Quick Navigation

Report Overview

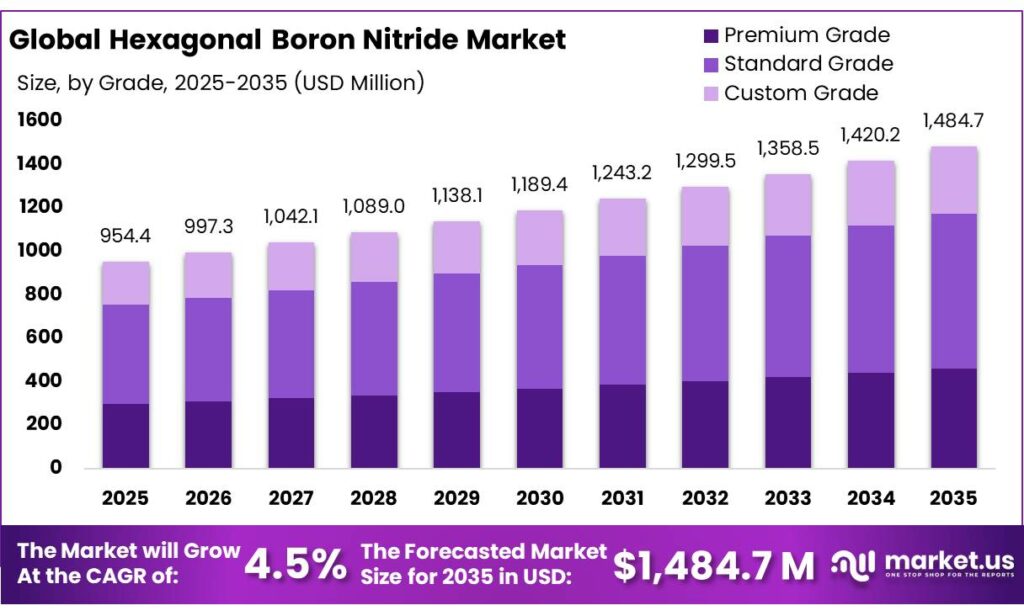

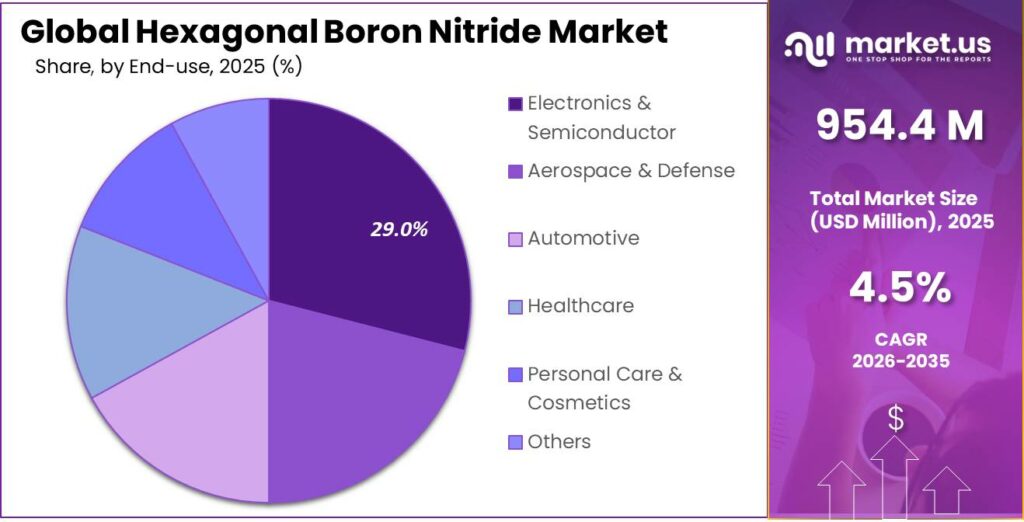

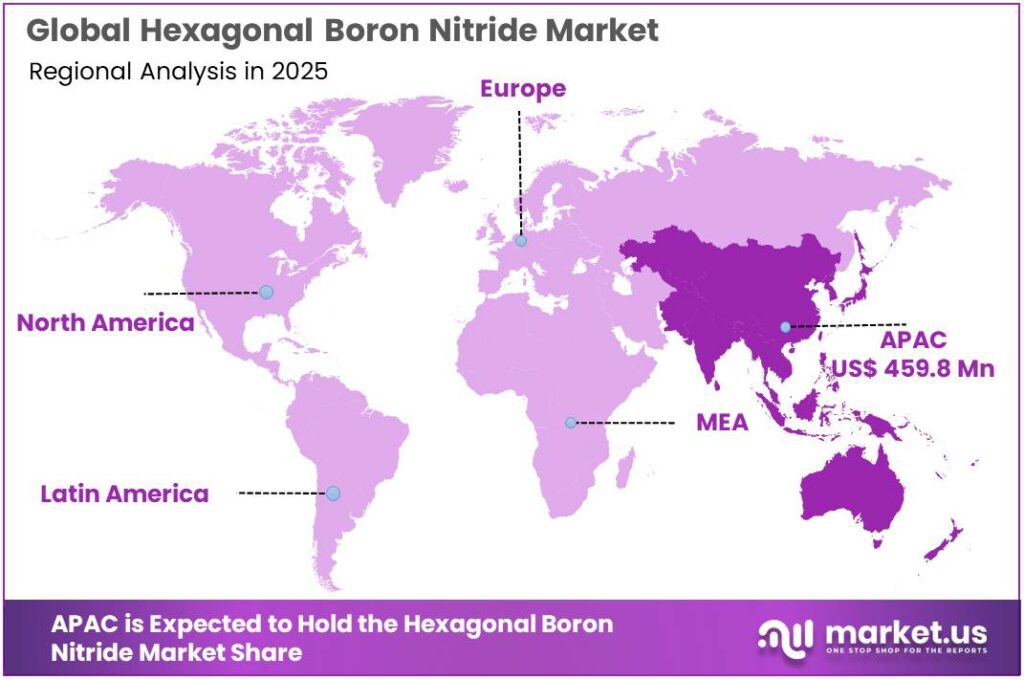

The Global Hexagonal Boron Nitride Market size is expected to be worth around USD 1,484.7 Million by 2035, from USD 954.4 Million in 2025, growing at a CAGR of 4.5% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 48.2% share, holding USD 459.8 Million revenue.

Hexagonal boron nitride (h-BN) is an advanced ceramic known for combining thermal conductivity, electrical insulation, chemical inertness, lubricity, and high-temperature stability in one material platform. In industrial terms, it sits between a performance filler and a strategic engineered material, because it can improve heat dissipation without sacrificing dielectric strength in polymers, coatings, films, and ceramic systems.

3M states that its boron nitride cooling fillers are used to improve thermal conductivity in polymers while maintaining electrical insulation, and reports dielectric resistivity of more than 10^15 ohm-cm, dielectric strength of more than 67 kV/mm, and optical reflectivity of more than 95% for relevant grades. 3M also notes that alumina-filled plastics typically reach about 3.5-4 W/m·K, underscoring why h-BN is favored where higher thermal performance is required.

The current industrial scenario is being shaped primarily by electronics, EVs, and semiconductor infrastructure. Electric car sales exceeded 17 million units in 2024, rising by more than 25% year on year, according to the IEA, while global motor vehicle production reached 92,504,338 units in 2024, according to OICA.

In parallel, SEMI reported that worldwide semiconductor manufacturing equipment billings increased 15% to $135.1 billion in 2025, with Taiwan at $31.5 billion, Korea at $25.8 billion, and Japan at $9.5 billion. This matters directly for h-BN because the material is increasingly selected where thermal loads are rising faster than acceptable package temperatures, especially in power electronics, battery systems, and advanced chip packaging.

The main growth drivers are therefore structural rather than cyclical. Data-centre electricity consumption is projected by the IEA to reach about 945 TWh by 2030, growing at roughly 15% per year from 2024 to 2030. That creates a stronger commercial case for thermally conductive but electrically insulating fillers in servers, power supplies, connectors, and AI hardware.

Government policy is reinforcing the same direction: the European Commission says the European Chips Act is backed by more than €43 billion in policy-driven investment through 2030, while the U.S. Department of Commerce Inspector General reports that the CHIPS Act provides $50 billion to Commerce, including $39 billion for semiconductor incentives and $11 billion for R&D, with about $33.7 billion in direct funding awarded as of January 31, 2025.

Key Takeaways

- Hexagonal Boron Nitride Market size is expected to be worth around USD 1,484.7 Million by 2035, from USD 954.4 Million in 2025, growing at a CAGR of 4.5%.

- Standard Grade held a dominant market position, capturing more than a 48.5% share.

- Thermal Management held a dominant market position, capturing more than a 31.6% share.

- Electronics & Semiconductor held a dominant market position, capturing more than a 29.3% share.

- Asia-Pacific held the dominant position in the hexagonal boron nitride market, accounting for 48.2% of the global share and reaching a value of USD 459.8 Mn.

By Grade Analysis

Standard Grade leads the hexagonal boron nitride market with 48.5% share, supported by its broad industrial fit and dependable performance.

In 2025, Standard Grade held a dominant market position, capturing more than a 48.5% share. This leadership was mainly driven by its strong use across a wide range of industrial applications where consistent thermal stability, electrical insulation, and lubrication properties are required. Standard grade hexagonal boron nitride remains the preferred choice for manufacturers because it offers a practical balance between performance and cost, making it suitable for ceramics, coatings, metallurgy, and electronic component production.

By Application Analysis

Thermal management stands strong in the hexagonal boron nitride market with 31.6% share, driven by rising heat-control needs in electronics and advanced materials.

In 2025, Thermal Management held a dominant market position, capturing more than a 31.6% share. This segment’s strong position was largely supported by the growing use of hexagonal boron nitride in applications that require efficient heat dissipation without compromising electrical insulation. Industries such as electronics, electric vehicles, batteries, semiconductors, and high-performance polymers increasingly relied on this material to improve thermal conductivity and maintain system stability under demanding operating conditions.

By End Use Analysis

Electronics & semiconductor leads with 29.3% share as heat control and insulation needs continue to rise in advanced devices.

In 2025, Electronics & Semiconductor held a dominant market position, capturing more than a 29.3% share. This segment remained the leading end-use industry due to the increasing demand for materials that can manage heat efficiently while providing strong electrical insulation in compact and high-performance devices. Hexagonal boron nitride is widely used in semiconductor processing equipment, thermal interface materials, insulating substrates, and electronic packaging, where stable performance under high temperatures is essential.

Key Market Segments

By Grade

- Premium Grade

- Standard Grade

- Custom Grade

By Application

- Thermal Management

- Electrical Insulation

- Lubrication

- Coatings

- Personal Care Products

- Composites

- Others

By End Use Industry

- Electronics & Semiconductor

- Aerospace & Defense

- Automotive

- Healthcare

- Personal Care & Cosmetics

- Others

Emerging Trends

2D h-BN coatings in electronics is the latest trend shaping the market

One of the most important latest trends in the hexagonal boron nitride market is the fast rise of 2D h-BN coatings for advanced electronics cooling. As AI processors, compact consumer devices, and EV control units generate more heat in smaller spaces, manufacturers are moving toward ultra-thin boron nitride layers that improve heat spreading without affecting electrical insulation.

A 2025 study published in Small showed that 2D h-BN coatings increased thermal conductivity at integrated circuit surfaces from below 0.3 W/m-K to nearly 260 W/m-K. The same work also reported a 17.4% reduction in power consumption in coated audio amplifier boards, showing how practical this trend has become for real-world electronics.

Government-backed semiconductor and EV localization is pushing next-gen adoption

A second major trend is the policy-led expansion of semiconductor fabs and EV battery manufacturing, which is increasing the use of h-BN in thermal interface materials and insulating substrates. Governments across India, the U.S., Europe, and East Asia are investing heavily in chip plants and battery gigafactories, where thermal stability materials are critical.

The International Energy Agency reported that electric cars represented more than 20% of global car sales in 2025, creating strong downstream demand for battery heat-management materials and safe dielectric fillers. This directly supports the trend of h-BN use in battery modules, ceramic separators, and power electronics insulation. Trusted policy programs such as India’s semiconductor mission and EV battery localization schemes are also encouraging advanced materials sourcing for domestic production ecosystems.

Drivers

Rising demand from electronics and EV thermal management is a major growth driver

One of the strongest driving factors for the hexagonal boron nitride market is the rapid rise in thermal management demand from electronics, semiconductors, and electric vehicles. As devices become smaller and more powerful, the amount of heat generated inside chips, batteries, and power modules has increased sharply.

This is where hexagonal boron nitride becomes highly valuable because it combines high thermal conductivity with electrical insulation, making it ideal for heat spreaders, interface pads, fillers, and battery insulation layers. Recent studies have shown that h-BN coatings can increase thermal conductivity at chip surfaces from below 0.3 W/m-K to nearly 260 W/m-K, while also reducing power consumption in electronic boards by 17.4%.

Government EV and advanced electronics initiatives are accelerating adoption

Another major factor supporting market expansion is the push from government-backed EV and advanced manufacturing programs, especially around battery safety and thermal control. In India, the Principal Scientific Adviser’s eMobility R&D Roadmap highlights thermal management as a core requirement for battery packs, motors, and power electronics in electric vehicles.

Restraints

High production cost and energy-intensive processing remain a key restraint

One of the biggest restraining factors for the hexagonal boron nitride market is its high production cost, especially for high-purity and fine-particle grades. Trusted technical sources show that boron nitride densification and phase-controlled processing can require temperatures of up to 2200°C under 90 MPa pressure, which directly raises utility and equipment costs.

Such demanding conditions make the material less affordable for cost-sensitive industries like general industrial coatings, consumer goods fillers, and low-end thermal plastics. Smaller manufacturers often hesitate to adopt h-BN because the cost difference versus conventional fillers like alumina or graphite can be substantial at scale. This pricing pressure becomes even more visible in applications where ultra-high purity is not essential.

Raw material dependence and limited boron mineral concentration add supply pressure

Another major restraint comes from the concentrated supply of boron feedstock and mineral dependency, which can influence pricing stability for h-BN producers. Since boron nitride production starts from boron-based precursors such as boric acid and boron oxide, any fluctuation in boron mineral supply directly impacts manufacturing economics.

According to the U.S. Geological Survey (USGS), global boron mineral production remains highly concentrated, with Turkey accounting for roughly 70% of world borate reserves, making the supply chain vulnerable to trade, logistics, or regional policy shifts. This concentration can create raw material pricing pressure for downstream h-BN manufacturers, especially in Asia and Europe where imported boron derivatives are common.

Opportunity

Expansion in electric vehicle batteries creates a strong growth opportunity

One of the biggest growth opportunities for hexagonal boron nitride lies in the rapid expansion of electric vehicle battery systems and advanced thermal interface materials. As EV batteries become larger, faster-charging, and more energy-dense, the need for safe heat dissipation materials is increasing quickly.

This creates a natural opportunity for h-BN because it offers strong thermal conductivity while remaining electrically insulating, which is highly valuable in battery modules, separators, potting compounds, and thermal gap fillers. According to the International Energy Agency, global lithium-ion battery deployment in 2025 was six times higher than in 2020, with electric vehicles contributing more than 70% of total battery deployment.

Government-led EV and semiconductor manufacturing programs support long-term upside

Another major opportunity is coming from government-backed EV, semiconductor, and advanced materials manufacturing initiatives, especially in Asia, Europe, and North America. Public investments in battery plants, chip fabs, and localized electronics supply chains are increasing the demand for materials that improve thermal stability and dielectric safety.

Hexagonal boron nitride fits well into this shift because it is already being explored in battery insulation films, semiconductor heat spreaders, and ceramic substrates. The IEA’s Global EV Outlook 2025 notes that EVs accounted for one in every four cars sold globally, showing how quickly the supporting component ecosystem is scaling.

Regional Insights

Asia-Pacific dominates the hexagonal boron nitride market with 48.2% share, reaching USD 459.8 Mn on the back of strong electronics and EV manufacturing demand

In 2025, Asia-Pacific held the dominant position in the hexagonal boron nitride market, accounting for 48.2% of the global share and reaching a value of USD 459.8 Mn. The region’s leadership is strongly supported by its deep concentration of electronics, semiconductor, electric vehicle, and advanced ceramics manufacturing hubs across China, Japan, South Korea, Taiwan, and India.

Asia-Pacific continues to serve as the global center for semiconductor packaging, thermal interface material production, and lithium-ion battery manufacturing, all of which are major consumption areas for hexagonal boron nitride due to its superior thermal conductivity and dielectric insulation performance.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

3M remains one of the most influential players in the hexagonal boron nitride market, supported by its advanced thermal filler portfolio and strong electronics materials presence. The company’s h-BN solutions are widely used in thermal interface compounds, semiconductor packaging, and EV battery systems. With the global h-BN market valued at nearly USD 1.0 billion in 2025, 3M continues to benefit from rising demand in thermal management applications.

Saint-Gobain remains one of the most dominant names in the hexagonal boron nitride market, with strong penetration across machinable ceramics, molten metal contact parts, and high-temperature insulation components. The company is estimated to hold nearly 16.9% market share among leading players, making it one of the strongest competitors globally. Its boron nitride ceramic portfolio includes crucibles, nozzles, rods, and custom machinable components used above 1000°C industrial conditions.

American Elements holds a strong position through its broad catalog of boron nitride powders, nanoparticles, and ultra-high-purity engineered materials. The company is known for supplying h-BN in purity levels above 99.0% to 99.9%, which supports demand from laboratories, aerospace coatings, and semiconductor R&D environments. Its numerical strength lies in customizable particle sizing from sub-micron to 100+ micron ranges, allowing flexibility across coatings, lubricants, and thermal fillers.

Top Key Players Outlook

- 3M

- American Elements

- Denka Company Limited

- Grolltex Inc.

- Saint-Gobain

- Yara

- Resonac Holdings Corporation.

- ZYP Coatings Inc.

- Momentive

- Resonac Europe GmbH

Recent Industry Developments

Denka reported JPY 400.3 billion in net sales and JPY 14.4 billion in operating income for the fiscal year ended March 31, 2025, giving it the scale to keep investing in advanced materials.

3M strength comes from its ability to combine high thermal conductivity of 400 W/m·K in-plane with electrical resistivity above 10¹⁵ Ohm·cm, making its materials highly suitable for heat-sensitive electronic systems.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 954.4 Mn |

| Forecast Revenue (2035) | USD 1,484.7 Mn |

| CAGR (2026-2035) | 4.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Grade (Premium Grade, Standard Grade, Custom Grade), By Application (Thermal Management, Electrical Insulation, Lubrication, Coatings, Personal Care Products, Composites, Others), By End Use Industry (Electronics And Semiconductor, Aerospace And Defense, Automotive, Healthcare, Personal Care And Cosmetics, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | 3M, American Elements, Denka Company Limited, Grolltex Inc., Saint-Gobain, Yara, Resonac Holdings Corporation., ZYP Coatings Inc., Momentive, Resonac Europe GmbH |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |