Quick Navigation

Report Overview

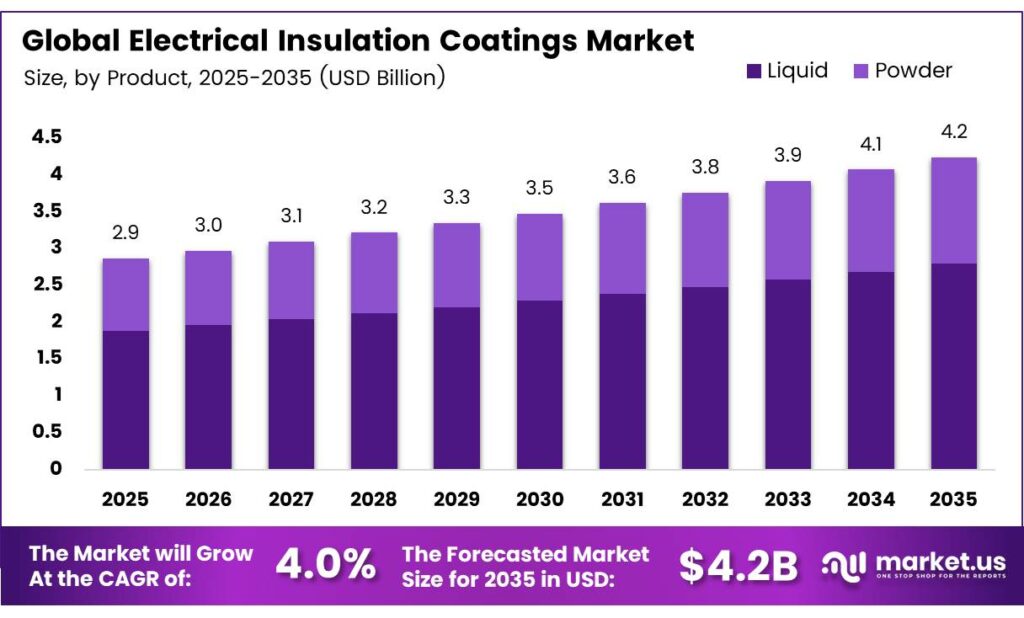

The Global Electrical Insulation Coatings Market size is expected to be worth around USD 4.2 billion by 2035 from USD 2.9 billion in 2025, growing at a CAGR of 4.0% during the forecast period 2026 to 2035.

Electrical insulation coatings are protective layers applied to conductors, motor windings, busbars, and electronic components to prevent current leakage, arc flash, and dielectric failure. They serve as the last line of defense between live electrical systems and operational failure — making coating performance a direct determinant of system reliability and safety.

Hydrophilic organosilane coatings on 220 kV overhead line conductors reduce corona discharge power losses by 25–60% compared with bare wires under rainy conditions. This performance range is commercially significant — it means utilities can demonstrably reduce transmission energy waste by selecting engineered surface coatings over uncoated aluminum conductors.

Axalta Coating Systems’ Alesta e-PRO FG Black showed no smoke or ignition at 1,200 °C, proving strong flame resistance for EV battery coatings. MacDermid Alpha Electronics Solutions’s Electrolube 2K301P delivered extremely high insulation resistance and CTI, meeting strict reliability standards.

Electric vehicle manufacturing has become one of the most structurally important demand channels for high-performance insulation coatings. Powertrain components in battery electric vehicles require coatings that can sustain high-frequency switching environments, thermal cycling, and voltage spikes — performance conditions that standard industrial coatings cannot consistently meet.

Key Takeaways

- The Global Electrical Insulation Coatings Market is valued at USD 2.9 billion in 2025 and is forecast to reach USD 4.2 billion by 2035, growing at a CAGR of 4.0% from 2026 to 2035.

- Liquid coatings dominate with a 69.2% market share in 2025.

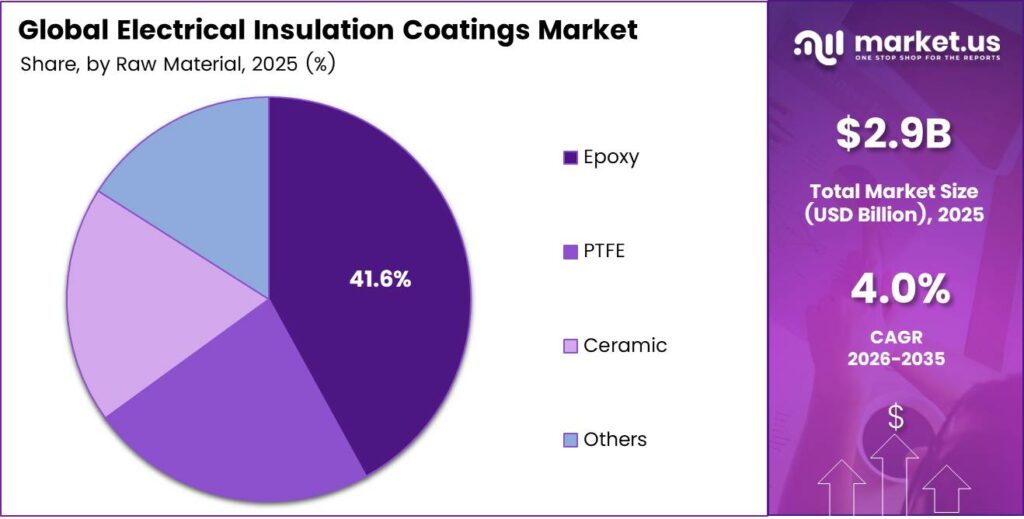

- Epoxy leads with a 41.6% share due to its superior dielectric and adhesion performance.

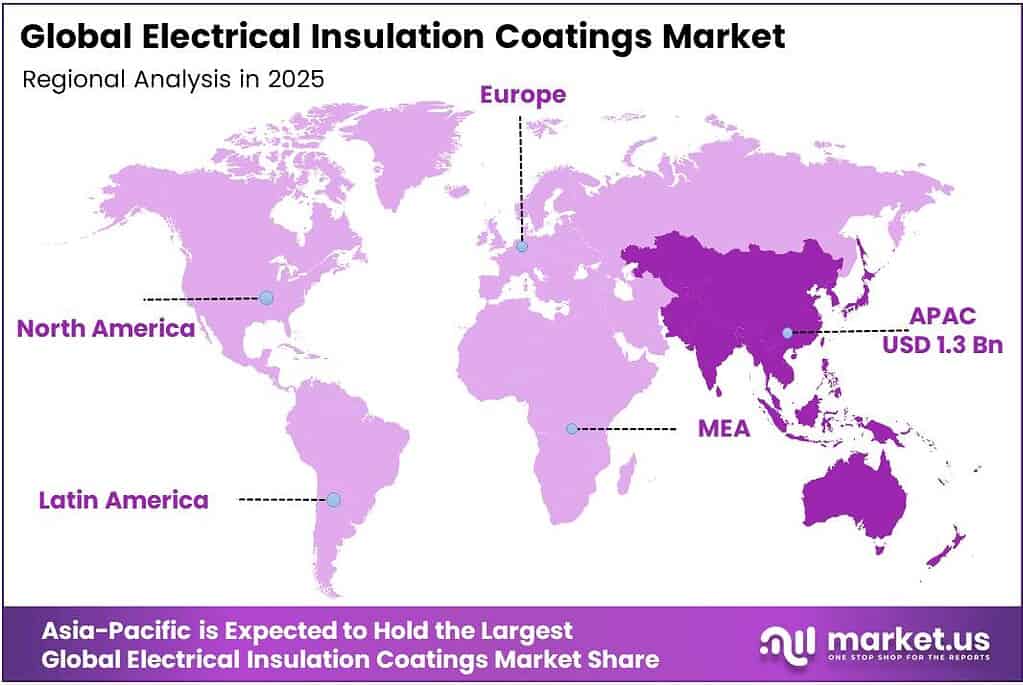

- Asia-Pacific holds the largest regional share at 43.7%, valued at approximately USD 1.3 billion in 2025.

Product Analysis

Liquid coatings dominate with 69.2% due to superior surface penetration and application versatility.

In 2025, Liquid held a dominant market position in the By Product segment of the Electrical Insulation Coatings Market, with a 69.2% share. Liquid formulations penetrate complex geometries in motor windings, transformer coils, and printed circuit boards — environments where powder coatings cannot achieve consistent dielectric coverage. This application advantage locks liquid coatings into the highest-volume end-use segments.

Powder coatings serve as the preferred solution where mechanical durability and chemical resistance outweigh application flexibility requirements. Powder systems deliver uniform layer thickness on flat or simple curved surfaces such as busbars and switchgear enclosures.

Raw Material Analysis

Epoxy dominates with 41.6% due to proven dielectric strength and adhesion performance.

In 2025, Epoxy held a dominant market position in the By Raw Material segment of the Electrical Insulation Coatings Market, with a 41.6% share. Epoxy’s combination of high dielectric strength, strong substrate adhesion, chemical resistance, and processing versatility makes it the default base material for both liquid and powder insulation coating systems. Its established supply chain and wide formulator knowledge base reinforce its structural lead over alternative chemistries.

PTFE differentiates through its exceptional non-stick, low-friction, and high-temperature performance — properties that liquid and powder epoxy formulations cannot replicate in extreme thermal environments. PTFE-based insulation coatings command higher price points and are concentrated in aerospace, defense, and specialty industrial applications where performance requirements justify the cost premium.

Ceramic coatings carry the highest thermal performance ceiling within the raw material category. Ceramic-based insulation solutions are applied via thermal spray or plasma processes onto components operating at sustained high temperatures, such as power electronics heat sinks and turbine electrical systems. Their brittleness limits adoption in mechanically dynamic environments, confining them to niche but structurally defensible applications.

Key Market Segments

By Product

- Liquid

- Powder

By Raw Material

- Epoxy

- PTFE

- Ceramic

- Others

Emerging Trends

Smart, Eco-Friendly, and AI-Driven Coating Technologies Redefine Electrical Insulation Performance Standards

Formulators are shifting away from solvent-based systems toward water-based and eco-friendly electrical insulation coating technologies. This transition is not voluntary — tightening VOC emission regulations in the EU and North America are eliminating solvent-heavy formulations from regulated markets. Manufacturers that complete this reformulation early gain access to markets where environmental compliance is a procurement prerequisite.

The Electrolube 2K301P conformal coating delivers 90 kV/mm dielectric strength and 2×10¹⁶ Ω surface insulation resistance. These figures establish a measurable performance ceiling for next-generation conformal coating products — signaling that the market for advanced protective coatings in electronics is shifting from basic protection to high-frequency, high-voltage dielectric performance.

AI-driven manufacturing processes now enable precision coating application with real-time quality monitoring, reducing material waste and coating defects on complex geometries. Simultaneously, hybrid polymer formulations with self-healing and condition monitoring capabilities are entering pilot deployment. These smart coating systems represent a structural shift — insulation coatings are evolving from passive protective layers into active system components.

Drivers

Electric Vehicle Expansion and Grid Modernization Create Sustained Demand for High-Performance Insulation Coatings

Electric vehicle powertrain components — including motor windings, battery modules, and power electronics — require insulation coatings that withstand high-frequency switching, thermal cycling, and continuous dielectric stress. Its Alesta e-PRO Dielectric Gray EV battery insulation coating passes 6 kV hipot testing — a benchmark that confirms commercial-grade dielectric performance for battery pack applications and sets a measurable qualification standard for EV coating suppliers.

Renewable energy infrastructure — including wind turbine generators, solar inverters, and offshore cable systems — demands insulation coatings that perform reliably in humid, thermally variable, and chemically aggressive environments. Utilities and project developers are specifying engineered coatings rather than standard products because field failures in renewable assets carry significant replacement and downtime costs that justify premium material selection at installation.

Miniaturization of electronic devices is compressing the physical space available for insulation — forcing coating systems to deliver higher dielectric performance in thinner layers. This technical requirement creates a structural advantage for specialty coating formulators who can engineer thin-film systems with proven dielectric credentials. Moreover, smart grid investments in substation automation and digital monitoring equipment are adding new coating demand across the transmission and distribution segment.

Restraints

Raw Material Price Volatility and VOC Compliance Costs Compress Manufacturer Margins and Limit Formulation Flexibility

Raw material price volatility — particularly for epoxy resins, fluoropolymers, and specialty ceramic precursors — directly compresses gross margins for insulation coating manufacturers. When base material costs spike, formulators face a binary choice: absorb the margin hit or pass costs to customers who operate under fixed-price contracts. Neither option is commercially neutral, and smaller formulators with limited hedging capability face the greatest exposure.

Stringent VOC emission regulations restrict the formulation options available to coating manufacturers in key markets. Inappropriate surface texturing in certain high-wettability coatings can produce shear ice adhesion levels of 265 ± 45 kPa — approximately three times higher than bare or hydrophilic-coated surfaces. This finding illustrates that reformulation to meet environmental standards is technically complex — performance tradeoffs in one property can degrade another critical characteristic.

The compliance burden extends beyond reformulation costs. Companies must invest in emissions testing, regulatory documentation, and application process modifications to maintain market access in the EU and California. These fixed compliance costs disproportionately affect mid-size manufacturers, effectively acting as a barrier to entry that consolidates the addressable market toward larger, better-resourced players.

Growth Factors

Nano-Coatings, Aerospace Demand, and Electrified Transportation Open New Revenue Segments for Advanced Insulation Formulators

Nano-insulation coatings represent a technically distinct growth path for formulators willing to invest in materials science differentiation. A polyimide enamel coating achieved a dielectric strength of 270.1 kV/mm — a 29.1% improvement over standard polyimide film. This performance gain is commercially meaningful: it enables motor designers to reduce winding insulation thickness while maintaining voltage withstand — directly supporting higher power density in compact EV and industrial motor designs.

Aerospace and defense procurement for lightweight, high-temperature-resistant insulation coatings is expanding as platform electrification increases across both sectors. Aircraft manufacturers and defense prime contractors require materials qualified to military and aviation standards — a qualification barrier that limits competition but rewards formulators that achieve approved vendor status with long-duration, high-value supply contracts.

High-speed rail electrification and industrial automation are creating additional addressable volume for motor and equipment insulation coatings. Optimized alumina insulation coatings reported a dielectric strength of 33.63 kV/mm, a relative density of 95.61%, and adhesion strength of 13.25 MPa — performance figures that qualify ceramic-based coatings for heavy industrial motor and rail traction applications where mechanical durability and dielectric stability are both mandatory.

Regional Analysis

Asia-Pacific Dominates the Electrical Insulation Coatings Market with a Market Share of 43.7%, Valued at USD 1.3 Billion

Asia-Pacific holds a 43.7% share of the global market, valued at approximately USD 1.3 billion in 2025. China, Japan, South Korea, and India concentrate the world’s largest electronics manufacturing, EV production, and grid infrastructure investment — three end-use segments that directly drive insulation coating consumption. This structural concentration of demand means the region’s lead is self-reinforcing, not cyclical.

North America commands a substantial share driven by advanced EV manufacturing, grid modernization mandates, and aerospace procurement. The United States is the primary demand engine, with domestic EV production scaling rapidly and federal infrastructure programs directing capital into transmission grid upgrades that specify engineered insulation materials over commodity alternatives.

Europe’s insulation coating demand is shaped by the EU’s industrial decarbonization agenda and mandatory VOC emission reduction targets. Germany, France, and Scandinavia lead in renewable energy deployment and industrial automation — both end-use categories that require high-performance insulation solutions. European procurement standards also incentivize eco-reformulated, water-based coating systems over legacy solvent-based products.

The Middle East is investing in power generation and transmission infrastructure to support economic diversification programs. GCC nations are constructing utility-scale solar and grid interconnection projects that require long-service-life insulation coatings suited to high-temperature, high-humidity desert environments. Africa’s market remains at an early stage, constrained by infrastructure financing gaps and limited local manufacturing capability.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Evonik Industries AG positions itself as a specialty chemistry supplier rather than a volume coatings manufacturer — a distinction that matters in this market. By focusing on high-performance silicone, polyimide, and hybrid resin systems, Evonik targets segments where dielectric and thermal specifications eliminate commodity competitors, allowing margin capture that standard coating producers cannot access.

3M leverages its cross-divisional materials science platform to deliver integrated insulation solutions — combining films, tapes, and liquid coatings under a single qualified vendor relationship. This bundled approach reduces customer qualification costs and strengthens switching barriers. In EV and aerospace segments, where multi-material insulation systems require coordinated performance validation, 3M’s integration advantage is commercially meaningful.

PPG Industries, Inc. applies its global manufacturing and distribution infrastructure to compete across both industrial and specialty insulation coating segments. PPG’s scale enables competitive pricing in volume applications while its R&D investment supports premium product development for high-specification markets. This dual positioning allows PPG to capture share across the market’s full price spectrum without ceding ground in either tier.

Thermal Spray Coatings (A Fisher Barton Company) specializes in thermally sprayed ceramic and metallic insulation coatings — a process-specific capability that serves the highest-temperature, highest-wear industrial environments. Their focus on thermal spray as a core competency, rather than a product line, creates defensible positioning in aerospace, power generation, and heavy industrial markets where alternative coating processes cannot meet performance requirements.

Key Players

- Evonik Industries AG

- 3M

- PPG Industries, Inc.

- Thermal Spray Coatings (A Fisher Barton Company)

- GfE Gesellschaft für Elektrometallurgie mbH

- ELANTAS PDG, Inc.

- GLS Coatings Ltd.

- SK FORMULATIONS INDIA PVT. LTD.

- PTFE Applied Coatings

- Axalta Coating Systems, LLC

- Akzo Nobel N.V.

Recent Developments

- In 2025, Evonik Industries AG focused on sustainable, high-performance coatings additives at the European Coatings. Evonik showcased new additives, resins, and curing agents aimed at improving the durability, efficiency, and sustainability of coatings.

- In 2025, 3M continues to strengthen its position in electrical insulation through advanced dielectric films, tapes, and thermal interface materials, especially targeting electric vehicles and high-voltage systems, reflecting a broader industry move toward electrification, even though its recent disclosures emphasize integrated insulation systems rather than standalone coatings.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2.9 Billion |

| Forecast Revenue (2035) | USD 4.2 Billion |

| CAGR (2026-2035) | 4.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Liquid, Powder), By Raw Material (Epoxy, PTFE, Ceramic, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Evonik Industries AG, 3M, PPG Industries Inc., Thermal Spray Coatings (A Fisher Barton Company), GfE Gesellschaft für Elektrometallurgie mbH, ELANTAS PDG Inc., GLS Coatings Ltd., SK FORMULATIONS INDIA PVT. LTD., PTFE Applied Coatings, Axalta Coating Systems LLC, Akzo Nobel N.V. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |