Quick Navigation

Report Overview

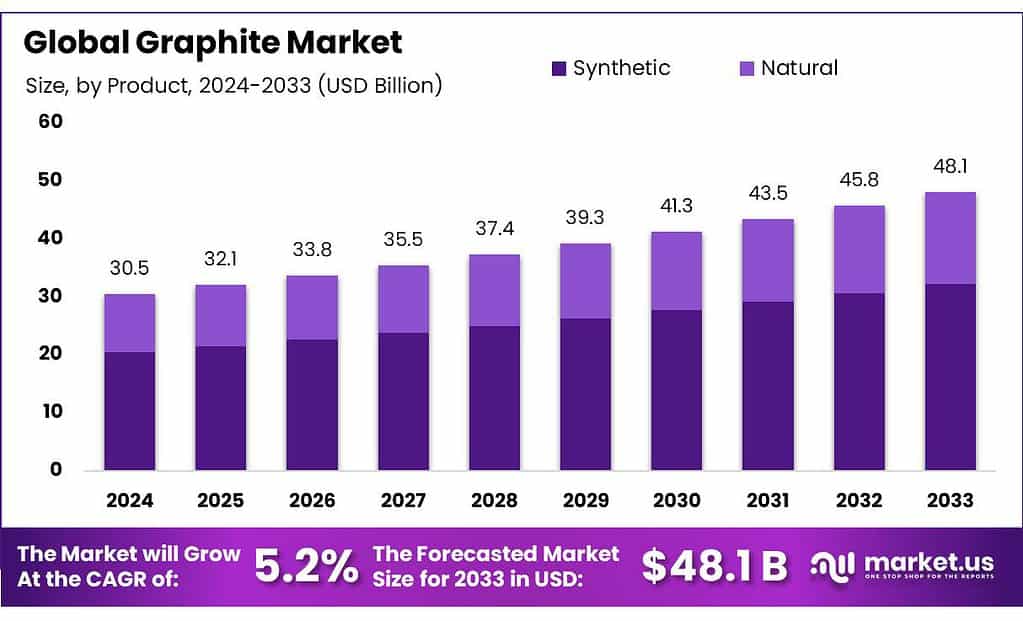

The global Graphite Market size is expected to be worth around USD 48.1 billion by 2033, from USD 30.5 billion in 2023, growing at a CAGR of 5.2% during the forecast period from 2023 to 2033.

The graphite market encompasses the global industry involved in producing, distributing, and applying graphite, a carbon form prized for its excellent conductivity, thermal resistance, and lubrication properties. Graphite plays a crucial role in high-tech applications, especially in lithium-ion batteries used in electric vehicles (EVs). It’s also integral to producing lubricants, conductive materials, and advanced composites. The market spans from graphite mining and refining to its use in diverse sectors such as automotive, electronics, aerospace, and energy.

Environmental standards regulate graphite production and use to ensure safety and minimize environmental impact. The European Union’s REACH regulation governs the use of chemicals like graphite, while the U.S. Environmental Protection Agency (EPA) enforces regulations on graphite mining and processing. Adhering to these regulations is essential for market access and compliance.

Global trade dynamics are significant for graphite due to its role in various high-tech industries. In 2022, the trade value of graphite and its products was about $14 billion. China dominates as the largest exporter, responsible for nearly 60% of global exports. The United States, which imported around $1.5 billion of graphite in 2022, highly depends on these imports to meet its domestic needs.

Governments are investing heavily in graphite-related technologies and infrastructure. For instance, the U.S. Department of Energy (DOE) is funding projects to improve graphite’s use in energy storage solutions. The European Union’s Horizon Europe program, with a budget of €95.5 billion for 2021-2027, supports research and development in advanced materials, including graphite.

Innovation in graphite technology is driving market growth, with advancements such as high-purity graphite for batteries and advanced materials. Significant industry movements include the 2022 merger between GrafTech International and Superior Graphite, expanding their market reach. Additionally, companies like Tesla are investing in new graphite sourcing and processing technologies to secure their supply chains for EV batteries. These factors collectively shape the graphite market, highlighting its importance and ongoing development.

Key Takeaways

- Market Growth is Expected to rise from USD 30.5 billion in 2023 to USD 48.1 billion by 2033, growing at a CAGR of 5.2%.

- Synthetic Graphite Holds over 67.5% of the market share in 2023, crucial for high-tech applications like lithium-ion batteries.

- Powder Graphite Dominates with a 28.5% share in 2023, favored for its versatility in applications such as lubricants and conductive materials.

- Refractories Leading application with a 35.3% market share in 2023, due to graphite’s high thermal stability and corrosion resistance.

- Automobile & Aerospace Captures over 38.4% of the market in 2023, driven by demand for high-performance components in these sectors.

- Asia Pacific (APAC) Accounts for 57.9% of the market, valued at USD 17.4 billion in 2023, with strong industrial and technological growth.

By Product

In 2023, Synthetic graphite held a dominant market position, capturing more than a 67.5% share. This type of graphite is highly valued for its consistent quality and performance in high-tech applications. It is primarily used in batteries, especially for electric vehicles, due to its superior conductivity and thermal properties. Synthetic graphite’s manufacturing process allows for precise control over its properties, making it ideal for advanced technologies.

Natural graphite, on the other hand, accounted for the remaining market share. It is sourced from mining operations and is used in applications such as lubricants and traditional batteries. While natural graphite is more abundant, its use is often limited by variable quality and impurities.

However, it remains important for various industrial applications where high purity is not as critical. The balance between synthetic and natural graphite reflects their respective roles and growing demands in the market.

By Form

In 2023, Powder graphite held a dominant market position, capturing more than a 28.5% share. This form of graphite is widely used due to its versatility and ease of integration into various products. It is crucial in applications such as lubricants, batteries, and conductive materials. The powder form allows for fine dispersion and effective performance in diverse uses.

Flake additives, another significant segment, are used for their high purity and performance in applications like battery anodes and specialty coatings. Expandable flakes are valued in industries requiring expandable and high-strength materials, such as fire retardants and high-performance lubricants.

Pellets are utilized in applications requiring precise measurements and consistent performance, such as in metallurgy. Film and sheet graphite are employed in advanced technologies, including thermal management and electrical applications. Other forms, though less prominent, serve specialized needs across various industries. Each form plays a specific role, contributing to the overall demand and application of graphite in the market.

By Application

In 2023, Refractories held a dominant market position, capturing more than a 35.3% share. Graphite is essential in refractories due to its high thermal stability and resistance to corrosion. It is widely used in furnaces and kilns to withstand extreme temperatures and harsh conditions.

Batteries, especially those for electric vehicles, followed closely as a significant application. Graphite’s role in battery anodes is crucial for high energy density and performance. Friction products also account for a notable share, as graphite’s lubricating properties are ideal for reducing wear and tear in automotive brakes and clutches.

Lubricants are another major segment, where graphite’s lubricating characteristics enhance performance and durability in various industrial applications. Recarburizing, the process of adding carbon to steel, relies on graphite to improve the quality and properties of the final product. Other applications, while smaller in scale, also contribute to the market by addressing specialized needs across different industries. Each application leverages graphite’s unique properties, driving its diverse use across sectors.

By End-use

In 2023, Automobile & Aerospace held a dominant market position, capturing more than a 38.4% share. Graphite is critical in these sectors for its use in high-performance components, including batteries and thermal management systems in vehicles and aircraft. Its properties support advanced manufacturing and operational efficiency in these demanding industries.

Power Generation also represents a significant portion of the market. Graphite is used in various applications such as high-temperature coatings and components in power plants, which require materials that can withstand intense conditions.

The Electronics sector is another major user of graphite. It is essential in components like batteries and conductors, where its electrical conductivity and thermal resistance are key advantages. Other sectors, while smaller, still rely on graphite for specialized uses, such as in certain industrial processes and products. Each end-use sector highlights graphite’s versatility and importance across diverse applications.

Key Market Segments

By Product

- Synthetic

- Natural

By Form

- Flake Additives

- Powder

- Expandable Flakes

- Pellets

- Film & Sheet

- Others

By Application

- Refractories

- Foundries

- Batteries

- Friction Products

- Lubricants

- Recarburizing

- Others

By End-use

- Automobile & Aerospace

- Power Generation

- Electronic

- Others

Driving Factors

Growing Demand for Electric Vehicles (EVs)

The increasing demand for electric vehicles (EVs) is a major driving factor for the graphite market. Graphite plays a crucial role in the production of lithium-ion batteries, which are essential for EVs. According to the International Energy Agency (IEA), global EV sales reached 10 million units in 2022, representing a significant growth of 55% from the previous year. This surge in EV sales directly boosts the demand for graphite, as each EV battery requires a substantial amount of this material.

Graphite is used primarily in the anodes of lithium-ion batteries. The battery industry alone accounted for around 40% of global graphite consumption in 2022. As the shift toward electric vehicles continues, the need for high-quality graphite to improve battery efficiency and performance is expected to rise.

Government initiatives and policies aimed at reducing carbon emissions and promoting green technology further accelerate this trend. For instance, the European Union has set ambitious targets for reducing CO2 emissions from new cars, with plans to cut emissions by 55% by 2030. Similarly, the U.S. government is offering incentives for EV purchases and investing in charging infrastructure, which supports the broader adoption of electric vehicles. These policies drive up the demand for EVs and, consequently, the demand for graphite used in their batteries.

Moreover, the shift towards renewable energy sources, which also rely on advanced battery technologies for energy storage, contributes to the growing need for graphite. The International Renewable Energy Agency (IRENA) reports that renewable energy capacity expanded by 9.6% in 2022, further highlighting the increasing reliance on battery storage solutions, where graphite plays a critical role.

Restraints Factors

Environmental and Regulatory Challenges

One major restraining factor for the graphite market is the environmental and regulatory challenges associated with graphite mining and processing. These challenges can significantly impact production costs and market dynamics.

Graphite mining, particularly in countries like China, which produces about 60% of the world’s graphite, often involves practices that raise environmental concerns. The extraction and processing of graphite can lead to soil and water contamination, air pollution, and significant ecological disruption. According to a report by the United Nations Environment Programme (UNEP), mining activities contribute to about 70% of industrial pollution, including heavy metals and toxic chemicals. The environmental impact of graphite mining is a concern for governments and organizations globally, driving stricter regulations.

Regulatory frameworks, such as the European Union’s REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) and the U.S. Environmental Protection Agency’s (EPA) regulations, impose stringent standards on the mining and processing of graphite.

The EU REACH regulation requires companies to provide detailed safety data for chemicals, including graphite, to ensure that they do not pose risks to human health or the environment. Compliance with these regulations can be costly and complex. For instance, the European Chemical Agency (ECHA) reported that the cost of compliance with REACH can exceed €1 million for large chemical companies, including those involved in graphite production.

Additionally, the U.S. EPA has set guidelines under the Toxic Substances Control Act (TSCA) for managing and controlling hazardous substances, which affect graphite production. Adhering to these regulations can increase operational costs and impact profitability. The EPA’s recent updates to TSCA regulations have placed further restrictions on industrial practices, which could affect graphite mining and processing operations.

The focus on sustainable and environmentally friendly practices is increasing, driven by both government policies and public awareness. The global push towards sustainability means that companies must invest in cleaner technologies and processes to mitigate environmental damage. For example, the International Energy Agency (IEA) highlights that transitioning to greener mining practices could increase production costs by up to 20%. These costs are often passed on to consumers, potentially affecting the market demand for graphite.

Moreover, trade policies and tariffs can add to the complexities of the graphite market. For instance, recent trade tensions between major graphite-producing countries, such as China and the U.S., have led to tariffs and trade barriers that disrupt global supply chains. The imposition of tariffs can increase the cost of imported graphite, affecting global market stability and pricing.

Growth Opportunity

Expansion in Battery Technologies

A major growth opportunity for the graphite market lies in the expansion of battery technologies, particularly those used in electric vehicles (EVs) and renewable energy storage systems. Graphite is a crucial component in lithium-ion batteries, which are increasingly adopted due to their efficiency and performance.

The U.S. DOE’s initiative includes funding for research and development projects that focus on improving battery performance and reducing costs. Similarly, the European Union’s Horizon Europe program, with a budget of €95.5 billion for 2021-2027, supports innovations in energy storage and battery technologies, including those involving graphite.

Additionally, the shift towards renewable energy sources increases the demand for battery storage solutions. According to the International Renewable Energy Agency (IRENA), renewable energy capacity grew by 9.6% in 2022, emphasizing the need for effective energy storage systems. Graphite’s role in enhancing energy storage technologies makes it integral to the growth of this sector.

Latest Trends

Advancements in Graphite Anode Technology

One major latest trend in the graphite market is the advancement in graphite anode technology, particularly in the context of lithium-ion batteries used for electric vehicles (EVs) and energy storage systems. This trend reflects ongoing innovations aimed at improving battery performance and efficiency.

Graphite anodes are crucial for lithium-ion batteries, which are essential for the growing EV market. In 2023, the global electric vehicle market saw a record 11 million units sold, a notable increase from previous years, according to the International Energy Agency (IEA). This growth has fueled the demand for advanced graphite anodes, which enhance battery performance by providing better energy density and longer cycle life.

Recent innovations focus on developing high-capacity and high-conductivity graphite anodes to improve battery efficiency. For instance, the development of silicon-graphite composite anodes aims to increase the energy storage capacity of batteries.

Silicon-graphite anodes can theoretically offer up to 30% higher capacity than traditional graphite anodes, according to a study by the U.S. Department of Energy’s (DOE) Argonne National Laboratory. This advancement is significant as it addresses the limitations of conventional graphite anodes and meets the rising demand for high-performance batteries.

Government initiatives are also supporting advancements in graphite anode technology. In the United States, the DOE has invested over $200 million in research projects focused on improving battery technologies, including those related to graphite anodes. This funding is part of the DOE’s broader strategy to enhance energy storage technologies and reduce the cost of electric vehicle batteries.

Similarly, the European Union’s Horizon Europe program provides significant funding for research in advanced materials, including innovations in battery technology. The EU’s commitment to advancing energy storage solutions is underscored by its allocation of €95.5 billion for research and innovation from 2021 to 2027.

Moreover, companies are increasingly focusing on technological improvements in graphite anodes. For example, in 2023, Tesla announced plans to use advanced graphite anodes in its new battery technology, aiming to increase the energy density of its electric vehicle batteries. This move highlights the industry’s shift toward incorporating cutting-edge materials and technologies to enhance battery performance.

The growth in renewable energy storage systems also drives this trend. The International Renewable Energy Agency (IRENA) reported that renewable energy capacity increased by 9.6% in 2022, emphasizing the need for efficient energy storage solutions. High-performance graphite anodes play a crucial role in improving the efficiency of storage systems, supporting the broader adoption of renewable energy technologies.

Regional Analysis

The global graphite market exhibits substantial regional disparities, reflecting varied growth dynamics and demand drivers across different geographies. Asia Pacific (APAC) is the dominant region in the graphite market, commanding a significant 57.9% share, with a market value reaching USD 17.4 billion in 2023.

This dominance is largely driven by the region’s robust industrial sector, extensive manufacturing base, and rapid advancements in technology, particularly in electric vehicles and energy storage systems. Countries such as China, India, and Japan are key contributors, with China leading as the largest producer and consumer of graphite globally.

North America follows as a notable market for graphite, supported by its growing demand in the battery and aerospace industries. The region’s market is bolstered by ongoing investments in electric vehicle production and renewable energy technologies, which are increasing the demand for high-quality graphite. In 2023, North America’s market share was substantial, driven by technological innovation and significant industrial applications.

Europe also represents a significant segment of the graphite market, with a focus on sustainable technologies and high-performance applications. The European market benefits from stringent environmental regulations and a strong emphasis on green technologies, which drive demand for advanced graphite products. Key countries like Germany and the UK are pivotal in this region’s market dynamics.

In the Middle East & Africa, the graphite market is emerging, with growth fueled by increasing industrial activities and investments in infrastructure. The region is expected to experience steady growth, driven by expanding construction and energy sectors.

Latin America, while smaller in comparison, shows gradual growth due to rising industrialization and infrastructure development, particularly in countries like Brazil and Argentina. The market is supported by increasing investments in mining and manufacturing.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Market Key Players

- AMG

- Asbury Carbons

- BTR NEW Material Group Co., Ltd.

- Eagle Graphite

- EPM Group

- Grafitbergbau Kaisersberg GmbH

- Graphite India Limited

- Imerys S.A.

- Mineral Commodities Ltd.

- Nacional de Grafite

- NIPPON GRAPHITE INDUSTRIES CO. LTD.

- NORTHERN GRAPHITE CORPORATION

- Qingdao Tennry Carbon Co., Ltd.

- SGL Carbon

- SHOWA DENKO K.K.

- Stoker Concast Pvt. Ltd.

- Superior Graphite

- Syrah Resources Limited

- Tirupati Carbons & Chemicals Pvt. Ltd.

- Tokai Carbon Co., Ltd.

Recent Development

In 2023, Asbury Carbons maintained its strong market presence through continued investments in expanding its product range and enhancing its production capabilities.

In 2023, BTR New Material Group Co., Ltd. continued to strengthen its position by expanding its production capabilities and enhancing its product offerings, particularly in high-performance graphite materials for energy storage and electronics.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 30.5 Bn |

| Forecast Revenue (2033) | US$ 48.1 Bn |

| CAGR (2024-2033) | 5.2% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product(Synthetic, Natural), By Form(Flake Additives, Powder, Expandable Flakes, Pellets, Film and Sheet, Others), By Application(Refractories, Foundries, Batteries, Friction Products, Lubricants, Recarburizing, Others), By End-use(Automobile and Aerospace, Power Generation, Electronic, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | AMG, Asbury Carbons, BTR NEW Material Group Co., Ltd., Eagle Graphite, EPM Group, Grafitbergbau Kaisersberg GmbH, Graphite India Limited, Imerys S.A., Mineral Commodities Ltd., Nacional de Grafite, NIPPON GRAPHITE INDUSTRIES CO. LTD., NORTHERN GRAPHITE CORPORATION, Qingdao Tennry Carbon Co., Ltd., SGL Carbon, SHOWA DENKO K.K., Stoker Concast Pvt. Ltd., Superior Graphite, Syrah Resources Limited, Tirupati Carbons & Chemicals Pvt. Ltd., Tokai Carbon Co., Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |