Quick Navigation

Report Overview

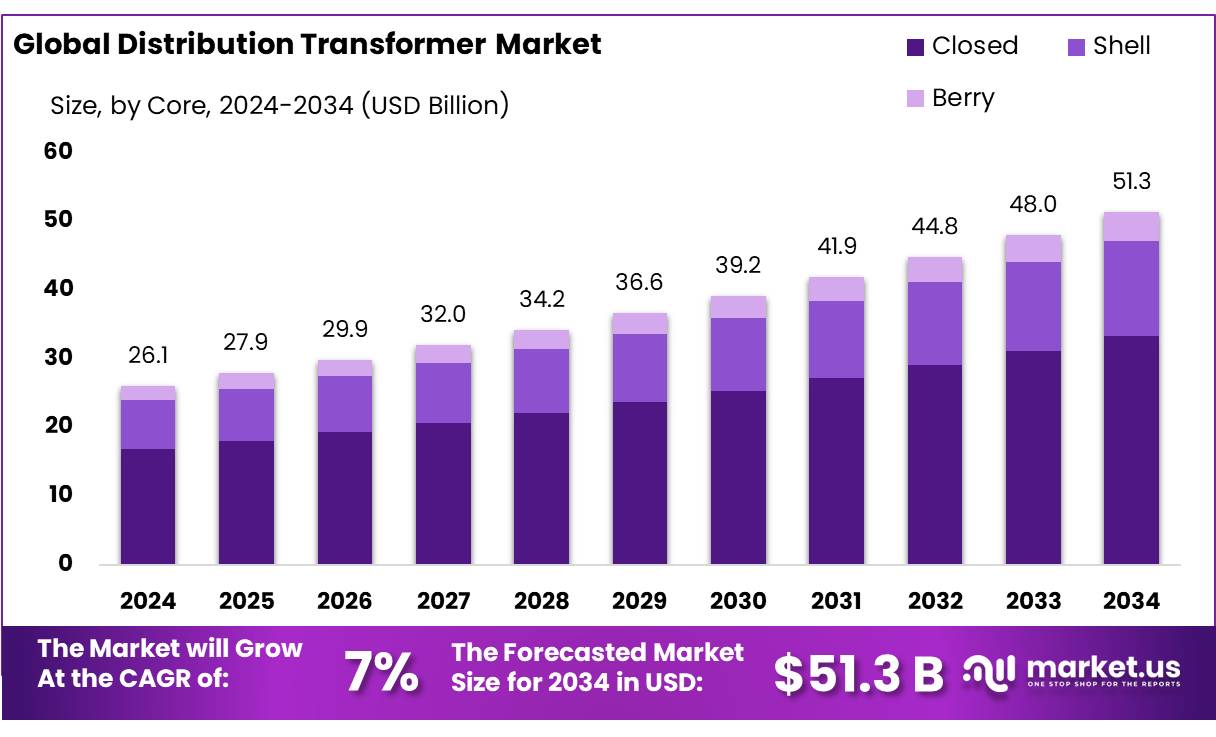

The Global Distribution Transformer Market size is expected to be worth around USD 51.3 Billion by 2034, from USD 26.1 Billion in 2024, growing at a CAGR of 7.0% during the forecast period from 2025 to 2034.

Distribution transformers are critical components in the electrical power distribution system, stepping down high-voltage electricity from transmission lines to lower voltages suitable for residential, commercial, and industrial use. They ensure the safe and efficient delivery of electricity to end-users, maintaining voltage levels within acceptable limits and minimizing power losses.

The integration of renewable energy sources into the grid has also necessitated the deployment of advanced distribution transformers capable of handling variable power inputs. For instance, Gujarat’s Green Energy Corridor (GEC-III) project, with an investment of ₹29,000 crore, aims to transmit 16,500 MW of renewable power across the state. This initiative involves the construction of new substations and transmission lines, requiring the installation of distribution transformers to manage the flow of green energy.

The integration of renewable energy sources is another significant driver. As of March 2024, renewable energy accounted for 46.3% of India’s total installed power capacity. The government’s target of achieving 500 GW of renewable energy capacity by 2030 necessitates the deployment of advanced distribution transformers capable of handling variable power inputs and ensuring grid stability.

Government initiatives have played a pivotal role in bolstering the distribution transformer market. The Revamped Distribution Sector Scheme (RDSS), launched in 2021 with an outlay of ₹3 trillion, aims to enhance the operational efficiency and financial sustainability of distribution companies. Additionally, the National Infrastructure Pipeline (NIP) has earmarked substantial investments for the energy sector, further supporting the expansion and modernization of the power distribution network.

Government initiatives have been instrumental in propelling the distribution transformer market. The Ujwal DISCOM Assurance Yojana (UDAY), launched in 2015, aimed to improve the financial health of power distribution companies (DISCOMs) by allowing state governments to take over 75% of their debt and issue bonds for the remaining 25%. Additionally, the Saubhagya scheme has significantly advanced rural electrification, thereby increasing the demand for distribution transformers in newly electrified areas.

Key Takeaways

- Distribution Transformer Market size is expected to be worth around USD 51.3 Billion by 2034, from USD 26.1 Billion in 2024, growing at a CAGR of 7.0%.

- Oil held a dominant market position, capturing more than a 57.9% share in the Distribution Transformer market

- Three held a dominant market position, capturing more than an 81.1% share in the Distribution Transformer market.

- ≤2.5 MVA held a dominant market position, capturing more than a 56.3% share in the Distribution Transformer market.

- Pad held a dominant market position, capturing more than a 59.5% share in the Distribution Transformer market.

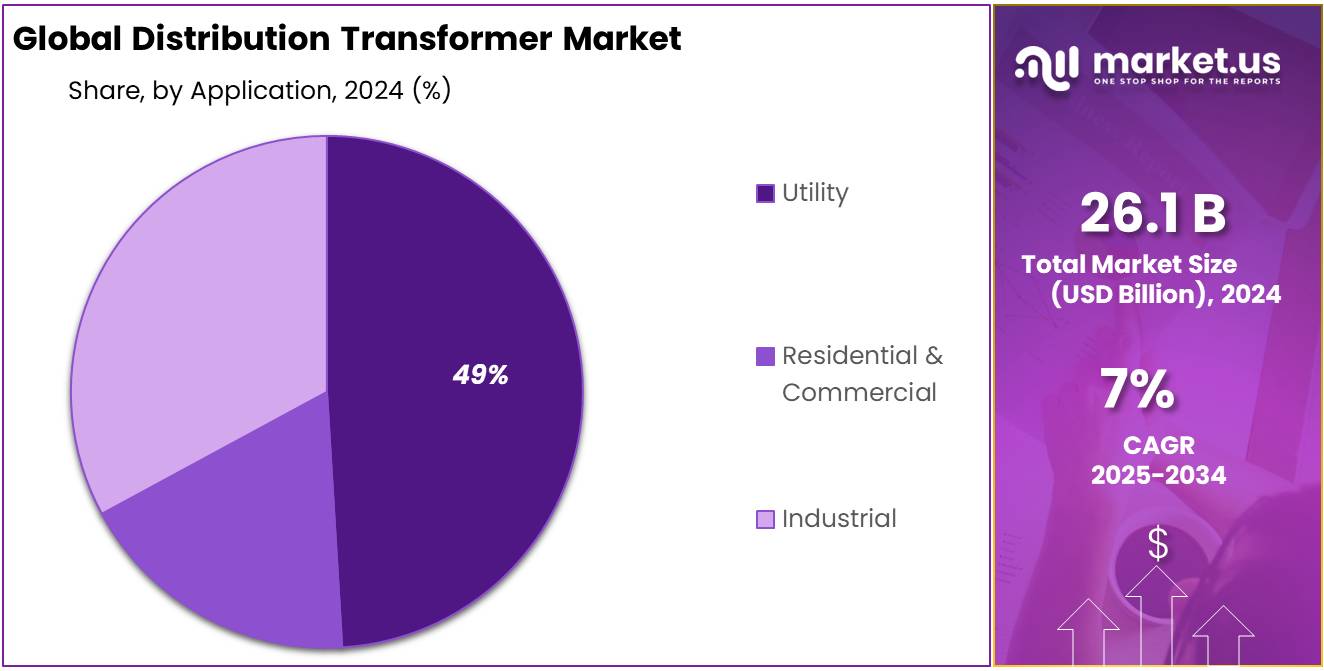

- Utility held a dominant market position, capturing more than a 49.2% share in the Distribution Transformer market.

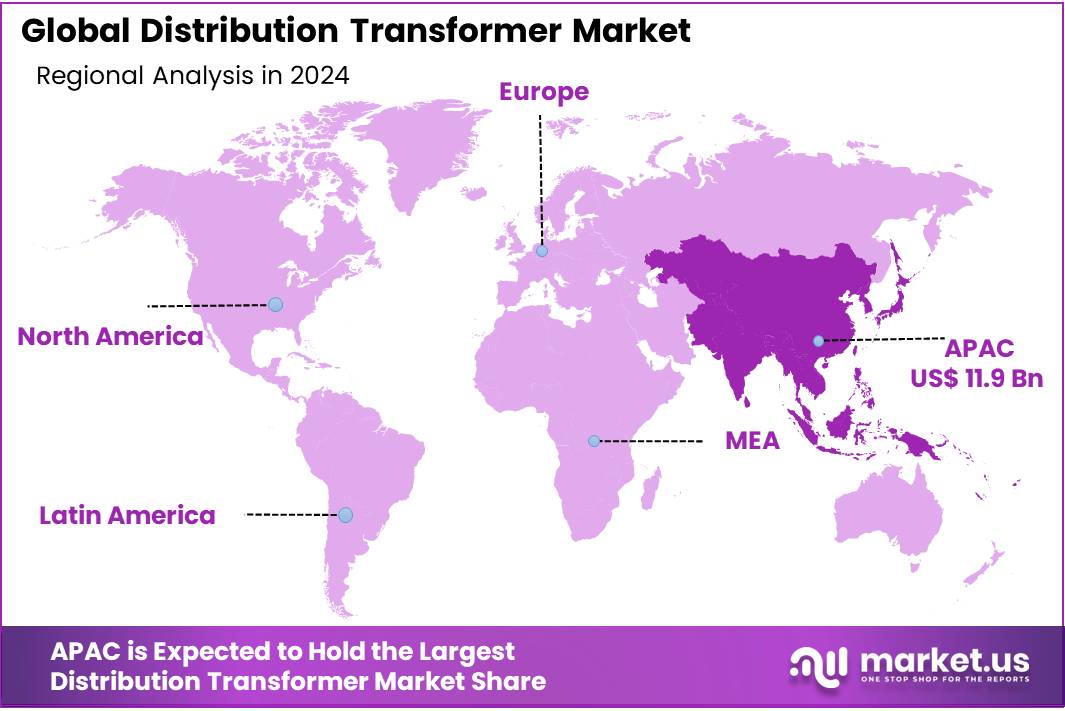

- Asia-Pacific (APAC) region solidified its position as the leading market for distribution transformers, commanding a substantial 45.6% share, equivalent to approximately USD 11.9 billion.

By Insulation

Oil-Insulated Distribution Transformers dominate with 57.9% share in 2024 due to high durability and cost-efficiency

In 2024, Oil held a dominant market position, capturing more than a 57.9% share in the Distribution Transformer market by insulation type. This dominance is largely attributed to the oil insulation’s proven reliability, effective cooling capabilities, and lower initial cost compared to alternative insulation types. Oil-filled transformers continue to be the preferred choice for utilities and industrial users, particularly in rural and semi-urban areas, where load patterns are variable and equipment longevity is critical. The robustness of mineral oil as an insulating medium also supports long operational life and better fault tolerance under fluctuating load conditions.

By Phase

Three-Phase Distribution Transformers dominate with 81.1% share in 2024 driven by large-scale commercial and industrial demand

In 2024, Three held a dominant market position, capturing more than an 81.1% share in the Distribution Transformer market by phase type. This clear dominance is the result of the widespread use of three-phase transformers in industrial facilities, commercial buildings, and large residential complexes where higher load handling and balanced power supply are critical. These transformers offer efficient energy transfer, reduced conductor material requirements, and are more suitable for high-capacity networks compared to single-phase units.

By Rating

≤2.5 MVA Distribution Transformers dominate with 56.3% share in 2024 due to widespread use in rural and residential networks

In 2024, ≤2.5 MVA held a dominant market position, capturing more than a 56.3% share in the Distribution Transformer market by rating. This segment leads primarily because of the extensive deployment of low-rating transformers across residential areas, small commercial facilities, and rural electrification projects. These units are ideal for low-to-moderate power demand, offering cost-effective and space-efficient solutions where full-scale grid infrastructure is either unnecessary or still under development.

By Mounting

Pad-Mounted Distribution Transformers lead with 59.5% share in 2024 owing to their safety and space-saving design in urban areas

In 2024, Pad held a dominant market position, capturing more than a 59.5% share in the Distribution Transformer market by mounting type. This strong performance is largely due to the rising adoption of pad-mounted transformers in urban and suburban settings, where space constraints, safety requirements, and aesthetics are key considerations. These transformers are installed at ground level in locked metal enclosures, making them a preferred choice for public areas, commercial complexes, and residential neighborhoods.

By Application

Utility Sector leads Distribution Transformer Market with 49.2% share in 2024 due to rising electrification and grid upgrades

In 2024, Utility held a dominant market position, capturing more than a 49.2% share in the Distribution Transformer market by application. This lead stems from the increasing focus on electrification, rural connectivity, and nationwide grid expansion initiatives undertaken by public and private utility providers. Utilities play a central role in setting up power infrastructure to meet the growing energy needs of both urban and remote regions, and distribution transformers are essential to these efforts for stepping down high voltage to usable levels.

Key Market Segments

By Insulation

- Gas

- Oil

- Solid

- Air

- Others

By Phase

- Single

- Three

By Rating

- ≤2.5 MVA

- 2.6 MVA to 10 MVA

- > 10 MVA

By Mounting

- Pad

- Pole

- Others

By Application

- Utility

- Residential & Commercial

- Industrial

Drivers

Government Electrification Initiatives Fuel Distribution Transformer Demand

One of the primary drivers of the distribution transformer market is the global push for electrification, particularly in rural and underserved areas. Governments worldwide are implementing initiatives to expand electricity access, necessitating the deployment of distribution transformers to step down voltage levels for end-user consumption.

In India, significant strides have been made through programs like the Deen Dayal Upadhyaya Gram Jyoti Yojana (DDUGJY) and the Saubhagya scheme. These initiatives aim to provide continuous power supply to rural households and have led to the electrification of over 5.97 lakh villages by 2022. The government’s commitment to universal electrification has created a substantial demand for distribution transformers to support the expanding grid infrastructure.

Similarly, the Ujwal DISCOM Assurance Yojana (UDAY) focuses on improving the financial health of power distribution companies, enabling them to invest in infrastructure upgrades, including the procurement of modern distribution transformers. These efforts are crucial in reducing technical losses and enhancing the efficiency of power distribution networks.

The integration of renewable energy sources into the grid further amplifies the need for advanced distribution transformers. As countries aim to increase their renewable energy capacity, the variability and decentralized nature of sources like solar and wind power require transformers capable of handling fluctuating loads and bidirectional power flows.

In the United States, the National Renewable Energy Laboratory (NREL) has highlighted the aging infrastructure, noting that approximately 55% of distribution transformers are over 33 years old. To meet future electricity demand and accommodate renewable energy integration, the NREL estimates that distribution transformer capacity needs to increase by 160% to 260% by 2050 compared to 2021 levels.

Restraints

Rising Raw Material Costs and Supply Chain Constraints

One of the major forces holding back growth in the distribution transformer market is the steep rise in raw material costs—especially for steel and copper—combined with supply chain bottlenecks. These two challenges are intertwined, creating significant pressure on manufacturers and utilities.

Over the past few years, steel and copper prices have surged due to global demand pressures and trade tensions. For example, in the United States, tariffs imposed—such as 25% on steel and aluminium and 10% on Chinese imports—have escalated transformer production costs. According to industry estimates, transformer prices have risen by 70–100% since January 2020 purely due to rising material costs. When additional tariffs are taken into account, prices may climb another 8–9%, affecting both manufacturers and end-users.

Additionally, the complex logistical process for components has led to longer lead times. In the UK, lead times for lower-voltage transformers have doubled over the decade, while high-voltage units may require up to four years for delivery. This delay directly hinders electrification projects and grid expansions, making it challenging for utilities to meet energy targets on schedule.

Energy-intensive industries like food and beverage manufacturing feel similar pain. In the U.S., this industry accounts for roughly 6% of total industrial emissions, reflecting heavy energy use influenced by transformer costs and electricity prices. As energy becomes more expensive, these manufacturers face higher operation costs, which can dampen new investment and reduce demand for new transformers.

Opportunity

Smart Grid Modernization and Renewable Energy Integration

A significant growth opportunity in the distribution transformer market lies in the modernization of power grids and the integration of renewable energy sources. As countries strive to enhance energy efficiency and reduce carbon emissions, the demand for advanced distribution transformers capable of handling variable power inputs from renewable sources is increasing.

In the United States, the National Renewable Energy Laboratory (NREL) estimates that distribution transformer capacity may need to increase by 160% to 260% by 2050 compared to 2021 levels to meet the growing energy demands from residential, commercial, industrial, and transportation sectors . This surge is largely driven by the aging transformer fleet and the electrification of various sectors.

Similarly, in India, government initiatives such as the Revamped Distribution Sector Scheme (RDSS) aim to improve the operational efficiency and financial sustainability of distribution companies. The scheme includes provisions for the modernization of distribution infrastructure, including the deployment of smart meters and the upgradation of distribution transformers to accommodate renewable energy integration .

The food and beverage industry, being energy-intensive, also contributes to this demand. In the U.S., this sector accounts for approximately 6% of total industrial emissions, reflecting heavy energy use influenced by transformer costs and electricity prices. As energy becomes more expensive, these manufacturers face higher operation costs, which can dampen new investment and reduce demand for new transformers.

Trends

Smart Transformers: A Key Trend in Modernizing Power Distribution

A significant trend shaping the distribution transformer market is the integration of smart grid technologies. This evolution is driven by the need for more efficient, reliable, and flexible power distribution systems, especially in the face of growing urbanization and the proliferation of renewable energy sources.

Smart distribution transformers are equipped with advanced features such as remote monitoring, automated fault detection, and real-time data analytics. These capabilities enable utilities to proactively manage the electrical grid, swiftly respond to outages, and optimize load distribution. For instance, the U.S. Department of Energy’s Smart Grid Investment Grant program has allocated substantial funding to support the deployment of advanced metering infrastructure and distribution automation technologies. Such programs underscore the commitment to enhancing grid resilience and accommodating the dynamic nature of electricity demand and supply.

The adoption of smart grid solutions is further bolstered by governmental initiatives aimed at modernizing electrical infrastructure. In the United States, for example, the Department of Energy’s Smart Grid Investment Grant program has allocated substantial funding to support the deployment of advanced metering infrastructure and distribution automation technologies. Such programs underscore the commitment to enhancing grid resilience and accommodating the dynamic nature of electricity demand and supply.

Regional Analysis

In 2024, the Asia-Pacific (APAC) region solidified its position as the leading market for distribution transformers, commanding a substantial 45.6% share, equivalent to approximately USD 11.9 billion. This dominance is driven by rapid urbanization, industrial expansion, and significant investments in renewable energy infrastructure across key economies such as China, India, and Southeast Asian nations.

Technological advancements, particularly the adoption of smart transformers equipped with IoT sensors and real-time analytics, are gaining traction in APAC. These innovations enable predictive maintenance and efficient energy management, aligning with the region’s goals for energy efficiency and sustainability.

The distribution transformer market is underpinned by its rapid economic growth, infrastructural investments, and commitment to renewable energy integration. With continued focus on grid modernization and technological innovation, the region is poised to maintain its leading position in the global market.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

ABB remains a leading force in the distribution transformer market, known for its innovation and global reach. The company offers a wide range of oil-immersed and dry-type transformers catering to utility, industrial, and renewable applications. In 2024, ABB continued to expand its smart transformer portfolio with a focus on grid reliability and digital monitoring features. Strong presence in APAC and Europe, along with investments in sustainable transformer production, has reinforced ABB’s market position amid growing electrification and renewable integration initiatives.

Brush Electrical Machines Ltd. has built its reputation on high-quality engineering and customized transformer solutions for power utilities and industrial sectors. In 2024, the company focused on supplying medium-power distribution transformers to support modern grid upgrades and decentralized energy systems. With a manufacturing base in the UK and exports across Europe and the Middle East, Brush leverages its technical expertise and service reliability to maintain competitiveness in traditional and renewable energy markets undergoing transition.

Celme S.r.l., headquartered in Italy, specializes in oil-immersed power and distribution transformers. In 2024, Celme reinforced its presence in European and North African markets by offering tailored transformer units for solar parks and utility distribution networks. The company is recognized for its high-efficiency products and fast delivery times. With growing demand from grid modernization and electrification efforts in emerging markets, Celme has prioritized R&D in eco-efficient and compact transformer design solutions.

Top Key Players in the Market

- ABB

- Brush Electrical Machines Ltd.

- Celme S.r.l.

- CG Power and Industrial Solution Ltd.

- Crompton Greaves Ltd.

- Eaton Corporation PLc.

- Elsewedy Electric

- Emerson Electric Co.

- Eremu SA

- ERMCO

- Fuji Electric Co., Ltd.

- General Electric

- Hammond Power Solutions

- HD HYUNDAI ELECTRIC CO., LTD.

- Hitachi Energy Ltd.

- Lemi Trafo JSc

- Mitsubishi Electric Corporation

- Schneider Electric

- Siemens Energy

- Toshiba Energy Systems & Solutions Corporation

Recent Developments

In 2024, Celme S.r.l. product range includes units with capacities up to 40,000 kVA, designed for applications such as photovoltaic systems, wind energy, and hydroelectric plants.

In March 2025, CG Power and Industrial Solutions Ltd. initiative aims to increase CG Power’s total transformer manufacturing capacity to 85,000 MVA, catering to both domestic and international markets . Additionally, the company enhanced its existing Malanpur unit’s capacity from 25,000 MVA to 35,000 MVA, with plans to reach 40,000 MVA.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 26.1 Bn |

| Forecast Revenue (2034) | USD 51.3 Bn |

| CAGR (2025-2034) | 7% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Insulation (Gas, Oil, Solid, Air, Others), By Phase (Single, Three), By Rating (≤2.5 MVA, 2.6 MVA to 10 MVA, > 10 MVA), By Mounting (Pad, Pole, Others), By Application (Utility, Residential and Commercial, Industrial) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | ABB, Brush Electrical Machines Ltd., Celme S.r.l., CG Power and Industrial Solution Ltd., Crompton Greaves Ltd., Eaton Corporation PLc., Elsewedy Electric, Emerson Electric Co., Eremu SA, ERMCO, Fuji Electric Co., Ltd., General Electric, Hammond Power Solutions, HD HYUNDAI ELECTRIC CO., LTD., Hitachi Energy Ltd., Lemi Trafo JSc, Mitsubishi Electric Corporation, Schneider Electric, Siemens Energy, Toshiba Energy Systems & Solutions Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |