Quick Navigation

Report Overview

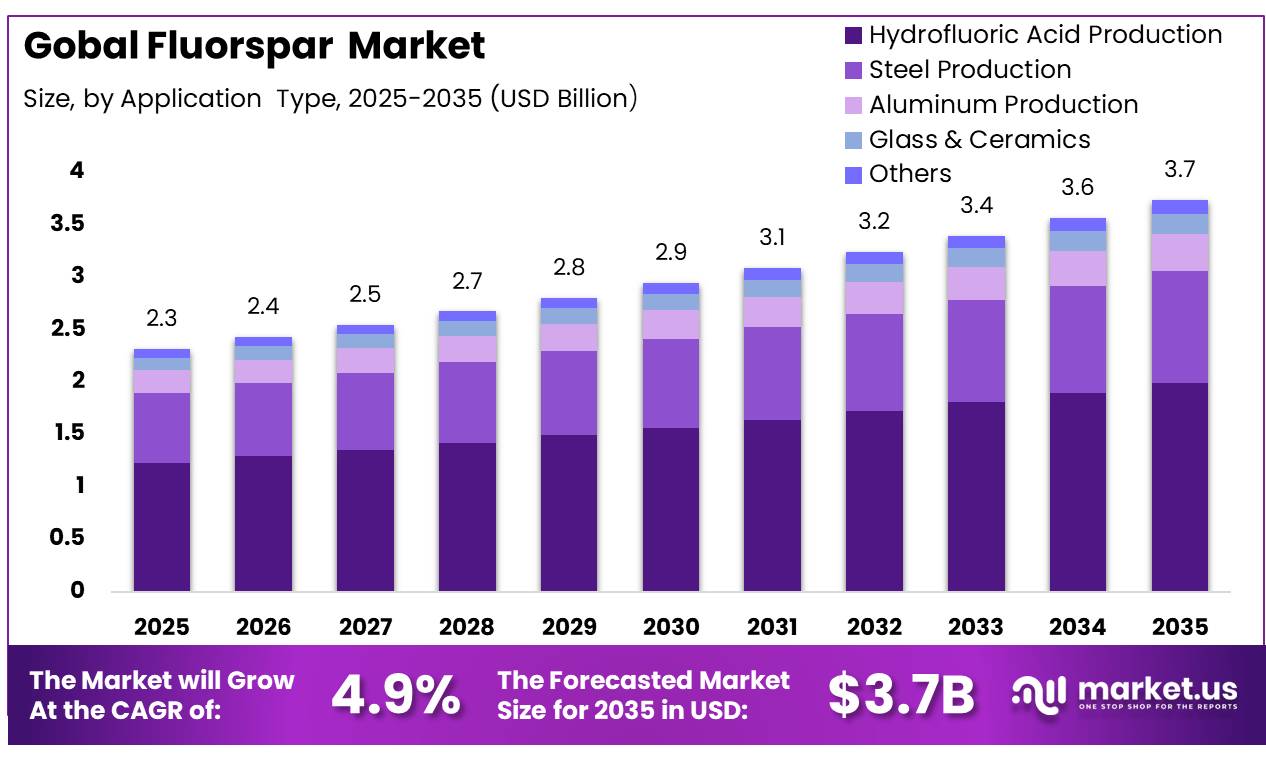

The Global Fluorspar Market size is expected to be worth around USD 3.7 Billion by 2035, from USD 2.3 Billion in 2025, growing at a CAGR of 4.9% during the forecast period from 2025 to 2035. Asia pacific held a dominant market position, capturing more than a 58.5% share, holding USD 1.35 billion in revenue.

Fluorspar, or fluorite, is a calcium fluoride mineral and the principal commercial source of fluorine. Acid-grade material is converted into hydrogen fluoride, the feedstock used across refrigerants, fluoropolymers, aluminum processing, uranium treatment, petrochemical catalysis, and semiconductor cleaning and etching. Metallurgical-grade material is mainly consumed as a flux in steelmaking, foundries, cement, glass, enamels, and welding products. These wide industrial linkages place fluorspar within the critical chemical-mineral supply chain.The industrial scenario remains highly concentrated.

- In February 2026, the U.S. Geological Survey estimated that global mine production declined 1% to 10 million metric tons during 2025. China produced approximately 6 million tons, representing about 60% of global output, while Mexico and Mongolia each supplied 1.5 million tons. China’s first-half 2025 imports increased 48% to 856,000 tons, with Mongolia providing 86%, highlighting tightening domestic availability and growing cross-border dependence.

- The United States remained 100% net-import reliant and imported about 380,000 tons in 2025. Acid-grade import values averaged US$470 per metric ton.

Key Takeaways

- The Global fluorspar market was valued at USD 2.3 billion in 2025.

- The Global fluorspar market is projected to grow at a CAGR of 4.9% and is estimated to reach USD 3.7 billion by 2035.

- On the basis of product type, acid-grade fluorspar dominated the market, constituting 64.7% of the total market share.

- Based on application, hydrofluoric acid production dominated the fluorspar market, with a substantial market share of around 53.2%.

- Among the end-use industries, the chemical industry held a major share in the fluorspar market, accounting for 55.4% of the total market.

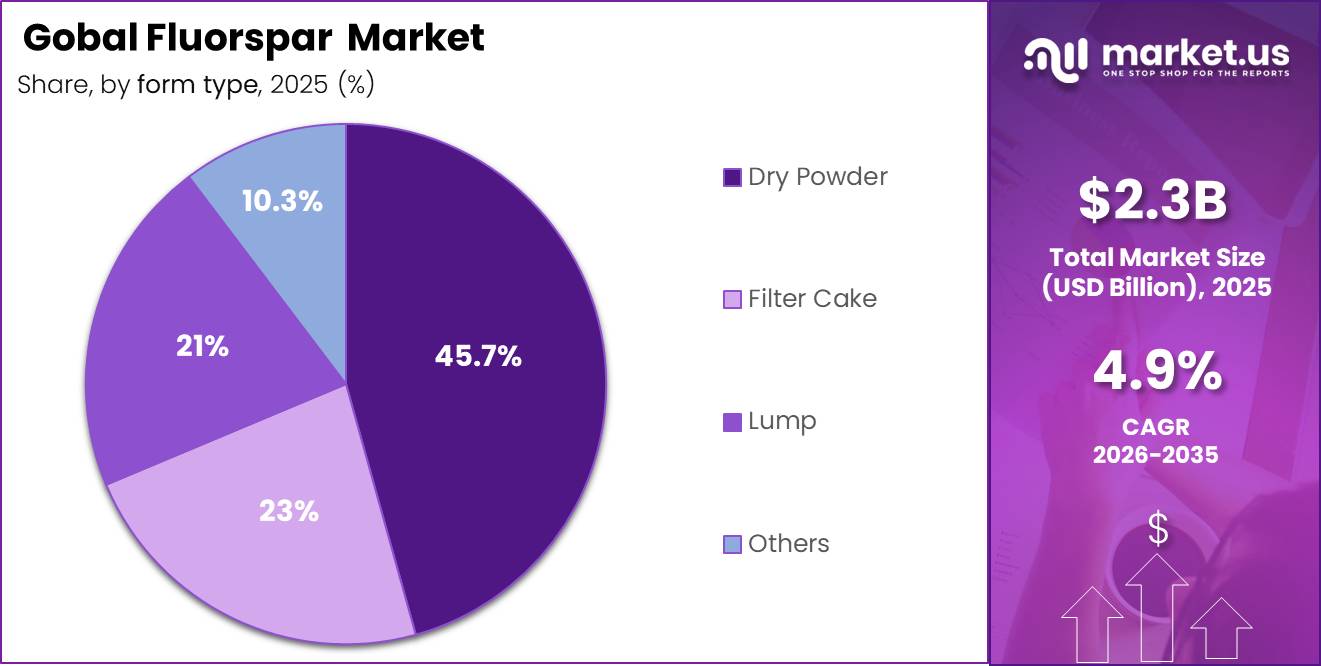

- Based on form, dry powder led the fluorspar market, comprising 45.7% of the total market share.

- Among the distribution channels, direct sales represented the most significant segment, accounting for around 68.52% of the market share.

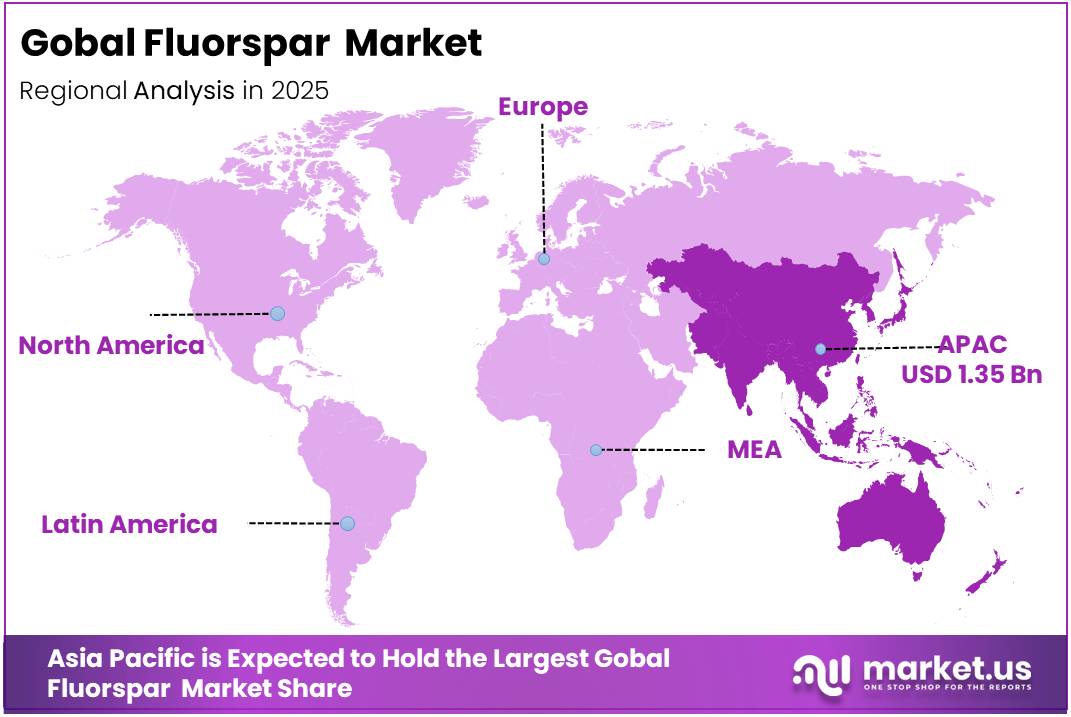

- In 2025, Asia Pacific was the most dominant region in the fluorspar market, accounting for 58.5% of the total market share.

Demand is supported by continued use of hydrogen fluoride in fluorochemicals, refrigeration, specialty polymers, aluminum, and semiconductor manufacturing. The U.S. Department of Energy also identifies fluorine among materials used in batteries, linking future fluorspar consumption with energy-storage supply chains. However, mine safety controls, production concentration, permitting requirements, and limited substitutes may create procurement and price risks.

Future opportunities are emerging through capacity restarts, new mines, and fluorine recovery. A Canadian operation restarted in August 2025 and targeted 200,000 tons of annual acid-grade output, while a new Xinjiang mine projected 300,000 tons annually. In the United States, 45,000 tons of fluorosilicic acid recovered from phosphate plants during 2025 equaled roughly 73,000 tons of pure-fluorspar equivalent. European Union classification of fluorspar among 34 critical raw materials should further encourage diversified sourcing, processing, recycling, and substitute-development initiatives across major downstream chemical and manufacturing markets.

Fluorspar Market Segmentation

Product Type Analysis

Acid Grade Fluorspar dominates with 64.7% due to its strong role in fluorochemical production

In 2025, Acid Grade Fluorspar held a dominant market position, capturing more than a 64.7% share. As of June 2026, the segment continued to benefit from its high purity and wide use in producing hydrofluoric acid, fluoropolymers, refrigerants, aluminum fluoride, and specialty chemicals. Chemical producers prefer acid grade material because it supports consistent processing, controlled reactions, and product quality. Its importance across chemical manufacturing, electronics, aluminum processing, and advanced industrial applications helped it remain the leading product type in the fluorspar market.

Metallurgical Grade Fluorspar is gaining steady demand because it is widely used as a flux in steelmaking and foundry operations. It helps lower melting temperatures, improves slag fluidity, and supports cleaner metal processing. Rising steel production, furnace efficiency needs, and demand from cement, welding, and glass applications are expected to strengthen its market position.

Application Analysis

Hydrofluoric Acid Production dominates with 53.2% due to its central role in fluorochemical manufacturing

In 2025, Hydrofluoric Acid Production held a dominant market position, capturing more than a 53.2% share. As of June 2026, the segment remained the leading application because hydrofluoric acid is required in refrigerants, fluoropolymers, aluminum fluoride, petroleum refining, glass treatment, and semiconductor processing. Fluorspar serves as the main raw material for producing this chemical, giving the segment a strong position across industrial supply chains. Demand from specialty chemicals, electronics, aluminum processing, and industrial cleaning continued to support its market leadership. Its broad application base and limited substitutes also strengthened consumption.

Steel Production is emerging as a growing application for fluorspar. Steelmakers use it as a flux to reduce melting temperatures, improve slag movement, remove impurities, and support smoother furnace operations. Expanding steel output, plant modernization, and demand for efficient metal processing are expected to increase consumption.

End-Use Industry Analysis

Chemical Industry dominates with 55.4% due to its strong demand for fluorine-based products

In 2025, Chemical Industry held a dominant market position, capturing more than a 55.4% share. As of June 2026, the segment remained the largest end-use industry because fluorspar is widely used to produce hydrofluoric acid, fluoropolymers, refrigerants, solvents, and other specialty chemicals. Chemical manufacturers rely on fluorspar for stable processing, consistent purity, and reliable fluorine content. Demand from electronics, pharmaceuticals, industrial coatings, and advanced materials continued to support consumption. Its broad role across several downstream chemical processes helped the segment maintain a leading position.

Aluminum Industry is emerging as a growing end-use segment. Fluorspar is used in producing aluminum fluoride and supporting smelting operations, where it helps improve bath chemistry and process efficiency. Rising aluminum demand from transport, packaging, construction, and electrical applications is expected to strengthen fluorspar consumption across this industry during future industrial production cycles.

By Form Analysis

Dry Powder dominates with 45.7% due to easy handling and broad industrial suitability

In 2025, Dry Powder held a dominant market position, capturing more than a 45.7% share. As of June 2026, the segment continued to lead because it offers storage, transportation, and controlled feeding across chemical and metallurgical operations. Its uniform particle size supports consistent blending and helps manufacturers maintain stable process conditions. Dry powder is widely preferred in hydrofluoric acid production, steelmaking, aluminum processing, glass, ceramics, and welding applications. Its longer storage life, lower handling complexity, and suitability for automated dosing systems support industrial use.

Filter Cake is emerging as a growing form because it reduces drying requirements and can be processed directly by chemical producers. It also supports lower dust generation during handling and offers benefits where moisture content can be managed within the production line. Expanding processing capacity and cost-focused operations are expected to support demand.

Distribution Channel Analysis

Direct Sales dominates with 68.52% due to stronger supplier relationships and reliable bulk procurement

In 2025, Direct Sales held a dominant market position, capturing more than a 68.52% share. As of June 2026, this channel remained preferred by large chemical producers, steelmakers, aluminum processors, and glass manufacturers that require stable quality, regular volumes, and dependable delivery schedules. Direct agreements allow buyers to negotiate product specifications, shipment timing, pricing terms, and long-term supply commitments effectively. Producers also benefit from closer customer contact, clearer demand planning, and lower dependence on multiple intermediaries. These advantages support efficient procurement and help industrial users manage raw-material availability across continuous production operations.

Indirect Sales is growing steadily as distributors and trading companies improve access for small and medium-sized buyers. This channel supports customers requiring flexible order sizes, regional availability, shorter lead times, and technical assistance. Wider distributor networks are strengthening fluorspar reach across developing industrial markets.

Key Market Segments

By Product Type

- Acid Grade Fluorspar

- Metallurgical Grade Fluorspar

- Ceramic Grade

By Application

- Hydrofluoric Acid Production

- Steel Production

- Aluminum Production

- Glass & Ceramics

- Others

By End-Use Industry

- Chemical Industry

- Steel Industry

- Aluminum Industry

- Glass & Ceramics Industry

- Others

By Form

- Dry Powder

- Lump

- Filter Cake

- Others

By Distribution Channel

- Direct Sales

- Indirect Sales

Drivers

Regulatory Push — HFC-to-HFO Refrigerant Transition

The U.S. AIM Act has already reduced production of high-GWP HFCs such as R-410A, R-134a, and R-404A by a combined 40% from baseline by January 2024, with compliance dates for equipment restrictions extending to 2028, forcing manufacturers toward HFO alternatives including R-1234yf and R-1234ze, both of which require HF as a synthesis input. The revised EU F-Gas Regulation 2024/573, published in February 2024, deepens the HFC phase-down timeline through 2050 and from 2025 has banned stationary refrigeration equipment with GWP ≥ 150 in specific categories, with chillers (≤12 kW) facing bans from 2027 a capital-replacement wave estimated to affect hundreds of thousands of installations across Europe.

Chemours reported a 25% revenue increase in its Thermal & Specialized Solutions division in Q2 2025, a direct financial validation that the HFC-to-HFO transition is translating into measurable HF demand growth. The business model impact for fluorspar producers is favorable: while HFO molecules require fewer carbon-fluorine bonds than legacy HFCs, the complexity of their synthesis increases HF consumption per unit weight of finished refrigerant, maintaining or slightly elevating fluorspar intensity per refrigerant tonne even as the total refrigerant volume managed under quota declines.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Battery Chemistry | +1.1% | Global — China, South Korea, India (core); North America, Europe (emerging) | Long term (≥ 4 years) |

| Metallurgical Demand | +0.7% | India (primary), Gulf/MENA (secondary), APAC (supporting) | Medium term (2–4 years) |

| Regulatory Push | +0.6% | North America, EU (core); UK, South America (spill-over) | Short–Medium term (1–4 years) |

| Supply Constraint | +0.5% | North America, EU (policy-driven); Mongolia, Vietnam as supply corridors | Short term (≤ 2 years) |

| Semiconductor Supercycle | +0.4% | North America (fab expansion), East Asia — Taiwan, South Korea, Japan | Medium term (2–4 years) |

| Fluoropolymer Diversification | +0.5% | Global — APAC dominates (57.7% share); North America growing at 7.62% CAGR | Long term (≥ 4 years) |

Restraints

Synthetic & Byproduct Substitutes — Competitive Displacement in AlF₃ and Cryolite Applications

FSA is produced at a rate of approximately 50 kg per tonne of hydrofluoric acid equivalents during the phosphate-to-fertilizer conversion process, and because this stream is effectively a zero-marginal-cost byproduct for phosphate producers who would otherwise bear disposal costs for a regulated hazardous acid, FSA-derived AlF₃ and cryolite can undercut natural fluorspar-sourced equivalents by 15–25% on a cost-of-fluorine basis in regions with established phosphate processing capacity such as North Africa, the Middle East, and parts of Eastern Europe.

The EU’s LIFE SYNFLUOR project funded under the LIFE environmental programme is actively validating a technology to recover synthetic calcium fluoride from fertilizer waste that would be directly substitutable for natural fluorspar in acid-grade applications, with pilot-scale results demonstrating CaF₂ purity levels above 95% that meet the threshold for most non-battery HF production uses; if scaled commercially, this technology could displace 200,000–400,000 tonnes per annum of natural acidspar demand in the EU alone within a 5–8 year horizon, equivalent to ~2.4–4.8% of current global mine output a substitution risk that is not yet embedded in consensus fluorspar demand forecasts and represents a latent structural downside not captured in headline CAGR figures.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| China Supply Concentration | -1.0% | Global — North America, EU, India (most exposed) | Short term (≤ 2 years) |

| Mine Development Lead Times | -0.7% | North America, EU, Australia (on-shoring regions) | Long term (≥ 4 years) |

| PFAS/Fluorochemical Regulatory Overhang | -0.6% | EU (core), North America; APAC (selective) | Medium term (2–4 years) |

| Environmental & Permitting Compliance Costs | -0.5% | Global — China, U.S., EU, South Africa (primary) | Short–Medium term (1–4 years) |

| Synthetic & Byproduct Substitutes | -0.4% | EU, North America; MENA (aluminum smelter belt) | Medium term (2–4 years) |

| Macro-Driven Price Volatility & Demand Cyclicality | -0.2% | Global — APAC (most price-sensitive), South America | Short term (≤ 2 years) |

Opportunity

African Fluorspar Asset Acquisition Unlocking Low-Geopolitical-Risk Reserves

The geopolitical calculus for this opportunity has shifted dramatically: with China’s mine rectification campaign having pushed Chinese self-import dependency to a 48% surge in H1 2025, and the U.S.–EU Critical Minerals Action Plan MoU of April 2026 explicitly earmarking investment promotion in non-Chinese supply corridors, African fluorspar assets now sit at the intersection of geopolitical urgency and structural underinvestment a combination that creates a narrow M&A window where asset valuations remain below intrinsic value before Western strategic buyers begin competing with Chinese state entities for the same resource base.

A 200,000-tonne-per-annum African acid-grade operation — requiring USD 80–120 million in greenfield CapEx would generate approximately USD 90–105 million in annual revenue at current benchmark pricing, implying a project-level EBITDA margin of 35–45% once steady-state production is achieved, with the added strategic premium of qualifying for EU Critical Raw Materials Act diversification credits and offtake premiums from European chemical companies seeking to document supply-chain provenance outside China for sustainability reporting obligations.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| Battery-Grade PVDF/LiPF₆ Vertical Integration | +1.2% | China, South Korea, India (core); North America, EU (growing) | Medium term (2–4 years) |

| African Fluorspar Asset Acquisition | +0.9% | Sub-Saharan Africa (origin); EU, North America (destination) | Medium–Long term (2–5 years) |

| Circular Fluorine Recovery | +0.7% | EU (regulatory mandate core); North America, South Korea, Japan | Long term (≥ 4 years) |

| PEM Green Hydrogen Electrolyzer Membranes | +0.6% | EU, Australia, Japan (core); India, North America (emerging) | Long term (≥ 4 years) |

| Pharmaceutical & Agrochemical Fluorination Chemistry | +0.5% | India (fastest-growing); EU, North America, China | Medium term (2–4 years) |

| India Domestic Fluorspar Production Scale-Up | +0.3% | India (primary); APAC spill-over | Short–Medium term (1–3 years) |

Challenge

Critical Minerals Talent Deficit Geologic, Process, and Engineering Expertise Shortage

The U.S. mining industry alone faces a net requirement for approximately 221,000 replacement workers by 2029 as more than half of the current workforce ages into retirement, while the number of accredited mining and minerals engineering programs at U.S. universities has shrunk from 25 in 1982 to 14 by 2014 and has not materially recovered since, meaning the educational pipeline produces roughly 1,500–2,000 mining engineering graduates per year against an industry demand that S&P Global and PwC estimate at 4,000–6,000 new hires annually to sustain expansion alongside attrition.

The 2026 PwC Mine Report explicitly identified talent shortfalls as a primary constraint, noting that 39% of mining employers expect an inability to attract talent to hinder their transformation programs and that output per worker has declined since 2020 as declining ore grades are compounded by under-staffed technical teams unable to optimize complex beneficiation circuits.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Ore Grade Decline & Beneficiation Cost Creep | -1.1% | China (Hunan, Zhejiang core); Mexico (Durango); global spill-over | Long term (≥ 4 years) |

| Critical Minerals Talent Deficit | -0.9% | North America, EU, Australia (on-shoring regions); Africa (frontier) | Long term (≥ 4 years) |

| HF Process Safety Liability & Insurance Friction | -0.7% | North America, EU, India (HF processing hubs) | Medium term (2–4 years) |

| ESG / Water-Energy Intensity at Mine Level | -0.6% | Global — China, South Africa, Mexico, Mongolia (most acute) | Medium–Long term (3–6 years) |

| Battery-Grade Purity Upgrade Technical Bottleneck | -0.5% | China (primary); South Africa, Inner Mongolia (secondary) | Medium term (2–4 years) |

| Digital Technology Adoption Gap in Fluorspar Operations | -0.3% | Global — emerging-market mine sites (Africa, APAC, LatAm) | Short–Medium term (1–3 years) |

Geopolitical Impact Analysis

Trade Policies and Regional Supply Tensions Are Directly Shaping the Global Fluorspar Market.

Trade policy and regional supply risks are playing a stronger role in the global fluorspar market. China remains the largest fluorspar producer, supported by its large mining base and downstream fluorochemical industry. This gives Chinese supply conditions a direct influence on global pricing, contract negotiations, and procurement planning. Past export quotas, duties, and licensing controls on fluorspar have also made international buyers more cautious, even when current restrictions are not applied in the same form.

Fluorspar is also gaining strategic importance because it is used to produce hydrofluoric acid, aluminum fluoride, refrigerants, fluoropolymers, and battery-related fluorochemicals. As a result, the U.S., Europe, and other import-dependent regions are placing more focus on supply security and non-Chinese sourcing. The Russia-Ukraine war has added further pressure by raising energy costs for Europe’s chemical industry, including energy-intensive fluorochemical operations. At the same time, South Africa and Kenya are gaining attention as alternative supply bases, especially where mining revival, beneficiation, and local processing can reduce dependence on raw ore imports.

Regional Analysis

Asia Pacific leads the Global Fluorspar Market with 58.5% revenue share in 2025.

In 2025, Asia Pacific maintained the leading position in the fluorspar market, supported by concentrated mining, chemical processing, steelmaking, and aluminum production. In February 2026, USGS estimated China’s 2025 fluorspar output at 6.0 million tons and Mongolia’s at 1.5 million tons, confirming the region’s strong supply base. North America remained an important consuming market, although the United States was 100% net import reliant and imported 380,000 tons in 2025.

Canada strengthened regional availability after restarting a mine in August 2025, targeting 200,000 tons of annual acid-grade capacity. Europe benefits from established fluorochemical and metallurgical industries, while fluorspar remains classified as an EU critical raw material. Latin America is supported by Mexico, which produced 1.5 million tons in 2025. The Middle East and Africa show developing potential, led by South Africa’s 410,000-ton output and increasing opportunities across steel, construction materials, and regional chemical processing activities during the coming industrial expansion cycle.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global fluorspar market is concentrated in relatively few hands, with Chinese producers collectively commanding the dominant share backed by the world’s largest mining and processing infrastructure. China Kings Resources Group and Sinochem Lantian operate at a scale that sets the market’s pricing rhythm, while Mexichem now operating under Orbia stands as the most consequential non-Chinese player, combining Mexican mining operations with downstream fluorochemical integration that pure miners cannot easily replicate.

Centralfluor Industries Group reinforces China’s grip on acid grade supply, while Koura Global and Kenya Fluorspar Company represent the diversification push that Western buyers are increasingly funding as supply security concerns move from background risk to boardroom priority. The competitive balance is shifting slowly but visibly producers outside China with high-purity reserves and processing ambitions are finding commercial leverage they simply did not have five years ago.

Market Key Players

- Orbia (Mexichem)

- Mongolrostsvetmet SOE

- China Kings Resources Group

- Inner Mongolia Baotou Steel Union

- Zhejiang Wuyi Shenlong Flotation

- Minersa

- SepFluor

- Haohua Chemical Science & Technology

- Luoyang FengRui Fluorine

- Masan High-Tech Materials

- Centralfluor Industries Group

- Kenya Fluorspar Company

- British Fluorspar Ltd.

- Tertiary Minerals plc

- Canada Fluorspar Inc.

- Others

Key Development

- May, 2026 – Mont Royal Resources / Commerce Resources – Received an extension of conditional funding approval of up to C$2.6 million from the Canadian government’s Critical Minerals Infrastructure Fund (CMIF) for the Ashram Rare Earths & Fluorspar Project in Quebec, supporting infrastructure and access road studies for future project development.

- January, 2026 – U.S. Department of Defense (DoD) / ARES Strategic Mining – The DoD awarded a long-term contract valued at approximately US$168.9 million (with a ceiling of up to US$250 million) for the supply of acid-grade fluorspar, highlighting fluorspar’s strategic importance within U.S. critical mineral security programs

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2.3 Bn |

| Forecast Revenue (2035) | USD 3.7 Bn |

| CAGR (2026-2035) | 4.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | Global Fluorspar Market Report By Product Type (Acid Grade Fluorspar, Metallurgical Grade Fluorspar, Ceramic Grade), By Application (Hydrofluoric Acid Production, Steel Production, Aluminum Production, Glass & Ceramics, Others), By End-Use Industry (Chemical Industry, Steel Industry, Aluminum Industry, Glass & Ceramics Industry, Others), By Form (Dry Powder, Lump, Filter Cake, Others), By Distribution Channel (Direct Sales, Indirect Sales), By Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2035 |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Orbia (Mexichem), Mongolrostsvetmet SOE, China Kings Resources Group, Inner Mongolia Baotou Steel Union, Zhejiang Wuyi Shenlong Flotation, Minersa, SepFluor, Haohua Chemical Science & Technology, Luoyang FengRui Fluorine, Masan High-Tech Materials, Centralfluor Industries Group, Kenya Fluorspar Company, British Fluorspar Ltd., Tertiary Minerals plc, Canada Fluorspar Inc., Others. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |