Quick Navigation

Report Overview

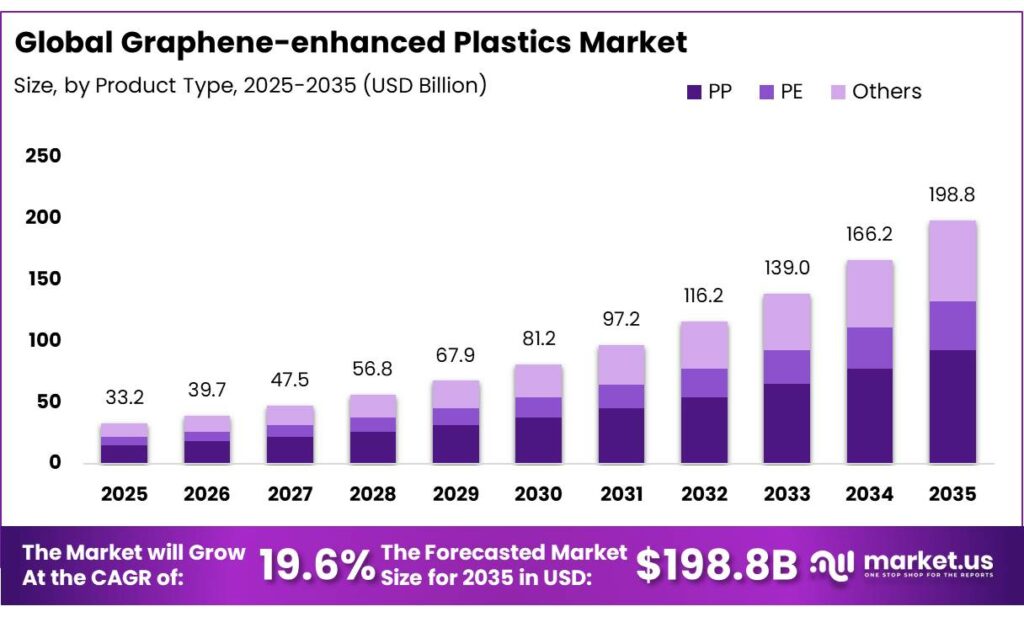

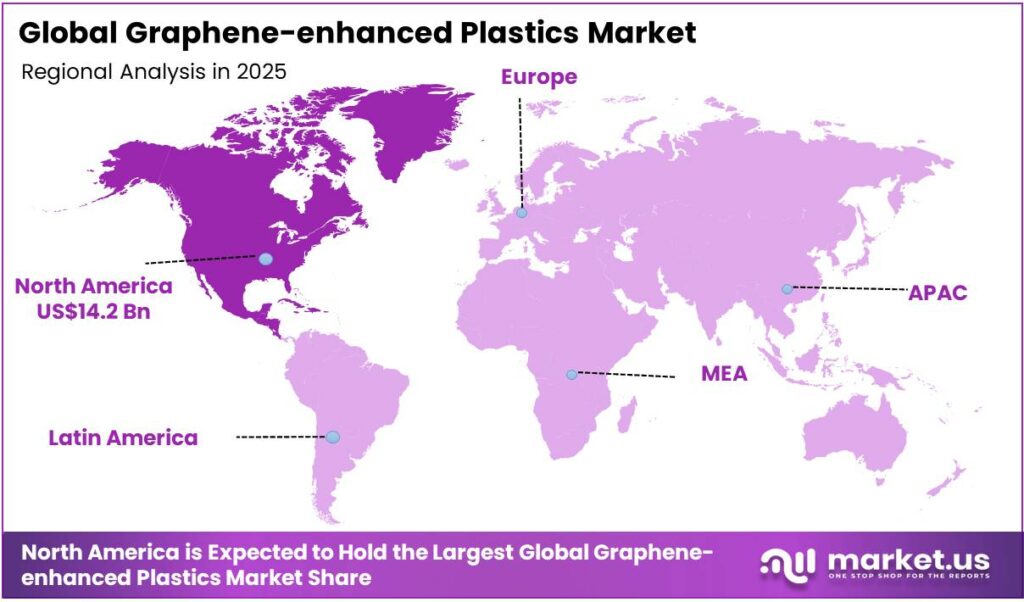

The Global Graphene-enhanced Plastics Market size is expected to be worth around USD 198.8 Billion by 2035, from USD 33.2 Billion in 2025, growing at a CAGR of 19.6% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 42.9% share, holding USD 14.2 Billion revenue.

Graphene-enhanced plastics are composite materials that integrate tiny amounts of graphene, a single layer of carbon atoms arranged in a honeycomb lattice, into a plastic matrix to create super plastics. The market is shaped by a convergence of performance-driven demand, regulatory pressures, and manufacturing constraints.

The automotive applications dominate due to high-volume production, regulatory mandates on emissions and lightweighting, and compatibility with existing polymer processing systems. Graphene-enhanced polypropylene is particularly favored for its balance of stiffness, thermal resistance, and processability. The electronics sector represents a strong opportunity, driven by quantified needs for conductivity, thermal management, and miniaturization.

Similarly, electric vehicles reinforce material demand by introducing battery-induced weight increases, intensifying the need for lightweight, multifunctional composites. However, economic and scaling challenges persist, including high production costs, suboptimal yields, and quality variability in graphene synthesis.

These constraints are compounded by geopolitical risks, as graphite supply remains highly concentrated, exposing the value chain to export controls and supply disruptions. Furthermore, technological progress in advanced production methods is gradually improving yield, consistency, and scalability, supporting broader industrial adoption.

Key Takeaways

- The global graphene-enhanced plastics market was valued at USD 33.2 billion in 2025.

- The global graphene-enhanced plastics market is projected to grow at a CAGR of 19.6% and is estimated to reach USD 198.8 billion by 2035.

- Based on the product type, graphene-enhanced PP dominated the graphene-enhanced plastics market, with a market share of around 46.9%.

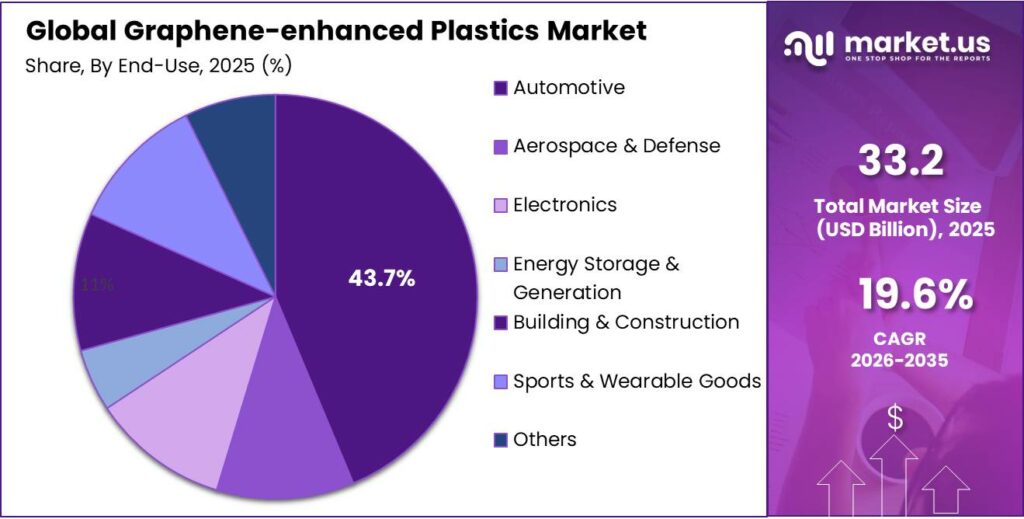

- Among the end-uses of graphene-enhanced plastics, the automotive sector held a major share in the market, 43.7% of the market share.

- In 2025, North America was the most dominant region in the graphene-enhanced plastics market, accounting for around 42.9% of the total global consumption.

Product Type Analysis

Graphene-enhanced PP Held the Largest Share in the Market.

The graphene-enhanced plastics market is segmented based on product type into PP, PE, and others. The graphene-enhanced PP dominated the market, comprising around 46.9% of the market share, primarily due to its balanced property profile and processing compatibility. The PP offers higher stiffness and thermal resistance than PE, allowing graphene reinforcement to translate more effectively into structural gains.

In addition, PP exhibits better interfacial interaction with graphene after functionalization, enabling more uniform dispersion at relatively low filler loadings. This improves electrical and mechanical performance without significantly increasing weight or viscosity. Similarly, PP is highly compatible with standard melt-processing techniques, and graphene can be incorporated using existing compounding infrastructure with minimal modification.

End-Use Analysis

Graphene-enhanced Plastics Are Mostly Utilized in the Automotive Industry.

Based on the end-uses of graphene-enhanced plastics, the market is divided into automotive, aerospace & defense, electronics, energy storage & generation, building & construction, sports & wearable goods, and others. The automotive sector dominated the graphene-enhanced plastics market, with a market share of 43.7%, as it offers the most immediate, scalable, and regulation-driven adoption pathway compared with other industries. The automotive manufacturing operates at high volumes with standardized polymer components, enabling rapid substitution with graphene-enhanced PP or similar materials using existing injection-molding infrastructure.

In addition, regulatory pressures on fuel efficiency and emissions create measurable incentives for lightweighting, making incremental material improvements commercially relevant. Similarly, the sector tolerates moderate material cost premiums when offset by durability, conductivity, or thermal benefits across large production runs. In contrast, aerospace & defense face stringent certification cycles, electronics demand ultra-high purity and consistency, and construction prioritizes cost over performance.

Key Market Segments

By Product Type

- PP

- PE

- Others

By End-Uses

- Automotive

- Aerospace & Defense

- Electronics

- Energy Storage & Generation

- Building & Construction

- Sports & Wearable Goods

- Others

Drivers

Demand from the Automotive Industry Drives the Graphene-enhanced Plastics Market.

Regulatory mandates and electrification are jointly reshaping material selection toward graphene-enhanced plastics through quantified efficiency pressures and structural vehicle redesign. The emissions regulations impose binding efficiency thresholds that implicitly incentivize lightweighting. Under EU Regulation (EU) 2019/631, fleet targets tighten from 93.6 g CO₂/km (2025-2029) to 49.5 g CO₂/km (2030-2034), reaching 0 g CO₂/km by 2035.

As tractive energy scales with mass, reducing weight directly lowers energy demand across inertial and rolling resistance components. A 15% weight increase raises EV energy consumption by 4-9%. In addition, EV diffusion introduces a countervailing mass penalty. Battery packs add significant weight to the EVs, increasing energy use and particulate emissions. It is observed that lightweighting in EV fleets can reduce CO₂ emissions and PM2.5 concentrations by up to 3%.

These combined pressures, regulatory stringency, and battery-induced mass are accelerating substitution toward high-strength, multifunctional materials. Graphene-enhanced plastics, offering high strength-to-weight ratios and conductivity, align with these quantified performance constraints without altering compliance frameworks.

Restraints

Manufacturing and Scaling Challenges Might Hamper the Demand for Graphene-enhanced Plastics.

Manufacturing and scaling constraints remain binding impediments to the commercialization of graphene-enhanced plastics, rooted in cost asymmetries, process inefficiencies, and industrial integration limits. Industrial viability requires about 82-85% yield, yet typical production yields range between 60-80%, with sub-70% levels rendering operations uneconomic due to material losses and rejection rates. Batch variability and defect formation further reduce usable output.

In addition, there is an urgent regulatory and industrial need for global standardization of nomenclature and test methods. The graphene is used generically to cover materials ranging from single-layer sheets to stacks of multiple layers (nanoplatelets), leading to unrepeatable performance in industrial masterbatches.

Similarly, integrating graphene into existing high-throughput extrusion and injection molding lines often requires specialized surface engineering, such as polymer grafting, to ensure chemical compatibility with the host plastic, adding further steps to the manufacturing cycle. The high-quality graphene is typically low-volume, while scalable methods produce defect-laden material, constraining consistent integration into plastics.

Opportunity

Demand from the Electronics Industry Creates Opportunities in the Market.

Demand from the electronics industry constitutes a structurally grounded opportunity for graphene-enhanced plastics, driven by performance requirements in conductivity, miniaturization, and thermal management. The electrical conductivity thresholds in electronics favor graphene composites, as graphene networks achieve conductivity exceeding 10⁵S/m, approaching metallic regimes for interconnects and conductive pathways.

In polymer systems, even low graphene loading enables measurable conductivity due to low percolation thresholds, allowing conductive plastics with minimal filler content. This enables substitution of heavier metal components in housings, connectors, and EMI shielding. In addition, device miniaturization and high-speed performance create material demand.

Graphene’s high electron mobility supports faster electronic devices and has enabled the fabrication of nanoscale transistors and high-frequency components. These properties align with requirements in flexible circuits, wearable electronics, and compact consumer devices. The thermal management constraints reinforce adoption. Measured thermal conductivity of single-layer graphene far exceeds conventional polymers, supporting heat dissipation in densely packed electronics.

Graphene-coated copper structures for flexible circuits can withstand 200,000 folds without damage, compared to standard copper, which fails after approximately 20,000 cycles. These electrical and thermal performance attributes underpin the integration of graphene-enhanced plastics into electronics, particularly where lightweight, conductive, and thermally stable materials are required.

Trends

Emergence of Advanced Production Methods.

The emergence of advanced production methods constitutes a structurally significant trend in graphene-enhanced plastics, driven by improvements in yield, scalability, and process adaptability. The electrochemical exfoliation is advancing toward scalable, high-yield production. Experimental reactor-based systems report graphene yields up to 65% with sheet sizes exceeding 30 µm, compared with earlier liquid-phase exfoliation yields near 12%.

Continuous electrochemical systems further emphasize process scalability through reactor design and electrolyte control, indicating movement toward industrial throughput. In addition, process innovation is reducing quality-scale trade-offs. Traditional liquid-phase methods produce small flakes and low yields, limiting industrial usability, whereas newer approaches improve layer control and defect management.

For instance, polymer-assisted exfoliation techniques leverage interfacial affinity to produce larger, higher-quality graphene suitable for composite integration. Established methods such as chemical vapor deposition (CVD) enable large-area, high-quality films for electronics, while top-down methods are being optimized for bulk composite fillers. These advances indicate a transition from laboratory-scale variability toward more standardized, application-aligned production pathways for graphene-enhanced plastics.

Geopolitical Impact Analysis

Geopolitical Tensions Are Impacting the Graphene-enhanced Plastics Due to Geographical Concentration.

The geopolitical tensions, particularly export controls, supply concentration, and industrial policy responses, are materially reshaping constraints and incentives in the graphene-enhanced plastics market through upstream graphite dependencies and downstream manufacturing risks. The extreme supply concentration of graphite introduces systemic vulnerability. According to the report by the USGS, in 2024, China accounted for around 78% of global natural graphite production and the majority of the supply chain, reinforcing single-country dependency.

Since graphene is frequently derived from graphite, this concentration directly transmits geopolitical risk into graphene-based material systems. In addition, export controls have introduced quantifiable supply constraints and administrative frictions. China’s 2023 measures require export permits for high-purity and natural graphite grades, explicitly citing national security considerations.

The policy responses indicate structural realignment but short-term rigidity. For instance, the United States remained 100% import-dependent for graphite in 2021, with the majority sourced from China, while extending EV policy provisions to accommodate supply constraints through 2026. These factors indicate that geopolitical tensions are increasing supply chain fragility, cost variability, and strategic prioritization of alternative materials, directly influencing the deployment trajectory of graphene-enhanced plastics.

Regional Analysis

North America Held the Largest Share of the Global Graphene-enhanced Plastics Market.

In 2025, North America dominated the global graphene-enhanced plastics market, holding about 42.9% of the total global consumption, underpinned by dominance in research intensity, industrial adoption, and downstream composite applications. The region benefits from a robust collaborative ecosystem. For instance, organizations such as the National Institute of Standards and Technology (NIST) and the National Graphene Association (NGA) provide the standardization frameworks essential for industrial master-batch consistency.

Additionally, recent legislative actions, such as the U.S. Inflation Reduction Act, incentivize the domestic processing of critical materials such as graphite, indirectly supporting the localized production of graphene for plastic composites. Similarly, industrial integration across end-use sectors is broad-based. Applications span conductive plastics in electronics, lightweight composites in aerospace, and energy storage systems, indicating diversified demand pull.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of graphene-enhanced plastics focus on a set of operational and technology-driven strategies. Companies invest in continuous production methods to improve yield consistency, reduce defect density, and lower unit costs, critical for integration into commodity polymers. Firms tailor graphene dispersion, loading ratios, and surface functionalization to meet targeted performance metrics for sectors such as electronics and automotive.

The strategic collaborations and co-development with OEMs and research institutions enable validation in end-use environments, accelerating qualification cycles. The intellectual property development, including patents on synthesis methods and composite formulations, supports differentiation. The supply chain integration, including securing graphite feedstock and in-house compounding capabilities, enhances reliability and reduces dependency risks.

The following are some of the major players in the industry

- Gerdau Graphene

- HydroGraph Clean Power

- Haydale Graphene Industries

- Graphene Composites Ltd

- Directa Plus

- Black Swan Graphene

- NanoXplore

- Levidian

- Versarien Plc

- HydroGraph Clean Power

- Other Key Players

Key Development

- In March 2023, Gerdau Graphene, a nanotechnology firm specializing in advanced graphene-based materials for industrial use, announced its first sales of Poly-G PE-07GM, a graphene-enhanced polyethylene master-batch.

- In August 2024, Haydale, a leading innovator in advanced materials and nanotechnology, announced a contract agreement with Gerdau Graphene for the development of graphene-infused product lines and synergy between the advanced materials.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 33.2 Bn |

| Forecast Revenue (2035) | USD 198.8 Bn |

| CAGR (2026-2035) | 19.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (PP, PE, and Others), By End-Use (Automotive, Aerospace & Defense, Electronics, Energy Storage & Generation, Building & Construction, Sports & Wearable Goods, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Gerdau Graphene, HydroGraph Clean Power, Haydale Graphene Industries, Graphene Composites Ltd., Directa Plus, Black Swan Graphene, NanoXplore, Levidian, Versarien Plc, HydroGraph Clean Power, and Other Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |