Quick Navigation

Report Overview

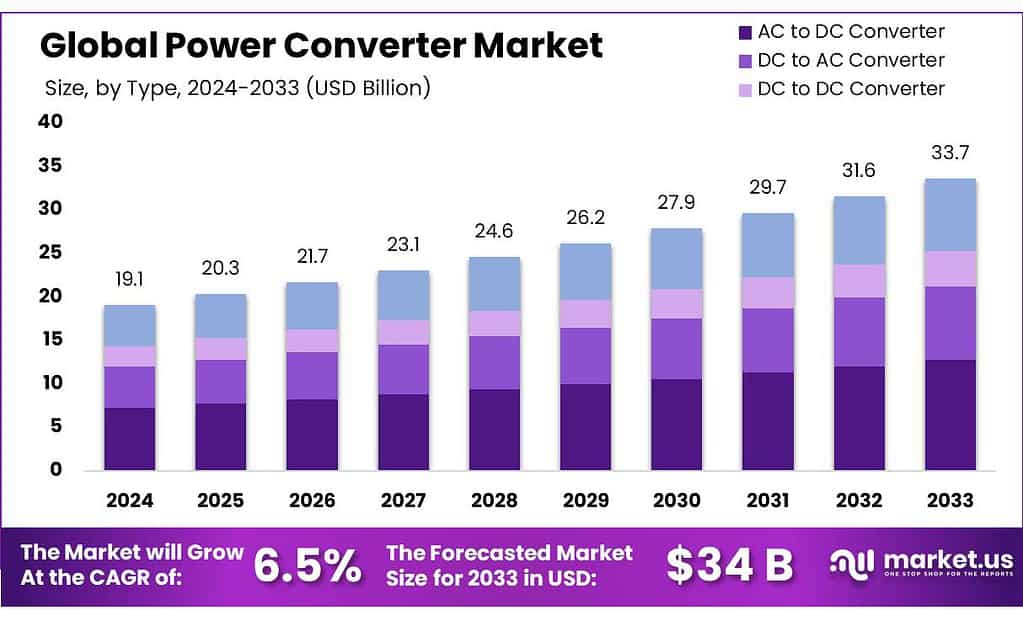

The Global Power Converter Market size is expected to be worth around USD 33.7 Bn by 2033, from USD 19.1 Bn in 2023, growing at a CAGR of 6.5% during the forecast period from 2024 to 2033.

A power converter is an electrical device that changes the form of an electric power source to suit a specific type of load or application. It can alter the voltage, current, or frequency of the power source, and comes in various types such as AC-to-DC, DC-to-AC, DC-to-DC, and AC-to-AC converters.

This revision allows the Canadian government to set stringent energy efficiency standards for electronic devices, particularly focusing on reducing standby power consumption. Historically, standby power has been a significant but often overlooked component of household energy use.

It’s estimated that approximately 40% of the electricity consumed by home electronics is used while these devices are off or in standby mode, contributing up to 10% of an average household’s electricity costs.

The new regulatory standards aim to decrease standby power consumption to between 2-4 watts by 2010 and further reduce it to 1-2 watts by 2013 for certain devices. This initiative is expected to mitigate unnecessary energy waste and curb rising domestic energy expenditures.

These modifications include lowering the capacity threshold for QFs from 20 megawatts to just 5 megawatts. This change is significant as it affects small power producers and co-generators, altering the landscape for smaller scale renewable energy projects and potentially enhancing market participation by making it easier for smaller installations to qualify for beneficial rates and terms.

On a global scale, investment in renewable energy infrastructure is witnessing significant growth. According to the International Energy Agency (IEA), global investments in renewable energy technologies soared to around $500 billion in 2022.

Key Takeaways

- Power Converter Market size is expected to be worth around USD 33.7 Bn by 2033, from USD 19.1 Bn in 2023, growing at a CAGR of 6.5%.

- AC to DC converter segment held a dominant market position, capturing more than a 38.3% share.

- 10-100 kW segment held a dominant market position, capturing more than a 34.5% share.

- Forced Air Cooling held a dominant market position, capturing more than a 48.2% share.

- Half-Bridge topology held a dominant market position, capturing more than a 42.4% share.

- Renewable Energy held a dominant market position, capturing more than a 29.2% share.

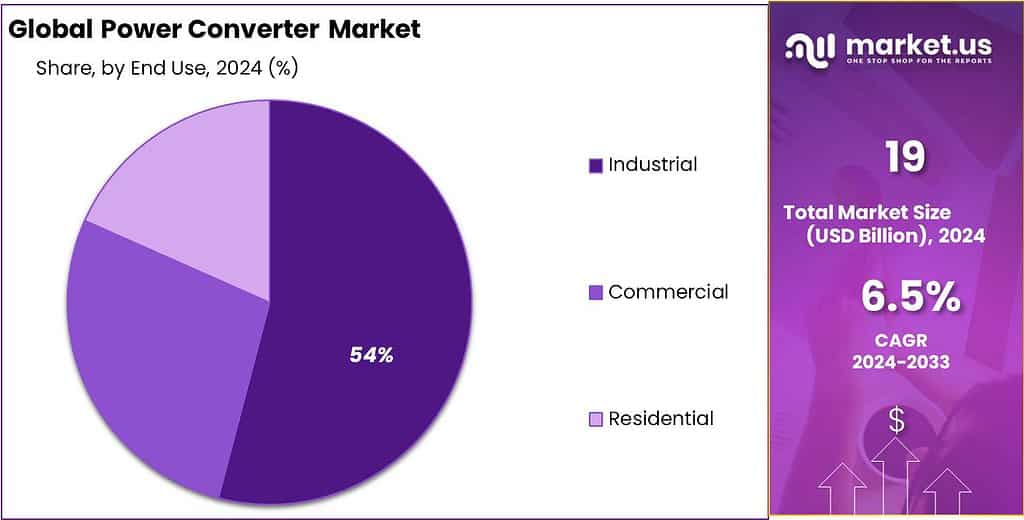

- Industrial segment held a dominant market position, capturing more than a 53.3% share.

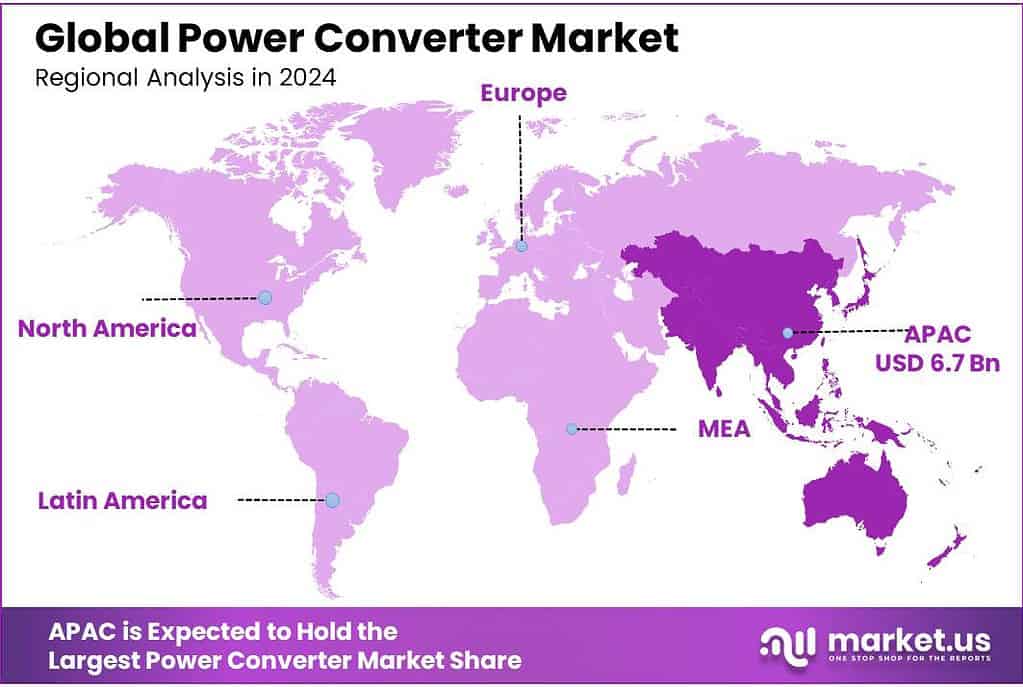

- Asia Pacific (APAC) region dominates with a commanding 35% market share, valued at USD 6.7 billion.

By Type

In 2023, the AC to DC converter segment held a dominant market position, capturing more than a 38.3% share. This segment benefits primarily from its widespread application in various electronic devices where these converters are essential for converting mains AC voltage to usable DC power. Their usage spans across consumer electronics, automotive sectors, and industrial settings, reflecting a robust demand driven by the expansion of these sectors.

The DC to AC converter market also shows considerable growth potential. These converters are pivotal in renewable energy systems, especially for converting battery-stored DC power back to AC, making them integral in solar power installations and home energy systems. The increasing shift toward renewable energy sources is likely to propel the demand for DC to AC converters.

Further, the DC to DC converter market is critical in spaces where different DC voltages are required from a single power source. They are vital in portable and battery-operated devices, such as laptops and smartphones, which require reliable power management systems to extend battery life and optimize device performance.

The AC to AC converter market is characterized by its use in applications requiring the conversion of one form of AC voltage to another. This includes uses in light dimmers, motor controls, and other industrial applications where precise voltage control is necessary for operational efficiency and equipment safety.

By Power Range

In 2023, the 10-100 kW segment held a dominant market position, capturing more than a 34.5% share. This range is extensively used in industrial and commercial applications, where medium-scale power conversion is essential for operational processes. The robust demand in this segment is driven by its critical role in industries such as manufacturing, where reliable power conversion affects production efficiency and safety.

For power converters below 1 kW, the market remains buoyant, driven by consumer electronics and small-scale energy applications. These devices are fundamental in everyday products such as smartphones, laptops, and household appliances, where low power conversion is required for functionality and safety.

The 1-10 kW segment also plays a pivotal role, particularly in smaller industrial and renewable energy implementations. These converters are crucial for small to medium enterprises that require efficient power management systems to enhance operational reliability and cost-effectiveness.

Above 100 kW converters are essential in heavy industrial settings and large-scale renewable energy systems. This segment benefits from the growing industrialization and the increasing adoption of green energy solutions, where high power output is necessary for large machinery and during peak energy production periods.

By Cooling Type

In 2023, Forced Air Cooling held a dominant market position, capturing more than a 48.2% share. This method is favored for its effectiveness and efficiency in dissipating heat in various electronic devices and machinery. The widespread adoption is primarily due to its cost-effectiveness and ease of implementation in sectors ranging from automotive to industrial electronics, which require robust cooling mechanisms to ensure device longevity and safety.

Natural Cooling also represents a significant portion of the market, particularly valued in applications where noise reduction and energy savings are crucial. This passive cooling method is preferred in residential and light commercial applications, where the environmental impact and energy consumption can be minimized.

Liquid Cooling, while less common, is increasingly being recognized for its superior cooling efficiency, especially in high-power and high-performance applications such as data centers and high-speed computing systems. This technology is gaining traction due to its ability to manage higher heat loads, offering a reliable solution for advanced electronics and large-scale industrial equipment.

By Topology

In 2023, the Half-Bridge topology held a dominant market position, capturing more than a 42.4% share. This configuration is widely favored for its balance between efficiency and cost, making it suitable for a variety of medium-power applications. It is commonly employed in DC to DC converters and inverter circuits, which are integral to consumer electronics and renewable energy systems, underscoring its broad market appeal.

The Full-Bridge topology also plays a crucial role, especially in applications requiring high power handling and efficiency. Its ability to handle higher voltages and currents makes it ideal for industrial and heavy-duty applications such as electric vehicle chargers and large-scale inverters, highlighting its importance in sectors pushing towards more robust power solutions.

The Push-Pull topology finds its niche in applications where size and efficiency are critical. This topology is particularly valued in space-constrained environments such as telecommunications equipment and portable electronics, where it provides an efficient solution for transforming voltages while minimizing physical footprint and energy loss.

By Application

In 2023, Renewable Energy held a dominant market position, capturing more than a 29.2% share. This segment benefits from the global shift towards sustainable energy sources, with power converters playing a crucial role in optimizing energy capture, conversion, and storage from renewable sources like solar and wind. The demand is fueled by both governmental incentives and a growing societal push for greener solutions.

Consumer Electronics is another significant segment, driven by the pervasive use of electronic devices such as smartphones, tablets, and personal computers. Power converters are essential in these devices to manage power supply efficiently, ensuring safety and enhancing battery life, which is critical for consumer satisfaction and device reliability.

Medical Equipment also relies heavily on power converters to ensure precise and reliable power management for critical health technology. These devices are crucial in everything from patient monitoring systems to advanced diagnostic machines, where stable and safe power supply is non-negotiable.

The Electric Vehicle segment is rapidly expanding, with power converters critical for managing the flow of electricity between batteries and motors. The growth in this segment is propelled by the increase in electric vehicle adoption, driven by environmental concerns and technological advancements in automotive industries.

By End-Use Industry

Key Market Segments

By Type

- AC to DC Converter

- DC to AC Converter

- DC to DC Converter

- AC to AC Convertor

By Power Range

- Below 1 kW

- 1-10 kW

- 10-100 kW

- Above 100 kW

By Cooling Type

- Natural Cooling

- Forced Air Cooling

- Liquid Cooling

By Topology

- Half-Bridge

- Full-Bridge

- Push-Pull

By Application

- Renewable Energy

- Consumer Electronics

- Medical Equipment

- Electric Vehicle

- Others

By End-Use Industry

- Residential

- Commercial

- Industrial

Driving Factors

Supportive Global Policies and Government Initiatives: In 2023, government policies played a pivotal role in the expansion of renewable power capacity, particularly in countries like China, the United States, and the European Union.

This supportive policy environment led to a nearly 50% increase in global renewable electricity capacity additions, reaching an estimated 507 gigawatts (GW). Key initiatives include the United States’ Inflation Reduction Act and the European Union’s continuous policy incentives aimed at decarbonizing energy systems and enhancing energy security.

Economic Incentives and Financial Support: The economic attractiveness of renewable technologies such as solar PV and wind, coupled with low-cost financing and government incentives, particularly in China, has driven substantial investment and installation of renewable power systems.

China’s renewable capacity growth, for example, is expected to triple in the next five years compared to the previous five, supported by its 14th Five-Year Plan and targets for Net Zero by 2060.

Rapid Technological Advancements and Cost Reductions: Technological advancements have significantly reduced the cost of renewable power technologies, making them more competitive than fossil fuel alternatives.

In 2023, an estimated 96% of newly installed, utility-scale solar PV and onshore wind capacity offered lower generation costs compared to new coal and natural gas plants. This cost competitiveness is expected to drive further adoption and installation of renewable energy systems globally.

Restraining Factors

Policy and Investment Gaps

A significant restraint on the power converter market, especially impacting the renewable energy sector, is the lack of adequate investment in grid infrastructure. The rapid growth in renewable capacity, which has seen renewable power additions soar, requires equally robust grid systems to handle the increased load and ensure reliable energy distribution.

However, the investment in grid infrastructure has not kept pace with the rate of renewable installations, causing a bottleneck that hampers further expansion of renewables and by extension, power converter deployments.

Permitting Delays and Administrative Barriers

Another critical factor is the cumbersome administrative and permitting processes that significantly delay renewable energy projects. For instance, the time required to secure permits for solar and wind projects can extend up to several years, depending on the region. These delays not only slow down the implementation of renewable projects but also affect the deployment of the necessary power converters that are integral to these projects.

Macroeconomic and Financial Challenges

The power converter market is also restrained by broader macroeconomic challenges that affect the renewable energy sector. Higher interest rates and inflation have increased the costs of financing and equipment, making renewable projects more expensive and less attractive to investors. This financial strain is particularly pronounced in emerging and developing economies where the cost of capital is significantly higher, further complicating efforts to scale up renewable installations and the power converters needed for them.

Growth Opportunity

Surge in Global Renewable Capacity Additions: The global renewable electricity capacity saw a dramatic increase in 2023, with an estimated 507 GW added—almost 50% higher than the previous year.

This unprecedented growth is expected to continue, driven by significant policy support in over 130 countries and substantial increases in the solar PV and wind sectors, which now represent 96% of new additions. This surge in renewable installations presents a substantial opportunity for the power converter market, as these technologies require efficient conversion systems to manage and integrate the generated power into the grid effectively.

Policy Incentives and Economic Factors: Nations such as China, the United States, and countries in the European Union are significantly investing in renewable energy, backed by strong government policies like China’s 14th Five-Year Plan and the U.S. Inflation Reduction Act. These policies not only support existing technology but also encourage the development of emerging renewable sectors, thus expanding the market for power converters needed to handle diverse energy sources and enhance grid integration.

Cost Competitiveness and Technological Advancements: The cost of generating power through solar PV and wind has become competitive with, or even cheaper than, fossil fuels in many regions. This cost-effectiveness, coupled with technological advancements in power conversion technologies, is likely to increase the demand for advanced power converters that can efficiently manage the variability and integration challenges associated with large-scale renewable outputs.

Latest Trends

Trend Towards Higher System Voltages

One of the most significant trends in the power converter market is the shift towards higher system voltages across various applications, including renewable energy systems and electric vehicles (EVs). This move is driven by the need to handle higher power levels efficiently. For instance, in the photovoltaic (PV) sector, the transition from traditional 1000 V systems to 1500 V systems has become more common. This change aims to reduce balance-of-system costs and enhance overall efficiency. Similarly, in the EV market, there is a growing adoption of 800-V systems to support faster charging capabilities.

Increasing Power Converter Power Levels

There’s also a trend towards larger installation sizes in power converter applications, which necessitates higher power levels. For example, string PV inverters now reach up to 385 kW, and central PV inverters can handle up to 6.8 MW. Wind turbine converters and Battery Energy Storage System (BESS) power conversion units are also seeing increases in their capacity, reflecting this trend towards higher power requirements.

Growth in Non-Automotive Applications

While the automotive sector continues to be a significant player in the power converter market, there is notable growth in non-automotive applications such as stationary battery energy storage systems, industrial motors, and EV DC charging stations. This diversification is spurred by different industry requirements such as converter density, reliability, and nominal voltage, creating new opportunities across various sectors.

Regional Analysis

In the power converter market, the Asia Pacific (APAC) region dominates with a commanding 35% market share, valued at USD 6.7 billion. This leadership is primarily due to the substantial investments in renewable energy projects, particularly in China and India, where government initiatives support large-scale solar and wind installations. The region’s focus on enhancing its industrial automation capabilities also drives demand for sophisticated power conversion technologies.

North America, characterized by robust technological advancements and a significant push towards renewable energy, follows APAC in market prominence. The region’s commitment to reducing carbon emissions through policy frameworks and incentives, such as tax rebates for solar energy, propels the development and uptake of high-efficiency power converters.

Europe stands out for its stringent energy regulations and aggressive targets for reducing greenhouse gas emissions, fostering a strong market for power converters across renewable and industrial applications. The European Union’s Green Deal and the substantial funding for transitioning to a low-carbon economy contribute to the region’s market growth.

The Middle East and Africa (MEA) region, though smaller in comparison, is experiencing rapid growth due to the increasing adoption of solar energy projects, especially in Gulf Cooperation Council (GCC) countries looking to diversify energy resources. Africa’s focus on improving energy access through off-grid renewable energy solutions also contributes to the demand for power converters.

Latin America shows promising growth driven by renewable energy developments, particularly in countries like Brazil and Chile, which are harnessing vast solar and wind resources. Government policies supporting renewable energy infrastructure are pivotal in stimulating the power converter market in this region.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The power converter market is characterized by the presence of several key global players, each contributing to the technological advancements and market expansion in various industries. Companies like ABB, Siemens, and Mitsubishi Electric are notable for their extensive portfolios that span a range of power electronic products, including converters that are integral to renewable energy systems, industrial automation, and more.

These companies have a significant R&D focus, driving innovations that enhance the efficiency and functionality of power conversion technologies.

On the other hand, firms such as GE, Schneider Electric, and Rockwell Automation are recognized for their strong market presence across multiple regions, underpinned by robust distribution networks and comprehensive service offerings.

These players have been pivotal in developing integrated solutions that cater to the evolving needs of the energy sector, particularly as industries shift towards sustainable practices. Schneider Electric and Rockwell Automation, for example, emphasize energy management and industrial automation solutions that optimize power usage and improve system reliability.

Smaller specialized players like Vicor, Vishay, and Wolfspeed also play critical roles, particularly in niche applications where high performance and reliability are paramount. Vicor focuses on high-efficiency power modules that serve demanding applications in the military, aerospace, and computing sectors.

Vishay and Wolfspeed have carved out unique positions with their offerings in semiconductor solutions and silicon carbide (SiC) materials, respectively, addressing the needs for higher efficiencies and compact designs in power converters. Together, these companies not only propel technological innovation but also intensify competition in the power converter market, fostering developments that might redefine future power conversion standards and practices.

Top Key Players in the Market

- ABB

- Honeywell

- ParkerHannifin

- Schneider Electric

- Toshiba

- Vicor

- Vishay

- Rockwell Automation

- GE

- Siemens

- Emerson Electric

- TDK

- Mitsubishi Electric

- Phoenix Contact

- Wolfspeed

Recent Developments

In 2023 ABB’s commitment to sustainability is also prominent, expected to avoid 74 megatons of CO2 emissions over their lifetime. This is part of a broader goal to help customers avoid 600 megatons of GHG emissions from 2022 to 2030.

In 2023 Honeywell’s financial performance in 2023 reflected the effectiveness of these strategies. The company reported a 3% increase in sales, with a more significant 6% growth on an organic basis, underscoring its resilience and ability to navigate economic challenges effectively

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 19.1 Bn |

| Forecast Revenue (2033) | USD 33.7 Bn |

| CAGR (2024-2033) | 6.5% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type(AC to DC Converter, DC to AC Converter, DC to DC Converter, AC to AC Convertor), By Power Range(Below 1 kW, 1-10 kW, 10-100 kW, Above 100 kW), By Cooling Type(Natural Cooling, Forced Air Cooling, Liquid Cooling), By Topology(Half-Bridge, Full-Bridge, Push-Pull), By Application(Renewable Energy, Consumer Electronics, Medical Equipment, Electric Vehicle, Others), By End-Use Industry(Residential, Commercial, Industrial) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | ABB, Honeywell, ParkerHannifin, Schneider Electric, Toshiba, Vicor, Vishay, Rockwell Automation, GE, Siemens, Emerson Electric, TDK, Mitsubishi Electric, Phoenix Contact, Wolfspeed |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |