Quick Navigation

Report Overview

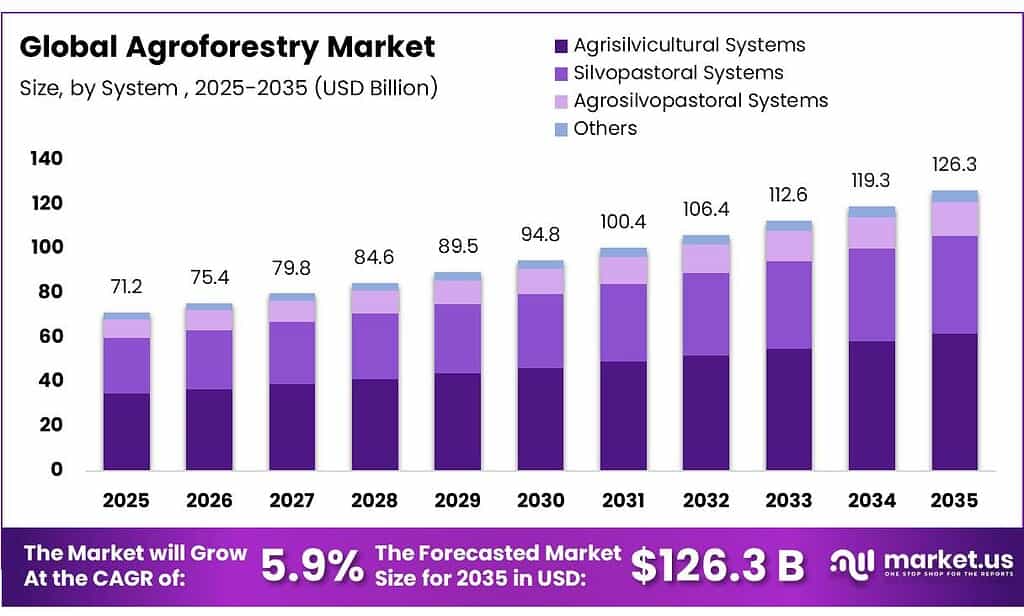

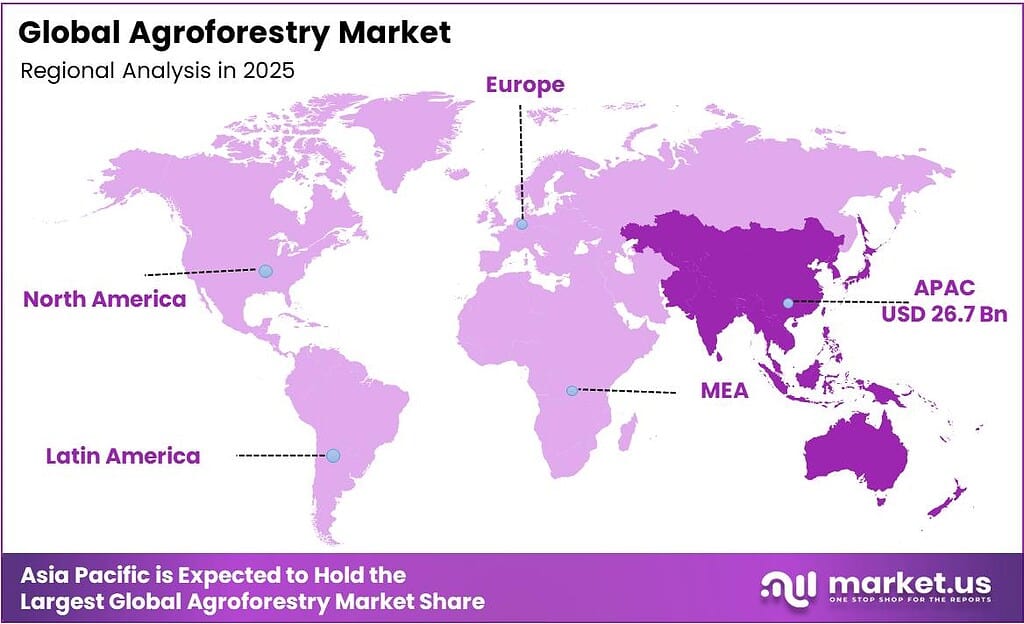

The Global Agroforestry Market size is expected to be worth around USD 126.3 Billion by 2035, from USD 71.2 Billion in 2025, growing at a CAGR of 5.9% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 37.5% share, holding USD 5.5 Billion revenue.

Agroforestry is a sustainable land management system that intentionally integrates trees and shrubs (woody perennials) with agricultural crops and/or livestock on the same piece of land. This practice aims to create ecological and economic interactions between these components to enhance overall productivity and environmental health.

- According to the study by the FAO in 2024, agro forestry spans over 43% of global agricultural land, where 30% of the rural population resides, indicating a large pre-existing base for policy-driven scaling.

The agro forestry sector is shaped by the integration of trees with crops and/or livestock to enhance productivity, resilience, and environmental outcomes. The agriculturalist systems dominate due to their compatibility with crop-based smallholder farming, lower capital needs, and more predictable short-term returns. Timber-oriented models are particularly prevalent, supported by established processing industries and clearer regulatory pathways compared to non-timber products.

Sustainability imperatives and environmental regulations are key structural drivers, as agro forestry contributes to carbon sequestration, biodiversity conservation, and land restoration. Similarly, adoption is constrained by high upfront establishment costs, delayed returns from tree components, and land tenure or policy uncertainties affecting long-term investments.

Furthermore, technological integration, such as precision agriculture and digital monitoring, is emerging as an enabling factor to manage system complexity and improve efficiency. Regionally, countries such as India and China anchor large-scale adoption through policy support and extensive smallholder participation. The sector reflects a balance between ecological benefits, economic practicality, and regulatory alignment.

Key Takeaways

- The global agroforestry market was valued at USD 71.2 billion in 2025.

- The global agroforestry market is projected to grow at a CAGR of 5.9% and is estimated to reach USD 126.3 billion by 2035.

- Based on the system of agroforestry, agrisilvicultural systems dominated the agroforestry market, with a market share of around 48.9%.

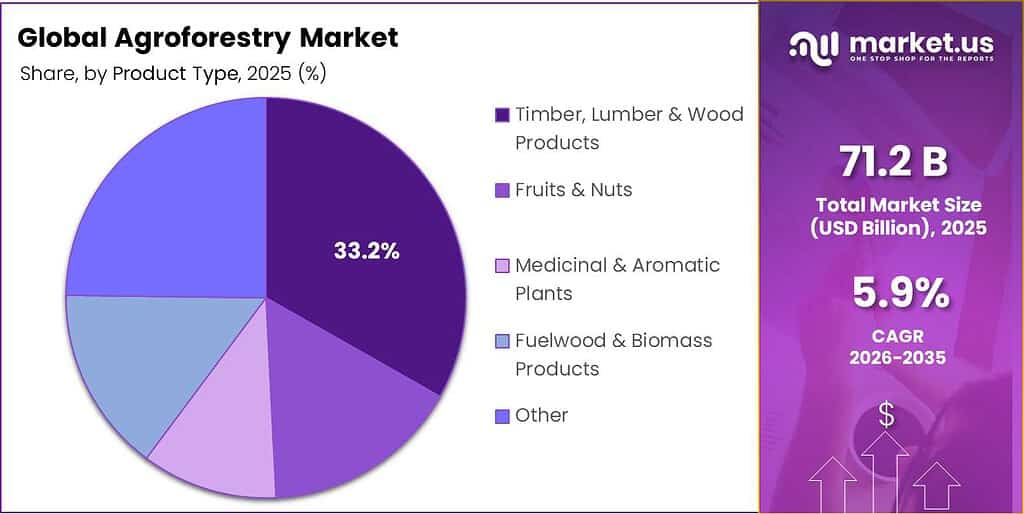

- Among the product types of agroforestry, timber, lumber & wood products held a major share in the market, 33.2% of the market share.

- In 2025, the Asia Pacific was the most dominant region in the agroforestry market, accounting for around 37.5% of the total global consumption.

System Analysis

Agrisilvicultural Systems Held the Largest Share in the Agroforestry Market.

The agroforestry market is segmented based on compound type into agrisilvicultural systems, silvopastoral systems, agrosilvopastoral systems, and others. The agrisilvicultural systems dominated the agroforestry market, comprising around 48.9% of the market share, as they align closely with existing smallholder farming structures and food security priorities.

Most farms, particularly in regions such as India and China, are crop-centric, making tree-crop integration operationally simpler than introducing livestock components. These systems require lower capital investment and management complexity compared to silvopastoral or agrosilvopastoral models, which depend on grazing management, fodder systems, and animal health infrastructure.

Agrisilviculture further provides earlier and more predictable returns through annual crops, while trees mature over longer cycles, reducing income risk. Land constraints further favour this model, as livestock-based systems need larger contiguous areas. In addition, regulatory and cultural factors, such as land-use norms and limited grazing rights, often restrict livestock integration, reinforcing the dominance of tree-crop systems in agroforestry adoption.

Product Type Analysis

Timber, Lumber & Wood Products Dominated the Agroforestry Market.

Based on the product types of agroforestry, the market is divided into timber, lumber & wood products, fruits & nuts, medicinal & aromatic plants, fuelwood & biomass products, and other. The timber, lumber & wood products dominated the agroforestry market, with a market share of 33.2%. Agroforestry is most widely oriented toward timber, lumber, and wood products as these outputs align with clear regulatory frameworks, established value chains, and standardized grading systems.

In countries such as India, policy reforms have simplified tree harvesting and transit for commercially important timber species, creating predictable market access compared with non-timber products. In addition, timber trees offer high biomass accumulation and long rotation value, enabling farmers to use them as a form of asset storage or risk diversification. In contrast, fruits, nuts, and medicinal plants often require specialized post-harvest handling, cold chains, or processing infrastructure, which are less accessible in rural settings.

Moreover, fuelwood and biomass products, while widely used, are typically low-value and locally consumed, limiting their role in structured markets. Additionally, wood-based industries, such as construction, plywood, and paper, generate consistent bulk demand, reinforcing farmer preference for timber-oriented agroforestry systems.

Key Market Segments

By System

- Agrisilvicultural Systems

- Silvopastoral Systems

- Agrosilvopastoral Systems

- Others

By Product Type

- Timber, Lumber & Wood Products

- Fruits & Nuts

- Medicinal & Aromatic Plants

- Fuelwood & Biomass Products

- Other

Drivers

Shift Towards Sustainability Drives the Agroforestry Market.

The agroforestry market is primarily driven by a global shift toward sustainability and stringent environmental regulations aimed at climate mitigation and biodiversity conservation. Institutional frameworks, such as the United Nations Sustainable Development Goals (SDGs) and the Paris Agreement, have repositioned agroforestry as a nature-based solution.

To meet net-zero commitments, governments are incentivizing terrestrial carbon management. Agroforestry is a key mechanism, with research indicating its potential to contribute to a 3.1%-3.5% reduction in Mean Species Abundance (MSA) loss globally through improved ecosystem management. Similarly, regulations such as the UN Convention on Biological Diversity drive adoption by mandating habitat protection.

Moreover, environment-centric Official Development Assistance (ODA) for agroforestry has increasingly focused on the process. For instance, since 1997, approximately 57.03%, US$43.64 million, of aid has been allocated specifically to biodiversity conservation. Furthermore, in India, complementary programs through agroforestry policies aim to restore 26 million hectares of degraded land and contribute to 2.5-3 billion tons of CO₂-equivalent carbon sinks, embedding agroforestry within climate commitments.

Restraints

Significant Upfront Investment Might Hamper the Growth of the Agroforestry Market.

The agroforestry market faces significant structural barriers, specifically high initial establishment costs and insecure land tenure, which impede widespread adoption despite long-term profitability. The establishment of agroforestry is capital-intensive compared to mono-cropping. Similarly, high establishment and maintenance costs create significant time lags. Feasibility studies indicate a payback period of approximately 6 years and 2 months for agroforestry projects, compared to the immediate, lag-free returns of conventional monocultures such as maize.

Furthermore, while agroforestry can outperform cereal mono-cropping in Net Present Value (NPV), short-term financial constraints often make the required investments non-viable for smallholders without subsidies. Moreover, only 25% of land is formally recognized, and only 10% of indigenous and community-managed land is legally documented. Farmers without secure, long-term tenure are less likely to invest in woody perennials that take years to mature.

Similarly, eligibility for preferential property tax programs (PPTPs) often disincentives agroforestry. For instance, in the U.S., some state statutes require land to return at least US$10,000/year in gross income for two consecutive years, a threshold difficult for new agroforestry systems to meet during early growth phases.

Opportunity

Smart Agriculture Systems Create Opportunities in the Agroforestry Market.

The integration of smart agriculture systems presents a structural opportunity for agroforestry by improving the productivity, manageability, and ecological performance of multi-layered land-use systems. Digital agriculture, encompassing IoT, remote sensing, and AI, enables real-time monitoring of soil moisture, tree-crop interactions, and microclimatic conditions, which are otherwise complex in agroforestry settings.

For instance, IoT-enabled systems have demonstrated a 30% reduction in water use by utilizing real-time soil moisture and weather data to ensure precise application. Similarly, big data analytics can optimize nitrogen fertilizer application, leading to estimated cost reductions of 15% and enhancing crop yield predictions by up to 25%. Similarly, AI-driven digital soil mapping algorithms have reduced physical soil sampling requirements by 40%, improving the accuracy of carbon sequestration assessments essential for agroforestry’s role in climate mitigation.

For agroforestry, these capabilities address inherent system complexity by digitizing heterogeneous components, thereby lowering management uncertainty and improving long-term productivity, sustainability, and traceability within regulated agricultural systems.

Trends

Adoption of Silvopasture and Livestock Systems.

The adoption of silvopasture, the deliberate integration of trees, forage, and livestock, is an accelerating trend driven by its capacity to improve animal welfare and system-wide productivity. The silvopasture can significantly increase global system productivity compared to traditional open-pasture systems. For instance, in the Caribbean region of Colombia, silvopastoral schemes showed a 13% (± 25%) increase in carrying capacity per hectare and a 3-litre increase in milk production per surface unit.

Similarly, high retention rates reflect producer satisfaction. According to a case study, approximately 88% of producers who adopt silvopasture intend to continue the practice. Furthermore, 96% of producers use silvopasture as a complementary component in their rotational grazing systems rather than a total replacement. Furthermore, the silvopastoral systems can restore degraded rangelands and improve livestock productivity simultaneously.

Moreover, it was noted that in fire-prone regions, managed silvopasture has been shown to reduce grass biomass and litter depth, lowering potential fuel loads compared to non-grazed forests. This trend reflects a shift from monoculture grazing toward integrated land-use systems that align livestock production with climate resilience, land restoration, and diversified farm outputs.

Geopolitical Impact Analysis

Geopolitical Tensions Are Impacting the Supply Chains for Inputs of the Agroforestry Market.

The geopolitical tensions are exerting measurable, multi-channel impacts on agroforestry through input markets, trade flows, and land-use decisions. Agrifood systems are structurally exposed as input supply chains, such as for fertilizer, fuel, and machinery, are tightly interconnected with global trade networks. Disruptions in conflict zones and transit corridors directly transmit cost shocks. For instance, fertilizer prices rose between late 2025 and early 2026 amid conflict-linked supply constraints, affecting farm-level input use decisions.

Additionally, trade disruptions further amplify volatility. Around 20% of global calories are traded internationally, making agricultural systems sensitive to geopolitical instability and export restrictions. The conflicts in major producing regions have disrupted grain exports, elevating food prices and altering cropping patterns. Such volatility can indirectly favor agroforestry adoption, where it reduces dependence on external inputs and diversifies production, but it can further delay long-gestation tree investments due to heightened uncertainty.

Price and supply volatility are explicitly linked to geopolitical risks in agricultural outlook assessments, which note increased market instability and input-access constraints under such conditions. The geopolitical tensions function as a dual constraint. They elevate input costs and trade uncertainty, discouraging long-term investments such as agroforestry, while simultaneously reinforcing the strategic value of diversified, low-input production systems.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Agroforestry Market.

In 2025, the Asia Pacific dominated the global agroforestry market, holding about 37.5% of the total global consumption. The region constitutes the largest agroforestry base due to land availability, policy integration, and high smallholder dependence on mixed farming systems.

It accounts for a substantial share of global agroforestry practitioners, with countries such as India and China leading adoption. India alone reports agroforestry across approximately 28 million hectares, supported by the National Agroforestry Policy, which formalizes tree-crop integration within agricultural systems.

According to a study by the FAO, over 60% of rural households in parts of Asia depend on tree-based systems for fuelwood, fodder, or supplementary income. In China, large-scale ecological restoration programs have converted cropland to tree-based systems, embedding agroforestry principles in land-use transitions.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers and input providers in agroforestry focus on integrated, field-oriented strategies to strengthen competitiveness. A primary area is the development of high-yielding, climate-resilient tree seedlings and planting material, often aligned with national afforestation and land-restoration programs. Additionally, firms invest in nursery expansion and decentralized propagation networks to improve last-mile availability for smallholders.

Another key activity is technical extension and farmer training, including advisory on species selection, intercropping models, and compliance with local tree-felling and transit regulations. Companies increasingly integrate digital agriculture tools to optimize plantation management and traceability. Similarly, manufacturers emphasize sustainable certification, supply-chain traceability, and carbon-accounting frameworks, enabling participation in climate-linked procurement and ecosystem service markets while differentiating product quality and reliability.

The Major Players in The Industry

- Weyerhaeuser Company

- ArborGen LLC

- EcoPlanet Bamboo

- Green Resources AS

- Stora Enso

- Suzano S.A.

- West Fraser Timber Co. Ltd.

- Gratitude Farms

- Natba Greene

- Mul Biotech Farms

- Other Key Players

Key Development

- In October 2025, Weyerhaeuser Company announced a commitment to invest US$1 million in Buckhannon, West Virginia, through its THRIVE program.

- In January 2026, the Food and Agriculture Organization (FAO) launched a two-year regional project Greening Agroforestry Economies strengthening non-wood forest product chains and smallholder cooperatives.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 71.2 Bn |

| Forecast Revenue (2035) | US$ 126.3 Bn |

| CAGR (2026-2035) | 5.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By System (Agrisilvicultural Systems, Silvopastoral Systems, Agrosilvopastoral Systems, and Others), By Product Type (Timber, Lumber & Wood Products, Fruits & Nuts, Medicinal & Aromatic Plants, Fuelwood & Biomass Products, and Other) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Weyerhaeuser Company, ArborGen LLC, EcoPlanet Bamboo, Green Resources AS, Stora Enso, Suzano S.A., West Fraser Timber Co. Ltd., Gratitude Farms, Natba Greene, Mul Biotech Farms, and Other Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |