Quick Navigation

Report Overview

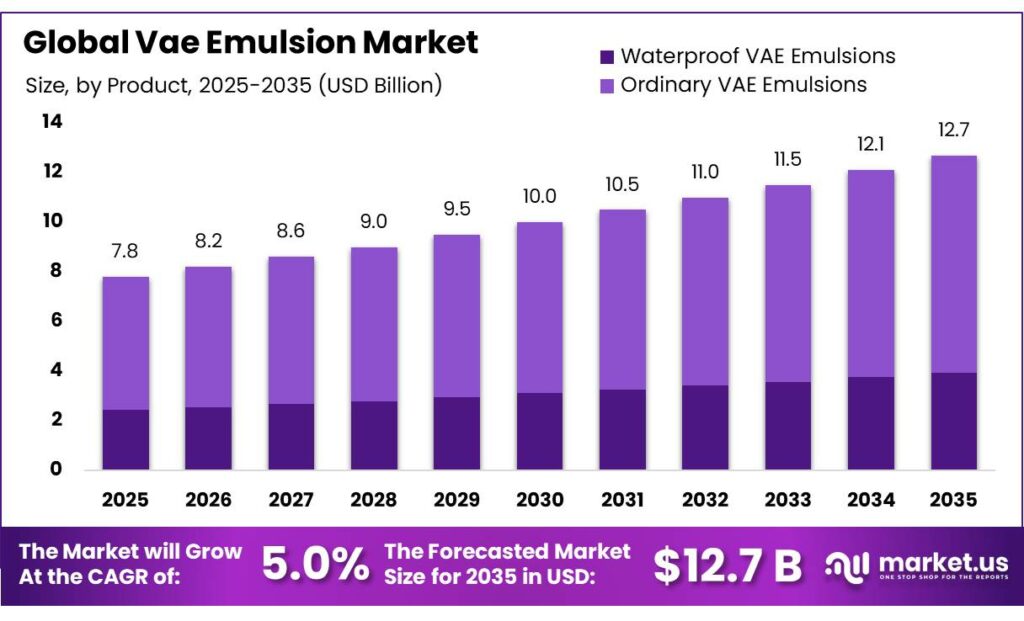

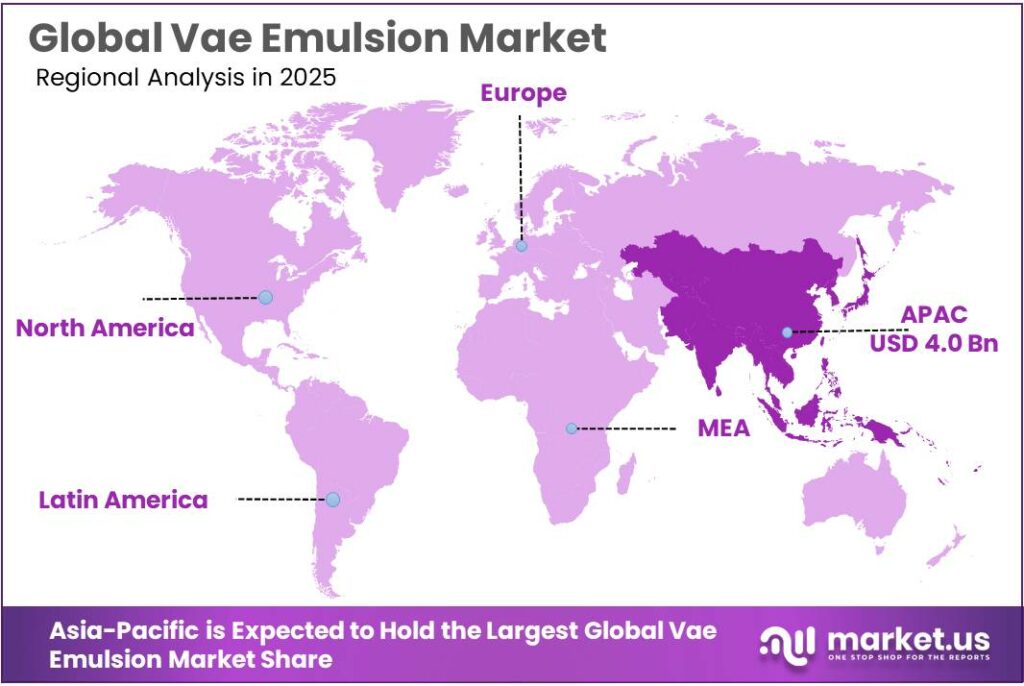

The Global Vae Emulsion Market size is expected to be worth around USD 12.7 Billion by 2035, from USD 7.8 Billion in 2025, growing at a CAGR of 5.0% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 51.8% share, holding USD 4.0 Billion revenue.

Vinyl acetate-ethylene (VAE) emulsion remains a strategically important water-based binder for coatings, construction materials, paper and packaging adhesives, carpet applications, and selected nonwovens because it combines flexibility, adhesion, low odor, and comparatively low volatile organic compound (VOC) formulation potential.

In industrial terms, its relevance is strongest where producers are shifting from higher-VOC solvent systems toward waterborne chemistries without sacrificing film formation or bond strength. That positioning is supported by formal regulation as well as end-use demand: in the United States, national VOC standards for architectural coatings remain in force under 40 CFR Part 59 Subpart D, while the EU’s Packaging and Packaging Waste Regulation, Regulation (EU) 2025/40, is pushing the packaging chain toward more sustainable material choices and compliance discipline.

The present industrial scenario remains most closely tied to construction and refurbishment activity, because VAE emulsions are heavily consumed in tile adhesives, wall systems, paints, façade materials, and flooring formulations. In the United States, total construction spending reached a seasonally adjusted annual rate of $2,190.4 billion in January 2026, with residential construction at $933.0 billion, nonresidential at $728.2 billion, and highway construction at $148.5 billion.

In Europe, Eurostat reported that EU construction production in October 2025 increased 0.8% month on month and 1.3% year on year. This points to a still-active downstream demand base for binders used in dry-mix mortars, coatings, and specialty adhesives, even as regional sub-segments move unevenly.

The main demand drivers are increasingly regulatory and performance-led rather than purely volume-led. The European Commission states that buildings account for around 40% of EU energy consumption, around 50% of EU gas consumption, and about 80% of energy used in EU homes for heating, cooling, and hot water.

In parallel, the EU Renovation Wave aims to renovate 35 million buildings by 2030 and at least double the annual rate of energy renovations. Such policy direction favors VAE emulsion because formulators need binders that help construction products maintain adhesion, flexibility, and durability in lower-carbon building systems and renovation materials.

The European Commission’s packaging rules target making all packaging on the EU market recyclable in an economically viable way by 2030 and place the sector on track to climate neutrality by 2050. That matters for VAE because water-based adhesive and coating systems are already used in paper packaging, converting, and specialty laminating applications. At the same time, U.S. EPA VOC standards for architectural coatings continue to support the shift toward waterborne technologies, reinforcing the competitive position of low-odor, low-VOC VAE-based formulations.

In 2025, WACKER highlighted at the European Coatings Show that the cement industry is increasingly shifting from Portland cement CEM I to Portland composite cement CEM II, and presented VINNAPAS solutions designed to help dry-mix mortar producers maintain performance through that transition. WACKER had also identified a 2025 VAE dispersion capacity expansion in Calvert City as part of its growth pipeline.

Key Takeaways

- Vae Emulsion Market size is expected to be worth around USD 12.7 Billion by 2035, from USD 7.8 Billion in 2025, growing at a CAGR of 5.0%.

- Ordinary VAE Emulsions held a dominant market position, capturing more than a 69.4% share.

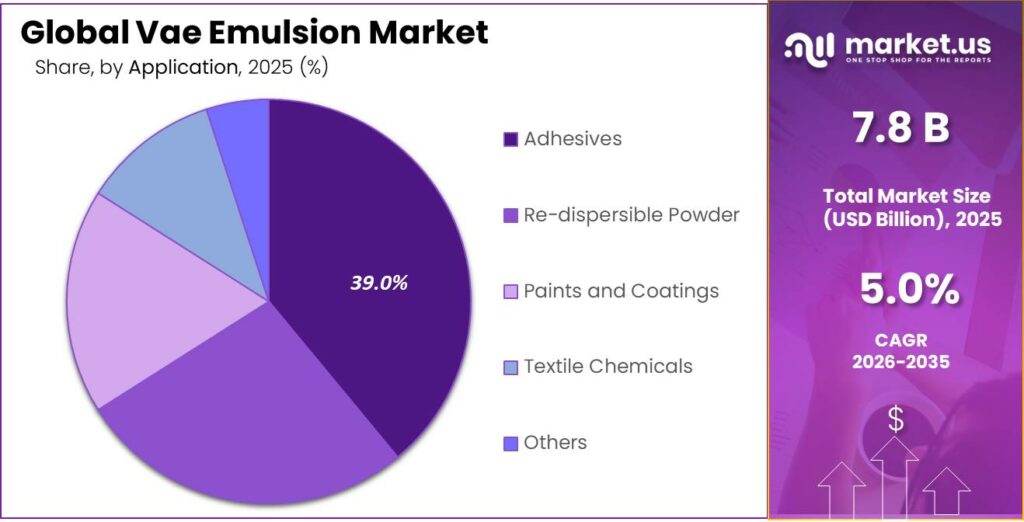

- Adhesives held a dominant market position, capturing more than a 39.5% share.

- Asia-Pacific emerged as the dominating region in the VAE emulsion market, accounting for 51.8% of the global share and valued at USD 4.0 Bn.

By Product Analysis

Ordinary VAE Emulsions dominates with 69.4% share, supported by its everyday use across adhesives, paints, and construction applications.

In 2025, Ordinary VAE Emulsions held a dominant market position, capturing more than a 69.4% share. This strong position was mainly supported by its wide usage in standard adhesive formulations, interior paints, paper processing, and general construction chemicals where reliable bonding performance and easy formulation are more important than premium specialty properties. Its consistent demand from packaging, woodworking, and building material manufacturers helped this segment stay ahead, as many end users continue to prefer cost-efficient and proven emulsion grades for large-volume production.

By Application Analysis

Adhesives leads with 39.5% share, driven by strong demand from packaging, woodworking, and construction bonding uses.

In 2025, Adhesives held a dominant market position, capturing more than a 39.5% share. This leading share was mainly supported by the broad use of VAE emulsions in packaging adhesives, woodworking glue, paper lamination, labels, and construction bonding products where strong adhesion, flexibility, and low VOC performance are highly valued. The segment continued to benefit from steady demand across furniture manufacturing, carton sealing, and bookbinding applications, as producers increasingly preferred VAE-based adhesive systems for their dependable bonding strength and ease of use on different substrates.

Key Market Segments

By Product

- Waterproof VAE Emulsions

- Ordinary VAE Emulsions

By Application

- Adhesives

- Re-dispersible Powder

- Paints and Coatings

- Textile Chemicals

- Others

Emerging Trends

Low-VOC and green building certifications are the latest trend shaping VAE emulsion demand

One of the most visible latest trends in the VAE emulsion market is the fast movement toward low-VOC, green-certified construction materials, especially in adhesives, interior coatings, tile systems, and dry-mix mortars. VAE emulsions are increasingly becoming the preferred binder because they support water-based formulations, better indoor air quality, and easier compliance with green building standards. A strong indicator of this trend comes from India’s green building materials ecosystem, which is projected to reach US$ 70–80 billion by 2030, expanding at 10–12% CAGR, supported by policy-led sustainable construction and low-emission material adoption.

This is directly increasing the use of VAE emulsions in wall putty, skim coats, insulation adhesives, and eco-friendly paints where solvent-free performance is now a key buying factor. In 2025 and continuing into 2026, builders are not only looking for bonding strength, but also materials that help projects qualify for LEED, GRIHA, and similar certification systems. This shift is making low-odor and safer VAE grades one of the most practical formulation choices across modern residential and commercial projects.

Government-backed urban housing and sustainable infrastructure are pushing specialty VAE use

Another important trend is the rising use of specialty VAE emulsions in affordable housing and smart infrastructure projects backed by public sustainability initiatives. India alone is expected to add over 35 billion square feet of new built space by 2050, which is nearly double the current stock, creating massive long-term demand for polymer-modified mortars, tile adhesives, repair compounds, and crack-resistant coatings.

Government schemes focused on urban housing, metro expansion, public buildings, and low-carbon infrastructure are encouraging the use of water-based materials that are easier to apply and safer for enclosed environments. This is gradually shifting demand from ordinary emulsions toward higher-performance VAE grades that offer better flexibility, moisture resistance, and durability. In simple terms, the latest market trend is no longer only about volume growth, but about performance plus sustainability, where VAE emulsions are being tailored for green construction specifications.

Drivers

Rising construction and low-VOC building materials demand is a major growth driver for VAE emulsion

One of the strongest driving factors for the VAE emulsion market is the steady rise in construction activity and the growing shift toward low-VOC, water-based building materials. VAE emulsions are widely used in tile adhesives, wall putty, waterproofing coatings, cement modification, and insulation bonding systems, all of which move directly with residential and infrastructure growth. A strong example comes from India’s cement sector, where production reached approximately 391 million tonnes in FY 2024–25, reflecting robust building and renovation activity supported by public infrastructure spending and housing demand.

This directly lifts the need for VAE-based dry mix mortars and construction adhesives used in modern building systems. Government-backed housing programs, smart city development, and urban transport expansion are also increasing the use of environmentally safer bonding materials, where VAE emulsions are preferred because of their flexibility, crack resistance, and low odor profile. In 2026, this trend is expected to stay strong as more countries continue to tighten emission rules for solvent-based chemicals, pushing builders and formulators toward water-based polymer systems.

Packaging and paper converting expansion continues to push adhesive-grade VAE consumption

Another major factor supporting VAE emulsion demand is the rapid expansion of packaging, labeling, and paper converting industries. VAE emulsions are commonly used in carton sealing, paper lamination, label stock, bookbinding, and flexible packaging adhesives because they provide strong bonding, good film formation, and safer low-emission performance. A trusted industrial indicator is the global packaging industry, which crossed USD 1.18 trillion in 2025, driven by e-commerce shipments, food delivery, pharmaceutical packaging, and retail logistics growth.

This rise in packaging volume directly increases adhesive consumption, especially water-based formulations where VAE remains a preferred chemistry. Food and beverage packaging has been one of the biggest contributors, as brands increasingly shift toward recyclable paper-based packs that require reliable adhesive performance. Public sustainability initiatives encouraging reduced plastic waste and better recycling compatibility are also helping VAE-based paper adhesives gain wider acceptance. Moving into 2026, stronger corrugated box demand and label stock production are expected to keep this growth factor highly influential for the market.

Restraints

Raw material price volatility remains a key restraint for VAE emulsion demand

One major restraining factor for the VAE emulsion market is the frequent fluctuation in raw material prices, especially vinyl acetate monomer (VAM) and ethylene, both of which are closely linked to crude oil and natural gas value chains. When feedstock costs move sharply, manufacturers face pressure on production margins, and this often leads to unstable pricing for adhesives, paints, and construction additives made with VAE emulsions. A clear signal comes from the energy side: the U.S. produced a record 13.2 million barrels per day of crude oil in 2024, highlighting how strongly petrochemical chains still depend on oil-linked supply economics.

Even when supply is high, geopolitical risks, freight disruptions, and refinery outages can quickly shift downstream ethylene and VAM prices. This creates uncertainty for adhesive and dry-mix mortar producers that work on long-term supply contracts. In 2025, many buyers continued to prefer shorter procurement cycles to avoid cost spikes, which limited aggressive volume commitments for VAE-based formulations. Moving into 2026, this pricing instability is still expected to remain a major challenge, especially for small and mid-sized formulators operating in cost-sensitive construction and packaging markets.

Margin pressure on construction and packaging converters slows wider VAE adoption

The impact of raw material volatility becomes even stronger at the converter level, where adhesive, paper coating, and construction chemical manufacturers often cannot immediately pass higher costs to customers. This creates a practical restraint on VAE emulsion usage growth, particularly in price-driven emerging markets. For example, the International Energy Agency noted that global oil demand rose to around 103.9 million barrels per day in 2025, keeping petrochemical feedstock markets highly sensitive to supply-demand shifts.

Opportunity

Green building and low-VOC construction materials create the biggest growth opportunity for VAE emulsion

One of the strongest growth opportunities for the VAE emulsion market is the fast shift toward green building materials and low-VOC construction systems. VAE emulsions fit naturally into this trend because they are water-based, safer to use indoors, and widely used in tile adhesives, wall putty, skim coats, waterproofing layers, and insulation bonding systems. A strong industry indicator comes from India’s green building push, where the green building materials market is projected to reach US$ 70–80 billion by 2030, growing at 10–12% annually, supported by policy-led sustainable construction and lower-emission building targets.

This directly opens new demand for VAE-based binders in eco-friendly mortars and modern façade systems. Government-backed housing expansion, smart city projects, and public infrastructure upgrades are further increasing the use of polymer-modified cement systems that need flexible and durable emulsions. In 2025 and moving into 2026, builders are increasingly choosing materials that support indoor air quality and green certifications, which gives VAE emulsions a clear long-term opportunity across both residential and commercial construction.

Public infrastructure and affordable housing programs expand adhesive and mortar demand

Another major growth opportunity comes from government-supported housing and infrastructure development, especially where sustainable materials are becoming part of procurement standards. India is expected to add over 35 billion square feet of new built space by 2050, which is nearly double the current stock, showing the long runway for advanced construction chemicals and binders.

This expansion creates direct demand for VAE emulsions in cement modifiers, crack-resistant repair mortars, tile fixing adhesives, and external insulation systems. Public sector focus on lower-emission construction materials is also improving acceptance of water-based polymer technologies in roads, metro projects, housing clusters, and institutional buildings. As more governments push green procurement and sustainable urban development in 2026, the opportunity for VAE emulsions becomes stronger not only in traditional adhesives but also in specialty dry-mix and energy-efficient building envelope applications.

Regional Insights

Asia-Pacific dominated the VAE Emulsion market with a 51.8% share, reaching USD 4.0 Bn, backed by strong construction, packaging, and manufacturing demand across China, India, and Southeast Asia.

Asia-Pacific emerged as the dominating region in the VAE emulsion market, accounting for 51.8% of the global share and valued at USD 4.0 Bn. The region’s leadership is mainly supported by its large-scale construction activity, expanding packaging sector, strong paints and coatings production, and fast-growing adhesive consumption across major economies such as China, India, Japan, South Korea, and ASEAN countries.

A major strength of Asia-Pacific lies in its massive infrastructure pipeline and manufacturing-led economies. Countries across Southeast Asia are also becoming increasingly influential in industrial production and trade expansion, with economic strength remaining the largest contributor to regional growth momentum. Recent regional economic assessments show that the economic dimension contributes nearly 35–40% of the region’s overall influence structure, highlighting the strong industrial and production base that supports downstream polymer demand.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Wacker Chemie AG remains one of the most influential players in the VAE emulsion market, supported by its strong VINNAPAS® dispersion portfolio used in adhesives, construction chemicals, and coatings. In 2025, the company reported €5.5 billion in annual sales, showing its strong global chemical footprint and deep reach in polymer dispersions. Its 27 production sites and 47 sales offices further strengthen supply reliability across Asia-Pacific and Europe.

Vinavil holds a strong place in the VAE emulsion market through its established expertise in polymer emulsions, dispersions, and specialty binders for industrial use. The company is particularly strong in Europe, where demand for low-emission adhesives and construction materials continues to rise. In numerical terms, its strength comes from high-volume supply into paper, packaging, textile, and building chemistry applications, where VAE emulsions remain a preferred water-based binder.

Celanese continues to hold a strong numerical position in the VAE emulsion space through its broad emulsion polymers and adhesive raw material business. The company benefits from its global acetyl chain integration, which gives better control over vinyl acetate-based feedstock economics, a major competitive advantage in this market. In 2025, Celanese maintained strong exposure across construction adhesives, paper packaging, and specialty coatings, where VAE demand remained linked to low-VOC formulations.

Top Key Players Outlook

- Wacher Chemie AG

- Celanese

- DCC

- Vinavil

- The Beijing Eastern Petro-chemical

- Wanwei

- BouLing Chemical Co., Limited

- Sinopec Sichuan Vinylon Works

- Sumika Chemtex Company, Limited

- Shaanxi XuTai Technology Co., Ltd

- Yunnan Zhengbang Technology

Recent Industry Developments

In 2025, Wacker Chemie AG continued to strengthen its leadership in the VAE emulsion sector through its well-established VINNAPAS® VAE dispersions and polymer binders portfolio, which is widely used in adhesives, tile mortars, waterproofing systems, paints, and paper coatings. The company’s polymers division, which includes VAE dispersions, reported €1,463 million in sales in 2024, giving a strong base for its 2025 market momentum.

Celanese also continues to benefit from strong backward integration in vinyl acetate monomer (VAM), giving it a cost and supply advantage in VAE production. A major numerical strength is its 2025 full-year net sales of USD 9.5 billion, supported by the broader acetyl and emulsion materials portfolio.

In 2025, DCC’s role linked to the VAE emulsion value chain is best understood through its specialty distribution strength and industrial supply reach rather than direct manufacturing, making it an important channel partner for adhesives, construction chemicals, coatings, and packaging raw materials where VAE emulsions are widely consumed. The company reported £18.0 billion in group revenue for FY 2025, with £617.5 million in adjusted operating profit, showing strong scale in industrial distribution and customer access across multiple end-use sectors.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 7.8 Bn |

| Forecast Revenue (2035) | USD 12.7 Bn |

| CAGR (2026-2035) | 5.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Waterproof VAE Emulsions, Ordinary VAE Emulsions), By Application (Adhesives, Re-dispersible Powder, Paints and Coatings, Textile Chemicals, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Wacher Chemie AG, Celanese, DCC, Vinavil, The Beijing Eastern Petro-chemical, Wanwei, BouLing Chemical Co., Limited, Sinopec Sichuan Vinylon Works, Sumika Chemtex Company, Limited, Shaanxi XuTai Technology Co., Ltd, Yunnan Zhengbang Technology |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |