Quick Navigation

Report Overview

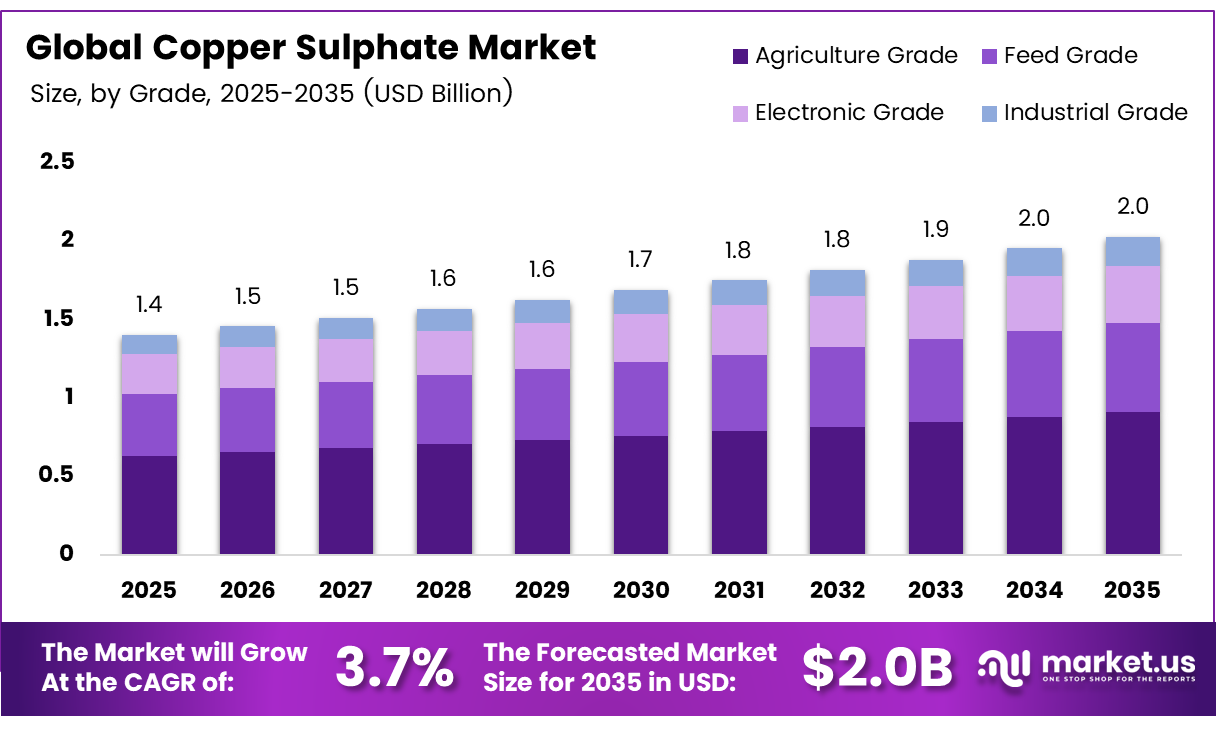

The Global Copper Sulphate Market size is expected to be worth around USD 2.0 billion by 2035 from USD 1.4 billion in 2025, growing at a CAGR of 3.7% during the forecast period 2026 to 2035.

Copper sulphate is an inorganic compound with broad industrial utility across agriculture, mining, electronics, and water treatment. Its versatility as both a fungicide and micronutrient fertilizer makes it a critical input for modern crop protection programs. The compound’s role spans from basic commodity chemical to high-purity specialty grade.

Agricultural applications anchor the market structure. Copper sulphate-based fungicides protect high-value crops from fungal pathogens, while micronutrient formulations correct copper deficiencies in soil-depleted farmland. This dual-use profile means agricultural buyers treat copper sulphate as an essential input, not a discretionary purchase — a structural demand floor that limits downside risk for producers.

The U.S. EPA classified the 3.3% copper sulfate pentahydrate product “TERMINATOR” as restricted-use, increasing oversight of copper-based biocides. Meanwhile, copper electroplating optimization reduced non-uniformity from 20.3% to 12.3%, setting a new benchmark for high-purity copper sulphate in electronics manufacturing.

Mining and metallurgical processing represent the second major demand pillar. Copper sulphate functions as a flotation agent in ore separation, directly linking its consumption to global mining output levels. As copper ore grades decline globally, operators intensify chemical use per tonne processed, which supports volume consumption even without production volume growth.

Water treatment facilities consume copper sulphate for algae control and industrial wastewater purification. Municipal infrastructure upgrades across developing economies are expanding treatment capacity, pulling through steady incremental demand. This end-use provides relative volume stability since water treatment is a regulated, non-discretionary operational function.

Key Takeaways

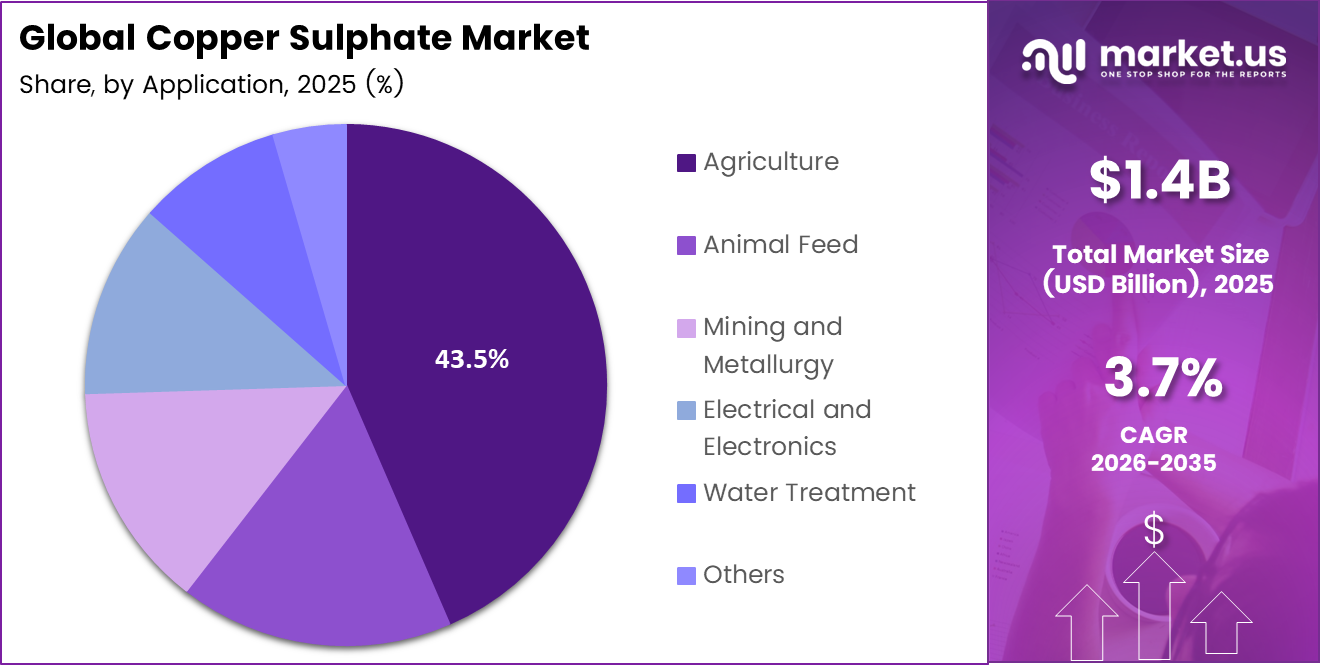

- The Global Copper Sulphate Market is valued at USD 1.4 billion in 2025 and is forecast to reach USD 2.0 billion by 2035 at a CAGR of 3.7% during the forecast period 2026 to 2035.

- Agriculture Grade dominates with a 43.8% share in 2025.

- Agriculture leads with a 43.5% share, confirming crop protection as the primary demand driver.

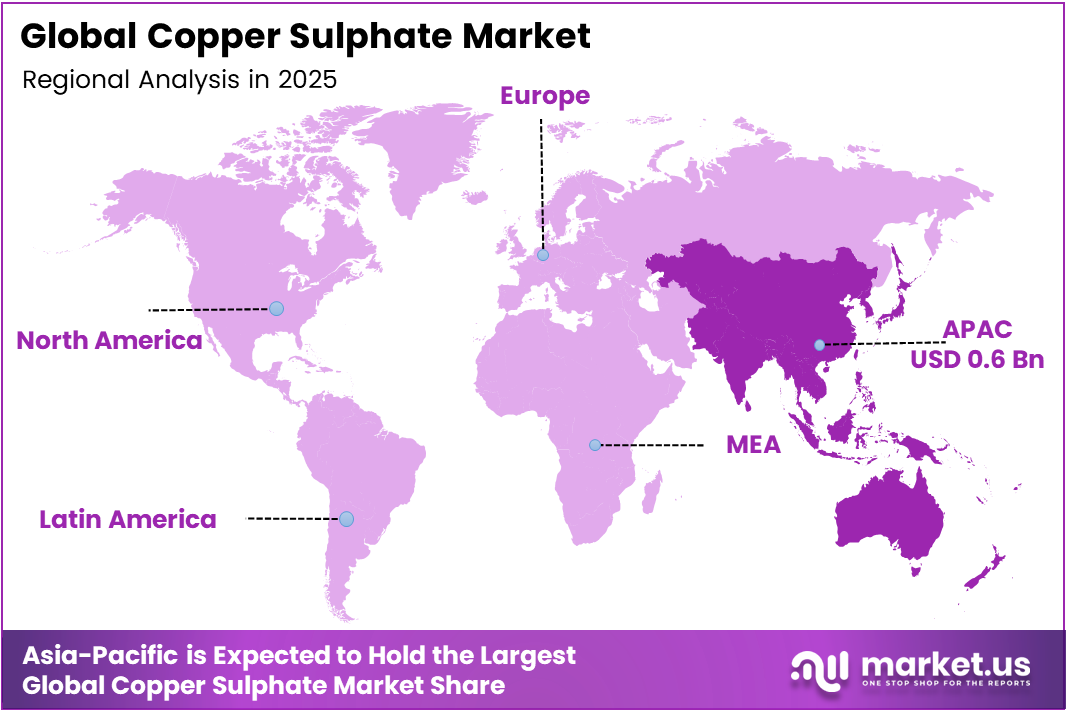

- Asia-Pacific holds the largest regional share at 43.9%, valued at approximately USD 0.6 billion in 2025.

Grade Analysis

Agriculture Grade dominates with 43.8% due to widespread use in crop fungicide and fertilizer programs.

In 2025, Agriculture Grade held a dominant market position in the By Grade segment of the Copper Sulphate Market, with a 43.8% share. This grade serves as the primary active ingredient in copper-based fungicides and micronutrient fertilizers, making it a non-substitutable input for high-yield crop production. Its formulation compatibility with existing agrochemical delivery systems reinforces buyer lock-in.

Feed-Grade copper sulphate serves as a controlled antimicrobial and growth-promoting additive in livestock and poultry nutrition programs. Regulatory approval requirements differ across geographies, creating compliance complexity that limits smaller producers from entering this segment. However, producers who achieve certification unlock recurring B2B contracts with large-scale animal nutrition manufacturers.

Electronic Grade carries the highest purity specification within the copper sulphate product range. Electroplating and printed circuit board manufacturing demand tight chemical consistency to ensure plating uniformity and conductivity performance. As the electronics industry moves toward miniaturized components, the tolerance for chemical variance narrows further, which structurally favors producers with advanced refining capabilities.

Application Analysis

Agriculture dominates with 43.5% due to critical fungicide and soil micronutrient requirements in crop production.

In 2025, Agriculture held a dominant market position in the By Application segment of the Copper Sulphate Market, with a 43.5% share. Copper sulphate functions as both a contact fungicide and a copper micronutrient source, addressing two distinct crop protection needs simultaneously. This dual-function value proposition makes it cost-efficient for farmers compared to using separate chemical inputs.

Animal Feed applications use copper sulphate as a trace mineral supplement that supports metabolic function and immune health in livestock and poultry. The transition from antibiotic growth promoters toward copper-based alternatives in regulated markets has widened the addressable buyer base for feed-grade copper sulphate, creating a demand channel that did not exist at scale a decade ago.

Mining and Metallurgy applications rely on copper sulphate as a flotation activator in the selective separation of sulphide ore minerals. Rising ore processing volumes in Latin America and Africa, where copper-zinc and lead-copper deposits are actively developed, are expanding the installed base of flotation plants that consume copper sulphate on an industrial scale.

Key Market Segments

By Grade

- Agriculture Grade

- Feed Grade

- Electronic Grade

- Industrial Grade

By Application

- Agriculture

- Animal Feed

- Mining and Metallurgy

- Electrical and Electronics

- Water Treatment

- Others

Emerging Trends

Eco-Efficient Formulations and Advanced Material Integration Are Redefining Copper Sulphate’s Industrial Role

Agricultural buyers are shifting preference toward eco-efficient copper sulphate formulations that minimize soil accumulation and reduce ecotoxicological load. This preference reflects regulatory pressure in the EU and North America, where copper application limits per hectare are tightening. Producers who develop low-dose, high-efficacy formulations will capture premium positioning as compliance requirements intensify.

Automated chemical dosing systems in municipal and industrial water treatment plants are reshaping procurement patterns for copper sulphate. Copper-modified reduced graphene oxide achieved 75.41% dye removal compared with 44.92% for standard reduced graphene oxide, demonstrating that copper-enhanced composites are outperforming conventional materials in industrial treatment applications.

Research institutions and chemical manufacturers are accelerating the development of nano-grade copper sulphate for high-performance industrial and scientific applications. Strategic partnerships between agrochemical producers and raw material suppliers are also forming to stabilize supply chains. Both trends signal a structural shift from copper sulphate as a bulk commodity toward a differentiated specialty chemical category, which will reward vertically integrated producers with R&D capabilities.

Drivers

Multi-Sector Consumption Across Agriculture, Mining, and Electronics Sustains Broad-Based Copper Sulphate Demand

Copper sulphate fungicides protect staple and high-value crops across Asia, Europe, and Latin America, where copper-based chemistry remains the registered standard for diseases such as downy mildew and bacterial blight. The compound’s status as both a pest control agent and a soil micronutrient creates a dual procurement rationale for agricultural buyers. This two-function value keeps demand structurally resilient across different growing seasons and crop types.

Mining operators use copper sulphate to activate sulphide mineral surfaces during flotation, selectively separating target metals from gangue. As global ore grades decline and processing complexity increases, chemical consumption per tonne of ore processed rises. Copper sulfate pentahydrate in pesticide formulations is limited to 80 ppm end-use concentration — a regulatory ceiling that standardizes formulation density and ensures consistent chemical quality across supply chains, reducing variability risk for industrial buyers.

Chemical manufacturing and electroplating industries consume large quantities of high-purity copper sulphate in surface finishing and circuit board production. Silica xerogel adsorption reported an optimal contact time of 80–120 minutes for copper(II) removal from copper sulfate solution, with maximum adsorption capacity reaching 67.5 mg/L — supporting development of more efficient copper recovery systems in industrial wastewater treatment.

Restraints

Copper Price Volatility and Heavy Metal Regulations Constrain Producer Margins and Limit Market Entry

Copper sulphate production costs move directly with raw copper prices, which are subject to LME volatility driven by macroeconomic cycles, mining strikes, and energy cost fluctuations. Producers operating without long-term copper supply contracts face margin compression during price spikes. This cost structure disadvantages smaller manufacturers who lack the procurement scale to hedge raw material exposure effectively.

Environmental regulations governing heavy metal discharge restrict copper sulphate use in several key application areas. Treated potable water must not exceed 1 ppm metallic copper residual — a limit that constrains dosing flexibility in municipal water systems and forces operators toward precision-controlled application methods. Compliance with these thresholds requires capital investment in monitoring and dosing infrastructure.

Regulatory complexity across geographies creates a fragmented compliance landscape that increases the cost of market entry and product registration. Sico Fertilisers updated its product portfolio to include copper sulphate pentahydrate at 25% Cu content in blue powder and crystal form, signaling active product line expansion by European fertilizer manufacturers targeting copper micronutrient deficiency correction in commercial crop programs.

Growth Factors

Aquaculture Expansion, Developing Economy Industrialization, and Advanced Purification Technology Open New Revenue Channels

Copper sulphate-based feed additives are gaining adoption in livestock and poultry nutrition programs as operators seek alternatives to antibiotic growth promoters. This shift is accelerating in markets where antibiotic restrictions are now legally enforced. Producers with feed-grade certification can access recurring contracts with large animal nutrition manufacturers — a buyer category that prioritizes supply consistency and regulatory compliance over price alone.

Rapid industrialization in developing economies is expanding textile dyeing, chemical processing, and mining sectors that rely on copper sulphate as a core process chemical. Silica xerogel treatment achieved 90% maximum copper(II) removal from copper sulfate solution, with a maximum adsorption capacity of 67.5 mg/L — indicating that advanced material science is enabling more efficient copper recovery and recycling within industrial processes.

Investment in sustainable aquaculture infrastructure is expanding the use of copper sulphate for water, sanitation, and disease prevention in fish farming operations. Technological advances in high-purity copper sulphate production are simultaneously supporting entry into advanced electronics and specialty chemical sectors. These two growth vectors — one volume-driven, one value-driven — offer producers distinct strategic pathways to expand revenue without competing solely on commodity price.

Regional Analysis

Asia-Pacific Dominates the Copper Sulphate Market with a Market Share of 43.9%, Valued at USD 0.6 Billion

Asia-Pacific leads the global copper sulphate market with a 43.9% share, valued at approximately USD 0.6 billion in 2025. The region’s dominance reflects simultaneous demand across agriculture, electronics manufacturing, and mining — three sectors where Asia-Pacific holds the highest global output volumes. China and India drive the largest consumption volumes, supported by expansive agricultural land under copper-sensitive crops and active copper mining operations.

North America benefits from a mature agrochemical regulatory framework and a well-established industrial chemical procurement infrastructure. EPA registration requirements for copper sulphate products, including restricted-use classifications, standardize quality expectations, and create a compliance-based entry barrier. This environment favors established chemical producers with full regulatory documentation over lower-cost import competition.

Europe enforces strict limits on copper application per hectare under organic and conventional farming regulations, which is reshaping demand toward low-dose, high-efficacy copper sulphate formulations. The EU’s REACH framework governs chemical safety documentation across all industrial grades. Consequently, European buyers prioritize suppliers with full REACH compliance — a certification requirement that filters the supplier base and supports pricing stability.

Latin America’s copper sulphate consumption is anchored by large-scale soy, coffee, and fruit crop production that relies on copper-based fungicides for disease management. The region also hosts major copper mining operations in Chile and Peru, generating internal industrial demand. Agricultural expansion into frontier farmland in Brazil is creating incremental demand for both fungicide and micronutrient fertilizer applications.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Ataman Chemicals positions itself as a broad-portfolio industrial chemical distributor serving agrochemical, mining, and electroplating sectors across the Middle East and Europe. Its regional distribution strength allows it to serve mid-sized industrial buyers who require a consistent supply without the minimum volume commitments that large producers typically impose. This positioning makes it a critical intermediary in fragmented regional markets.

BAKIRSULFAT AS operates as a dedicated copper sulphate producer with manufacturing infrastructure calibrated for agricultural and industrial grade output. Specialization in a single compound class allows the company to optimize production efficiency and maintain competitive cost structures. Buyers in price-sensitive agricultural markets prioritize suppliers like BAKIRSULFAT AS that can offer consistent grade quality at scale without diversification-related supply variability.

GAMBIT focuses on chemical supply to the mining and industrial processing sectors, where copper sulphate is consumed as a functional reagent rather than a finished product. Its technical sales approach — supplying chemical solutions to specific process problems — gives it differentiated access to metallurgical buyers who evaluate suppliers on application knowledge, not just price.

Hebei Jinchangsheng Chemical Technology Co., Ltd. operates within China’s integrated chemical manufacturing ecosystem, benefiting from domestic copper supply access and proximity to Asia-Pacific’s largest agricultural and electronics markets. Its scale and upstream integration support competitive pricing across multiple grades. For global buyers evaluating Asia-Pacific sourcing, Chinese producers like Hebei Jinchangsheng represent the benchmark cost reference against which all other suppliers are evaluated.

Key Players

- Ataman Chemicals

- BAKIRSULFAT AS

- GAMBIT

- Hebei Jinchangsheng Chemical Technology Co., Ltd.

- Highnic Group

- Max Chemicals Co., Ltd.

- Old Bridge Minerals

- Sulcona

- Sumitomo Metal Mining Co., Ltd.

- Vigro Chemicals PTY Ltd.

Recent Developments

- In 2025, BAKIRSULFAT AS produces and sells copper sulphate for feed, mining, chemical, agriculture, and other industries. The company page states production capacity across two factories was around 22,000 tpa, and planned to increase to 30,000 tpa.

- In 2025, GAMBIT / Gambit Kutno says it produces copper sulphate feed grade and offers copper sulphate pentahydrate (CuSO₄ 5H₂O) in feed and technical grades, with min—24% copper. Kutno city reported that Gambit is a significant producer/distributor of feed-grade copper sulphate in Europe/worldwide, and that its related TAP Kutno investment launched a modern factory in the Kutno subzone of the Łódź Special Economic Zone.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.4 Billion |

| Forecast Revenue (2035) | USD 2.0 Billion |

| CAGR (2026-2035) | 3.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Grade (Agriculture Grade, Feed Grade, Electronic Grade, Industrial Grade), By Application (Agriculture, Animal Feed, Mining and Metallurgy, Electrical and Electronics, Water Treatment, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Ataman Chemicals, BAKIRSULFAT AS, GAMBIT, Hebei Jinchangsheng Chemical Technology Co., Ltd., Highnic Group, Max Chemicals Co., Ltd., Old Bridge Minerals, Sulcona, Sumitomo Metal Mining Co., Ltd., Vigro Chemicals PTY Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |