Quick Navigation

Report Overview

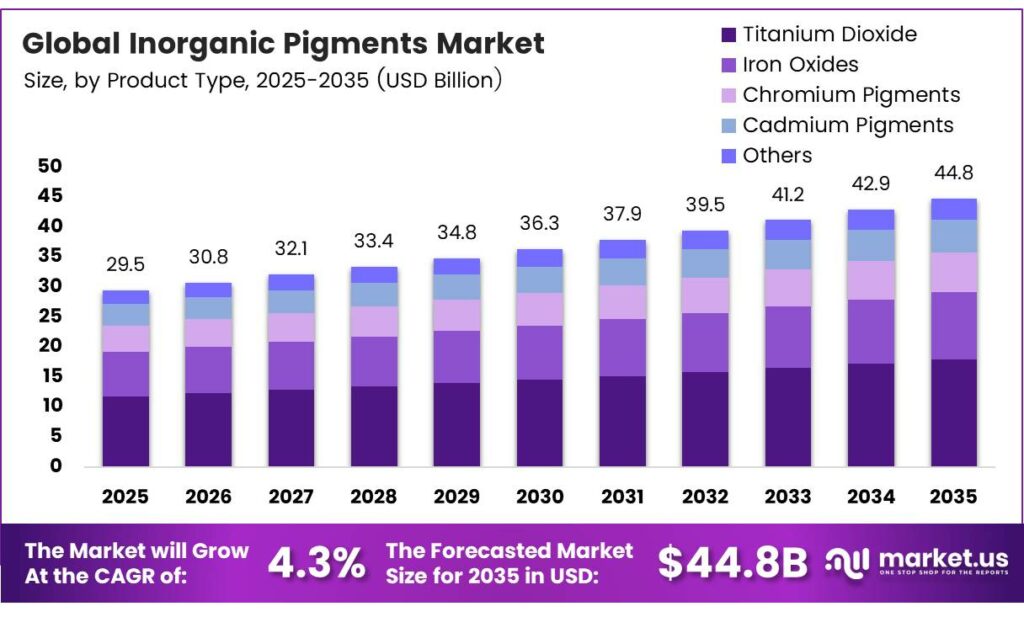

The Global Inorganic Pigments Market size is expected to be worth around USD 44.8 billion by 2035 from USD 29.5 billion in 2025, growing at a CAGR of 4.3% during the forecast period 2026 to 2035.

Inorganic pigments are naturally derived or synthetically produced coloring agents made from mineral compounds. Industries use them widely in paints, coatings, plastics, ceramics, and construction materials. Moreover, their strong heat resistance and lightfastness make them preferred over organic alternatives in demanding applications.

Inorganic cool color pigments improve energy efficiency by reflecting infrared radiation, reducing cooling energy use by up to 22% and lowering surface temperatures by 10–12 °C compared to conventional pigments. This helps limit heat buildup and supports better thermal comfort.

Bimetallic tungstate pigments offer high solar reflectance, 53.26%–84.36%, outperforming traditional dark ceramics, while advanced inorganic coating systems also provide strong durability, resisting corrosion for up to 987 hours in ASTM B117 salt-spray testing.

Construction and automotive sectors drive consistent demand for inorganic pigments globally. Infrastructure expansion across emerging economies increases the need for durable exterior coatings. Additionally, automotive OEMs specify pigments that withstand UV exposure and temperature cycling without color degradation, supporting steady industrial consumption.

Key Takeaways

- The Global Inorganic Pigments Market is projected to reach USD 44.8 billion by 2035, up from USD 29.5 billion in 2025 at a CAGR of 4.3% during the forecast period 2026 to 2035.

- Titanium Dioxide dominates with a 48.6% market share in 2025.

- Paints and Coatings lead with a 43.1% share in 2025.

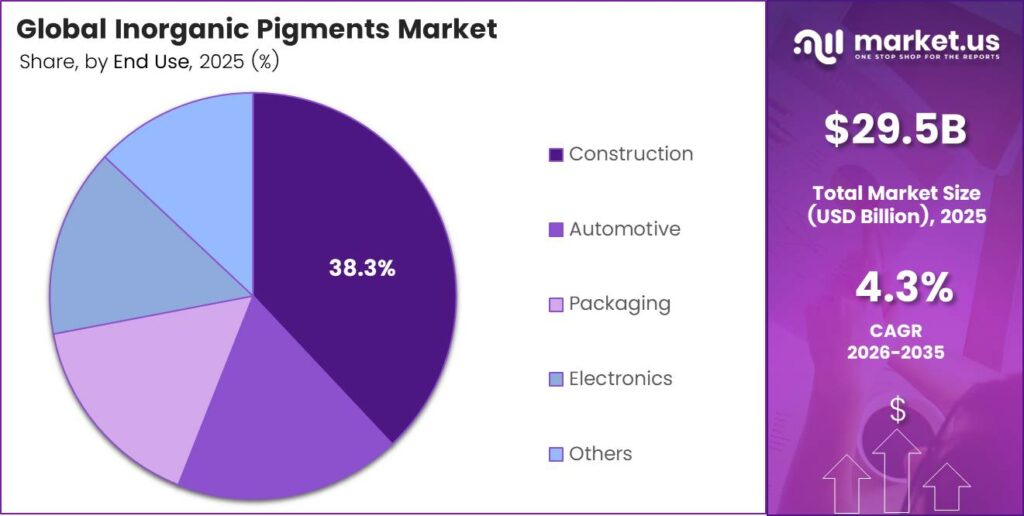

- Construction holds the largest share at 38.3% in 2025.

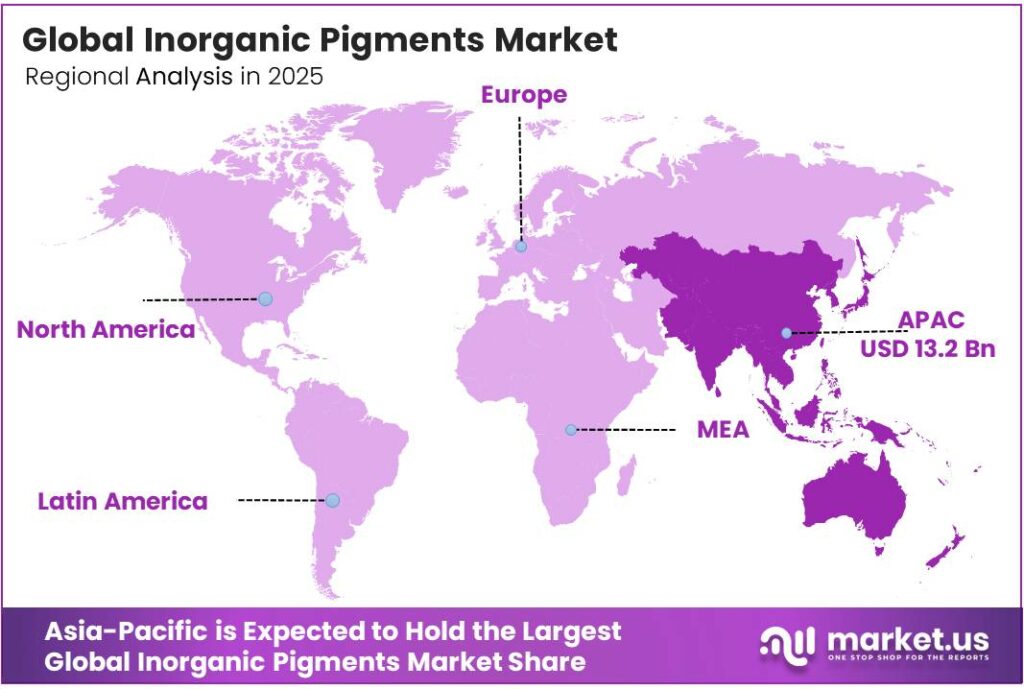

- Asia-Pacific dominates regionally with a 44.7% share, valued at USD 13.2 billion.

Product Type Analysis

Titanium Dioxide dominates with 48.6% due to its superior opacity, brightness, and broad industrial applicability.

In 2025, Titanium Dioxide held a dominant market position in the By Product Type segment of the Inorganic Pigments Market, with a 48.6% share. Its unmatched whiteness, UV resistance, and non-toxic profile make it the preferred choice in paints, coatings, and plastics globally. Moreover, its widespread regulatory acceptance further strengthens adoption across industrial and consumer applications.

Iron Oxides represent a key segment offering a wide color range from yellow and red to black. Manufacturers use them extensively in construction materials, coatings, and cosmetics. Additionally, their chemical stability and resistance to alkalis make iron oxide pigments highly suitable for demanding outdoor and industrial environments requiring long-term color durability.

Chromium Pigments serve specialized industrial markets requiring intense green and yellow shades with strong heat stability. Consequently, applications in high-temperature coatings and engineering plastics rely on chromium-based options. However, increasing environmental scrutiny on hexavalent chromium compounds pushes manufacturers to develop safer chromium pigment variants and compliant alternatives.

Application Analysis

Paints and Coatings dominate with 43.1% due to high industrial and architectural coating demand worldwide.

In 2025, Paints and Coatings held a dominant market position in the By Application segment of the Inorganic Pigments Market, with a 43.1% share. The segment benefits from continuous growth in construction, automotive refinishing, and industrial maintenance coatings. Moreover, stricter durability and weathering requirements from OEMs drive demand for high-performance inorganic pigment grades in this segment.

Plastics represent a major application segment where inorganic pigments provide heat stability during high-temperature processing. Manufacturers prefer them in polyolefins, engineering plastics, and masterbatches requiring consistent color. Additionally, their chemical inertness and resistance to migration make them suitable for food-contact and outdoor plastic products needing long-term color retention.

Printing Inks use inorganic pigments for specialty applications requiring metallic effects, opacity, and UV resistance. The segment grows with expanding packaging and commercial printing demand. Building materials, including concrete, tiles, and fiber cement, rely on iron oxides and titanium dioxide for uniform color and weather resistance in exterior applications.

End Use Analysis

Construction dominates with 38.3% due to massive infrastructure expansion and rising demand for durable building materials.

In 2025, Construction held a dominant market position in the By End Use segment of the Inorganic Pigments Market, with a 38.3% share. Rapid urbanization across Asia-Pacific, the Middle East, and Latin America fuels consistent demand for pigmented concrete, masonry coatings, and decorative finishes. Moreover, increasing focus on energy-efficient buildings drives the adoption of cool-color inorganic pigments in facade applications.

The Automotive segment demands inorganic pigments that pass rigorous OEM durability standards, including UV resistance and weathering performance. High-performance coating systems for vehicle exteriors require consistent color stability over extended service life. Additionally, growing electric vehicle production creates new opportunities for specialty pigment applications in lightweight composite body panels and battery housings.

The Packaging segment uses inorganic pigments in flexible packaging, rigid containers, and printed cartons, requiring food-safe color solutions. Demand grows with expanding e-commerce and consumer goods sectors globally. Electronics manufacturers use high-purity inorganic pigments for functional coatings, printed circuit boards, and specialty encapsulants requiring precise optical and thermal properties.

Key Market Segments

By Product Type

- Titanium Dioxide

- Iron Oxides

- Chromium Pigments

- Cadmium Pigments

- Others

By Application

- Paints and Coatings

- Plastics

- Printing Inks

- Building Materials

- Textiles

- Others

By End Use

- Construction

- Automotive

- Packaging

- Electronics

- Others

Emerging Trends

Nanotechnology and High-Purity Pigments Drive Performance Innovation

Nanotechnology-based inorganic pigments gain rapid traction across industrial and specialty applications. Manufacturers develop nano-scale formulations that deliver enhanced color strength, improved dispersion, and superior surface coverage. Infrared-reflective inorganic pigments reduced exterior surface temperatures of coated building elements by up to 10–12°C compared with standard pigments under identical solar exposure conditions, supporting adoption in hot-climate construction markets

Digital Color Matching and Sustainable Production Transform the Industry

Digital color matching technologies now integrate directly into pigment manufacturing workflows. Producers use real-time spectral analysis to ensure batch consistency and reduce waste. Moreover, the industry shifts toward sustainable production methods aligned with circular economy principles. Manufacturers increasingly adopt low-emission processes and renewable feedstocks, responding to regulatory pressure and customer demand for environmentally responsible inorganic pigment supply chains.

Drivers

Construction Boom and Infrastructure Growth Accelerate Pigment Demand

Rapid expansion of construction and infrastructure projects across Asia, Africa, and Latin America drives strong demand for durable inorganic pigments. Builders require pigments that withstand harsh outdoor conditions in concrete, coatings, and tiles. Moreover, coatings innovation reviews for 2025 confirm that waterborne and powder coating systems increasingly rely on inorganic pigments and complex inorganic color pigments to meet tighter VOC and hazardous-substance limits while preserving exterior durability.

Automotive Production and Industrial Coating Requirements Fuel Market Expansion

Rising automotive production globally drives significant consumption of high-performance coating pigments. OEM specifications demand pigments that pass more than 1,000 hours of accelerated weathering without color change. Additionally, growing preference for environmentally stable and lightfast pigments in plastics and packaging applications expands market volume. Consequently, producers invest in specialized product lines targeting automotive and industrial customers with stringent performance and compliance requirements.

Restraints

Environmental Regulations on Heavy Metal Pigments Constrain Market Segments

Stringent regulations on heavy metal-based pigments significantly limit the use of lead chromate, cadmium, and hexavalent chromium compounds in key markets. Lead-chromate control policies have led to the near-elimination of new lead-chromate paint production in countries with strict regulations, driving substitution toward alternative inorganic pigment systems. Consequently, manufacturers face reformulation costs and technical challenges in matching the performance of restricted pigments.

Raw Material Price Volatility Pressures Production Economics

Volatile raw material prices for titanium ore, iron compounds, and specialty metal oxides create significant cost uncertainty for pigment producers. Price fluctuations directly compress profit margins, particularly for mid-sized manufacturers with limited purchasing leverage. Moreover, supply chain disruptions in key mineral-producing regions intensify pricing instability. Therefore, companies increasingly invest in long-term supplier contracts, backward integration, and process efficiency improvements to manage cost exposure effectively.

Growth Factors

Eco-Friendly Pigments and Smart Coatings Open High-Value Market Segments

Rising demand for low-toxicity and eco-friendly pigment alternatives creates strong growth opportunities across global markets. Manufacturers develop chromium-free and cadmium-free grades that meet evolving regulatory standards without sacrificing performance. Bimetallic tungstate cool pigments show total solar reflectance values between 53.26% and 84.36%, demonstrating strong potential for energy-efficient architectural coatings.

Renewable Energy and Developing Economy Demand Drive Long-Term Expansion

The renewable energy sector, including solar panels and energy storage devices, adopts inorganic pigments for functional coatings requiring thermal stability and UV resistance. This emerging application channel adds a new demand driver beyond traditional industries. Furthermore, rapid industrialization and urbanization across developing economies in Southeast Asia, Africa, and Latin America generate growing consumption of pigmented construction materials, plastics, and packaging products, supporting sustained long-term market expansion.

Regional Analysis

Asia-Pacific Dominates the Inorganic Pigments Market with a Market Share of 44.7%, Valued at USD 13.2 Billion

Asia-Pacific leads the global inorganic pigments market with a 44.7% share, valued at USD 13.2 billion in 2025. China, India, and Southeast Asian nations drive this dominance through large-scale construction activity, growing automotive production, and expanding plastics manufacturing. Moreover, the region hosts major pigment production facilities that serve both domestic demand and global export markets.

North America maintains a mature and stable inorganic pigments market supported by strong automotive, aerospace, and industrial coating sectors. The United States leads regional demand through advanced manufacturing activity and premium coating applications. Additionally, regulatory pressure from the EPA accelerates the shift toward low-toxicity and compliant pigment formulations across both architectural and industrial applications.

Europe drives demand for high-performance and sustainable inorganic pigments aligned with REACH and EU chemical regulations. Germany, France, and the UK represent the largest consumers within the region. Consequently, European manufacturers invest heavily in eco-friendly pigment development and circular production processes to meet sustainability commitments and maintain competitiveness in premium coating and plastics markets.

The Middle East and Africa region presents a growing demand for inorganic pigments tied to large infrastructure projects and expanding construction activity. Gulf Cooperation Council nations invest significantly in mega-projects that drive coatings and building materials consumption. Moreover, South Africa represents an important industrial market with growing demand for pigmented coatings in mining, manufacturing, and automotive applications.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Atul Ltd. is an India-based specialty chemicals company with a strong presence in inorganic and organic pigment production. The company serves diverse end markets, including coatings, plastics, and textiles across domestic and export channels. Moreover, Atul continues to expand its pigment product portfolio through R&D investment and capacity additions targeting high-growth segments in the Asia-Pacific region.

BASF operates as one of the world’s largest chemical producers with an extensive inorganic pigments business serving coatings, plastics, and construction sectors globally. The company develops advanced dispersant and pigment systems optimized for industrial coating performance and durability. Additionally, BASF focuses on sustainable chemistry and compliant formulations that help customers meet tightening environmental regulations across major markets.

Cabot Corporation delivers specialty inorganic pigment solutions with a focus on carbon black and functional materials for demanding industrial applications. The company serves automotive, electronics, and infrastructure markets through a broad global manufacturing network. Consequently, Cabot invests in performance-enhancing pigment technologies that address customer needs for thermal stability, conductivity, and environmental compliance in advanced material applications.

Clariant provides a wide range of high-performance inorganic and effect pigments for coatings, plastics, and printing applications. The company emphasizes sustainable pigment innovation and regulatory compliance across its global product lines. Furthermore, Clariant actively develops eco-friendly alternatives to restricted heavy-metal pigments, positioning itself as a preferred partner for customers seeking compliant, high-performance colorant solutions in regulated markets worldwide.

Top Key Players in the Market

- Atul Ltd.

- BASF

- Cabot Corporation

- Clariant

- DuPont de Nemours, Inc.

- Essel Propack Ltd.

- Hebei Honghua Chemical Industry Group Co., Ltd.

- Kronos Worldwide

- Lanxess AG

- Nanjing Zijin Organic Chemical Co., Ltd.

- Orient International Holding Limited

Recent Developments

- In 2025, Atul remains directly relevant to pigments through its Colors business, which serves textile, paint/coatings, and paper end-markets and includes high-performance pigments in its portfolio. The Colors sub-segment covered textile dyes and pigments, and key products cited included Pigment Red 168 alongside vat and sulfur dyes.

- In 2025, BASF’s current relevance is more adjacent to inorganic pigments than as a standalone pigment producer: the company’s Dispersions & Resins business remains active in additives and raw materials used to formulate coatings, inks, and color systems. BASF’s 2025 Factbook describes Dispersions & Resins as a leading supplier of raw materials for coatings, construction, paper, printing/packaging, adhesives, and electronics.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 29.5 Billion |

| Forecast Revenue (2035) | USD 44.8 Billion |

| CAGR (2026-2035) | 4.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Titanium Dioxide, Iron Oxides, Chromium Pigments, Cadmium Pigments, Others), By Application (Paints and Coatings, Plastics, Printing Inks, Building Materials, Textiles, Others), By End Use (Construction, Automotive, Packaging, Electronics, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Atul Ltd., BASF, Cabot Corporation, Clariant, DuPont de Nemours, Inc., Essel Propack Ltd., Hebei Honghua Chemical Industry Group Co., Ltd., Kronos Worldwide, Lanxess AG, Nanjing Zijin Organic Chemical Co., Ltd., Orient International Holding Limited |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |