Quick Navigation

Report Overview

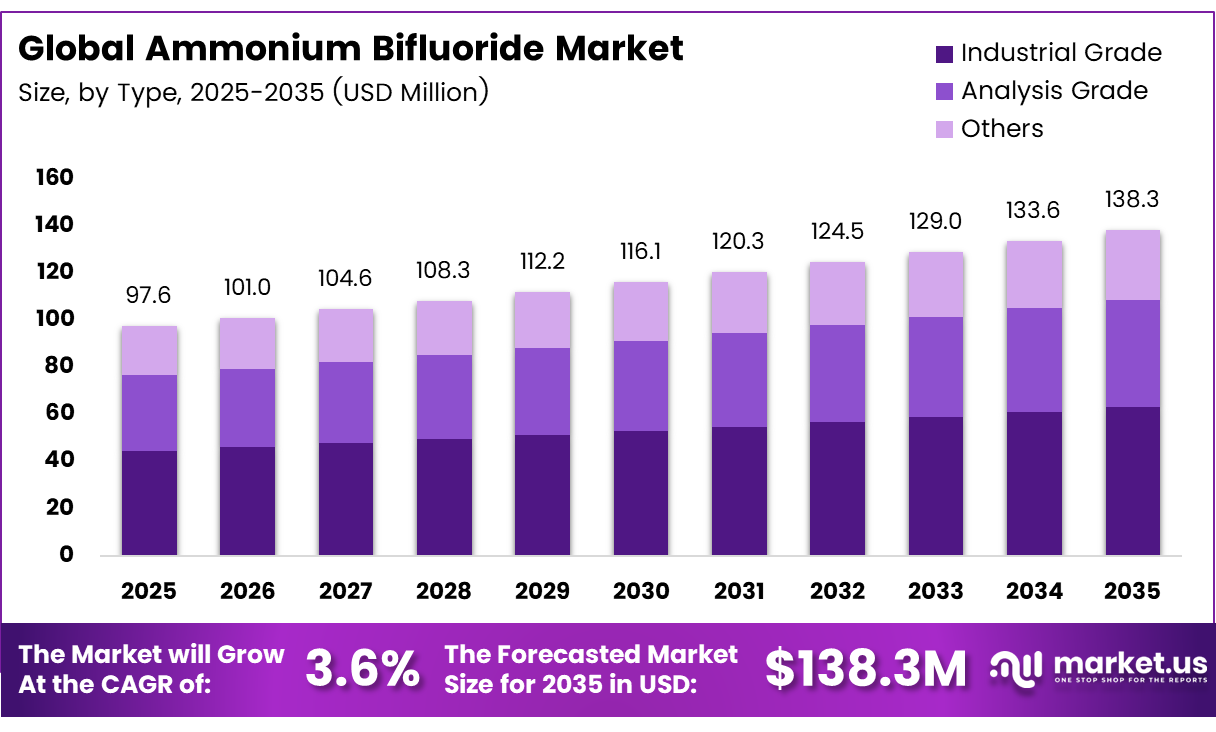

The Global Ammonium Bifluoride Market size is expected to be worth around USD 138.3 million by 2035 from USD 97.6 million in 2025, growing at a CAGR of 3.6% during the forecast period 2026 to 2035.

Ammonium bifluoride (NH4HF2) is a fluoride-based inorganic compound used for etching, metal treatment, and industrial preservation. Its ability to dissolve silica and oxide layers makes it a safer, more controllable alternative to hydrofluoric acid in industries such as electronics, glass processing, stainless-steel cleaning, and oilfield drilling, supporting steady market demand and growth.

Using ammonium bifluoride instead of hydrofluoric acid can reduce operational costs by 10–15%, providing procurement managers with a clear financial incentive to shift away from more hazardous fluoride chemicals. In equivalent working mixtures, ammonium bifluoride requires 1.55× less material than 45% hydrofluoric acid, lowering both procurement costs and hazardous material handling exposure. These advantages are accelerating adoption in regulated industrial environments with strict safety and compliance requirements.

Ammonium bifluoride specifications now require a minimum assay of 98%, with non-volatile matter and sulphate each limited to 0.05%. Additional impurity controls include chloride at 0.002%, iron at 0.005%, and lead capped at 0.01%. These stricter purity standards reflect growing demand from electronics, semiconductor, pharmaceutical, and precision engineering industries for highly consistent industrial-grade materials.

In metal finishing, aluminum brightener formulations commonly contain 28 wt% ammonium bifluoride and 72 wt% water, with moisture content controlled at 0.59% to ensure consistent surface treatment performance. Separately, CDH Fine Chemical confirms a minimum 98.0% assay by acidimetric method for commercial ammonium bifluoride supplies, providing buyers with a standardized and auditable quality benchmark for global procurement and supplier qualification.

Key Takeaways

- The Global Ammonium Bifluoride Market was valued at USD 97.6 million in 2025 and is projected to reach USD 138.3 million by 2035. at a CAGR of 3.6% during the forecast period 2026 to 2035.

- Industrial Grade dominates with a 67.2% market share in 2025.

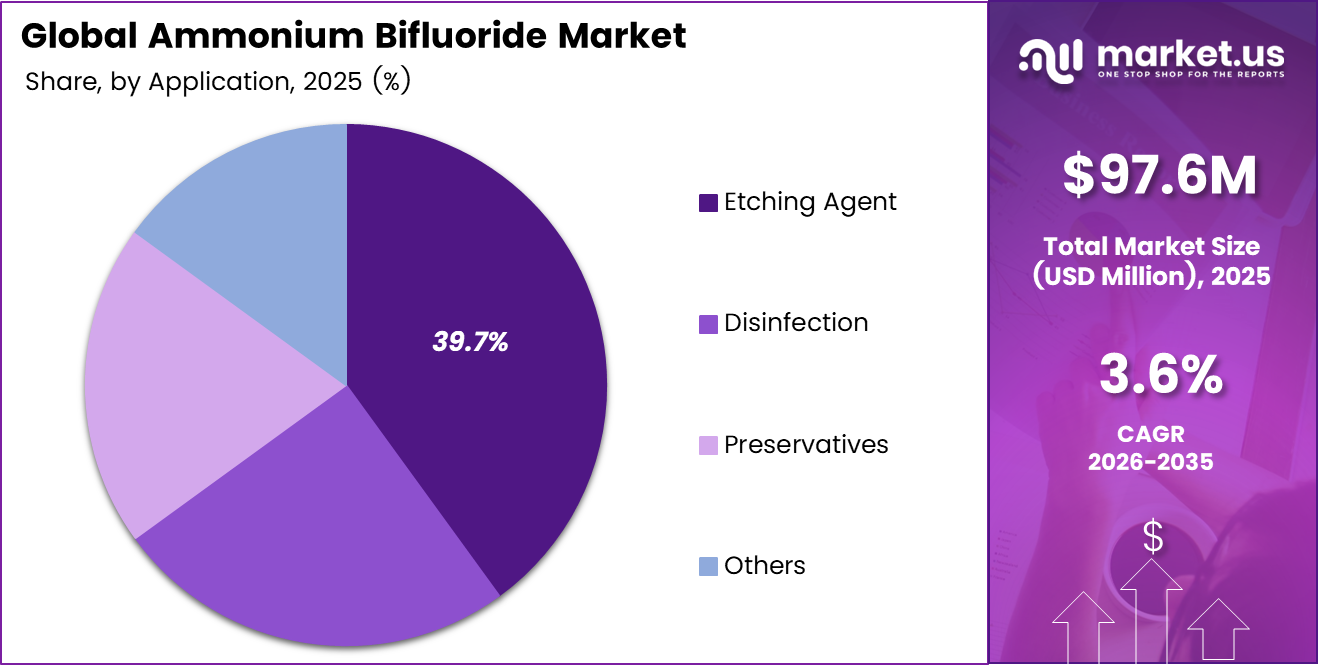

- Etching Agent leads with a 39.7% share of total market consumption.

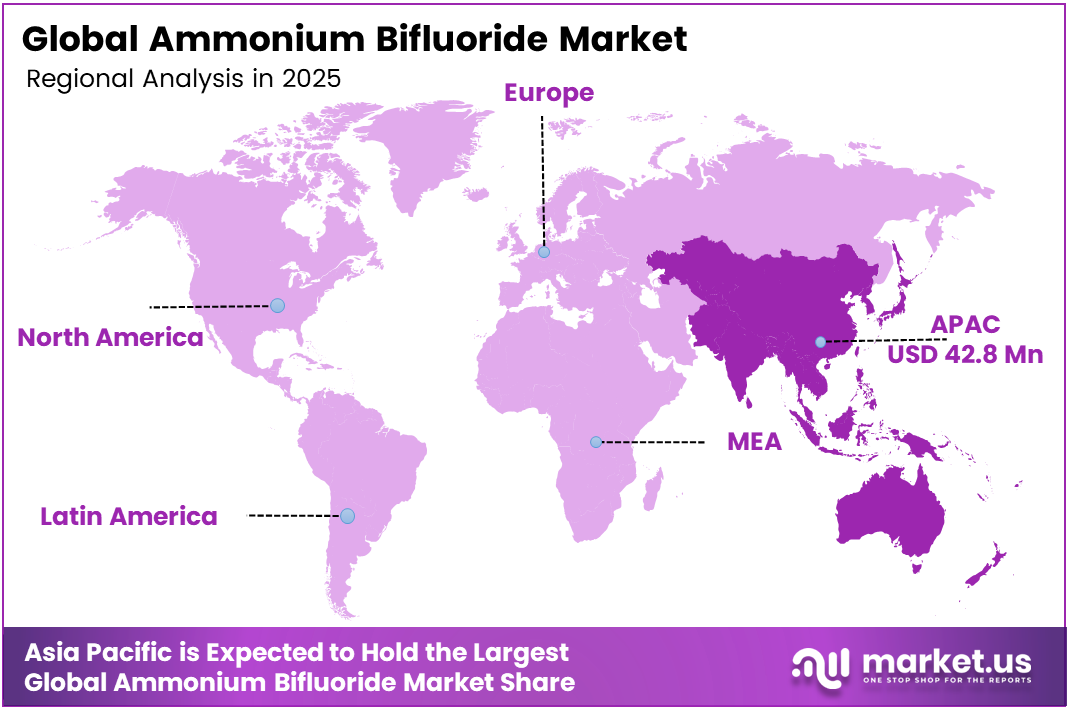

- Asia-Pacific holds the largest regional share at 43.9%, valued at USD 42.8 million in 2025.

Type Analysis

Industrial Grade dominates with 67.2% due to bulk demand across etching and surface treatment.

In 2025, Industrial Grade held a dominant market position in the By Type segment of the Ammonium Bifluoride Market, with a 67.2% share. Bulk procurement from glass etching, metal treatment, and oilfield operations drives this concentration. Buyers in these sectors prioritize cost efficiency and consistent supply volume over purity specification, which structurally favors industrial-grade producers.

Analysis Grade serves the segment where process sensitivity demands tighter chemical specifications. Semiconductor fabrication and precision laboratory applications require controlled impurity levels, making analysis-grade ammonium bifluoride a higher-margin niche. However, this segment represents a smaller share of total volume, meaning suppliers must balance production economics carefully to justify the added purification investment.

Application Analysis

Etching Agent dominates with 39.7% due to high-volume electronics and glass manufacturing demand.

In 2025, Etching Agent held a dominant market position in the By Application segment of the Ammonium Bifluoride Market, with a 39.7% share. Electronics manufacturers and architectural glass processors rely on fluoride-based etching for precise surface modification. This structural dependency on glass and semiconductor production volumes makes the etching agent segment the most volume-consistent revenue driver in the market.

Disinfection applications use ammonium bifluoride as an antimicrobial agent in industrial and water treatment contexts. This application category benefits from its broad-spectrum efficacy against bacteria and algae in industrial water systems. However, substitution risk from alternative biocides remains a constraint, meaning disinfection volumes depend on cost and regulatory positioning relative to competing chemistries.

Preservatives represent the application of ammonium bifluoride in wood treatment and anti-corrosion formulations, where fluoride chemistry slows biological and chemical degradation. This use case is sensitive to construction sector cycles and environmental regulations governing fluoride runoff. Consequently, preservative demand tracks closely with infrastructure investment patterns in key manufacturing economies.

Key Market Segments

By Type

- Industrial Grade

- Analysis Grade

- Others

By Application

- Etching Agent

- Disinfection

- Preservatives

- Others

Emerging Trends

High-Purity Grades and Automated Handling Systems Redefine Industrial Fluoride Standards

Electronics and semiconductor manufacturers now specify ammonium bifluoride with tighter impurity thresholds, pushing suppliers toward high-purity production. A January 2025 specification confirms a minimum assay at 98.0% by the acidimetric method. This precision standard signals that buyers in sensitive process industries no longer accept broad-tolerance grades.

Industrial processors also shift toward automated chemical dispensing and storage systems to reduce human exposure to fluoride compounds. This operational change reflects both safety compliance pressure and a desire for process consistency. Suppliers that develop compatible packaging and delivery formats gain preferential access to automated production facilities.

Chemical manufacturers and electronics suppliers increasingly enter formal collaboration agreements to co-develop application-specific fluoride formulations. These partnerships compress product development cycles and align chemical specifications directly to end-use process requirements, reducing qualification time for new grades and creating stickier commercial relationships between producers and industrial buyers.

Drivers

Electronics Etching and Industrial Surface Treatment Demand Positions Ammonium Bifluoride as a Critical Process Chemical

Glass etching in electronics and architectural applications requires precise chemical control, which ammonium bifluoride delivers more safely than hydrofluoric acid alternatives. Semiconductor manufacturers and display glass producers consistently specify fluoride-based etching agents because surface quality directly affects device yield and product performance. This technical dependency creates durable, non-discretionary demand.

Metal surface treatment operations — including stainless-steel cleaning and aluminum brightening — consume ammonium bifluoride at scale. The minimum assay reaches 98%, confirming that industrial suppliers now routinely deliver high-specification products. This quality consistency reduces rejection rates and strengthens supplier credibility with quality-sensitive metal fabrication customers.

Oilfield drilling, mining, and mineral processing operations use fluoride chemicals to dissolve silicate scales and improve extraction efficiency. The RXSOL cost reduction data — showing 10–15% savings versus hydrofluoric acid — gives procurement teams in capital-intensive extraction industries a measurable financial reason to adopt ammonium bifluoride formulations, which reinforces volume growth across this application cluster.

Restraints

Regulatory Compliance Costs and Raw Material Volatility Compress Margins for Fluoride Chemical Producers

Ammonium bifluoride’s CERCLA/SARA reportable quantity is 100 lb (45.4 kg). This low threshold means even modest handling incidents trigger mandatory regulatory reporting, adding compliance overhead that smaller producers struggle to absorb. Consequently, regulatory burden consolidates market participation toward larger, better-resourced chemical manufacturers.

Transport classification under UN 1727 and IMDG Class 8 Packing Group II adds logistics cost and restricts carrier options across international supply chains. Manufacturers must invest in certified packaging, trained handling personnel, and documentation systems. These non-negotiable compliance costs raise the effective delivered cost of ammonium bifluoride, limiting price competitiveness versus less-regulated chemical alternatives in cost-sensitive markets.

Raw material supply chain volatility further pressures producer economics. Fluorite ore pricing and ammonia costs — the primary feedstocks for ammonium bifluoride production — fluctuate with energy markets and mining output cycles. When input costs rise, producers face a margin squeeze because long-term supply contracts with industrial buyers typically limit their ability to pass costs through quickly.

Growth Factors

Renewable Energy Processing, Aerospace Cleaning, and Developing Economy Industrialization Open New Revenue Channels

Solar glass manufacturers require fluoride-based etching to achieve anti-reflective surface properties that improve photovoltaic panel efficiency. This application connects ammonium bifluoride demand directly to solar energy capacity expansion, a capital investment cycle that runs independently of traditional industrial output. Suppliers positioned early in solar supply chains capture long-term specification advantages as panel production scales.

Aerospace and automotive manufacturers invest in advanced industrial cleaning solutions where conventional acids create unacceptable material compatibility risks. Ammonium bifluoride dissolves in water at 60.2 g/100 mL at 20°C, enabling precise concentration control in cleaning baths. This high and predictable solubility supports formulation consistency across automated cleaning systems used in precision manufacturing environments.

Developing economies across Southeast Asia, South Asia, and Latin America expand industrial processing capacity in metals, construction materials, and electronics assembly. This industrialization wave creates new downstream demand for surface treatment and etching chemicals. Fluoride chemical producers that establish regional distribution partnerships ahead of this build-out secure first-mover supply chain positioning in markets where local sourcing infrastructure remains underdeveloped.

Regional Analysis

Asia-Pacific Dominates the Ammonium Bifluoride Market with a Market Share of 43.9%, Valued at USD 42.8 Million

Asia-Pacific controls 43.9% of the global ammonium bifluoride market, valued at USD 42.8 million in 2025. China, Japan, and South Korea drive this share through their concentrated electronics manufacturing ecosystems. The density of semiconductor fabs, display panel plants, and precision metal processing facilities in this region creates structural, recurring demand for high-specification fluoride etching chemicals.

North America represents a mature market anchored by oilfield services, aerospace manufacturing, and semiconductor fabrication. Strict CERCLA/SARA regulatory thresholds — such as the 100 lb reportable quantity — shape procurement decisions toward compliant, certified suppliers. This regulatory discipline consolidates North American sourcing around established chemical distributors with certified hazardous material handling infrastructure.

Europe’s ammonium bifluoride consumption concentrates in glass processing, specialty chemical manufacturing, and precision engineering sectors in Germany, France, and the UK. REACH compliance requirements and IMDG Class 8 transport rules enforce stringent supplier qualification standards. These conditions create a relatively high-barrier procurement environment that favors suppliers with full European regulatory certification and established distribution networks.

The Middle East and Africa region uses ammonium bifluoride primarily in oilfield acid stimulation and mineral processing operations. GCC countries with active oil and gas extraction programs represent the primary consumption centers. Infrastructure investment in petrochemical and mining processing facilities supports measured volume growth, though limited local production capacity means the region depends on imports from Asian and European chemical producers.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

DERIVADOS DEL FLUOR, S.A. operates as a vertically integrated fluorine chemistry specialist with deep expertise in fluoride compound manufacturing. Its strategic advantage lies in controlling upstream fluorite processing, which insulates margins from spot market raw material volatility. This integration positions the company as a reliable long-term supplier for procurement teams managing strict industrial quality and continuity requirements.

Dongyue Group Limited leverages its scale in China’s fluorochemical industry to serve both domestic and export markets with cost-competitive ammonium bifluoride supply. The company’s proximity to Asia-Pacific’s electronics manufacturing cluster provides logistical and lead-time advantages over Western competitors. This geographic alignment with the market’s dominant regional demand center reinforces its volume position across etching and surface treatment applications.

Honeywell International Inc. brings advanced specialty chemical manufacturing capability and a broad industrial distribution network to the ammonium bifluoride supply landscape. Its established relationships with aerospace, semiconductor, and oil & gas customers allow it to position high-purity fluoride grades as validated process chemicals. This technical credibility reduces customer qualification cycles and supports premium pricing relative to commodity-grade suppliers.

Fluoro Chemicals focuses on fluoride compound production with applications spanning industrial cleaning, metal treatment, and chemical intermediates. Its competitive positioning centers on application-specific grade development, enabling it to serve niche industrial buyers who require custom formulations beyond standard industrial specifications. This specialization strategy reduces direct price competition with high-volume commodity producers and supports higher per-unit margins.

Key Players

- DERIVADOS DEL FLUOR, S.A.

- Dongyue Group Limited

- Honeywell International Inc.

- Fluoro Chemicals

- Halliburton Company

- Zhejiang Sanmei Chemical Industry Co., Ltd.

- Shanghai Yixin Chemical Co., Ltd.

- Jay Intermediates & Chemicals

- Shaowu Huaxin Chemical Co, Ltd.

- Solvay S.A.

Recent Developments

- In 2026, Halliburton’s release reported $5.4 billion in revenue, 13% operating margin, and $123 million in free cash flow; Completion and Production revenue fell 3% YoY, partly due to lower stimulation activity in North America. A Halliburton-related 2025 patent publication describes one-step treatment compositions using acid/ammonium salt, an HF source, and a fluoride scale inhibitor for treatment operations.

- In 2025, Fluoro Chemicals, Vapi, is listed as established in 1988 and as a processor/supplier/exporter of inorganic fluorine and allied chemicals, using inputs including hydrofluoric acid. Fluoro Chemicals is listed in Vapi, Gujarat, as offering Ammonium Bifluoride F2H5N, MOQ 500 kg.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 97.6 Million |

| Forecast Revenue (2035) | USD 138.3 Million |

| CAGR (2026-2035) | 3.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Industrial Grade, Analysis Grade, Others), By Application (Etching Agent, Disinfection, Preservatives, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | DERIVADOS DEL FLUOR, S.A., Dongyue Group Limited, Honeywell International Inc., Fluoro Chemicals, Halliburton Company, Zhejiang Sanmei Chemical Industry Co. Ltd., Shanghai Yixin Chemical Co. Ltd., Jay Intermediates & Chemicals, Shaowu Huaxin Chemical Co Ltd., Solvay S.A. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |