Quick Navigation

Report Overview

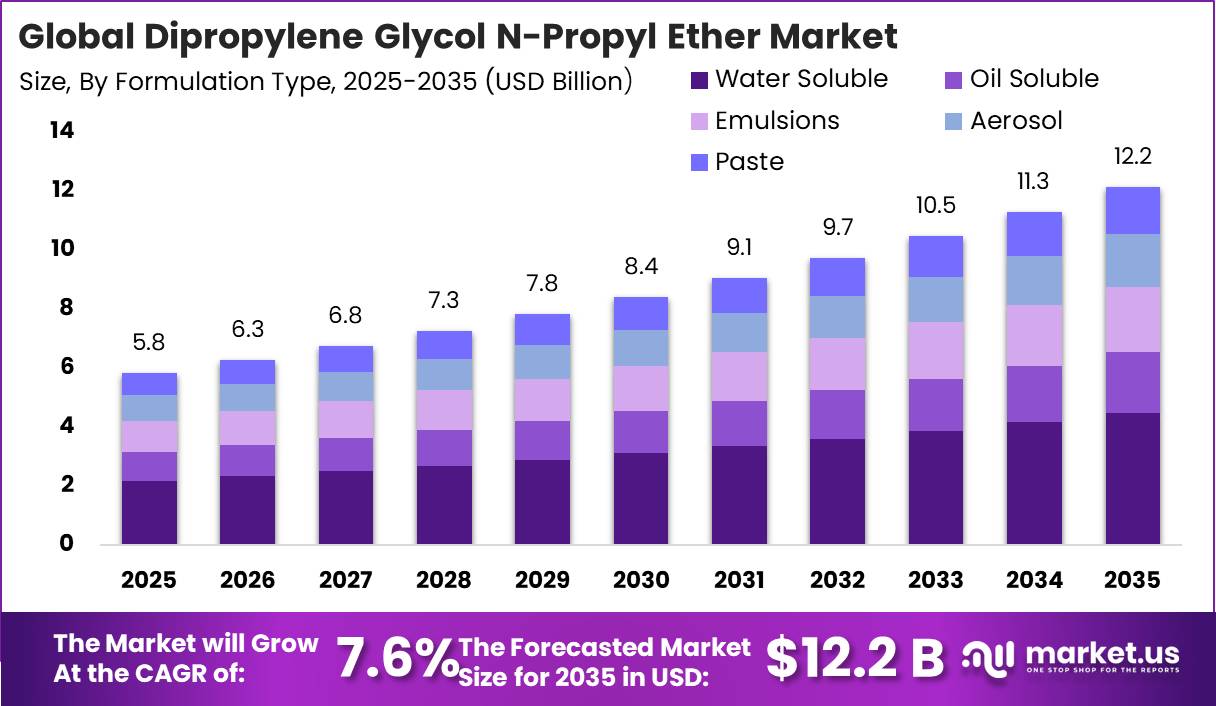

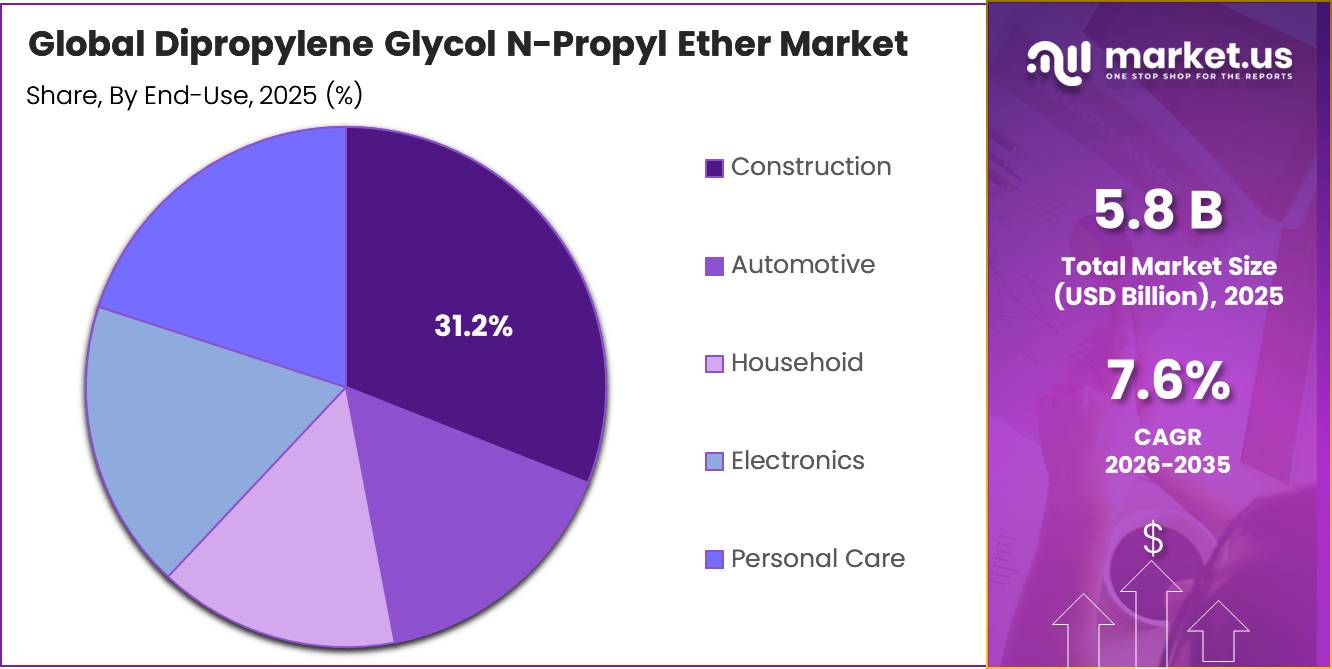

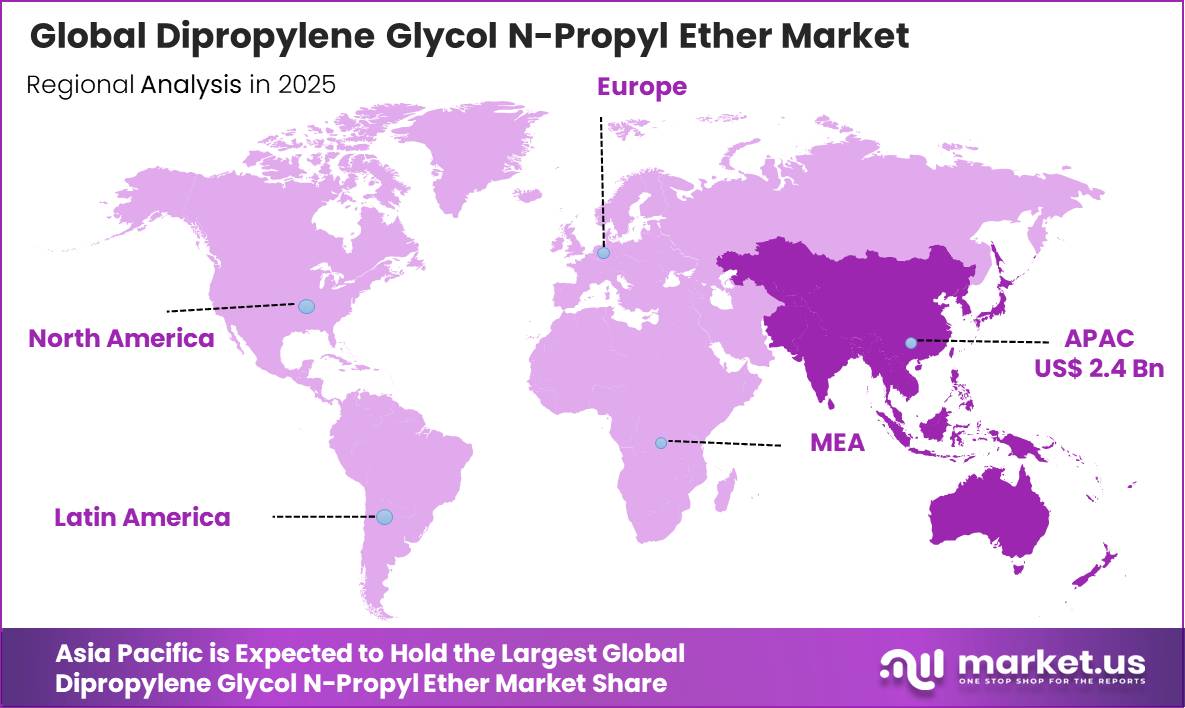

The Global Dipropylene Glycol N-Propyl Ether Market size is expected to be worth around USD 12.2 Billion by 2035, from USD 5.8 Billion in 2025, growing at a CAGR of 7.6% during the forecast period from 2026 to 2035. In 2025, Asia-Pacific held a dominant market position, capturing more than a 41.4% share, holding USD 2.4 Billion revenue.

Dipropylene glycol n-propyl ether (DPnP) operates as a specialty glycol ether solvent valued for its balanced evaporation profile, strong solvency, and compatibility with both aqueous and non-aqueous systems. Its use is concentrated in formulations where controlled drying, surface wetting, and residue-free cleaning are required, particularly in coatings, industrial cleaners, adhesives, and selected personal care applications. The material’s relatively low vapor pressure and functional stability make it suitable for waterborne and low-emission systems, especially where regulatory frameworks limit volatile organic compound content in end-use products.

Consumption patterns are closely linked to industrial activity in construction, automotive refinishing, electronics manufacturing, and institutional cleaning. Expanding urban infrastructure and increased demand for durable coatings have reinforced its role in formulation chemistry, while electronics and precision cleaning applications require high-performance solvent consistency. Supply dynamics are shaped by its petrochemical feedstock dependence, tying pricing and availability to upstream propylene derivatives.

Manufacturing activity is concentrated in integrated chemical hubs, with emphasis on production efficiency, product purity differentiation, and regulatory compliance. Growing adoption of environmentally aligned formulations and water-based systems continues to support its relevance in evolving industrial and consumer chemical applications.

Key Takeaways

- The global dipropylene glycol n-propyl ether market was valued at US$5.8 billion in 2025.

- The global dipropylene glycol n-propyl ether market is projected to grow at a CAGR of 7.6% and is estimated to reach US$12.2 billion by 2035.

- On the basis of formulation type, water-soluble dipropylene glycol n-propyl ether dominated the market, constituting 36.9% of the total market share.

- Based on the applications of the dipropylene glycol n-propyl ether, coatings led the market, comprising 32.8% of the total market.

- Among the end-uses, the construction industry held a major share in the dipropylene glycol n-propyl ether market, 31.2% of the market share.

- In 2025, the Asia Pacific was the most dominant region in the dipropylene glycol n-propyl ether market, accounting for 41.4% of the total global consumption.

Formulation Type Analysis

Water Soluble Dipropylene Glycol N-Propyl Ether is a Prominent Segment in the Market.

Water-soluble formulations represent the dominant segment within the dipropylene glycol n-propyl ether market, accounting for 36.9% share, supported by their extensive use in systems requiring high compatibility with aqueous chemistries. This segment benefits from the solvent’s strong coupling ability between water and organic phases, enabling stable formulations in coatings, cleaning agents, and industrial degreasers. Its effectiveness in reducing surface tension and enhancing solvency in diluted systems makes it particularly suitable for waterborne coatings and institutional cleaning products, where performance consistency and low residue characteristics are critical.

Regulatory emphasis on reducing volatile organic compound emissions has further reinforced adoption in water-based systems. Additionally, expanding demand for environmentally compatible formulations across construction, automotive refinishing, and household cleaning applications continues to strengthen the prominence of water-soluble DPnP-based solutions, positioning this segment as a key contributor to overall market consumption patterns.

Application Analysis

Coatings Held a Major Share of the Dipropylene Glycol N-Propyl Ether Market.

Coatings represent the leading application segment, accounting for 32.8% share, supported by the extensive use of dipropylene glycol n-propyl ether as a functional solvent and coalescing aid in both industrial and architectural coating systems. Its balanced evaporation rate and strong solvency enable improved film formation, pigment dispersion, and flow characteristics, which are critical in achieving uniform surface finishes.

The segment benefits from increasing adoption of waterborne and low-VOC coating technologies, where DPnP helps bridge compatibility between hydrophilic resins and hydrophobic additives. Demand is further reinforced by growth in construction activities, automotive refinishing, and protective coatings for industrial equipment.

End-Use Analysis

Dipropylene Glycol N-Propyl Ether is Mostly Utilized in the Construction Industry.

Construction is the leading end-use segment, accounting for 31.2% share, driven by extensive consumption of dipropylene glycol n-propyl ether in coatings, surface preparation, and maintenance applications. The solvent is widely utilized in architectural paints, protective coatings, and cleaning formulations used during building construction and infrastructure development activities. Its strong solvency and compatibility with water-based systems support improved application performance, particularly in formulations designed to meet modern low-emission requirements.

Expanding urbanization, residential and commercial construction, and large-scale infrastructure projects continue to sustain demand for high-performance coating and cleaning solutions. The segment also benefits from increasing preference for durable, weather-resistant finishes that require efficient film formation and uniform dispersion properties. As construction activities intensify across emerging economies, the reliance on glycol ether-based formulations is expected to remain structurally significant within this end-use category.

Key Market Segments

By Formulation Type

- Water Soluble

- Oil Soluble

- Emulsions

- Aerosol

- Paste

By Application

- Coatings

- Cleaning Agents

- Personal Care Products

- Adhesives

- Industrial Solvents

By End-Use

- Construction

- Automotive

- Household

- Electronics

- Personal Care

Drivers

Rising Demand for Low-VOC and High-Performance Solvents Drives the Dipropylene Glycol N-Propyl Ether Market.

Regulatory tightening on volatile organic compound (VOC) emissions is materially influencing solvent selection across coatings, cleaners, and allied applications. The U.S. Environmental Protection Agency specifies VOC content thresholds for coatings at 275 g/L (baked) and 340 g/L (air-dried), with mandatory tracking and reporting of emissions during use. Parallel frameworks from the California Air Resources Board and EPA define low-VOC or exempt solvents based on vapor pressure thresholds of less than 0.1 mmHg at 20°C, effectively encouraging the adoption of low-volatility chemistries.

Within this compliance environment, glycol ethers such as DPnP align with formulation requirements due to their low vapor pressure, approximately 0.08 mmHg at 20°C, and capability to meet low-VOC criteria in specific applications. Such solvents can be classified as low-VOC capable and are readily biodegradable, supporting their use in environmentally aligned formulations.

Furthermore, the adoption is reinforced by performance characteristics that reduce total solvent demand. For instance, DPnP-based systems may require lower solvent loading while maintaining cleaning efficiency and film formation properties. The convergence of quantified emission limits, definitional thresholds for VOC exemption, and validated low-volatility solvent performance is sustaining a measurable shift toward DPnP in regulated product categories.

Restraints

Volatility in Raw Material Pricing and Petrochemical Dependence Pose Challenges to the Dipropylene Glycol N-Propyl Ether Market.

Production economics for dipropylene glycol n-propyl ether (DPnP) are tightly coupled to upstream petrochemical chains, particularly propylene and propylene oxide, both of which exhibit strong price linkage to crude oil benchmarks. Data from the U.S. Energy Information Administration indicates that crude oil markets are inherently volatile due to geopolitical disruptions, supply inelasticity, and demand shocks, with price swings often required to rebalance supply-demand conditions. This volatility transmits directly into downstream intermediates.

For instance, propylene pricing historically trades at 1.3-1.4 times crude oil on a barrel-equivalent basis, reinforcing structural dependence on energy markets. Such feedstock sensitivity introduces cost unpredictability for glycol ether producers, complicating procurement planning and contract pricing. The resulting margin pressure is amplified by regional arbitrage and supply-demand imbalances, constraining stable adoption despite consistent end-use demand.

Opportunity

Expansion in High-Growth End-Use Industries in Emerging Markets Creates Opportunities in the Dipropylene Glycol N-Propyl Ether Market.

Accelerated industrialization across emerging economies is expanding the consumption base for high-performance solvents used in coatings, cleaning systems, and electronics processing. Government data indicate that electronics manufacturing alone is scaling rapidly. In India, output increased from INR 1.9 lakh crore in 2014-15 to INR 11.3 lakh crore in 2024-25, representing a six-fold expansion, alongside the creation of 2.5 million jobs in the same period. Parallel policy frameworks targeting domestic manufacturing have resulted in more than 300 mobile production units and large-scale component investments, reinforcing downstream demand for precision cleaning and formulation chemicals.

Infrastructure expansion is occurring simultaneously, with construction positioned as a core economic driver. The projections indicate that 50% of the population will be urbanized by 2046, supporting sustained growth in housing, logistics, and commercial assets. Engineering and capital goods sectors, which underpin automotive and industrial manufacturing, continue to benefit from policy-led investments and export activity exceeding US$100 billion annually.

These developments collectively increase demand for solvents capable of supporting coatings durability, surface preparation, and contamination control. The convergence of manufacturing scale-up, infrastructure buildout, and policy-backed industrial diversification provides a quantifiable foundation for expanded DPnP utilization across multiple high-growth end-use segments.

Trends

Shift Toward Water-Based and Environmentally Compatible Formulations.

Regulatory pressure on emissions and product safety is accelerating the transition toward water-based and environmentally compatible formulations across coatings and cleaning systems. Under the U.S. Clean Air Act framework, architectural and industrial coatings must comply with defined VOC content limits, with thresholds such as 250 g/L historically and as low as 50 g/L in stricter jurisdictions, compelling reformulation toward lower-emission systems.

In parallel, federal standards require manufacturers to document and control VOC emissions, reinforcing the adoption of compliant materials, including waterborne and high-solids coatings. Water-based coatings typically contain 5-40% organic co-solvent compared to significantly higher solvent fractions in conventional systems, resulting in materially reduced VOC emissions while maintaining application performance.

Within these systems, glycol ethers such as DPnP function as coalescing and coupling agents that stabilize resin dispersions and improve film formation, particularly in acrylic and polyurethane dispersions. Their relatively low volatility further contributes to delayed emission profiles, with co-solvents becoming dominant only after primary solvent evaporation phases.

The convergence of mandated reporting requirements and formulation constraints is systematically shifting solvent selection toward low-VOC, water-compatible chemistries, reinforcing the structural role of glycol ethers in compliant product systems.

Geopolitical Impact Analysis

Trade Route Fragility and Feedstock Disruption Dynamics in Glycol Ether Value Chains.

Heightened geopolitical friction across the Middle East and associated trade-route instability have introduced measurable stress across petrochemical value chains that supply intermediates such as propylene oxide and glycol ethers used in DPnP production. Maritime data indicates that the Strait of Hormuz handles the majority of global seaborne crude oil flows, alongside significant volumes of naphtha and LPG that feed steam crackers producing propylene derivatives.

Any restriction in this corridor has immediate upstream implications, as seen in reported rerouting of vessels and reduced tanker traffic, with shipping firms avoiding the passage due to elevated risk premiums and insurance costs. Propylene oxide and related intermediates recorded price increases during episodes of supply constraint driven by logistics disruption and crude feedstock escalation. Simultaneously, operating rates of Asian crackers have been reduced as naphtha deliveries face delays and force majeure declarations increase across supply contracts.

For glycol ether value chains, these disruptions propagate through higher propylene costs, extended lead times, and reduced spot availability of key intermediates. The effect is compounded by rerouted trade flows toward alternative suppliers, particularly from the U.S. Gulf Coast, where export activity has surged due to redirected demand. This rebalancing intensifies regional price differentials and creates intermittent shortages in importing markets.

The geopolitical instability is functioning less as a temporary shock and more as a recurring structural variable influencing feedstock accessibility, pricing volatility, and supply assurance for DPnP-linked chemical production.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Dipropylene Glycol N-Propyl Ether Market.

In 2025, Asia Pacific dominated the global dipropylene glycol n-propyl ether market, holding about 41.4% of the total global consumption, due to its large-scale integration of petrochemical production and downstream manufacturing intensity. The region holds demand, driven primarily by China, India, Japan, and South Korea, reflecting its concentration of coatings, electronics, and industrial cleaning applications. China represents the majority of regional solvent consumption, supported by its extensive coatings and electronics manufacturing base, where industrial solvent usage exceeds multi-million metric ton levels annually in broader chemical categories.

Strong output from construction and infrastructure development further reinforces demand, with India contributing largely to regional consumption, supported by rapid urbanization and expansion in paints and coatings use cases. Similarly, Japan and South Korea contribute to regional demand, largely influenced by high-precision electronics and semiconductor cleaning requirements, where solvent purity and performance consistency are critical.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of dipropylene glycol n-propyl ether concentrate on strengthening control over feedstock integration and production efficiency to stabilize output costs and ensure consistent supply. Many operators invest in backward integration into propylene oxide and related intermediates to reduce exposure to raw material volatility and secure long-term availability. Product differentiation is further prioritized through the development of high-purity and application-specific grades suited for coatings, electronics cleaning, and precision industrial uses.

Expansion of geographically diversified production facilities helps reduce logistics risks and improves responsiveness to regional demand fluctuations. Companies increasingly emphasize compliance with evolving environmental and safety regulations by optimizing low-VOC and low-toxicity product profiles. Strategic partnerships with downstream formulators and distributors support better alignment with end-use requirements and strengthen customer retention.

Key Development

- In March 2025, LyondellBasell announced an investment to expand propylene production capacity at its Channelview Complex near Houston.

The Major Players in The Industry

- Eastman Chemical Company

- Monument Chemical, LLC

- India Glycols Limited

- ADEKA Corporation

- Jiangsu Yida Chemical Co., Ltd.

- LyondellBasell Industries Holdings B.V.

- Midland Chemicals Ltd.

- Global Bio-Chem Technology Group Company Limited

- Manali Petrochemicals Limited

- Jiangsu Dynamic Chemical Co., Ltd.

- The Dow Chemical Company

- Other Key Players

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$5.8 Bn |

| Forecast Revenue (2035) | US$12.2 Bn |

| CAGR (2026-2035) | 7.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Formulation Type (Water Soluble, Oil Soluble, Emulsions, Aerosol, and Paste), By Application (Coatings, Cleaning Agents, Personal Care Products, Adhesives, and Industrial Solvents), By End-Use (Construction, Automotive, Household, Electronics, and Personal Care) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Eastman Chemical Company, Monument Chemical, LLC, India Glycols Limited, ADEKA Corporation, Jiangsu Yida Chemical Co., Ltd., LyondellBasell Industries Holdings B.V., Midland Chemicals Ltd., Global Bio-Chem Technology Group Company Limited, Manali Petrochemicals Limited, Jiangsu Dynamic Chemical Co., Ltd., The Dow Chemical Company, and Other Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |