Quick Navigation

Report Overview

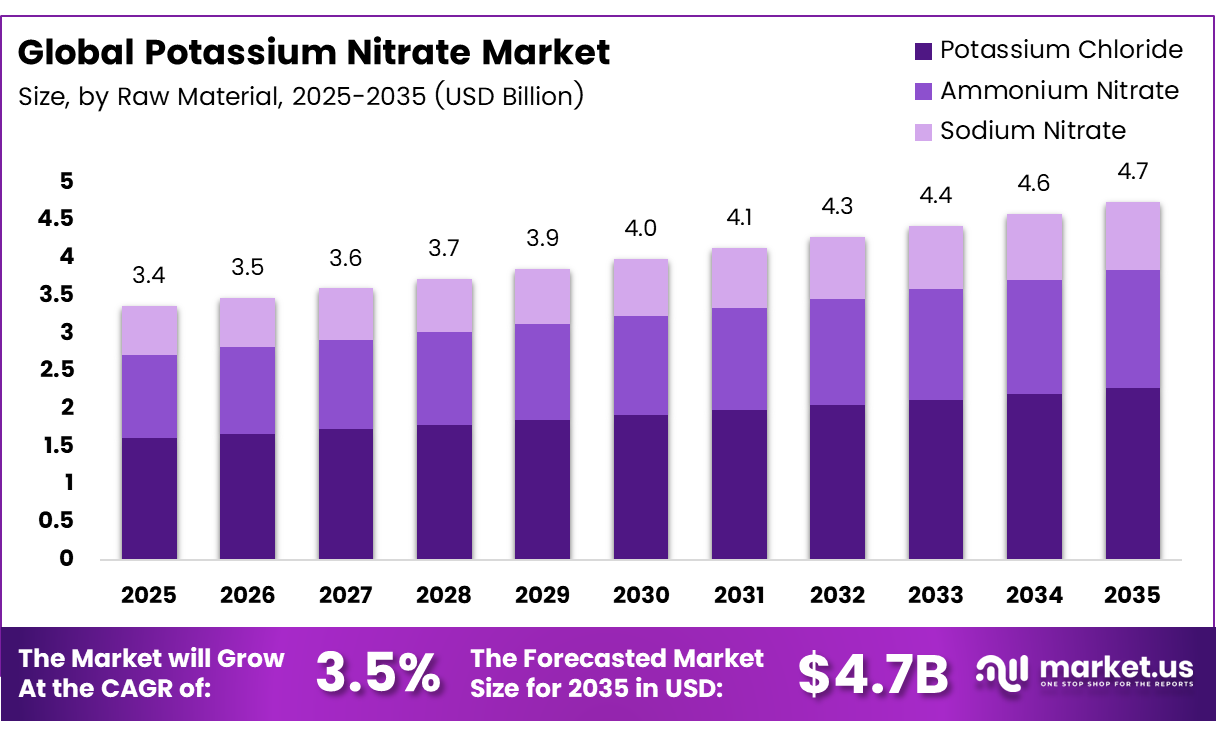

The Global Potassium Nitrate Market size is expected to be worth around USD 4.7 billion by 2035 from USD 3.4 billion in 2025, growing at a CAGR of 3.5% during the forecast period 2026 to 2035.

Potassium nitrate is a high-purity inorganic compound serving as a critical input across agriculture, explosives, glass manufacturing, pharmaceuticals, and food preservation. Its dual function as both a potassium and nitrogen source makes it irreplaceable in precision nutrient delivery systems. This combination positions it differently from single-nutrient fertilizers.

Agriculture commands the largest share of potassium nitrate consumption. Specialty crop growers, greenhouse operators, and hydroponic farmers choose it specifically because it delivers chloride-free nutrition. Chloride sensitivity in high-value crops such as fruits, vegetables, and tobacco makes potassium nitrate the preferred input over conventional fertilizers that risk yield damage.

Industrial-symbiosis KNO₃ production cut climate impact by 76.5% and reduced emissions from 2.37 to 0.56 kg CO₂-eq/kg, helping producers meet ESG procurement standards. The CORALIS process also lowered production costs by 82%, from €0.9228 to €0.1630 per kg, creating a major cost and competitive advantage over conventional methods.

Beyond agriculture, the compound serves as an oxidizing agent in mining explosives, a flux in glass and ceramics production, and a heat transfer medium in industrial processes. This multi-sector utility insulates the market from single-industry downturns. When one end-use softens, other sectors absorb demand shifts, creating structural resilience.

Key Takeaways

- The Global Potassium Nitrate Market is valued at USD 3.4 billion in 2025 and is forecast to reach USD 4.7 billion by 2035 at a CAGR of 3.5% from 2026 to 2035.

- Potassium Chloride leads with a 48.2% market share.

- Granular holds the top position with a 47.9% share.

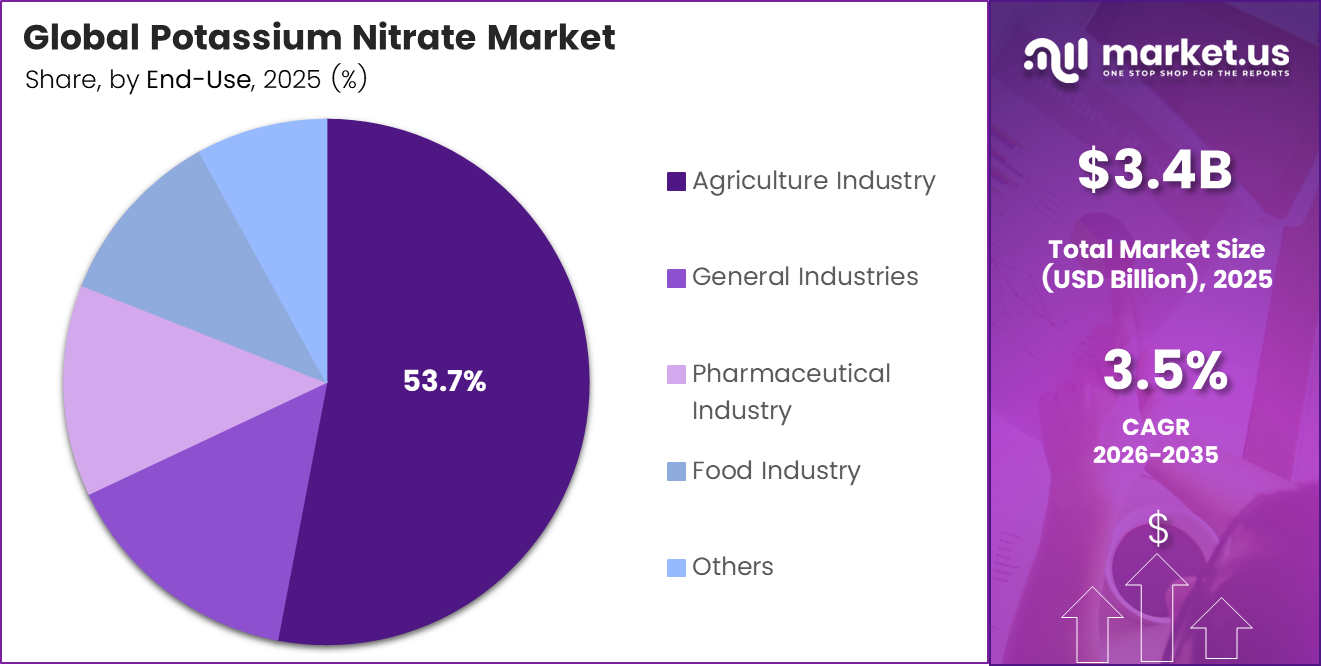

- The Agriculture Industry commands the largest share at 53.7%.

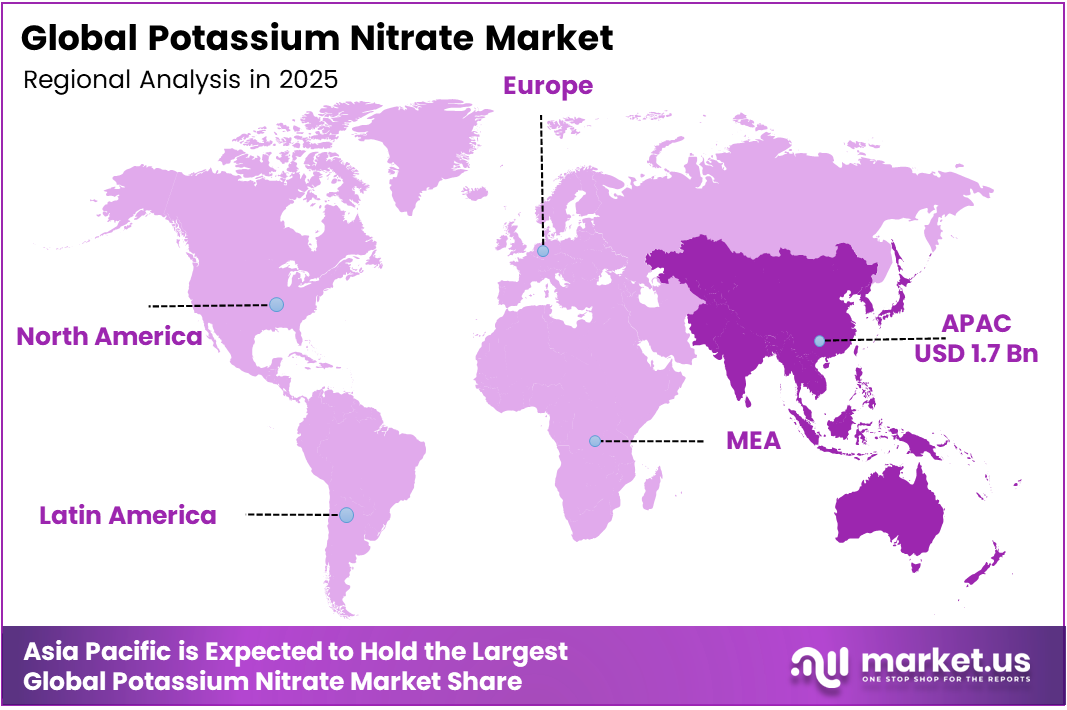

- Asia-Pacific holds the dominant regional share at 48.6%, valued at approximately USD 1.7 billion in 2025.

Raw Material Analysis

Potassium Chloride dominates with 48.2% due to an abundant global supply and low input cost.

In 2025, Potassium Chloride held a dominant market position in the By Raw Material segment of the Potassium Nitrate Market, with a 48.2% share. Its dominance reflects a cost-driven procurement logic: potassium chloride remains among the most widely mined and traded mineral inputs globally. Producers favor it because it lowers conversion costs compared to alternative raw materials, protecting margins in a price-sensitive fertilizer supply chain.

Ammonium Nitrate serves as the nitrogen donor in double-displacement synthesis routes that produce potassium nitrate without relying on chloride chemistry. Manufacturers use this pathway primarily when end-product purity requirements are higher, particularly for pharmaceutical and food-grade applications. However, its use carries tighter regulatory burdens due to explosive classification, limiting its share among smaller regional producers.

Formulation Analysis

Granular dominates with 47.9% due to ease of application and broad crop compatibility.

In 2025, Granular held a dominant market position in the By Formulation segment of the Potassium Nitrate Market, with a 47.9% share. Granular formulations dominate because they serve traditional broadcast and soil-application methods that most field crop producers already operate. Their handling simplicity, storage stability, and compatibility with standard spreading equipment reduce the adoption barrier for smallholder and mid-scale farming operations globally.

Liquid formulations carry the highest growth trajectory within the formulation segment. Fertigation and hydroponic systems require fully soluble nutrient inputs that integrate directly into irrigation lines, and liquid potassium nitrate eliminates the dissolution step. As greenhouse and vertical farming infrastructure scales across Asia and Europe, liquid formulations gain structural tailwinds that granular products cannot access through conventional distribution channels.

End-Use Analysis

The agriculture industry dominates with 53.7% due to the demand for chloride-free nutrition in specialty crops.

In 2025, the Agriculture Industry held a dominant market position in the By End-Use segment of the Potassium Nitrate Market, with a 53.7% share. High-value crop producers — spanning fruits, vegetables, flowers, and tobacco — choose potassium nitrate specifically to avoid chloride toxicity that damages sensitive root systems. This agronomic necessity, rather than price preference, locks in demand and creates a defensible consumption base that persists regardless of commodity fertilizer price cycles.

General Industries encompasses mining, explosives manufacturing, glass production, ceramic firing, and heat transfer applications. These industries rely on potassium nitrate as an oxidizing compound and molten salt medium. Industrial demand provides a stable counterweight to agricultural seasonality, ensuring year-round production utilization for manufacturers serving both segments simultaneously.

Key Market Segments

By Raw Material

- Potassium Chloride

- Ammonium Nitrate

- Sodium Nitrate

By Formulation

- Granular

- Liquid

- Powder

By End-Use

- Agriculture Industry

- General Industries

- Pharmaceutical Industry

- Food Industry

- Others

Emerging Trends

Chloride-Free and Smart Fertigation Solutions Reshape Potassium Nitrate Consumption Patterns

Commercial agriculture producers are shifting away from chloride-containing fertilizers at a measurable rate. Chloride-sensitive crops, including tomatoes, peppers, and berries, suffer yield losses under conventional NPK regimens. This agronomic reality converts chloride-free potassium nitrate from a premium option into an operational requirement for growers supplying export and premium retail markets.

Smart irrigation and fertigation technology adoption accelerates potassium nitrate consumption in ways that traditional broadcast application cannot. Drip irrigation systems paired with soluble nutrient dosing equipment require fully water-soluble inputs delivered in precise concentrations. Industrial-symbiosis production processes cut fossil-resource scarcity impact by 77.9%, meaning greener supply chains now align directly with buyer sustainability mandates.

Strategic collaborations between fertilizer manufacturers and agri-tech firms are accelerating the development of customized nutrient blends built around soluble potassium nitrate. These partnerships allow agri-tech platforms to offer data-driven nutrient prescription services where potassium nitrate dosing adjusts in real time based on soil sensors and crop models. Early movers in this space gain long-term supply agreements that commodity fertilizer producers cannot replicate through price competition alone.

Drivers

Specialty Crop Agriculture and Industrial Expansion Drive Structural Potassium Nitrate Demand

High-value crop cultivation requires chloride-free potassium and nitrogen inputs that conventional fertilizers cannot safely deliver. As precision agriculture adoption expands across Asia, Latin America, and the Mediterranean, growers of fruits, vegetables, and flowers consistently select potassium nitrate over alternative fertilizers. This agronomic specification requirement, not price sensitivity, anchors long-term agricultural demand. New production processes cut water consumption by 82.6%, from 0.0605 to 0.0105 m³ per kg KNO₃, making sustainable supply chains commercially viable at scale.

Mining, quarrying, and infrastructure development consume potassium nitrate as an oxidizing agent in explosive formulations. Infrastructure build-out programs across Southeast Asia, Africa, and the Middle East sustain industrial-grade demand independent of agricultural cycles. Consequently, producers serving both agricultural and industrial channels gain revenue diversification that single-market competitors cannot match, reducing exposure to sector-specific demand contractions.

Greenhouse farming and controlled environment agriculture operators specifically require fully soluble nutrient inputs compatible with automated fertigation systems. Sustainability confirmed that industrial-symbiosis potassium nitrate production cut total environmental externality costs by 76.9%, from €0.3545 to €0.0819 per kg KNO₃, providing producers with a quantified ESG credential that supports access to sustainability-linked supply contracts with multinational buyers.

Restraints

Raw Material Price Volatility and Hazardous Chemical Regulations Constrain Market Expansion

Potassium chloride and energy costs represent the two largest input cost components in potassium nitrate manufacturing. Both are subject to swings in commodity markets driven by geopolitical supply disruptions, freight rate changes, and energy price shocks. When input costs spike, smaller regional producers face margin compression that they cannot pass through to agricultural buyers operating on fixed seasonal budgets, forcing temporary capacity reductions.

Potassium nitrate carries a dual-use classification in many jurisdictions due to its role in explosive formulations. This classification triggers storage quantity limits, transportation permits, end-use reporting requirements, and facility inspection obligations. The CORALIS industrial-symbiosis KNO₃ process delivered a total OPEX reduction from €437.50 million to €10.04 million over a 30-year lifecycle, demonstrating that circular production methods for potassium nitrate are commercially viable at an industrial scale and not just theoretically sustainable.

Cross-border trade in potassium nitrate faces compound regulatory friction — export controls, import licensing, and customs security documentation requirements vary significantly across jurisdictions. Manufacturers serving global markets must navigate inconsistent regulatory frameworks that delay shipments, increase logistics costs, and limit market responsiveness. These friction points slow the speed at which supply can adjust to geographic demand shifts, creating periodic regional supply imbalances.

Growth Factors

Developing Market Fertigation Adoption and High-Purity Production Advances Unlock New Revenue Streams

Agricultural economies across South Asia, Sub-Saharan Africa, and Southeast Asia are adopting fertigation infrastructure at scale, supported by government irrigation modernization programs. These markets represent structurally underpenetrated demand for potassium nitrate-based nutrient products. As drip irrigation coverage expands in India, Bangladesh, and Vietnam, soluble fertilizer consumption follows, creating multi-year volume growth for producers that establish distribution in these corridors early.

Sustainable agriculture programs funded by multilateral development institutions are promoting nutrient-efficient delivery methods that reduce soil degradation and groundwater contamination. Potassium nitrate’s high nutrient efficiency per unit applied aligns precisely with these program objectives. The total life-cycle cost of industrial-symbiosis production declined 77.7%, from €0.9241 to €0.2058 per kg, demonstrating that sustainable production methods now offer genuine cost competitiveness rather than just environmental credentials.

Hydroponics and vertical farming represent the fastest-scaling new consumption channel for soluble potassium nitrate. Urban farming ventures in the Middle East, Japan, and the Netherlands are investing in large-format indoor production facilities that depend entirely on precisely formulated water-soluble nutrient solutions. Simultaneously, pharmaceutical manufacturers are investing in high-purity potassium nitrate supply chains for drug intermediate synthesis, adding a premium-margin end-use segment that agricultural-grade producers are not yet equipped to serve.

Regional Analysis

Asia-Pacific Dominates the Potassium Nitrate Market with a Market Share of 48.6%, Valued at USD 1.7 Billion

Asia-Pacific commands 48.6% of the global market, valued at approximately USD 1.7 billion in 2025. China and India drive this dominance through the intersection of large-scale agricultural output, expanding greenhouse infrastructure, and domestic mining activity requiring industrial-grade explosive inputs. The region’s combination of production scale and consumption volume creates a self-reinforcing demand concentration that other regions will not displace within the forecast period.

North America maintains a mature but strategically significant market position, anchored by precision agriculture adoption in the US and Canada. Commercial greenhouse operators, berry growers, and controlled environment agriculture companies in this region specify chloride-free soluble fertilizers as standard practice. Regulatory frameworks around hazardous chemical handling are well-established, reducing compliance uncertainty for producers and distributors operating at an industrial scale.

Europe applies the strictest environmental standards on fertilizer inputs globally, creating a structural advantage for high-purity, low-emission potassium nitrate producers. The EU’s Farm to Fork Strategy actively promotes reduced synthetic nutrient inputs, but simultaneously pushes adoption toward nutrient-efficient compounds — a policy dynamic that favors precision-application potassium nitrate over bulk conventional alternatives across the Netherlands, Spain, and Italy.

Latin America presents an expanding consumption base tied to Brazil and Mexico’s growth in export-oriented horticulture. Producers supplying European and North American fresh produce markets face increasingly strict residue and input traceability requirements, pushing farms toward certified chloride-free fertilizer programs. Fertigation infrastructure investment in Chile and Peru further extends the addressable market for soluble potassium nitrate beyond traditional field application.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Haifa Group positions itself as a specialty nutrition company rather than a commodity fertilizer producer — a distinction that matters commercially. By focusing on fully soluble, chloride-free formulations for high-value crops and fertigation systems, Haifa targets buyer segments where performance specifications, not price, determine supplier selection. This positioning insulates it from commodity pricing pressure that affects producers competing on bulk volume alone.

Migao Corporation leverages vertically integrated potassium compound production in China to maintain cost advantages in the world’s largest potassium nitrate consumption market. Its upstream integration into raw material sourcing reduces exposure to potassium chloride spot price volatility that squeezes standalone formulators. This structural cost position allows Migao to compete on price in high-volume agricultural segments while maintaining capacity utilization across market cycles.

SQM S.A. holds a strategically rare position as both a potassium nitrate producer and a natural iodine and lithium resource owner in Chile’s Atacama Desert. Its access to natural nitrate deposits provides a distinct raw material pathway that synthetic producers cannot replicate. This resource advantage gives SQM defensible supply security and a lower-carbon production profile increasingly valued by European and North American buyers under sustainability procurement frameworks.

Yara applies its global crop nutrition infrastructure to position potassium nitrate within broader precision farming solution packages rather than selling it as a standalone input. By bundling fertilizer supply with agronomic advisory services and digital crop monitoring tools, Yara builds multi-year farmer relationships that reduce customer churn and support premium pricing. This integrated service model creates competitive barriers that pure-play potassium nitrate producers cannot easily overcome.

Key Players

- Haifa Group

- Migao Corporation

- SQM S.A.

- Yara

- ANISH CHEMICALS

- SNDB

- RAM SHREE CHEMICALS

- YOGI CHEMICAL INDUSTRIES

- Ravi Chem Industries

- Akshay Group of Companies

- Uma Organics

- Sam Industries

- Jagannath Chemicals

- A.G.I. Industries

Recent Developments

- In 2025, Haifa continues to position Multi-K potassium nitrate as a core specialty fertilizer. Recent ESG actions tied to its nitrate value chain include 2024–2030 optimization to reduce N₂O emissions from its nitric acid plant, a 2025 switch from Freon to ammonia coolant, and planned renewable-energy expansion at Haifa Negev.

- In 2024, Migao updated its New Sichuan Production Facility plan: the intended facility included 8 SOP lines, 1 NOP/potassium nitrate line, and 1 compound fertilizer line, but the original Mianyang location became infeasible after stricter ecological zoning controls; Migao said it would reassess feasibility/location.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 3.4 Billion |

| Forecast Revenue (2035) | USD 4.7 Billion |

| CAGR (2026-2035) | 3.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Raw Material (Potassium Chloride, Ammonium Nitrate, Sodium Nitrate), By Formulation (Granular, Liquid, Powder), By End-Use (Agriculture Industry, General Industries, Pharmaceutical Industry, Food Industry, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Haifa Group, Migao Corporation, SQM S.A., Yara, ANISH CHEMICALS, SNDB, RAM SHREE CHEMICALS, YOGI CHEMICAL INDUSTRIES, Ravi Chem Industries, Akshay Group of Companies, Uma Organics, Sam Industries, Jagannath Chemicals, A.G.I. Industries |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |