Quick Navigation

Report Overview

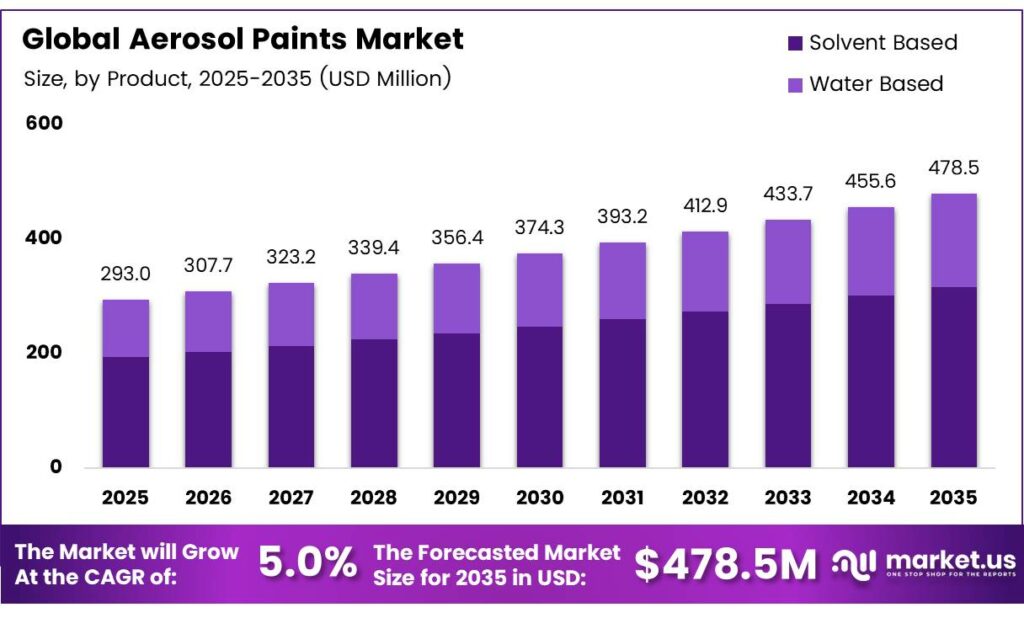

The Global Aerosol Paints Market size is expected to be worth around USD 478.5 million by 2035 from USD 293.0 million in 2025, growing at a CAGR of 5.0% during the forecast period 2026 to 2035.

Aerosol paints are pressure-packaged coating systems that deliver consistent, fine-mist coverage across automotive, construction, and furniture surfaces. Their convenience over brush-applied alternatives makes them a standard tool for both professional refinishers and DIY users. This dual demand base gives the market structural stability that purely industrial coatings categories rarely enjoy.

The National VOC Emission Standards for Aerosol Coatings, the default aerosol coating reactivity factor was reset to 18.50 grams of ozone per gram of VOC. This signals that prior compliance thresholds were set too loosely, meaning a meaningful portion of existing solvent-based aerosol formulations must now be reformulated to remain market-legal.

The Shellac Sealers aerosol category faces a limit of 1.00 g O₃/g VOC, one of the tightest category-specific thresholds in the revised standard. This forces specialty aerosol producers serving the shellac sealer niche to rebuild formulations from the ground up, compressing margins in the short term but creating a barrier that protects compliant producers from lower-cost competition.

The transition toward water-based aerosol formulations accelerates as compliance timelines shorten. Producers investing early in low-VOC chemistry gain a pricing premium over solvent-based competitors who face reformulation costs. For investors, this regulatory-driven product cycle represents a defined catalyst — not an open-ended trend — with measurable timelines attached to new product revenue.

Key Takeaways

- The Global Aerosol Paints Market was valued at USD 293.0 million in 2025 and is forecast to reach USD 478.5 million by 2035, growing at a CAGR of 5.0% from 2026 to 2035.

- Solvent-based holds the leading share at 67.1% of the total market volume.

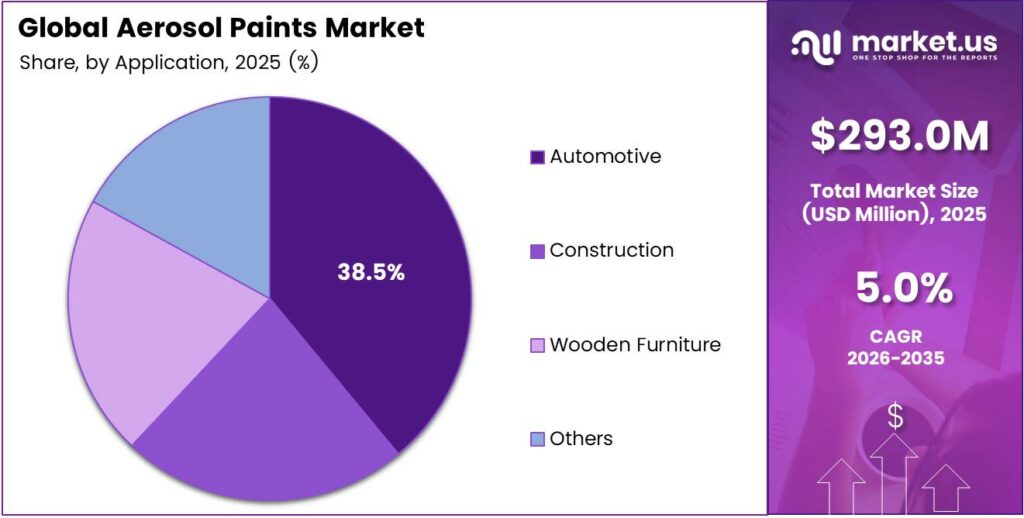

- Automotive leads with a 38.5% share, reflecting strong demand from vehicle refinish and repair channels.

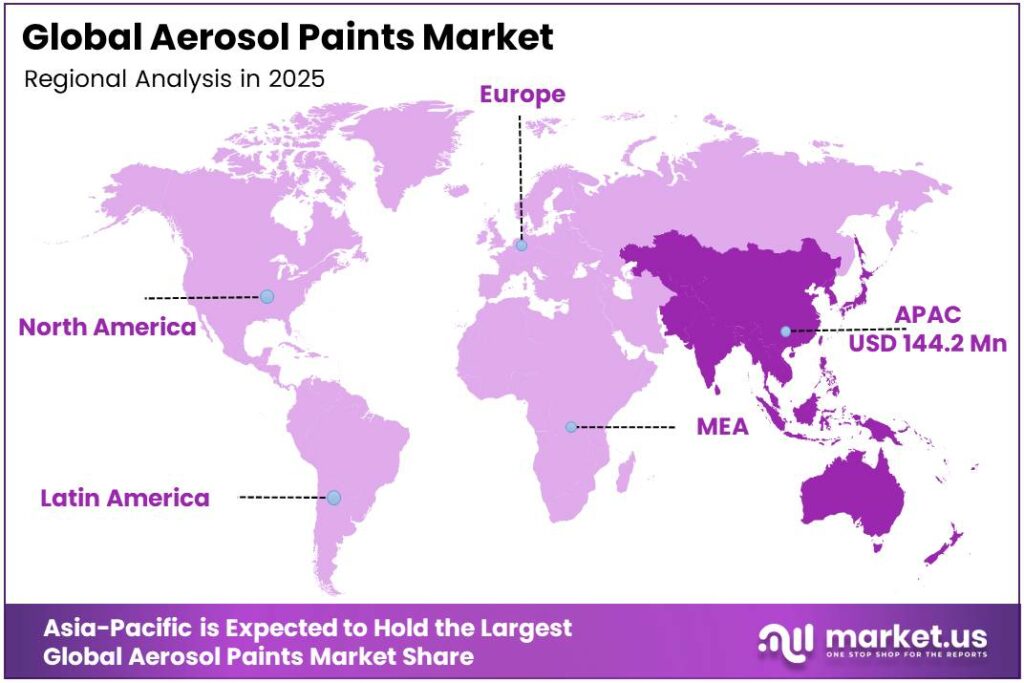

- Asia-Pacific dominates regionally with a 49.2% share, valued at approximately USD 144.2 million.

Product Analysis

Solvent-based dominates with 67.1% due to superior adhesion and fast dry performance.

In 2025, Solvent-based aerosol paints held a dominant market position in the by-product segment of the Aerosol Paints Market, with a 67.1% share. Solvent-based chemistry delivers faster dry times, stronger adhesion to metal and plastic, and broader temperature tolerance — attributes that automotive refinishers and industrial applicators consistently prioritize over cost or environmental considerations.

Water-based aerosol paints serve as the compliance-driven alternative for buyers operating under VOC restrictions. Their share remains below solvent-based formats today, but tightening EPA and EU emission standards are redirecting new product development budgets toward water-based lines.

Application Analysis

Automotive dominates with 38.5% due to high refinish and spot-repair volume.

In 2025, Automotive held a dominant market position in the By Application segment of the Aerosol Paints Market, with a 38.5% share. Body shops, collision repair centers, and individual vehicle owners rely on aerosol formats for panel color matching, primer application, and protective coatings — a usage pattern that generates repeat purchases and sustains consistent commercial volume across economic cycles.

Construction applications cover structural steel protection, masonry marking, and site equipment identification. This segment benefits from large project volumes in Asia-Pacific and the Middle East, where ongoing infrastructure build-out keeps aerosol paint consumption elevated.

Wooden Furniture coatings represent a specialized niche where finish quality and grain clarity drive purchase decisions rather than price. Aerosol formats allow furniture manufacturers and restoration professionals to apply thin, even coats without spray equipment investment. Consequently, this sub-segment commands higher per-unit margins than commodity aerosol categories, making it attractive for premium coating brands.

Key Market Segments

By Product

- Solvent Based

- Water Based

By Application

- Automotive

- Construction

- Wooden Furniture

- Others

Emerging Trends

LED UV Curing, Bio-Based Formulations, and Digital Integration Redefine Aerosol Paint Performance Standards

The shift toward LED UV curing systems replaces traditional mercury-lamp setups with energy-efficient alternatives that offer longer operational lifespans. Aerosol paint producers adopting LED-compatible formulations gain a dual advantage: lower energy cost per cure cycle and compatibility with heat-sensitive substrates where conventional UV systems fail. This technology shift sets new minimum performance expectations for buyers in electronics and industrial printing segments.

Bio-based and sustainable UV curable ink formulations represent the next frontier for aerosol chemistry. Producers developing plant-derived binder systems reduce dependence on petrochemical raw materials. Acid Etch Primer aerosol maintains a VOC content of a maximum of 690 g/L, below the EU limit of 840 g/L — demonstrating that performance compliance and sustainability targets can be met simultaneously without sacrificing coating functionality.

Digital printing integration with aerosol ink systems enables shorter production runs and faster color changeovers, which matter directly for packaging clients serving fast-moving consumer goods. Moreover, the focus on customization and short-run capabilities positions aerosol formats as viable alternatives to large-format industrial printers for low-volume, high-variety applications.

Drivers

VOC Compliance Mandates and High-Speed Packaging Demand Accelerate Aerosol Paint Adoption Across Industrial Segments

Packaging and labeling industries demand faster print throughput without sacrificing surface adhesion or color density. Reducing line downtime and per-unit coating cost. The American Coatings Association’s 2025 update confirms that the revised default reactivity value of 18.50 g O₃/g VOC is now the highest in EPA Table 2A — effectively making prior compliance frameworks obsolete and pushing buyers toward newly certified, higher-performance aerosol formulations.

The electronics segment adds a second, structurally distinct demand source. Circuit board protection, component marking, and ESD-safe coatings require precision aerosol delivery that brush or roller application cannot match. Consequently, electronics manufacturers increasingly specify aerosol-format coatings in their supplier standards, locking in recurring purchase volume for aerosol producers who qualify through certification processes.

Technological advances in ink performance — including faster curing, higher gloss retention, and improved substrate bonding — expand the functional range of aerosol paints into applications previously served by liquid spray systems. This performance convergence matters because it reduces the equipment cost barrier for smaller fabricators, bringing new buyer cohorts into the aerosol paints market without requiring capital-intensive spray line investments.

Restraints

High VOC Compliance Costs and Substrate Compatibility Limits Constrain Aerosol Paint Market Expansion

UV curing equipment carries high upfront capital costs that smaller fabricators and regional coating shops cannot readily absorb. This cost structure concentrates adoption among large-scale operators and limits the addressable customer base for premium aerosol paint systems. Therefore, vendors targeting mid-market buyers must offer financing options or phased adoption paths to convert price-sensitive prospects without discounting product value.

Heat-sensitive substrates — including certain plastics, foils, and electronic components — cannot tolerate the thermal output of conventional UV curing systems. Universal Spot Primer aerosol reports a VOC content of a maximum of 615 g/L, below the EU limit of 840 g/L, illustrating that formulation compliance is achievable. However, achieving both heat compatibility and full VOC compliance simultaneously requires R&D investment that not all producers can sustain, creating a product gap in this substrate category.

Limited substrate compatibility slows penetration in flexible packaging and medical device printing, two segments with high per-unit value. Additionally, reformulation cycles triggered by tightening VOC standards require producers to re-qualify existing products with end-customers, extending sales cycles and temporarily displacing revenue. These combined friction points delay the pace at which new aerosol paint applications convert from pilot to commercial-scale purchase volumes.

Growth Factors

3D Printing, Flexible Packaging, and Medical Segment Adoption Open New Revenue Streams for Aerosol Paint Producers

UV-compatible aerosol inks find application in 3D printing and additive manufacturing as post-processing coatings that seal printed surfaces and enhance finish quality. This use case is structurally additive — it does not compete with existing aerosol markets but creates an entirely new purchase occasion. Producers who qualify their formulations for additive manufacturing workflows position themselves in a high-growth adjacent market with above-average pricing power.

Flexible packaging and smart labeling require coatings that adhere to substrates under mechanical stress without cracking or delaminating. U-POL SPOT Universal Spot Primer’s compliance at 615 g/L VOC — well below the EU ceiling — demonstrates that high-flexibility formulations can meet regulatory thresholds. The 2K High Speed Clear aerosol achieves 92 gloss units at 20°, with an 8-hour pot life, confirming that aerosol formats can now meet the optical and durability specifications that flexible packaging buyers demand.

Medical device and pharmaceutical printing applications demand traceable, contamination-free coatings with validated performance data. Aerosol formats offer controlled deposition and lot-specific documentation that bulk liquid systems struggle to match at small batch sizes. Developing markets in Southeast Asia and Latin America are building out pharmaceutical manufacturing capacity.

Regional Analysis

Asia-Pacific Dominates the Aerosol Paints Market with a Market Share of 49.2%, Valued at USD 144.2 Million

Asia-Pacific commands 49.2% of global aerosol paint revenue, valued at USD 144.2 million. This position reflects a unique combination of high automotive production volumes, active construction markets, and cost-efficient domestic manufacturing. China, Japan, and India collectively sustain the region’s lead, with automotive refinish and industrial maintenance as the primary demand channels.

North America benefits from a mature automotive aftermarket infrastructure and early adoption of VOC compliance frameworks. U.S. EPA amendments in January 2025 reset the default reactivity factor, triggering a product reformulation cycle that drives replacement purchases. This regulatory momentum sustains commercial volume even as overall construction activity moderates.

Europe applies some of the world’s tightest aerosol VOC limits, with the EU ceiling for many coating categories. This regulatory environment accelerates the shift toward water-based and low-VOC aerosol formats. Automotive refinish remains the dominant application, but construction and furniture restoration markets add meaningful secondary volume across Germany, France, and the UK.

Latin America’s aerosol paint consumption ties closely to construction and automotive production cycles in Brazil and Mexico. Infrastructure investment programs and a growing DIY home improvement culture support baseline demand for spray coatings. However, currency volatility and import-dependent raw material supply chains limit the pace at which the region scales production capacity.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Nippon Paint Holdings Co., Ltd. positions itself as the formulation leader in Asia-Pacific, where it benefits from proximity to the region’s largest automotive and construction markets. Its R&D investment in water-based and low-VOC aerosol lines gives it a compliance advantage as regional regulators tighten emission standards, allowing it to convert regulatory pressure into a market share opportunity ahead of smaller domestic competitors.

Masco Corp. operates across multiple coatings and home improvement categories, giving its aerosol paint lines built-in distribution through home improvement retail channels. This channel breadth reduces dependence on industrial distributors and allows Masco to capture DIY demand directly at the point of sale. However, its diversified portfolio means aerosol paints compete internally for R&D and marketing budget against higher-margin product categories.

Dupli-Color Products Company focuses narrowly on automotive aerosol coatings, a strategic choice that concentrates its technical capabilities on color matching accuracy and finish durability. This specialization matters because automotive refinishers require exact OEM color replication — a performance bar that generalist aerosol brands cannot consistently clear. Dupli-Color’s focused positioning gives it a defensible share in the most commercially active application segment.

LA-CO Industries, Inc. targets industrial marking and maintenance applications where aerosol paint durability under harsh conditions outweighs cosmetic finish quality. Its product lines serve utilities, manufacturers, and construction firms that require high-visibility, weather-resistant markings. This industrial focus insulates LA-CO from direct competition with consumer aerosol brands while locking in recurring institutional purchase contracts that provide revenue stability.

Key Players

- Nippon Paint Holdings Co., Ltd.

- Masco Corp.

- Dupli-Color Products Company

- LA-CO Industries, Inc.

- Krylon Products Group

- Montana Colors S.L.

- Southfield Paints Ltd.

- Kobra Paint

- Rust-Oleum

- Aeroaids Corp

Recent Developments

- In 2025, Nippon Paint Automotive Coatings jointly developed Japan’s first large thermoplastic automotive exterior in-mold coating technology, aimed at reducing automotive coating process CO₂. Related coatings, not aerosol-specific.

- In 2025, Dupli-Color continues positioning around aerosol automotive refinishing: Perfect Match is described as fast-drying acrylic lacquer aerosol paint matching OEM colors; broader catalog includes wheel/caliper, truck-bed, undercoating, and effects coatings.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 293.0 Million |

| Forecast Revenue (2035) | USD 478.5 Million |

| CAGR (2026-2035) | 5.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Solvent Based, Water Based), By Application (Automotive, Construction, Wooden Furniture, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Nippon Paint Holdings Co., Ltd., Masco Corp., Dupli-Color Products Company, LA-CO Industries Inc., Krylon Products Group, Montana Colors S.L., Southfield Paints Ltd., Kobra Paint, Rust-Oleum, Aeroaids Corp |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |