Quick Navigation

Report Overview

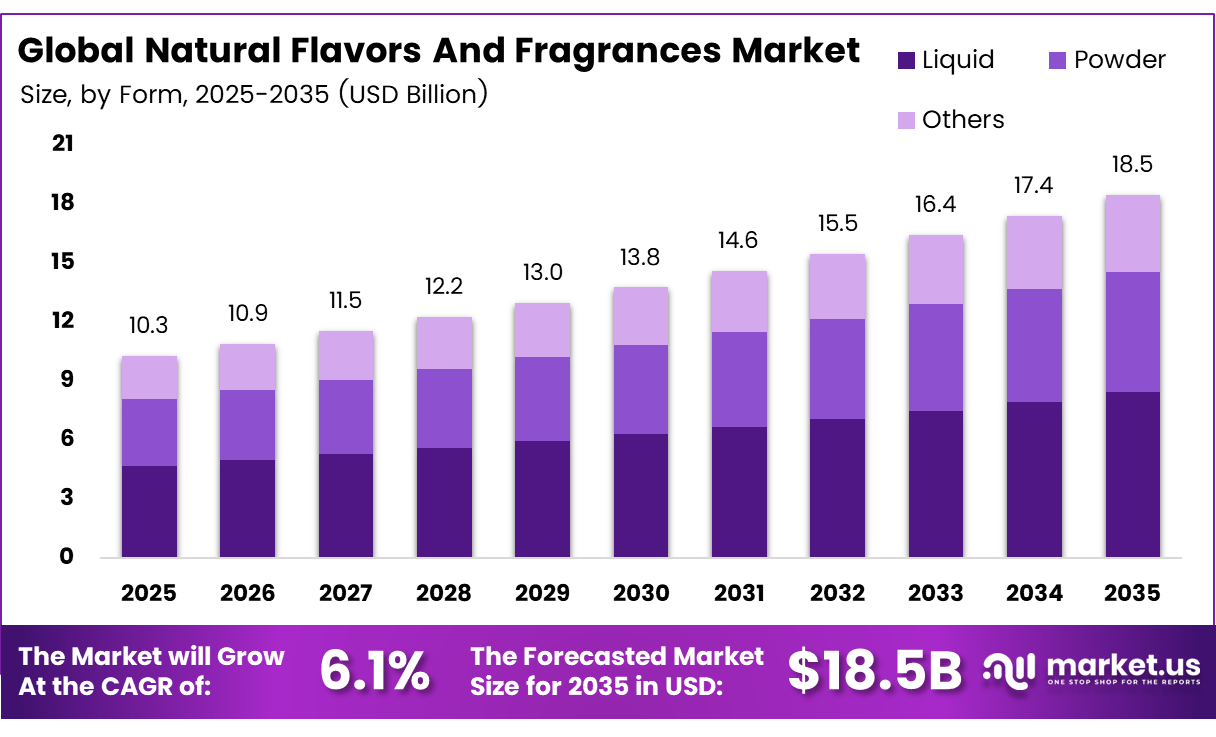

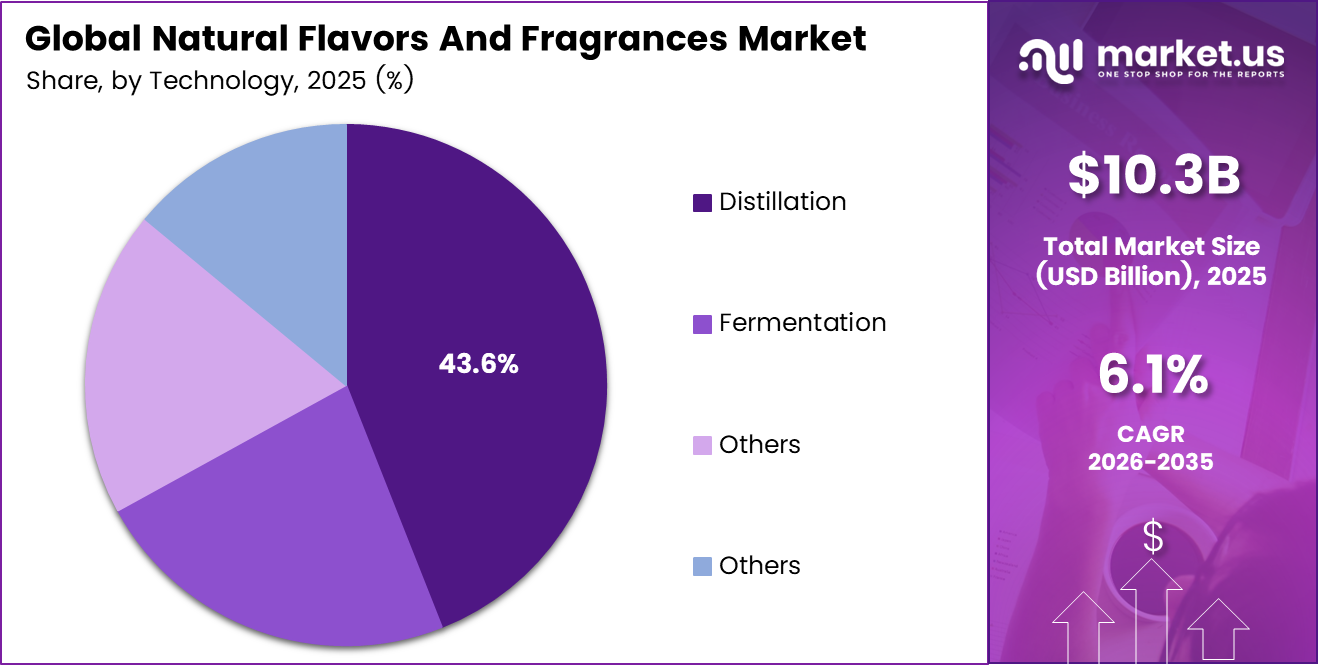

The Global Natural Flavors and Fragrances Market size is expected to be worth around USD 18.5 billion by 2035 from USD 10.3 billion in 2025, growing at a CAGR of 6.1% during the forecast period 2026 to 2035.

The natural flavors and fragrances market covers plant-derived and biotechnology-produced compounds used in food, beverages, cosmetics, and personal care. Manufacturers extract these ingredients through distillation, fermentation, and solvent extraction from botanical sources. Consequently, the supply base spans essential oils, oleoresins, herbal extracts, and dried crops across global agricultural regions.

Consumer behavior has shifted decisively toward clean-label products. Buyers now actively reject synthetic additives in food and personal care, forcing manufacturers to reformulate with plant-derived alternatives. This structural shift creates durable procurement pressure on natural ingredient suppliers, making the category less cyclical and more embedded in product development pipelines.

Symrise achieved €50 million in savings versus its €40 million target, boosting adjusted EBITDA margin to 21.9%, while BASF launched Isobionics Natural alpha-Farnesene 95 with over 95% purity for flavor applications at 10 ppm. DSM-Firmenich recorded 3% organic sales growth, a 21.7% adjusted EBITDA margin, and completed 100% life-cycle assessment coverage across its Perfumery & Beauty portfolio.

The premium cosmetics and functional food sectors drive the highest-value demand for natural compounds. Wellness product developers incorporate adaptogenic herbs, citrus terpenes, and floral extracts into formulations targeting mood, energy, and immunity. These high-margin application categories reward suppliers who invest in exotic botanical sourcing and proprietary extraction capabilities.

Biotechnology and fermentation now enable scalable production of nature-identical compounds previously constrained by crop availability. This technology shift reduces supply volatility while maintaining the natural positioning that consumers value. MANE’s newly inaugurated Dahej facility, designed for a 25% reduction in energy consumption with an annual capacity of 2,000 tonnes of flavor products and 3,000 tonnes of fragrance products, signals how leading producers are scaling sustainable manufacturing infrastructure.

Key Takeaways

- The Global Natural Flavors and Fragrances Market is valued at USD 10.3 billion in 2025 and is forecast to reach USD 18.5 billion by 2035 at a CAGR of 6.1% during the forecast period 2026 to 2035.

- Liquid holds the dominant share at 58.3% of the total market.

- Essential Oils leads with a 42.7% market share.

- Distillation dominates with a 43.6% share of the technology segment.

- Flavors leads with a 56.2% share, ahead of Fragrances.

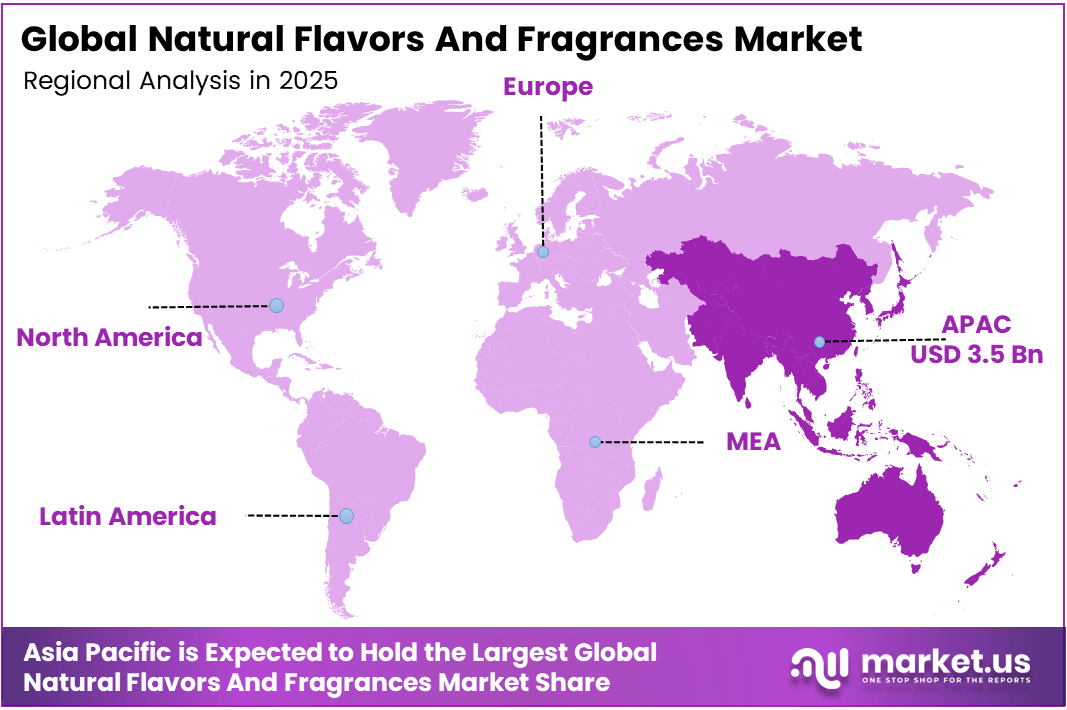

- Asia-Pacific is the dominant region with a 34.2% share, valued at USD 3.5 billion in 2025.

Form Analysis

Liquid dominates with 58.3% due to superior solubility and processing compatibility.

In 2025, Liquid held a dominant market position in the By Form segment of the Natural Flavors and Fragrances Market, with a 58.3% share. Liquid formats integrate seamlessly into beverage, cosmetic, and food manufacturing lines, removing the blending steps required by powder alternatives. This processing advantage locks in liquid formats as the default specification across high-volume application categories.

Powder serves manufacturers who prioritize shelf stability and reduced logistics costs over immediate solubility. Powder formats find the strongest adoption in dry bakery mixes, seasoning blends, and encapsulated fragrance applications where moisture control is critical. However, their share remains secondary because converting liquid extracts to powder adds processing cost without proportional value gain for most end-use categories.

Product Type Analysis

Essential Oils dominate with 42.7% due to a broad application range and consumer recognition.

In 2025, Essential Oils held a dominant market position in the By Product Type segment of the Natural Flavors and Fragrances Market, with a 42.7% share. Their dominance reflects decades of established supply chains for high-volume varieties and deep consumer familiarity in both food and personal care applications. This recognition advantage makes essential oils the lowest-risk natural ingredient specification for product developers entering new categories.

Oleoresins deliver concentrated flavor compounds in standardized potency levels, making them the preferred specification for food manufacturers requiring batch consistency. Unlike essential oils, oleoresins carry both the volatile aroma fraction and the non-volatile flavor compounds of the source material, providing a fuller flavor profile in applications like spice blends and marinades.

Technology Analysis

Distillation dominates with 43.6% due to proven scalability and industry-wide adoption.

In 2025, Distillation held a dominant market position in the By Technology segment of the Natural Flavors and Fragrances Market, with a 43.6% share. Steam and hydro-distillation remain the benchmark extraction method for essential oils because the process is capital-efficient at commercial scale and produces outputs with well-understood regulatory and sensory profiles.

Extraction encompasses solvent, supercritical CO₂, and cold-press methods that recover flavor and fragrance compounds from botanical materials. Supercritical CO₂ extraction attracts premium positioning due to its solvent-free output and ability to preserve thermally sensitive aroma compounds destroyed by distillation heat.

Application Analysis

Flavors dominate with 56.2% due to pervasive use across processed food categories.

In 2025, Flavors held a dominant market position in the By Application segment of the Natural Flavors and Fragrances Market, with a 56.2% share. The processed food and beverage industry’s scale creates structural demand for flavor compounds that no other application category can match. Clean-label reformulation across packaged food accelerates natural flavor adoption at a pace that sustains this dominant share through the forecast period.

Fragrances constitute the complementary half of the market, serving personal care, home care, and wellness applications where scent is the primary product value driver. The fragrance segment benefits from the premiumization of personal care globally, as consumers in developing economies trade up from basic hygiene products to scented formulations with natural ingredient credentials.

Key Market Segments

By Form

- Liquid

- Powder

- Others

By Product Type

- Essential Oils

- Orange

- Corn Mint

- Eucalyptus

- Pepper Mint

- Lemon

- Others

- Oleoresins

- Paprika

- Black Pepper

- Turmeric

- Ginger

- Others

- Dried Crops

- Herbal Extracts

- Others

By Technology

- Distillation

- Fermentation

- Extraction

- Others

By Application

- Flavors

- Confectionery

- Convenience Food

- Bakery Food

- Animal Feed

- Others

- Fragrances

- Fine Fragrances

- Cosmetics and Toiletries

- Soaps and Detergents

- Aromatherapy

- Others

Emerging Trends

AI-Driven Formulation and Wellness-Oriented Fragrance Profiles Reshape Product Development Timelines

Fragrance and flavor developers now deploy AI platforms to map consumer preference data against ingredient combinations, cutting development cycles from months to weeks. This shift gives producers who invest in data infrastructure a structural speed advantage over competitors still relying on manual sensory evaluation. The practical result is faster time-to-shelf for trend-responsive product lines in premium skincare and functional beverages.

Mood-enhancing and aromatherapy-based fragrance products are moving from specialty wellness channels into mainstream personal care retail. Consumers actively seek scent products linked to stress relief, focus, and energy — positioning that requires authenticated natural botanical inputs rather than synthetic equivalents. DSM-Firmenich reported 11,002 kt CO₂e Scope 1, 2, and 3 greenhouse gas emissions in its 2025 Integrated Annual Report, signaling that sustainability transparency is now a measurable operational benchmark for leading fragrance producers competing in the wellness segment.

Natural citrus, herbal, and floral notes are entering functional beverages and premium skincare at scale. Botanical and exotic ingredient blends inspired by regional and cultural flavor preferences — yuzu, kokum, and za’atar, for example — differentiate product lines in saturated markets where standard vanilla and citrus no longer command shelf premium. Early movers who secure a reliable supply of these emerging botanicals gain sourcing leverage that late entrants cannot quickly replicate.

Drivers

Clean-Label Mandates and Regulatory Pressure on Synthetics Accelerate Natural Ingredient Procurement

Consumer demand for transparent ingredient lists has moved beyond a marketing preference into a procurement mandate. Food, beverage, and personal care manufacturers now build natural flavor and fragrance specifications into core product briefs rather than treating them as optional upgrades. Symrise achieved 2.8% organic sales growth in full-year 2025, demonstrating that this demand environment already translates into measurable revenue expansion for established natural ingredient producers.

Regulatory tightening on synthetic additives accelerates the commercial timeline for natural alternatives. EU restrictions on artificial flavor compounds and synthetic fragrance allergens force reformulation across thousands of product SKUs, creating procurement windows that natural ingredient suppliers are positioned to fill. Manufacturers who delay reformulation face de-listing risk from retailers enforcing clean-label policies, making compliance a commercial imperative rather than a voluntary commitment.

Premium cosmetics and functional food categories reinforce this driver by embedding natural ingredient credentials into brand equity. Wellness product developers use botanical provenance as a core marketing asset, making natural flavor and fragrance sourcing inseparable from the commercial story. This brand-level dependency raises switching costs for buyers and strengthens long-term supplier relationships with producers who offer traceability documentation and certified origin credentials.

Restraints

Raw Material Cost Structures and Supply Chain Fragility Cap Natural Ingredient Scalability

Natural extraction processes carry inherently higher production costs than synthetic manufacturing. Steam distillation, supercritical CO₂ extraction, and cold-press operations require significant capital investment in equipment, energy, and skilled labor, with per-unit costs that synthetic alternatives cannot match at equivalent volumes. Dsm-firmenich sourced 100% of purchased electricity from renewable sources in 2025, demonstrating that leading producers absorb significant infrastructure investment to meet sustainability benchmarks — costs that smaller competitors cannot easily replicate.

Supply chain volatility represents the structural vulnerability that most limits natural ingredient scale. Botanical raw materials depend on agricultural cycles, climate conditions, and limited cultivable geographies. A drought in a key producing region, a pest outbreak affecting a specific crop, or a political disruption in a source country can remove significant supply from global markets within a single growing season. This exposure forces buyers to hold expensive safety stock or accept supply interruptions that synthetic-based supply chains eliminate.

The concentration of botanical cultivation in specific geographies amplifies this risk. Lavender in Bulgaria, corn mint in India, sandalwood in Australia — these geographic concentrations mean that single-country disruptions cascade through global fragrance and flavor supply chains simultaneously. Diversifying botanical sourcing requires multi-year agricultural development programs that carry cost and uncertainty profiles most manufacturers cannot justify without volume commitments that do not yet exist.

Growth Factors

Biotechnology, Urbanization-Led Premiumization, and Sustainability Investment Open New Revenue Horizons

Fermentation-based production of nature-identical compounds solves the scale constraint that limits conventional botanical extraction. Producers using microbial platforms can manufacture specific aroma compounds at industrial volume without crop dependency, reducing both cost and supply risk. DSM-Firmenich achieved 100% life-cycle assessment data coverage across its Perfumery & Beauty portfolio in 2025, illustrating how leading producers now quantify and optimize the environmental credentials of biotechnology-derived ingredients to satisfy corporate buyer sustainability requirements.

Urbanization and rising disposable incomes in Asia, Africa, and Latin America expand the consumer base for premium packaged food, personal care, and home fragrance products. These categories depend on natural flavor and fragrance inputs at higher intensity than their mass-market predecessors. Manufacturers entering these markets with premium positioning build natural ingredient specifications from launch rather than reformulating from synthetic baselines, creating structurally higher natural ingredient demand per product unit than mature Western markets generate.

Investment in sustainable packaging and eco-conscious formulations creates a multiplier effect for natural ingredient adoption. Brands committing to sustainability across packaging and ingredient sourcing find that natural flavor and fragrance credentials reinforce the overall brand narrative, increasing the commercial return on natural ingredient premiums. This alignment between sustainability investment and ingredient sourcing strategy makes natural flavor and fragrance adoption a portfolio-level decision rather than a category-specific cost trade-off.

Regional Analysis

Asia-Pacific Dominates the Natural Flavors and Fragrances Market with a Market Share of 34.2%, Valued at USD 3.5 Billion

Asia-Pacific holds a 34.2% market share, valued at USD 3.5 billion in 2025. China, India, and Southeast Asia drive this leadership through simultaneous roles as both the largest producing and fastest-expanding consuming regions. Rising middle-class incomes accelerate premiumization across packaged food, personal care, and home fragrance, pulling natural ingredient volumes at a pace that no other global region currently replicates.

North America holds the second-largest share, supported by mature clean-label regulation, well-funded food and beverage reformulation programs, and a premium personal care sector with established natural ingredient specifications. The FDA’s natural labeling standards and retailer clean-label mandates from major grocery chains convert compliance pressure directly into sustained procurement volume for natural flavor and fragrance suppliers.

Europe maintains a strong demand anchored by stringent EU regulations on synthetic additives and fragrance allergens, which effectively mandate natural reformulation across food and cosmetics categories. The EU’s Farm to Fork strategy and the Green Deal further reinforce natural ingredient sourcing by embedding sustainability criteria into food system policy, creating both a regulatory push and a consumer pull for certified botanical ingredients.

Latin America offers a structural supply-side advantage as a primary producer of citrus oils, tropical fruit extracts, and vanilla, while simultaneously expanding its own domestic consumption of premium packaged products. Brazil and Mexico lead regional demand growth as urban consumers trade up into natural-positioned food and personal care categories. This dual producer-consumer role positions Latin America as a strategic geography for vertically integrated natural ingredient businesses.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Analysis

MANE positions itself as a vertically integrated natural ingredient producer with expanding manufacturing capabilities in high-growth markets. The company’s Dahej facility in Gujarat was designed to reduce energy consumption while supporting large-scale production of flavor and fragrance products. This infrastructure investment in India reflects a deliberate strategy to serve Asia-Pacific demand from within the region rather than relying on long-haul supply chains.

BASF SE differentiates itself through fermentation-based production of high-purity natural compounds. Its Isobionics Natural alpha-Farnesene 95 is produced from renewable resources and performs effectively in citrus and floral flavor applications even at low concentrations. This biotechnology platform positions BASF to supply the natural flavor market at an industrial scale without the crop dependency associated with conventional botanical extraction, creating advantages in cost structure and supply reliability.

Symrise combines operational efficiency with organic revenue growth to build a defensible competitive position. The company improved profitability through cost-saving initiatives that exceeded internal targets while continuing to expand sales organically. This margin discipline demonstrates Symrise’s ability to convert scale into profitability more effectively than many peer competitors operating at similar revenue levels.

Firmenich operates in the premium fragrance and flavor segment, where proprietary naturals and exclusive botanical sourcing create differentiation that is less vulnerable to price competition. Its focus on luxury fragrance houses and premium personal care brands places it in application categories with strong natural ingredient intensity and significant pricing power. This positioning helps shield Firmenich from margin pressure in more commoditized areas of flavor and fragrance supply while allowing it to capture value at the high end of the market.

Key Players

- MANE

- BASF SE

- Symrise

- Firmenich SA

- Keva Flavours Pvt. Ltd.

- DOHLER GmbH

- ADM

- Stringer Flavours Ltd.

- BIOLANDES

- Falcon

- Givaudan

- Sensient Technologies

- FLAVEX Naturextrakte GmbH

- Blue Pacific Flavours, Inc.

- Young Living Essential Oils, LC

Recent Developments

- In 2025, MANE recently strengthened its position in the natural flavors and ingredients industry through strategic expansion activities. The company acquired FROMATECH Ingredients B.V., a move aimed at enhancing MANE’s savoury flavor solutions and functional ingredient portfolio while increasing its presence across Europe, the Middle East & Africa.

- In 2025, BASF SE will continue investing in biotechnology-driven aroma ingredients for the natural flavors and fragrances sector. BASF Aroma Ingredients launched Isobionics Natural alpha-Farnesene 95, a fermentation-derived natural lime flavor ingredient with more than 95% purity.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 10.3 Billion |

| Forecast Revenue (2035) | USD 18.5 Billion |

| CAGR (2026-2035) | 6.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Form (Liquid, Powder, Others), By Product Type (Essential Oils, Oleoresins, Dried Crops, Herbal Extracts, Others), By Technology (Distillation, Fermentation, Extraction, Others), By Application (Flavors, Fragrances) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | MANE, BASF SE, Symrise, Firmenich SA, Keva Flavours Pvt. Ltd., DOHLER GmbH, ADM, Stringer Flavours Ltd., BIOLANDES, Falcon, Givaudan, Sensient Technologies, FLAVEX Naturextrakte GmbH, Blue Pacific Flavours, Inc., Young Living Essential Oils, LC |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |