Quick Navigation

Report Overview

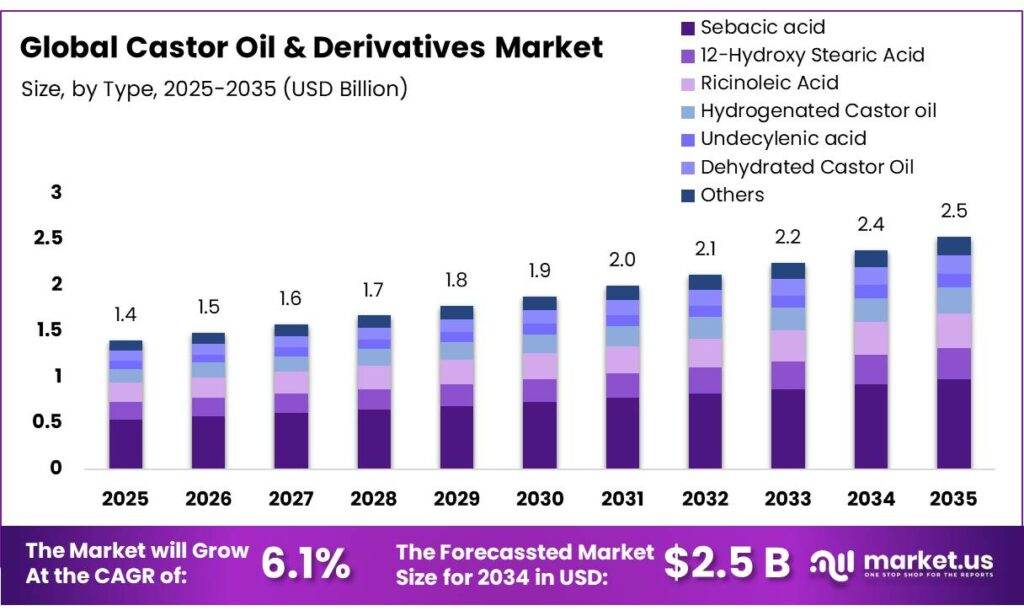

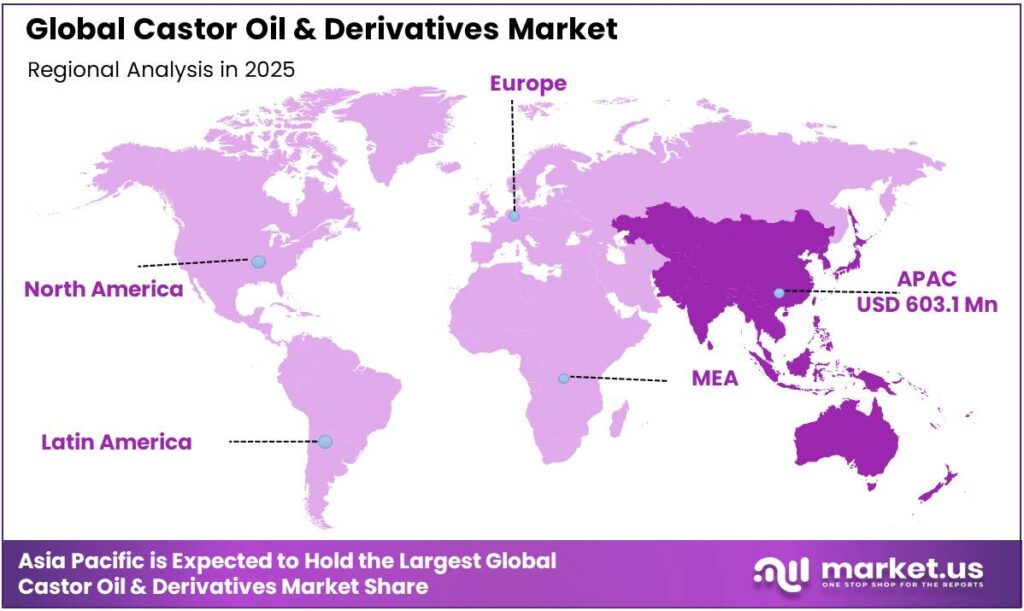

The Global Castor Oil And Derivatives Market size is expected to be worth around USD 2.5 Billion by 2035, from USD 1.4 Billion in 2025, growing at a CAGR of 6.1% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 43.7% share, holding USD 0.6 Billion revenue.

Castor oil is a versatile vegetable oil extracted from the seeds of the ricinus communis plant. It is unique among vegetable oils due to its high concentration of ricinoleic acid, a rare 18-carbon fatty acid that contains a hydroxyl group. This specific chemical structure allows it to be modified into hundreds of industrial derivatives that are often superior to petroleum-based alternatives.

The castor oil and derivatives market is characterized by high supply concentration, strong bio-based demand drivers, and diversified downstream applications. Production is geographically concentrated, with countries such as India accounting for the majority of global output, creating structural dependence on a limited agro-climatic base.

- India alone produces around 18 to 20 Lakh tons of castor seed and meets over 90% of global castor oil demand.

The castor oil’s non-edible, renewable nature and high ricinoleic acid content enable its conversion into key intermediates such as sebacic acid and undecylenic acid, which support large-scale use in polymers, plastics, and resins. These segments dominate consumption due to their high material intensity and integration into durable industrial applications.

Emerging trends include increasing adoption in biopolymers and personal care formulations, supported by regulatory acceptance and performance characteristics. However, the market faces constraints from ricin toxicity handling requirements, agricultural variability, and trade concentration risks. The sector is shaped by a combination of renewability-driven demand, chemical versatility, and supply-side concentration, influencing both growth opportunities and operational challenges.

Key Takeaways

- The global castor oil & derivatives market was valued at USD 1.4 billion in 2025.

- The global castor oil & derivatives market is projected to grow at a CAGR of 6.1% and is estimated to reach USD 2.5 million by 2035.

- Based on the types of castor oil & derivatives, sebacic acid dominated the castor oil & derivatives market, with a market share of around 38.7%.

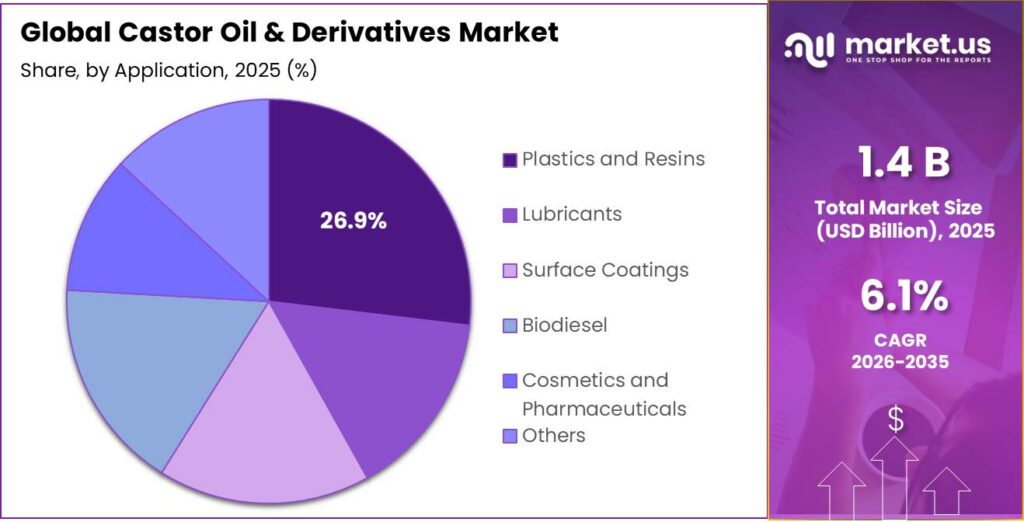

- Among the applications of castor oil & derivatives, plastics and resins held a major share in the market, 26.9% of the market share.

- In 2025, the Asia Pacific was the most dominant region in the castor oil & derivatives market, accounting for around 43.7% of the total global consumption.

Type Analysis

Sebacic Acid Held the Largest Share in the Castor Oil & Derivatives Market.

The castor oil & derivatives market is segmented based on types into sebacic acid, 12-hydroxy stearic acid, ricinoleic acid, hydrogenated castor oil, undecylenic acid, dehydrated castor oil, and others. The sebacic acid dominated the castor oil & derivatives market, comprising around 38.7% of the market share, as it functions as a versatile bifunctional intermediate (C10 dicarboxylic acid) with broad compatibility across polymer and chemical systems. Its two carboxyl groups enable efficient polymerization into polyamides, polyesters, and plasticizers, supporting applications in engineering plastics, lubricants, and coatings.

In contrast, ricinoleic acid and 12‑Hydroxystearic acid are primarily monofunctional or structurally constrained, limiting their role to niche uses such as surfactants or greases. Hydrogenated castor oil is mainly a wax/structuring agent, while undecylenic acid and dehydrated castor oil serve narrower roles in antifungal agents or coatings.

Additionally, sebacic acid offers thermal stability, low toxicity, and consistent reactivity, making it suitable for large-scale industrial synthesis. Its ability to serve as a building block across multiple value chains, rather than a formulation additive, underpins its wider adoption.

Application Analysis

Castor Oil & Derivatives is Mostly Utilized for Plastics and Resins.

Based on the applications of castor oil & derivatives, the market is divided into lubricants, surface coatings, biodiesel, cosmetics and pharmaceuticals, plastics and resins, and others. The plastics and resins dominated the castor oil & derivatives market, with a market share of 26.9%, as their chemical structure enables scalable conversion into polymer intermediates, creating broader industrial utility than other applications. The high ricinoleic acid content allows efficient transformation into bifunctional monomers such as sebacic acid and undecylenic acid, which are directly used in polyamides, polyesters, and plasticizers. These materials are embedded in durable goods, ensuring large-volume, repeat demand.

By comparison, lubricants and coatings use castor derivatives mainly as performance additives, limiting volumetric uptake. Biodiesel applications are constrained as castor oil’s high viscosity and poor cold-flow properties require additional processing. In cosmetics and pharmaceuticals, derivatives such as ricinoleic acid and hydrogenated castor oil serve specialized, lower-dose functions. Consequently, plastics and resins dominate due to feedstock-to-polymer integration, higher material intensity, and broader end-use penetration, rather than niche or formulation-limited consumption patterns.

Key Market Segments

By Type

- Sebacic Acid

- 12-Hydroxy Stearic Acid

- Ricinoleic Acid

- Hydrogenated Castor Oil

- Undecylenic Acid

- Dehydrated Castor Oil

- Others

By Application

- Lubricants

- Surface Coatings

- Biodiesel

- Cosmetics and Pharmaceuticals

- Plastics and Resins

- Others

Drivers

Sustainability and Bio-based Demand Drives the Castor Oil & Derivatives Market.

Sustainability considerations and bio-based substitution are structurally reinforcing demand for castor oil and its derivatives. Castor oil is a non-edible, renewable feedstock with high ricinoleic acid content, enabling its use as a substitute for petroleum inputs in specialty chemicals. The lifecycle assessments show that cultivation practices materially affect emissions, with certain production pathways achieving EUR3.75 economic output per kg CO₂-eq, indicating measurable environmental-economic trade-offs in bio-based systems.

Castor-derived polymers, such as polyurethanes and adhesives, are documented as renewable, biodegradable, and lower-toxicity alternatives to petrochemicals, with comparable mechanical performance across coatings, construction, and biomedical uses. Similarly, bio-based inputs are increasingly adopted in coatings, lubricants, and personal care to replace fossil-derived feedstocks, reflecting a broader shift toward circular and low-carbon material systems.

The sustainability attributes, such as renewability, biodegradability, and process-level emissions differentials, constitute a quantifiable and application-linked demand driver for the castor oil derivatives value chain.

Restraints

Supply Concentration and Safety Concerns Might Hamper the Demand for Castor Oil & Derivatives.

Supply concentration and inherent safety risks constitute structural constraints in the castor oil and derivatives market. Production is geographically concentrated, as global output is dominated by a few countries, with India alone producing about 1.6 million tons, compared with some thousand tons in Mozambique, China, and Brazil, indicating high supply dependence on a narrow agro-climatic base.

Agronomic characteristics further constrain scalable supply. Castor plants exhibit non-synchronous seed ripening, necessitating largely manual harvesting and increasing labor intensity, while seed shattering leads to measurable yield losses. These factors reduce mechanization potential and heighten vulnerability to climatic and labor disruptions.

Furthermore, safety concerns originate from ricin, a highly toxic protein present in castor seeds, classified as a hazardous toxin with severe effects via ingestion, inhalation, or injection. Even low-dose exposure can be lethal, necessitating strict handling and processing controls across cultivation and extraction stages. Although refined oil is largely free of ricin, the toxicity of upstream biomass, such as seed cake, imposes compliance, detoxification, and waste-management requirements, adding operational complexity and limiting by-product utilization without treatment.

Opportunity

Rapid Growth in Biopolymers & Plastics Industries Create Opportunities in the Market.

Rapid expansion in biopolymers and engineering plastics is creating application-linked opportunities for castor oil derivatives, particularly in high-performance polyamides. Castor oil is a unique commercial source of long-chain monomers required for bio-based nylons such as polyamide 11 (PA11), 6.10, and 10.10, which are not readily obtainable from other vegetable oils.

PA11 is 100% bio-based, with its carbon content entirely derived from renewable castor feedstock, enabling full substitution of fossil-derived inputs in specific polymer classes. Similarly, it can deliver around 40-50% lower CO₂ emissions versus petroleum-based alternatives, while maintaining performance characteristics such as chemical resistance and thermal stability.

Furthermore, its adoption is observable across multiple end uses, such as automotive fuel lines, wire coatings, 3D printing powders, and consumer goods, due to low density, −40°C to +130°C operating range, and durability. Additionally, certain grades, such as PA 6.10, incorporate about 60% renewable content, supporting incremental decarbonization pathways in engineering plastics. The scaling of bio-based plastics, driven by material performance parity and measurable emissions advantages, directly expands demand for castor-derived chemical intermediates.

Trends

Adoption in Personal Care and Cosmetic Products.

Adoption of castor oil in personal care and cosmetics reflects a material shift toward plant-based functional ingredients with defined safety profiles and multifunctionality. Castor oil and its derivatives are widely used as skin-conditioning agents, emulsion stabilizers, and surfactants, indicating broad formulation utility across creams, lip products, and hair care.

In addition, safety validation underpins this trend. The Cosmetic Ingredient Review Expert Panel has assessed multiple castor-derived ingredients as safe for use in cosmetics at specified concentrations, including PEG derivatives used at up to 50-100% concentration ranges without dermal or ocular irritation in evaluated cases.

Functionally, high ricinoleic acid content enables measurable performance. It acts as a humectant that reduces moisture loss, supporting its inclusion in moisturizers, lip balms, and cleansing formulations. Its application breadth is evident across product categories, such as skin hydration, anti-inflammatory formulations, and hair conditioning, while documented adverse effects remain limited to localized allergic reactions in sensitive users, necessitating patch testing. The regulatory clearance, concentration flexibility, and multifunctional performance collectively support increasing incorporation of castor-derived inputs in personal care formulations.

Geopolitical Impact Analysis

Geopolitical Tensions Are Impacting the Castor Oil & Derivatives Due to Extreme Geographical Concentration.

The geopolitical tensions affect the castor oil and derivatives market primarily through trade concentration, tariff exposure, and supply-chain sensitivity, rather than direct conflict-zone production disruptions. For instance, the supply dependence amplifies geopolitical risk transmission. India accounts for majority of global castor oil exports and its production, making downstream industries structurally reliant on a single geography. Any disruption to Indian agricultural output, logistics, or export policy has system-wide implications.

In addition, trade policy shifts directly affect market access. For instance, prior tariff tensions in the United States involved duties of up to 50% on castor oil derivatives, before bilateral adjustments reduced these barriers. Notably, India supplies most of U.S. demand, indicating high bilateral exposure. Such policy volatility alters procurement costs and sourcing strategies.

Similarly, demand concentration introduces geopolitical sensitivity. The United States, China, and Malaysia together account for majority of global imports, creating dependency on a limited set of industrial economies. Trade frictions or strategic stockpiling by these countries can shift availability and pricing.

The concentrated production, bilateral trade dependencies, and policy-driven frictions transmit geopolitical shocks into pricing, availability, and procurement stability across the castor oil derivatives value chain.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Castor Oil & Derivatives Market.

In 2025, the Asia Pacific dominated the global castor oil & derivatives market holding about 43.7% of the total global consumption. Asia Pacific constitutes the largest and most structurally dominant region in the castor oil and derivatives market due to extreme production concentration, agro-climatic suitability, and integrated downstream consumption.

- According to a report by the Solvent Extractors Association (SEA), castor seed production in India has increased by 11%, reaching 17.6 lakh tons for the 2025-26 period.

Production is heavily regionalized. Asia accounts for majority of global castor seed output, reflecting climatic advantages in tropical and semi-arid zones. Within the region, India is the pivotal supplier meeting over 90% of global castor oil demand. This supply dominance is reinforced by geographic clustering of cultivation across countries such as Myanmar, Thailand, Vietnam, and China, supporting regional raw material availability and processing integration.

Moreover, Asia Pacific further exhibits strong industrial absorption. Castor oil supports many applications, including polymers, lubricants, cosmetics, and pharmaceuticals, many of which are concentrated in regional manufacturing ecosystems. The region’s dominance is empirically anchored in production scale, geographic concentration, and vertically linked industrial demand, rather than purely trade or pricing dynamics.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of castor oil and derivatives focus on feedstock integration, product specialization, and regulatory alignment to strengthen competitiveness. Backward integration into contract farming and seed development improves yield stability and traceability, particularly in regions such as India where supply is concentrated. Additionally, firms invest in process optimization and derivative diversification to move toward higher-value, application-specific chemicals used in polymers, lubricants, and personal care.

Sustainability certification and compliance with frameworks such as REACH are prioritized to secure access to regulated markets. Additionally, manufacturers emphasize R&D in bio-based materials, including performance-enhanced polyamides and coatings, to align with low-carbon material demand. Strategic collaborations with downstream users enable customized formulations, while investments in supply-chain resilience and export logistics mitigate concentration risks and improve delivery reliability.

The following are some of the major players in the industry

- Jayant Agro-Organics Ltd.

- Thai Castor Oil Industries Co., Ltd.

- NK Proteins Pvt. Ltd.

- Adani Wilmar Ltd.

- Gokul Agri International Ltd.

- Hokoku Corporation

- Alberdingk Boley GmbH

- ITOH Oil Chemicals Co., Ltd.

- Kanak Castor Products Pvt. Ltd.

- Arvalli Castor Derivatives Pvt. Ltd.

- Italmatch Chemicals

- Arkema

- Other Key Players

Key Development

- In July 2025, Arkema announced the creation of the Castor Farmer Education Fund (CFEF) in partnership with Solidaridad and TT Foundation Advisors to promote sustainable farming techniques in India.

- In February 2026, Jayant Agro-Organics announced Project Pragati’s year 9 milestones, achieving 32% higher yields and 30% water savings in sustainable castor farming.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 1.4 Bn |

| Forecast Revenue (2035) | US$ 2.5 Bn |

| CAGR (2026-2035) | 6.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Sebacic Acid, 12-Hydroxy Stearic Acid, Ricinoleic Acid, Hydrogenated Castor Oil, Undecylenic Acid, Dehydrated Castor Oil, and Others), By Application (Lubricants, Surface Coatings, Biodiesel, Cosmetics and Pharmaceuticals, Plastics and Resins, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Jayant Agro-Organics Ltd., Thai Castor Oil Industries Co., Ltd., NK Proteins Pvt. Ltd., Adani Wilmar Ltd., Gokul Agri International Ltd., Hokoku Corporation, Alberdingk Boley GmbH, ITOH Oil Chemicals Co., Ltd., Kanak Castor Products Pvt. Ltd., Arvalli Castor Derivatives Pvt. Ltd., Italmatch Chemicals, Arkema, and Other Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |