Quick Navigation

Report Overview

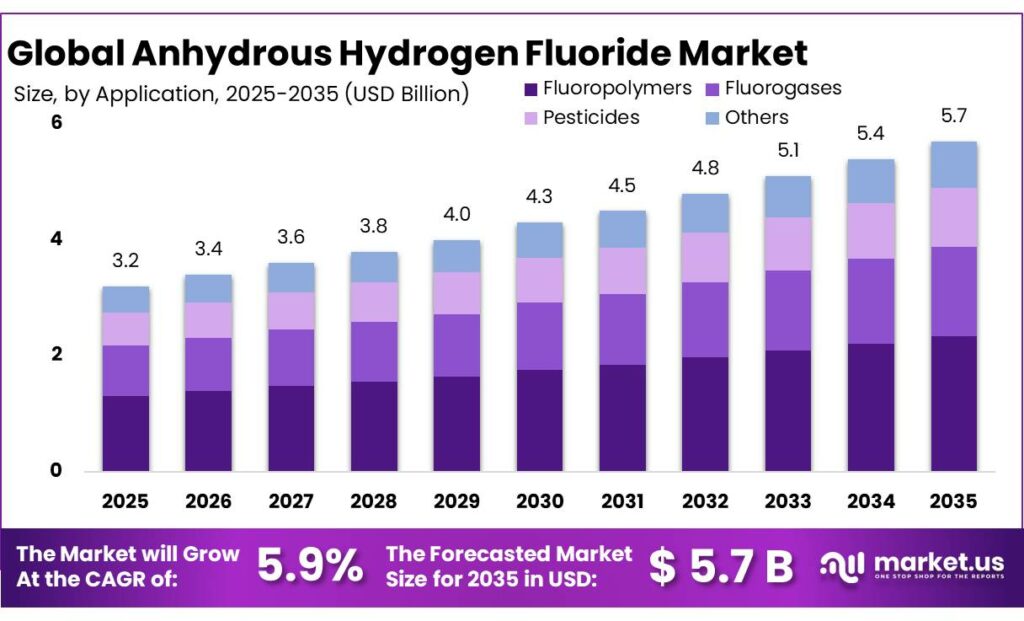

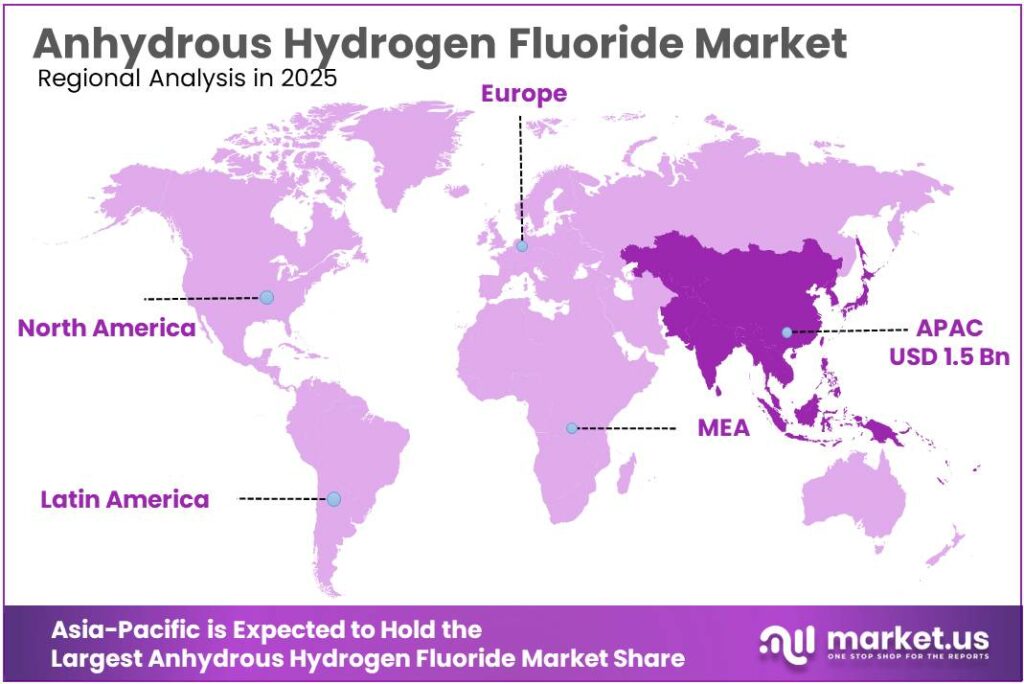

The Global Anhydrous Hydrogen Fluoride Market size is expected to be worth around USD 5.7 Billion by 2035, from USD 3.2 Billion in 2025, growing at a CAGR of 5.9% during the forecast period from 2026 to 2035. In 2025, Asia-Pacific held a dominant market position, capturing more than a 49.3% share, holding USD 1.5 Billion revenue.

Anhydrous hydrogen fluoride (AHF) is a foundational inorganic intermediate used to produce fluorocarbons, fluoropolymers, aluminum fluoride, uranium-processing chemicals, electronic-grade fluorine derivatives, and refinery alkylation catalysts. Industrially, its relevance is tied less to direct volume visibility and more to its position at the start of high-value fluorine chains, where supply security, hazardous-material handling capability, and regulatory compliance create high entry barriers.

Upstream availability remains closely linked to acid-grade fluorspar. The U.S. Geological Survey estimated global fluorspar mine production at 9.5 million metric tons in 2024, while estimated 2025 U.S. acid-grade fluorspar imports were 360,000 tons, underlining how strategically dependent the HF chain remains on mineral feedstock logistics and import reliability.

The industrial scenario points to a market that is structurally important but operationally sensitive to raw-material availability, compliance costs, and trade flows. In the United States, total fluorspar imports were estimated at 440 thousand metric tons in 2024, including 400 thousand metric tons of acid-grade material, while net import reliance remained 100% of apparent consumption.

Mexico accounted for 62% of U.S. fluorspar imports, followed by Vietnam at 14%, South Africa at 9%, and China at 8%. The average import value for acid-grade fluorspar rose to $470 per metric ton in 2024 from $429 per metric ton in 2023, which signals persistent cost pressure for AHF-linked chains.

Demand conditions remain favorable because the largest AHF-consuming downstream segments are still expanding. In electric mobility, global electric car sales exceeded 17 million units in 2024, up more than 25%, and the IEA expects sales to exceed 20 million in 2025, representing roughly 25% of total car sales. USGS also states that HF downstream products are used in lithium-ion batteries, including binders, electrolyte salts, and separator coatings. In semiconductors, global chip sales reached $791.7 billion in 2025, up 25.6% from $630.5 billion in 2024, reinforcing the broader electronics investment cycle that supports demand for ultra-pure fluorine chemistries.

Policy is another important growth driver. In Europe, Regulation (EU) 2024/573 started to apply on 11 March 2024, and the European Commission states that HFCs will be phased out by 2050; from 2025, producers receive rights equivalent to 60% of their 2011–2013 average annual production, falling to 15% by 2036. The same Commission data shows EU HFC supply was cut 45% from 2015 to 2024, with 2024 HFC usage in refrigeration, air-conditioning, and heat pumps down 10% year on year.

In the United States, Commerce announced $1.4 billion in January 2025 for advanced semiconductor packaging awards, while NIST said CHIPS for America had awarded over $33 billion across 22 states, expected to create more than 125,000 jobs. These initiatives support higher-value refrigerant transitions and electronics manufacturing, both constructive for AHF demand.

Key Takeaways

- Anhydrous Hydrogen Fluoride Market size is expected to be worth around USD 5.7 Billion by 2035, from USD 3.2 Billion in 2025, growing at a CAGR of 5.9%.

- Fluoropolymers held a dominant market position, capturing more than a 41.6% share.

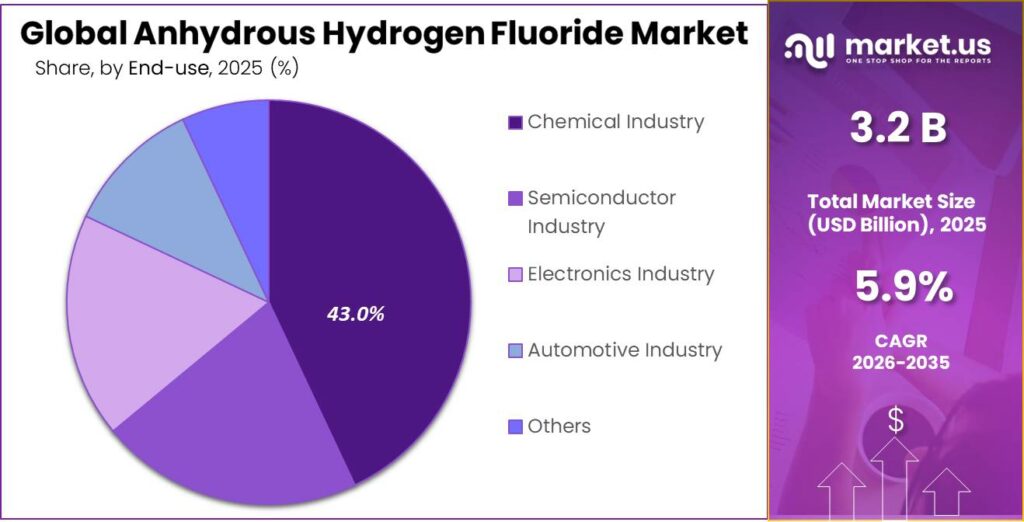

- Chemical Industry held a dominant market position, capturing more than a 43.8% share.

- Asia-Pacific held the leading position in the anhydrous hydrogen fluoride market, accounting for 49.3% share with a value of around USD 1.5 billion.

By Application Analysis

Fluoropolymers dominate with 41.6% driven by strong demand in high-performance applications

In 2025, Fluoropolymers held a dominant market position, capturing more than a 41.6% share. This strong position is mainly supported by their wide use in industries that require materials with high resistance to heat, chemicals, and electrical stress. Anhydrous hydrogen fluoride plays a key role in producing fluoropolymers such as PTFE and PVDF, which are commonly used in sectors like electronics, automotive, and chemical processing. The demand remained steady throughout 2025 as manufacturers continued to rely on these materials for durability and performance in harsh environments.

By End Use Analysis

Chemical Industry leads with 43.8% supported by its wide-scale industrial use

In 2025, Chemical Industry held a dominant market position, capturing more than a 43.8% share. This dominance comes from the essential role anhydrous hydrogen fluoride plays as a key raw material in producing a wide range of chemicals, including fluorocarbons, refrigerants, and specialty compounds. Throughout 2025, demand stayed strong as chemical manufacturers continued large-scale production to meet industrial and commercial needs. The segment also benefited from steady operations in agrochemicals and pharmaceuticals, where fluorine-based compounds are widely used.

Key Market Segments

By Application

- Fluoropolymers

- Fluorogases

- Pesticides.

- Others

By End Use

- Chemical Industry

- Semiconductor Industry

- Electronics Industry

- Automotive Industry

- Others

Emerging Trends

Shift toward high-purity and advanced-grade production is shaping the market

One of the most noticeable trends in the anhydrous hydrogen fluoride market is the growing shift toward high-purity grades, especially for advanced industries like semiconductors and electronics. As technology becomes more precise, the quality requirements for chemicals are also increasing. In 2025, industries started moving strongly toward ultra-high-purity hydrogen fluoride because even small impurities can affect chip performance.

At the same time, the semiconductor-related hydrofluoric acid market itself reached around USD 14.72 billion in 2025, showing how large and important this application has become. Governments are also supporting domestic chip manufacturing with strong policies and funding programs, especially in regions like the U.S. and Asia. This has pushed chemical producers to upgrade their production facilities to meet stricter purity standards.

Increasing focus on safety monitoring and smart industrial systems

Governments and regulatory bodies are playing a big role here by making safety compliance mandatory. Industries are now required to install real-time monitoring systems, automated alerts, and smart sensors to detect even small leaks. This has led to the adoption of IoT-based safety solutions that can track gas levels continuously and respond quickly in case of risk.

Drivers

Rising demand for fluorinated chemicals driving strong industrial usage

One of the biggest drivers for anhydrous hydrogen fluoride is its deep connection with fluorinated chemical production. This material is not something optional in the industry—it is a base input used to create refrigerants, fluoropolymers, agrochemicals, and specialty chemicals. As industries grow, the need for these materials naturally rises, and that pushes the demand for anhydrous hydrogen fluoride along with it.

In 2025, the global market itself was valued around USD 2.96 billion and continued to increase to about USD 3.11 billion in 2026, showing steady demand coming from chemical manufacturing and industrial applications.

This growth is closely linked to environmental shifts as well. Many countries are moving toward low-global-warming refrigerants, which are produced using fluorinated chemistry. Because of this transition, industries are increasing their use of hydrogen fluoride as a feedstock. Governments and regulatory bodies are also supporting this shift by encouraging cleaner cooling systems and limiting older chemicals.

Expansion of semiconductor and advanced electronics manufacturing

Governments across regions are actively supporting domestic semiconductor production through funding and infrastructure programs. These initiatives are not just about technology independence but also about strengthening supply chains. As more fabrication units are built, the need for high-purity hydrogen fluoride rises, especially for advanced chips.

In addition, sectors like electric vehicles and 5G networks are expanding fast, both of which rely on semiconductor components. This creates a strong, long-term demand base. In simple terms, as the world becomes more digital and connected, the need for anhydrous hydrogen fluoride keeps growing steadily alongside it.

Restraints

Strict safety regulations and exposure risks limit wider adoption

One major restraining factor for anhydrous hydrogen fluoride is its extremely hazardous nature, which brings strict safety rules and limits its use across industries. This chemical is not easy to handle—it can cause severe burns, respiratory damage, and even fatal effects if exposure is not controlled properly. According to Occupational Safety and Health Administration, the permissible exposure limit is set at just 3 ppm over an 8-hour work period, showing how tightly controlled its usage must be.

The risk becomes even more serious at higher concentrations. Data from National Institute for Occupational Safety and Health shows that exposure around 50 ppm can be fatal within 30 to 60 minutes, which highlights how dangerous this substance can be if mishandled. These safety concerns force companies to invest heavily in protective equipment, monitoring systems, and trained personnel. Many small and mid-sized manufacturers find it difficult to meet these requirements, which slows down adoption.

Industrial incidents and regulatory pressure affecting market confidence

Another important restraint is the history of industrial accidents and the increasing pressure from regulatory bodies. There have been several recorded incidents where workers were exposed to hydrogen fluoride, leading to injuries and even fatalities. Data from Occupational Safety and Health Administration accident records shows multiple cases, including situations where workers were injured or killed due to direct exposure to the chemical.

These incidents have pushed governments to tighten regulations further. Safety agencies now require detailed risk management systems, emergency response planning, and continuous monitoring in facilities handling this chemical. Even small leaks or exposure can lead to serious consequences, including delayed symptoms that may appear hours later, making it harder to detect early.

Opportunity

Growing semiconductor investments creating long-term demand

One of the biggest growth opportunities for anhydrous hydrogen fluoride is coming from the rapid expansion of the semiconductor industry. This chemical is widely used in chip manufacturing, especially for cleaning and etching silicon wafers. As the world becomes more digital, the demand for chips is rising across smartphones, electric vehicles, AI systems, and data centers.

Governments are actively supporting this shift. For example, the U.S. government introduced the CHIPS and Science Act, which includes around $52.7 billion in funding for semiconductor manufacturing and research, along with $39 billion specifically for production incentives. On top of that, there are additional investments such as $300 million for advanced packaging projects and over $470 million combined public-private investment to boost chip technology.

Expansion of advanced electronics and high-purity chemical demand

Another strong opportunity comes from the increasing need for high-performance electronics and precision manufacturing. Modern technologies like 5G networks, electric vehicles, and advanced computing systems depend heavily on high-quality semiconductor chips. These chips require ultra-clean processing, where anhydrous hydrogen fluoride plays a critical role. The market itself is already showing steady growth, reaching around USD 3.05 billion in 2026, with continued expansion expected as electronic applications grow.

In addition, industries are moving toward smaller and more efficient chips, which require even higher purity chemicals. This increases the demand for specialized grades of hydrogen fluoride. Government-backed programs and industry investments are also encouraging local manufacturing in regions like North America and Asia, reducing dependency on imports and strengthening supply chains.

Regional Insights

Asia-Pacific dominates with 49.3% share driven by strong chemical and electronics base

Asia-Pacific held the leading position in the anhydrous hydrogen fluoride market, accounting for 49.3% share with a value of around USD 1.5 billion, making it the most influential regional market. The region’s dominance is largely supported by its strong chemical manufacturing base and growing demand from electronics and semiconductor industries. In 2025, the Asia-Pacific market stood at nearly USD 1.49 billion, and it further increased to about USD 1.56 billion in 2026, showing steady year-on-year growth.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Arkema operates as a major global player in fluorochemicals, where anhydrous hydrogen fluoride is a key upstream input. In 2025, the company reported overall revenues of around €9.5 billion, reflecting its strong chemical portfolio and global footprint. A significant portion of its specialty materials segment is linked to fluorinated products, supporting steady demand for HF-based inputs.

Lanxess plays an important role in specialty chemicals where fluorine-based intermediates are essential. In 2025, Lanxess generated revenues close to €6.7 billion, supported by its advanced intermediates and specialty additives business. The company’s involvement in industrial chemicals and material protection products indirectly supports hydrogen fluoride demand.

Navin Fluorine International Limited is one of the leading players in fluorochemicals, with direct involvement in hydrogen fluoride production and downstream products. In 2025, the company reported revenues of around ₹2,200+ crore, driven by strong demand in specialty chemicals and high-performance materials. It has also been expanding capacity through projects focused on fluorinated intermediates and specialty applications.

Top Key Players Outlook

- Arkema

- Lanxess

- Navin Fluorine International Limited

- Fubao Group

- Foshan Nanhai Shuangfu Chemical Co., Ltd

- Foosung, Co Ltd

- Fluorchemie Dohna GmbH

- Fluorsid S.p.A.

- Derivados del Fluor SA

Recent Industry Developments

Arkema operates as a key player in the anhydrous hydrogen fluoride value chain through its strong fluorochemicals and specialty materials portfolio, especially in products like PVDF and other fluoropolymers that rely on hydrogen fluoride as a base input. In 2025, the company reported total sales of around €9,068 million, with an EBITDA of €1,251 million and an EBITDA margin of 13.8%, showing stable performance despite weak demand in some regions.

Lanxess plays a steady role in the anhydrous hydrogen fluoride value chain through its Advanced Intermediates segment, where fluorine-based intermediates and chemical building blocks are produced and supplied to downstream industries like agrochemicals, pharmaceuticals, and specialty materials. In 2025, the company reported total annual sales of around €5.67 billion, showing a decline of 10.9% year-on-year, mainly due to weak global demand and pricing pressure.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 3.2 Bn |

| Forecast Revenue (2035) | USD 5.7 Bn |

| CAGR (2026-2035) | 5.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Application (Fluoropolymers, Fluorogases, Pesticides, Others), By End Use (Chemical Industry, Semiconductor Industry, Electronics Industry, Automotive Industry, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Arkema, Lanxess, Navin Fluorine International Limited, Fubao Group, Foshan Nanhai Shuangfu Chemical Co., Ltd, Foosung, Co Ltd, Fluorchemie Dohna GmbH, Fluorsid S.p.A., Derivados del Fluor SA |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |