand from electric aviation and defense sectors. Its innovation continues to push the boundary of lightweight, ultra-efficient energy storage solutions.

Enevate Corporation is known for its fast-charging silicon-dominant anode technology, targeting electric vehicles and consumer electronics. Their XFC-Energy™ tech allows 5-minute ultra-fast charging and high energy density, enhancing EV driving range significantly. Backed by strategic investors including Nissan and LG Chem, Enevate is advancing towards commercial partnerships. In 2024, the company expanded its pilot production to serve OEMs globally looking for next-gen EV battery solutions.

Group14 Technologies develops advanced silicon-carbon composite materials under the brand SCC55™ to boost lithium-ion battery performance. In 2024, the company opened one of the world’s largest commercial silicon battery material factories in Washington. Its material delivers up to 50% more energy density and faster charging. With backing from Porsche and other major investors, Group14 is expanding globally, aiming to accelerate the electrification of transportation and grid systems.

Top Key Players in the Silicon Anode Battery Market

- Amprius technologies

- California Lithium Battery

- Enevate Corporation

- ENOVIX Corporation

- Group14 Technologies

- Hitachi Chemical Co., Ltd.

- LG Chem.

- Los Angeles Cleantech Incubator

- Nexeon Ltd

- OneD Material, Inc.

- Panasonic Corporation

- SAMSUNG SDI CO., LTD.

Recent Developments

In 2024, Amprius Technologies made significant strides in the silicon anode battery market. The company introduced its SiCore™ platform, delivering a 6.3Ah 21700 cylindrical cell with an energy density of 315 Wh/kg, marking a 25% capacity increase over standard 5.0Ah cells.

In 2024, California Lithium Battery (CalBattery) has established a pilot manufacturing facility with a capacity to produce up to 10,000 cells annually, housed within a 30,000 square foot space. This facility is equipped to produce both pouch and cylindrical cells, emphasizing next-generation technologies like lithium metal, silicon anodes, and novel electrolytes.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 327.1 Mn |

| Forecast Revenue (2034) | USD 10675.3 Mn |

| CAGR (2025-2034) | 41.7% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Capacity (Less than 1500 mAh, 1500 mAh to 2500mAh, Above 2500 mAh), By Application (Consumer Electronics, Automobile, Medical Devices, Energy Harvesting, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Amprius technologies, California Lithium Battery, Enevate Corporation, ENOVIX Corporation, Group14 Technologies, Hitachi Chemical Co., Ltd., LG Chem., Los Angeles Cleantech Incubator, Nexeon Ltd, OneD Material, Inc., Panasonic Corporation, SAMSUNG SDI CO., LTD |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |