Quick Navigation

Report Overview

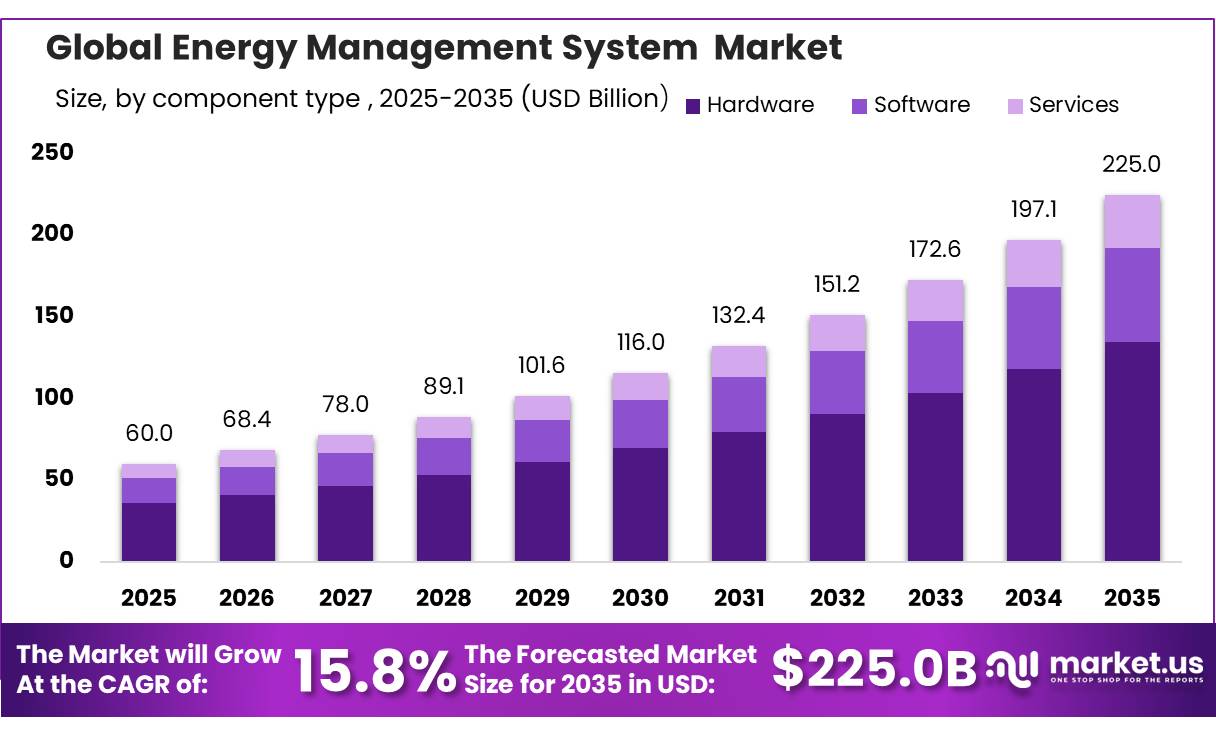

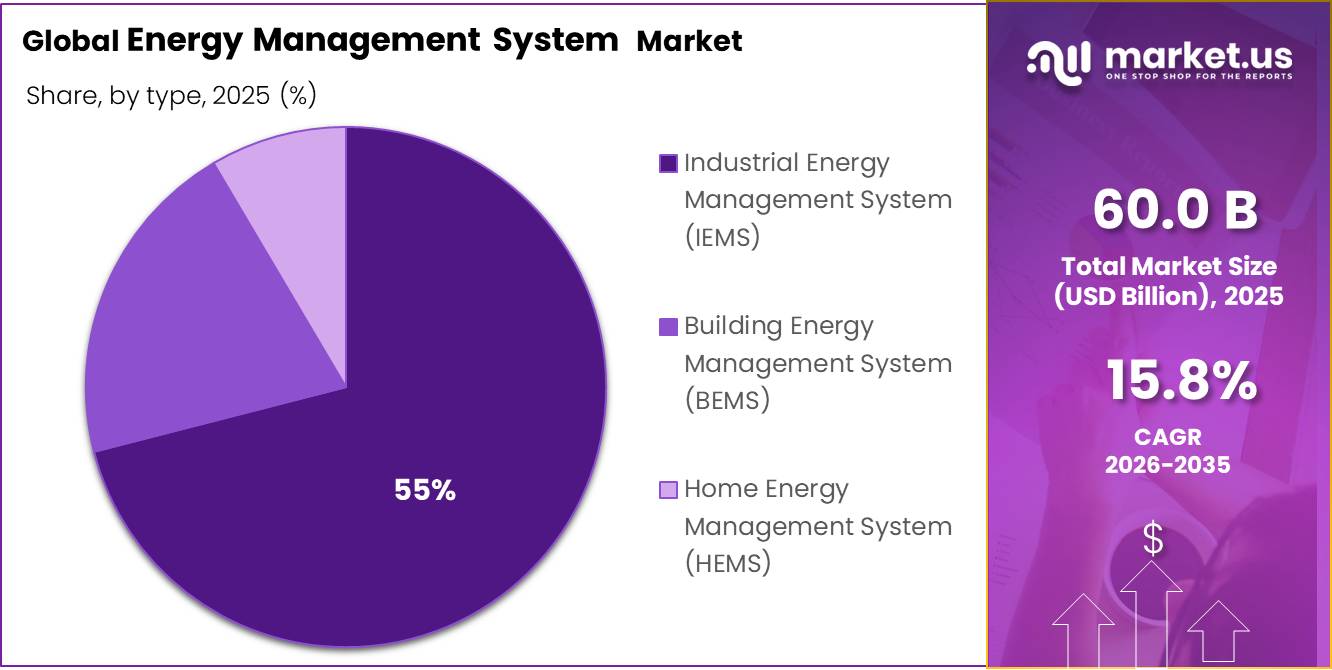

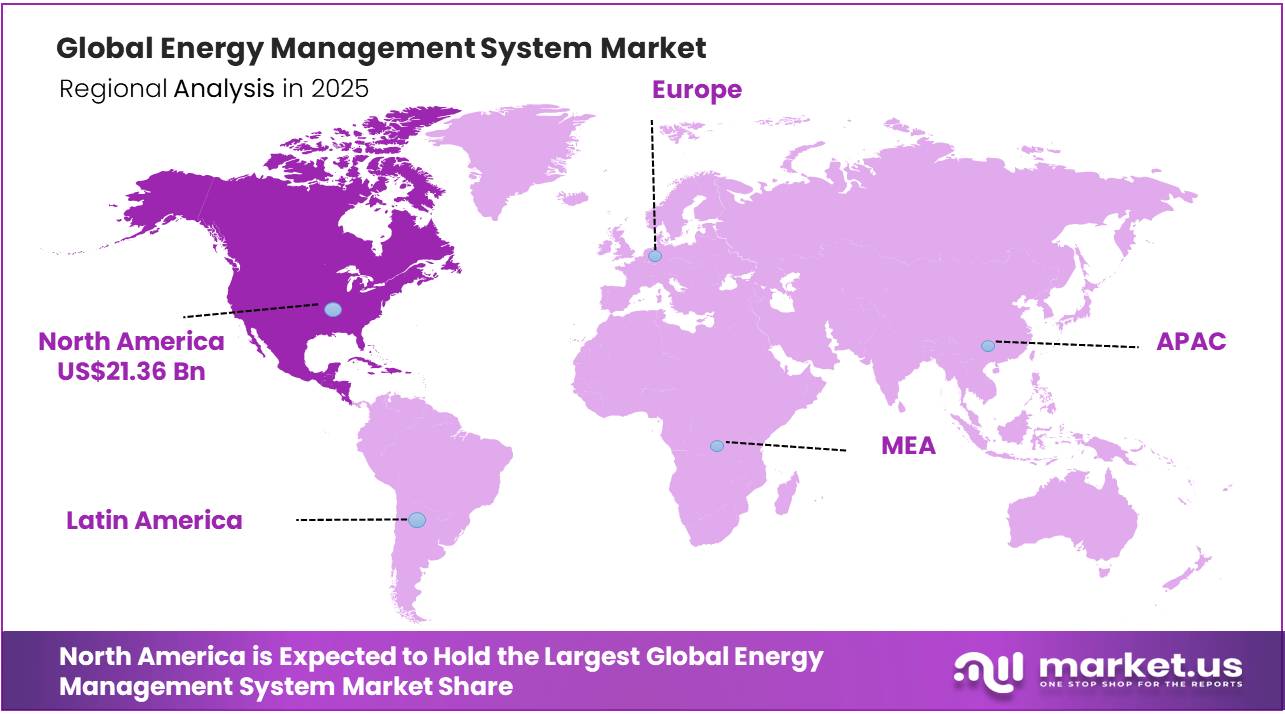

In 2025, the Global Energy Management System Market was valued at USD 60.0 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 15.8%, reaching about USD 225.0 billion by 2035. North America held a dominant Market position, capturing more than a 35.6% share, holding USD 21.36 Billion revenue.

The global energy landscape is undergoing a structural shift, compelling industries across sectors to adopt systematic approaches to monitoring, controlling, and optimizing energy consumption. Global electricity consumption rose by nearly 1,100 terawatt-hours (TWh) in 2024 the largest annual increase on record outside of post-recession rebound years driven by rising cooling demand, expanding data centre infrastructure, and accelerating industrial electrification.

Key Takeaways

- The global Energy Management System (EMS) market was valued at USD 60.0 billion in 2025.

- The global market is projected to grow at a CAGR of 15.8% and is estimated to reach USD 225.0 billion by 2035.

- On the basis of component, the hardware segment dominated the market, constituting 60.0% of the total market share,

- Based on the type, the Industrial Energy Management System (IEMS) dominated the EMS market, with a substantial market share of 71.0%,

- Based on the deployment mode, the cloud-based segment led the market, comprising 50.0% of the total market.

- Among the end-use industries, the manufacturing sector held a major share in the EMS market, accounting for 31.0% of the total market share.

- In 2024, North America was among the most dominant regions in the EMS market accounting for 35.6%.

Against this backdrop, Energy Management Systems have emerged as critical operational tools enabling enterprises to systematically reduce energy intensity, improve cost efficiency, and meet increasingly stringent regulatory compliance obligations. Combined public and private investment in energy efficiency across end-use sectors is expected to reach approximately USD 660 billion in 2024 nearly 50% higher than 2019 levels underscoring the scale of institutional commitment to efficiency-driven infrastructure.

The recast EU Energy Efficiency Directive sets a binding Union-wide target of an 11.7% reduction in energy consumption by 2030 compared to the 2020 reference scenario, embedding the “energy efficiency first” principle across policymaking, investment, and infrastructure planning (European Commission, Energy Efficiency Directive, October 2023. With over 250 new or updated energy efficiency policies introduced in 2025 across countries accounting for 85% of global energy demand, policymaking momentum continues to accelerate, reinforcing long-term EMS deployment across industrial, commercial, and public-sector verticals

Energy Management System Market Segment

By Component Analysis

Hardware Segment Represents the Dominant Segment in the EMS Market

The hardware segment dominates the global Energy Management System market, accounting for 60.0% of total market share, owing to its foundational and indispensable role in enabling the physical infrastructure required for effective energy monitoring, data collection, and real-time consumption management in industrial, commercial, and residential settings. EMS hardware includes a wide range of physical devices and equipment, such as smart meters, sensors, controllers, data loggers, display units, communication modules, and power monitoring devices, which together form the operational foundation of any comprehensive energy management system deployment.

- In February 2025, Honeywell International’s Honeywell Building Management System platform has been used to deploy advanced EMS hardware infrastructure, such as smart sensors, controllers, and power monitoring devices, in large-scale manufacturing and commercial building facilities around the world.

By Type Analysis

Industrial Energy Management System (IEMS) Represents the Dominant Segment in the Market

The Industrial Energy Management System (IEMS) dominates the global EMS market, accounting for 71.0% of total market share due to its widespread deployment in large-scale manufacturing facilities, power and energy plants, oil and gas operations, and heavy industrial environments around the world. IEMS solutions are specifically designed to meet the complex and high-volume energy consumption demands of industrial operations, with real-time monitoring, automated demand response, and advanced data analytics capabilities that allow organizations to achieve significant and measurable energy savings on a large scale.

- In April 2025, Siemens AG deployed its Industrial Energy Management System across multiple large-scale manufacturing facilities around the world, enabling real-time energy monitoring and automated demand response to help clients achieve annual energy savings of up to 30% demonstrating IEMS’s dominant role in driving measurable energy efficiency outcomes across industrial environments.

By Deployment Mode Analysis

Cloud-Based Deployment Holds a Major Share of the EMS Market

The cloud-based deployment mode dominates the global EMS market, accounting for 50.0% of the total market share, owing to its superior flexibility, scalability, cost efficiency, and remote accessibility advantages over traditional on-premises deployment models. Cloud-based EMS platforms allow organizations to monitor, manage, and optimize energy consumption across multiple facilities and geographies using a centralized digital interface, eliminating the need for costly on-site hardware infrastructure and lowering overall system implementation and maintenance costs.

The increasing adoption of cloud computing across industries, combined with the rapid expansion of high-speed internet connectivity and IoT device integration, has hastened the transition of businesses of all sizes to cloud-based energy management solutions.

By End-Use Industry

Manufacturing Sector Holds a Major Share in the EMS Market

When we think about where energy management systems matter most, the manufacturing sector stands out clearly at the top. Accounting for 31.0% of the total EMS market share, manufacturing facilities are among the biggest energy consumers in the world and for good reason. From automotive assembly lines and chemical processing plants to electronics production and consumer goods factories, these facilities run heavy machinery, complex HVAC systems, extensive lighting infrastructure, and continuous production lines around the clock.

Manufacturing environments generate enormous amounts of energy data every single day, and without the right system in place, most of it goes unnoticed and unused. Energy Management Systems change that completely by bringing order and clarity to this overwhelming flow of information. Plant operators can finally see exactly where energy is being wasted, adjust production schedules to take advantage of cheaper off-peak electricity rates, and automate responses to shifting energy demands all in real time.

Key Market Segments

By Component

- Hardware

- Software

- Services

By Type

- Industrial Energy Management System (IEMS)

- Building Energy Management System (BEMS)

- Home Energy Management System (HEMS)

By Deployment Mode

- On-Premises

- Cloud-Based

- Hybrid Cloud

By End-Use Industry

- Manufacturing

- Power & Energy / Utilities

- Telecom & IT

- Commercial & Residential Buildings

- Healthcare & Hospitals

- Food & Beverage

- Others

Drivers

EU building-efficiency mandates driving EMS retrofits

The strongest near-term demand driver for EMS is the regulatory conversion of building efficiency from a discretionary upgrade into a compliance-led capex category across Europe. The recast EPBD requires member states to transpose the directive by 29 May 2026, introduces minimum energy performance standards from 2026, mandates zero-emission public buildings from 2028 and all new buildings from 2030, and targets the worst-performing 16% of non-residential buildings by 2030 and 26% by 2033 for renovation action.

These deadlines directly favor EMS adoption because building owners cannot achieve recurring monitoring, optimization, and evidence-based compliance with static BMS alone; they increasingly need integrated metering, automated controls, demand response, and energy analytics. In business-model terms, this shifts EMS procurement from one-off facility automation to multi-year software-plus-services contracts with audit support, retrofit integration, and recurring optimization layers. The modeled CAGR uplift of +2.0 percentage points reflects a wave of compliance-driven retrofits in commercial, public, and logistics buildings across the EU, where EMS becomes part of the minimum digital stack for renovation roadmaps and zero-emission building readiness.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU building-efficiency mandates driving EMS retrofits | +2.0% | EU core, UK spill-over | Short term (≤ 2 years) |

| Smart-grid and AMI expansion lifting utility EMS demand | +1.8% | North America core, EU, APAC smart-grid corridors | Medium term (2-4 years) |

| DER, solar, storage, and EV orchestration needs | +1.7% | North America, EU, China, Japan, Australia | Medium term (2-4 years) |

| Industrial energy-cost pressure accelerating plant EMS adoption | +1.5% | Europe core, North America, India, China | Short term (≤ 2 years) |

| AI analytics and cloud control improving EMS ROI | +1.3% | North America core, EU, advanced APAC | Medium term (2-4 years) |

| Carbon reporting and whole-life compliance digitization | +1.2% | EU core, North America selective, global multinationals | Long term (≥ 4 years) |

Restraints

High upfront integration cost

The clearest near-term restraint on EMS adoption remains the capital and integration burden at the site level, especially for SMEs and mid-market portfolios that lack internal energy teams and face competing capex priorities. Typical EMS deployments for SMEs in 2026 require around US$20,000–80,000 of upfront integration and metering capex per site plus US$4,000–25,000 in annual subscription opex, and even well-executed projects that can deliver 10%–25% electricity savings and an additional 5%–10% bill reduction from load shifting still often present simple payback periods of roughly 2.5–4.5 years.

That payback is commercially acceptable in high-tariff environments, but many buyers still defer projects because the cost lands before the savings, metering upgrades must often be bundled with controls and software, and multisite deployments can scale into seven-figure budget lines. This restraint deducts an estimated 1.6 percentage points from baseline CAGR because EMS vendors continue to face higher customer-acquisition friction, slower procurement cycles, and lower conversion among cost-sensitive buildings, light industry, and SME operators despite the underlying efficiency case remaining strong.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront integration cost | -1.6% | North America, EU, SME-heavy APAC | Short term (≤ 2 years) |

| Legacy-system interoperability gaps | -1.4% | EU core, North America core, mature APAC buildings | Medium term (2-4 years) |

| Smart-meter rollout delays | -1.2% | India core, emerging APAC, selective utilities globally | Short term (≤ 2 years) |

| Cybersecurity and data-compliance burden | -1.1% | EU, North America, advanced APAC | Medium term (2-4 years) |

| Retrofit disruption and payback uncertainty | -1.0% | EU core, North America, aging commercial stock | Medium term (2-4 years) |

| Fragmented buyer ROI perception | -0.8% | Global mid-market, SMEs, multi-site portfolios | Long term (≥ 4 years) |

Opportunity

VPP orchestration platforms

This is a genuine opportunity rather than a current driver because most EMS vendors still monetize site-level monitoring and controls, while the larger untapped value pool sits one layer above the meter in aggregating fleets of distributed assets into virtual power plants that can trade flexibility, capacity, and balancing services. The VPP market was around US$7.7 billion in 2026 by one estimate, with multiple sources pointing to a multiyear expansion trajectory driven by software that coordinates solar, storage, EVs, CHP, and flexible loads in real time.

For EMS companies, the strategic pivot is not just feature expansion but revenue-model expansion: instead of charging only software subscription fees per site, vendors can earn performance-linked revenue from demand response, grid services, and flexibility sharing, potentially lifting gross margins by 500–1,000 basis points on qualified portfolios. This whitespace is still underpenetrated because most building and C&I customers are managed asset-by-asset rather than as dispatchable fleets; vendors that can move from energy optimization to market participation could lower customer acquisition cost through utility partnerships and add an estimated +2.2 percentage points to CAGR in North America, Europe, Australia, and Japan where market rules increasingly support flexibility monetization.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| VPP orchestration platforms | +2.2% | North America, EU, Australia, Japan | Medium term (2-4 years) |

| EV charging and V2G EMS stacks | +1.9% | EU core, North America, China, Korea | Short term (≤ 2 years) |

| AI-native EMS for data centers | +1.6% | EU, North America, APAC digital hubs | Medium term (2-4 years) |

| Cross-border energy data monetization | +1.3% | EU core, multinational portfolios | Medium term (2-4 years) |

| SME energy-as-a-service bundles | +1.5% | Europe, North America, India, Southeast Asia | Short term (≤ 2 years) |

| Carbon-compliance software roll-ups | +1.1% | EU core, North America selective | Long term (≥ 4 years) |

Challenges

Digital-skills and integrator gap

The digital-skills and integrator gap is a structural challenge because EMS value capture increasingly depends on advanced data modeling, AI-enabled controls, and cross-domain integration, while the workforce capable of delivering this at scale remains scarce across key regions; Eurostat data cited in 2026 shows only about 56% of Europeans aged 16–74 possess basic digital skills, and industry commentary stresses that the energy and digital transitions are already running into a talent shortage that spans engineering, software, and operational technology.

Implementation and transition training around EMS-aligned standards like ISO 14001:2026 reinforces this point: updated courses emphasize the need for skilled staff to manage lifecycle thinking, change management, internal audits, and continuous improvement, which small and mid-sized organizations struggle to resource. The result is longer deployment times, higher billable integration costs, and uneven performance across projects, which collectively subtracts an estimated 1.2 percentage points from the market’s achievable CAGR by slowing throughput and constraining the pool of high-quality delivery partners across Europe, North America, and major APAC metros.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Digital-skills and integrator gap | -1.2% | EU regulatory hubs, North America, APAC metros | Long term (≥ 4 years) |

| Smart-grid data quality and interoperability | -1.1% | North America, EU, APAC grid corridors | Medium term (2-4 years) |

| Cybersecurity and trust-by-design demands | -1.0% | EU, North America, advanced APAC | Medium term (2-4 years) |

| ISO 14001:2026 EMS governance complexity | -0.9% | Global corporates, EU-heavy portfolios | Long term (≥ 4 years) |

| Transition from pilots to portfolio scale | -0.8% | Global C&I customers, utilities | Medium term (2-4 years) |

| Vendor fragmentation and platform fatigue | -0.7% | Global multi-site enterprises | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Geopolitical Realignment and Energy Security Are Accelerating EMS Adoption Globally

The world’s shifting geopolitical landscape is quietly but powerfully reshaping how organizations think about energy management. As trade tensions rise, supply chains become more fragile, and governments grow increasingly serious about energy independence, the urgency to adopt intelligent EMS solutions has never been stronger.

Countries across North America, Europe, and Asia Pacific are responding with bold clean energy policies, carbon reduction mandates, and significant public investment in smart grid infrastructure all of which are directly fueling demand for advanced EMS platforms. At the same time, the Russia-Ukraine conflict’s impact on global energy prices served as a powerful wake-up call for industries worldwide, pushing businesses to take energy efficiency far more seriously than before. Simply put, geopolitics is no longer just a background issue it has become one of the most powerful forces driving EMS market growth globally.

The Russia-Ukraine conflict in 2022, the European Union fast-tracked its REPowerEU energy plan, committing over €300 billion toward energy efficiency, renewable energy deployment, and smart energy infrastructure across member states directly accelerating EMS adoption across European industrial facilities and commercial buildings as organizations rushed to reduce energy dependency and improve operational resilience in response to the geopolitical energy crisis.

Regional Analysis

North America Held the Largest Share of the Global Energy Management System Market.

In 2025, North America dominated the global Energy Management System market, holding about 35.6% and the reasons behind this are quite clear. This is a region where energy costs are high, regulatory pressure around sustainability and carbon reduction is intensifying, and businesses truly recognize the long-term value of investing in smarter and more efficient energy management practices.

Add to this the region’s world-class digital infrastructure, deep cloud computing ecosystem, and strong culture of technology adoption, and you have the perfect environment for energy management system market leadership. Canada is also contributing meaningfully, with growing investments in smart grid modernization and expanding energy efficiency programs that are steadily strengthening the regional market presence beyond the United States.

Beyond North America, the EMS story gets even more exciting. Europe is pushing hard through strict sustainability regulations and clean energy mandates, Asia Pacific is growing fastest driven by China, India, and Southeast Asia’s booming industrial sectors, Latin America is steadily building momentum through rising energy costs and renewable energy investments, while the Middle East and Africa are emerging confidently through ambitious national smart city and net zero transformation agendas.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global EMS market is competitive but well-structured, with a strong mix of global technology giants and innovative specialists leading the charge. Companies like Schneider Electric, Siemens AG, Honeywell International, ABB Ltd., General Electric, Emerson Electric, Johnson Controls, Eaton Corporation, IBM Corporation, and Cisco Systems dominate the market through continuous innovation, strong global distribution networks, and deep customer relationships across industrial, commercial, and residential sectors.

These players like Schneider Electric, Honeywell, Eaton, and Emerson Electric compete aggressively across hardware, software, and cloud-based deployment segments to strengthen and defend their market positions globally. What truly sets these companies apart is their ability to continuously evolve investing heavily in AI, IoT, and cloud technologies to deliver smarter, faster, and more precise energy management solutions that genuinely help organizations reduce costs, meet sustainability targets, and build more energy-resilient operations for the future.

The Major Players In The Industry

- Schneider Electric SE

- Siemens AG

- ABB Ltd.

- Honeywell International Inc.

- General Electric (GE Vernova)

- Eaton Corporation PLC

- Emerson Electric Co.

- IBM Corporation

- Johnson Controls International

- Huawei Technologies

- Oracle Corporation

- Rockwell Automation

- Cisco Systems Inc.

- Delta Electronics Inc.

- Landis+Gyr (Toshiba)

Key Development

- In March 2025, Schneider Electric SE unveiled its One Digital Grid Platform, an AI-enabled energy management solution designed to improve grid resilience, operational efficiency, and integration of distributed energy resources. The platform supports utilities in modernizing energy networks while accelerating digital transformation across power infrastructure.

- In November 2025, Siemens AG launched Gridscale X Flexibility Manager, a software solution that helps utilities optimize existing grid capacity and manage distributed energy resources. The platform can increase grid capacity utilization by up to 20%, supporting smarter energy management and faster electrification initiatives.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 60.0 Bn |

| Forecast Revenue (2035) | USD 225.0 Bn |

| CAGR (2026-2035) | 15.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Hardware, Software, and Services), By Type (Industrial Energy Management System (IEMS), Building Energy Management System (BEMS), and Home Energy Management System (HEMS)), By Deployment Mode (On-Premises, Cloud-Based, and Hybrid Cloud), By End-Use Industry (Manufacturing, Power & Energy/Utilities, Telecom & IT, Commercial & Residential Buildings, Healthcare & Hospitals, Food & Beverages, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Schneider Electric SE, Siemens AG, ABB Ltd., Honeywell International Inc., General Electric (GE Vernova), Eaton Corporation PLC, Emerson Electric Co., IBM Corporation, Johnson Controls International, Huawei Technologies, Oracle Corporation, Rockwell Automation, Cisco Systems Inc., Delta Electronics Inc., and Landis+Gyr (Toshiba). |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |