Quick Navigation

Report Overview

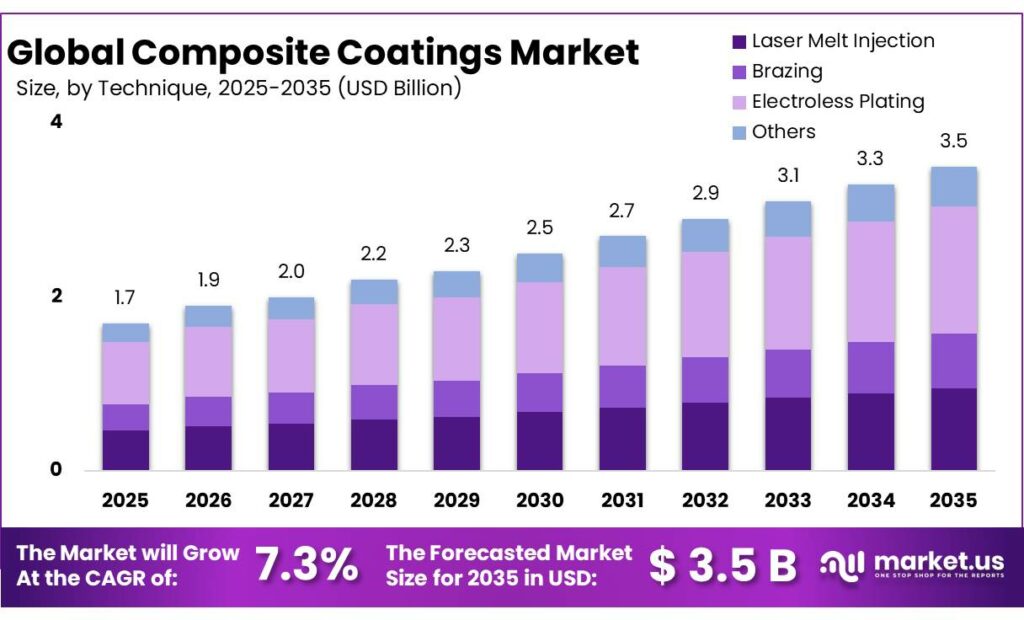

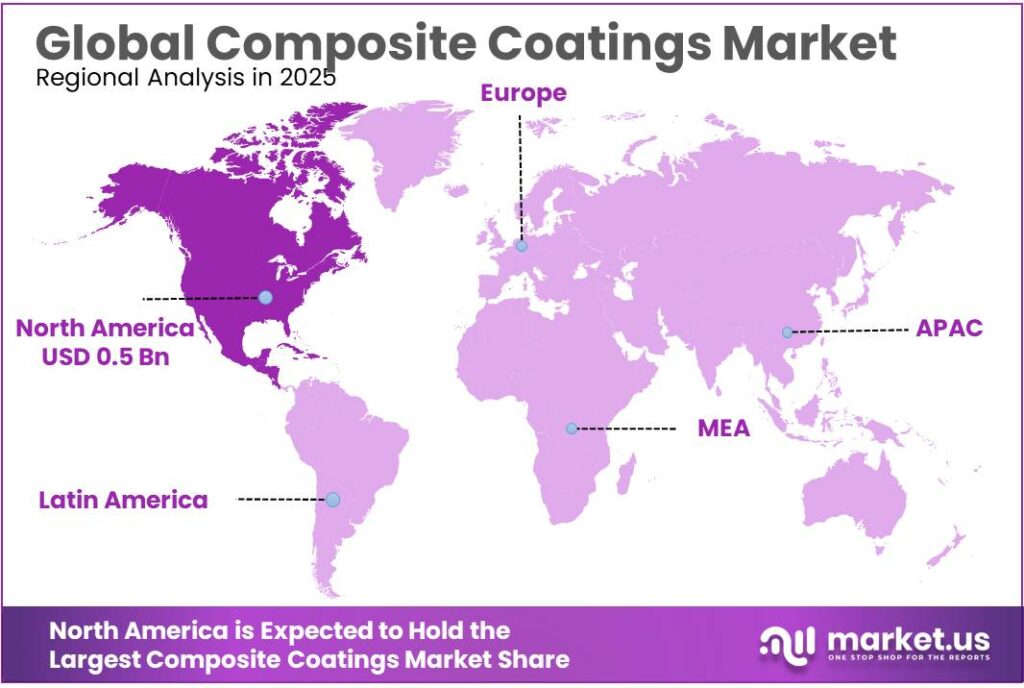

The Global Composite Coatings Market size is expected to be worth around USD 3.5 Billion by 2035, from USD 1.7 Billion in 2025, growing at a CAGR of 7.3% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 34.9% share, holding USD 0.5 Billion revenue.

Composite coatings represent a high-performance segment of the protective materials industry in which metallic, ceramic, polymeric, or hybrid reinforcements are engineered into a coating matrix to improve corrosion resistance, wear life, thermal stability, chemical resistance, and surface functionality. In industrial terms, their value proposition is strongest where equipment downtime, contamination risk, or harsh operating conditions raise the cost of failure.

That positioning remains commercially relevant because corrosion alone is estimated to cost the global economy about US$2.5 trillion, or roughly 3.4% of global GDP, while established corrosion-control practices could reduce that burden by 15% to 35%, equivalent to potential annual savings of US$375 billion to US$875 billion.

The current industrial scenario remains favorable because composite coatings are tied to large, durable end-use volumes rather than to a single niche. Food-system expansion alone supports this demand base. The OECD-FAO Agricultural Outlook 2025-2034 projects that global agricultural and fish production will expand by 14% over the next decade, while world meat production is projected to rise by 13%, or 46 million tonnes, to about 406 million tonnes by 2034. The same outlook projects global fisheries and aquaculture production to increase from 189 million tonnes in the base period to 212 million tonnes by 2034.

In parallel, FAO reports that 13.2% of food is still lost between harvest and retail, and FAO also estimates that the food cold chain is responsible for about 4% of global greenhouse gas emissions. For coating suppliers, that combination creates a clear need for more durable, hygienic, thermally efficient and lower-maintenance surfaces across tanks, processing lines, storage assets and food-packaging systems.

The main driving factors are performance economics, lightweighting, compliance, and decarbonization. The U.S. Department of Energy states that a 10% reduction in vehicle weight can improve fuel economy by 6% to 8%, and deploying lightweight materials in one quarter of the U.S. fleet could save more than 5 billion gallons of fuel annually by 2030; this directly supports advanced composite-coated substrates in transportation and industrial equipment.

On the supply side, Europe’s Critical Raw Materials Act is reshaping investment logic, and the European Commission announced 47 strategic projects tied to materials security, while the Act sets 2030 benchmarks for the EU to mine 10%, process 40%, and recycle 25% of its strategic raw material demand. These policies favor long-life, resource-efficient coatings that extend asset durability and reduce replacement intensity.

The principal driving factors are performance regulation, sustainability requirements, and process efficiency. In food-related applications, the U.S. FDA determined that 35 PFAS-related food contact notifications were no longer effective as of January 6, 2025, with a compliance date of June 30, 2025 for certain existing paper food packaging. In Europe, the packaging reform process secured a ban on PFAS in food packaging 18 months after the regulation enters into force.

Key Takeaways

- Composite Coatings Market size is expected to be worth around USD 3.5 Billion by 2035, from USD 1.7 Billion in 2025, growing at a CAGR of 7.3%.

- Electroless Plating held a dominant market position, capturing more than a 42.7% share.

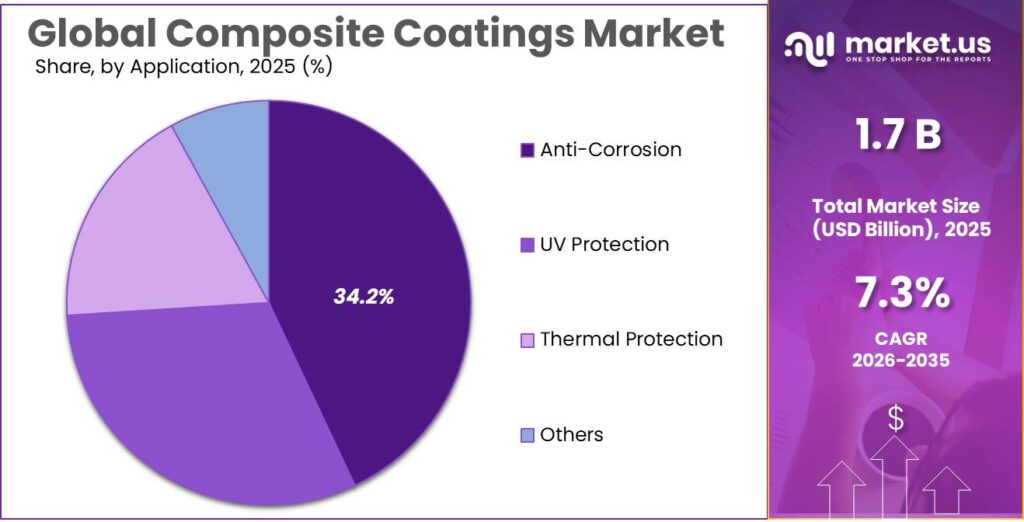

- Anti-Corrosion held a dominant market position, capturing more than a 43.1% share.

- Aerospace & Defense held a dominant market position, capturing more than a 37.2% share.

- North America holds a leading position in the composite coatings market, accounting for around 34.9% share with an estimated value of 0.5 billion.

By Technique Analysis

Electroless Plating dominates with 42.7% due to its uniform coating capability and cost-efficient processing

In 2025, Electroless Plating held a dominant market position, capturing more than a 42.7% share. This technique has gained strong preference across industries because it delivers a highly uniform coating, even on complex geometries where traditional methods often struggle. Its ability to produce consistent thickness without the need for electrical current makes it especially useful in sectors like automotive, electronics, and aerospace, where precision and reliability are critical. The demand remained steady through 2026, supported by increasing applications in corrosion resistance and wear protection.

By Application Analysis

Anti-Corrosion leads with 43.1% driven by rising demand for longer material life and protection

In 2025, Anti-Corrosion held a dominant market position, capturing more than a 43.1% share. This segment continues to grow steadily as industries focus more on extending the life of equipment and reducing maintenance costs. Composite coatings are widely used to protect metal surfaces from rust, chemical exposure, and harsh environmental conditions, especially in sectors like marine, oil & gas, and infrastructure. The demand remained strong in 2026 as companies increased investments in protective solutions to avoid frequent replacements and downtime.

By End-Use Analysis

Aerospace & Defense dominates with 37.2% driven by high performance coating needs and durability demands

In 2025, Aerospace & Defense held a dominant market position, capturing more than a 37.2% share. This segment has been a major user of composite coatings because of the need for lightweight materials that can withstand extreme conditions. These coatings are widely applied to improve resistance against heat, corrosion, and wear, which is critical for aircraft components and defense equipment. The demand stayed firm into 2026 as governments and private players continued investing in advanced aviation and defense systems.

Key Market Segments

By Technique

- Laser Melt Injection

- Brazing

- Electroless Plating

- Others

By Application

- Anti-Corrosion

- UV Protection

- Thermal Protection

- Others

By End-Use

- Aerospace & Defense

- Transportation

- Industrial

- Oil & Gas

- Others

Emerging Trends

Shift toward nanotechnology and smart coatings transforming the market

One of the most noticeable trends in the composite coatings market today is the growing use of nanotechnology and smart coatings. Industries are no longer just looking for basic protection—they want coatings that can actively improve performance. Nanocoatings, for example, are becoming popular because they offer better resistance to corrosion, heat, and wear while using thinner layers. The global nanocoatings segment itself is expanding steadily, showing strong demand across multiple industries

This trend is also clearly visible in the food industry. Advanced coatings are now being designed with antimicrobial and anti-fouling properties to improve hygiene and extend shelf life. Research shows that nanomaterial-based coatings are being used in food packaging to prevent contamination and improve safety standards. Governments and food safety authorities are encouraging such innovations to reduce food spoilage and ensure safer consumption.

Growing demand for eco-friendly and food-safe coatings shaping innovation

Another major trend is the increasing demand for eco-friendly and food-safe coatings. With stricter environmental rules and consumer awareness rising, industries are shifting toward coatings that are safer for both people and the environment. In the food sector, this shift is especially strong. The global food safety testing market alone crossed $20 billion in 2024, showing how seriously governments are taking food quality and safety

At the same time, the food-grade metal coating market reached about $518.7 million in 2025 and is expected to grow further as industries adopt safer coating materials. This growth is supported by regulations that require protective layers to prevent contamination from metals and chemicals. There is also a clear move toward water-based and low-emission coatings, reducing environmental impact while maintaining performance.

Drivers

Restraints

High initial cost and maintenance complexity limit wider adoption

One of the key restraining factors for composite coatings is the high initial cost involved in applying and maintaining these systems. While these coatings offer long-term protection, the upfront investment in advanced materials, surface preparation, and skilled labor often becomes a barrier, especially for small and mid-sized industries. This challenge is clearly visible in sectors like food processing, where equipment must meet strict hygiene standards. According to industry studies, the food processing sector alone spends nearly $2.1 billion annually on corrosion-related costs, including protective materials and maintenance.

In many cases, replacing or repairing equipment appears more affordable than investing in high-performance coatings. Government regulations such as food safety standards from authorities like the FDA also require frequent cleaning and inspection, which increases wear on coatings and adds to maintenance costs. This makes it harder for businesses to justify the higher initial investment. As a result, despite the long-term benefits, cost sensitivity continues to slow down the adoption of composite coatings in several industries.

Complex application process and operational challenges restrict usage

Another major restraint is the complexity involved in applying composite coatings and maintaining their performance over time. These coatings require precise surface preparation, controlled environments, and skilled technicians to ensure proper adhesion and durability. In industries like food and beverage manufacturing, the operating environment is highly corrosive due to moisture, chemicals, and continuous cleaning cycles, making coating performance even more challenging.

In addition, corrosion costs across industries remain extremely high, reaching about $276 billion annually in the U.S. alone, highlighting how difficult it is to manage and prevent corrosion effectively. Even with advanced coatings available, improper application or lack of maintenance can reduce their effectiveness, leading to rework and additional expenses. Governments and industry bodies encourage better corrosion management practices, but implementation at the ground level is still inconsistent.

Opportunity

Growing need for hygiene and safety standards in food industries creating new opportunities

One of the biggest growth opportunities for composite coatings is coming from the food processing industry, where hygiene and safety standards are becoming stricter every year. Food production environments are highly sensitive, and even small contamination risks can lead to major losses. Corrosion plays a big role here, as it can damage equipment and affect food quality. According to industry data, the food processing sector spends nearly $2.1 billion every year on corrosion-related issues such as equipment damage and maintenance

This huge spending is pushing companies to look for better and long-lasting protective solutions, and that is where composite coatings come in. These coatings offer better resistance to chemicals, moisture, and frequent cleaning processes, which are very common in food plants. Government bodies like the FDA and global food safety initiatives (GFSI) are also enforcing strict rules to ensure safe food production, which indirectly supports the use of advanced coatings.

Rising global corrosion losses opening doors for advanced coating solutions

Another major opportunity comes from the increasing global losses caused by corrosion across industries. Corrosion is not just a technical issue—it is a serious economic problem. Studies show that the global cost of corrosion is around $2.5 trillion, which is about 3.4% of the world’s GDP. In the United States alone, corrosion costs reach about $276 billion annually, showing how widespread the issue is

These massive losses are forcing industries and governments to focus more on prevention rather than repair. Reports suggest that proper corrosion management can save up to 15–35% of these costs, which is a huge amount at a global level. This shift is creating a strong demand for high-performance solutions like composite coatings, which can extend the life of equipment and reduce maintenance needs. Governments and infrastructure projects are also promoting better material protection practices to reduce long-term costs.

Regional Insights

North America dominates with 34.9% share supported by strong industrial base and high corrosion control demand

North America holds a leading position in the composite coatings market, accounting for around 34.9% share with an estimated value of 0.5 billion, making it the dominant regional market. The growth in this region is mainly supported by strong demand from aerospace, automotive, and industrial sectors where high-performance coatings are widely used. The region has a well-established manufacturing ecosystem and continues to invest heavily in advanced materials and protective technologies.

For instance, North America has consistently remained one of the largest contributors to the global composite coatings market due to rising demand for corrosion-resistant and durable coatings across industries. Corrosion-related challenges remain a key concern, pushing industries toward advanced coating solutions. Additionally, the regional market is experiencing steady expansion, with projections indicating growth at around 7.5% CAGR over the coming years, reflecting strong demand for high-performance coatings.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Akzo Nobel N.V. stands as one of the largest players in the global coatings market, with revenue reaching around €10.7 billion in 2023 and operations in more than 150 countries. The company employs over 35,000 people and maintains a strong presence across decorative paints and performance coatings. Its scale allows it to serve industries like aerospace, marine, and food packaging efficiently.

Axalta Coating Systems operates in over 130 countries and serves more than 100,000 customers globally. The company employs nearly 12,650 people and has built a strong base in automotive and industrial coatings. Axalta’s focus on high-performance coatings, especially for transportation and industrial use, supports its position in composite coatings. Its strong R&D infrastructure, including one of the largest coatings innovation centers, helps drive product innovation.

Bodycote is a global leader in thermal processing services, operating over 180 facilities worldwide. The company reported revenues of over £700 million and serves industries such as aerospace, automotive, and energy. Its expertise in surface technology and coating solutions supports advanced material performance. Bodycote focuses heavily on high-value sectors where durability and performance are critical.

Top Key Players Outlook

- Akzo Nobel N.V.

- Axalta Coating Systems, LLC

- BEECK Mineral Paints

- Bodycote

- FUSION Mineral Paint

- Hempel A/S

- Henkel AG and Co. KGaA

- Jotun

- KC Jones Plating Company

- KEIM Mineral Coatings of America, Inc.

- Mäder Group

- The Sherwin-Williams Company

Recent Industry Developments

Akzo Nobel N.V. continues to play a strong role in the composite coatings sector, mainly through its performance coatings portfolio used in aerospace, marine, automotive, and industrial applications. In 2025, the company reported total revenue of around $11.49 billion, showing its large-scale presence in the global coatings space.

Axalta Coating Systems continues to hold a solid position in the composite coatings space, mainly through its performance coatings and mobility coatings segments that serve automotive, industrial, and aerospace applications. In 2025, the company reported total revenue of about $5.12 billion, with its Performance Coatings segment alone contributing nearly $3.3 billion, showing how important industrial and protective coatings are to its business.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.7 Bn |

| Forecast Revenue (2035) | USD 3.5 Bn |

| CAGR (2026-2035) | 7.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Technique (Laser Melt Injection, Brazing, Electroless Plating, Others), By Application (Anti-Corrosion, UV Protection, Thermal Protection, Others), By End-Use (Aerospace And Defense, Transportation, Industrial, Oil And Gas, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Akzo Nobel N.V., Axalta Coating Systems, LLC, BEECK Mineral Paints, Bodycote, FUSION Mineral Paint, Hempel A/S, Henkel AG and Co. KGaA, Jotun, KC Jones Plating Company, KEIM Mineral Coatings of America, Inc., Mäder Group, The Sherwin-Williams Company |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |