Quick Navigation

Report Overview

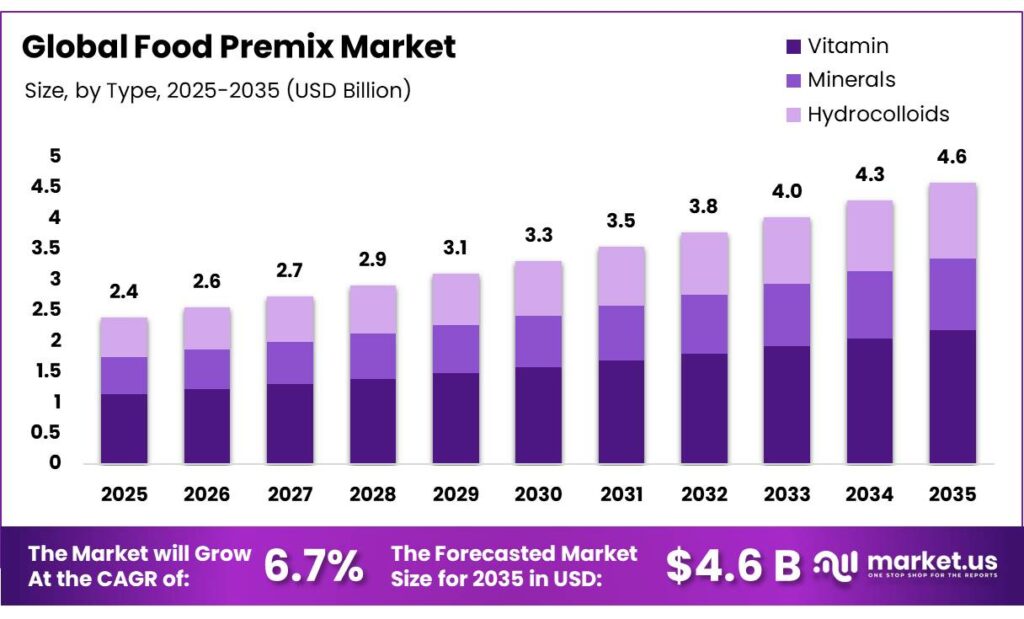

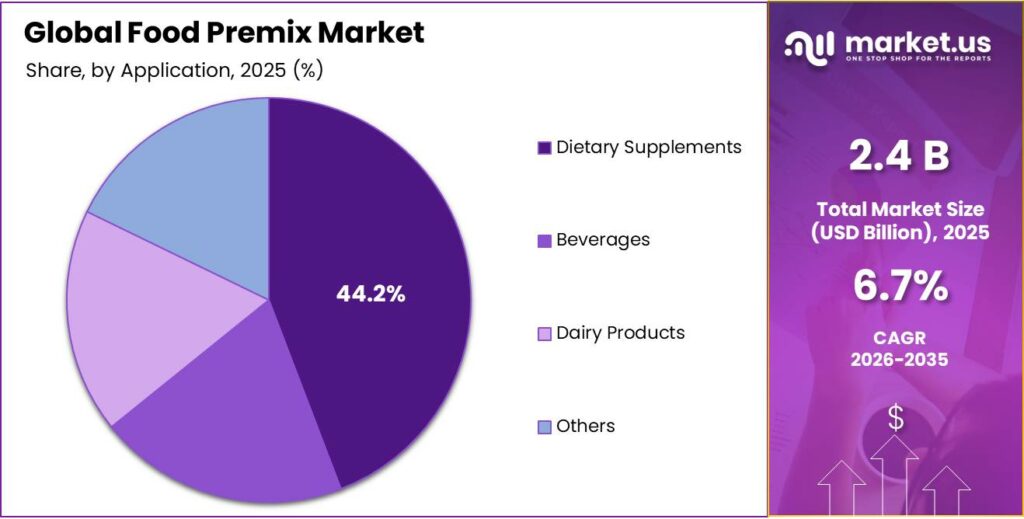

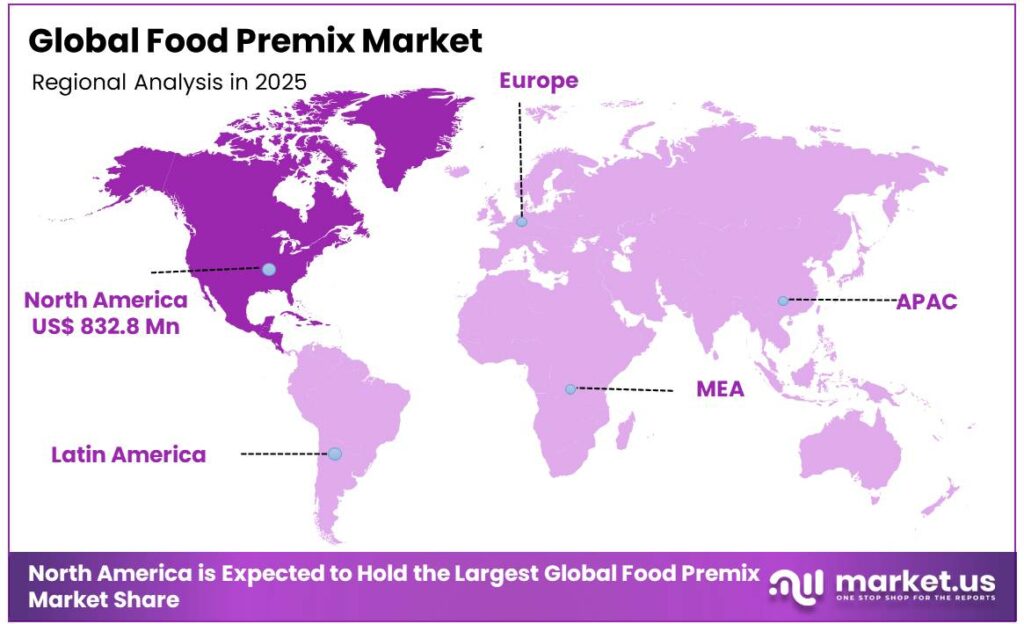

The Global Food Premix Market size is expected to be worth around USD 4.6 Billion by 2035, from USD 2.4 Billion in 2025, growing at a CAGR of 6.7% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 44.6% share, holding USD 378.2 Million revenue.

The food premix market is shaped by a combination of structural demand drivers, regulatory mandates, and evolving consumer preferences. Premixes, which are blends of vitamins, minerals, and functional ingredients, are widely used to address global micronutrient deficiencies, particularly in staple foods and dietary supplements, where fortified intake constitutes a significant source of nutrients such as vitamin D, vitamin A, and iron.

North America is a leading market, underpinned by mandatory fortification policies, widespread processed food consumption, and industrial-scale blending infrastructure. Powdered premixes dominate due to stability, ease of handling, and compatibility with dry-mix manufacturing, while vitamins are preferred over minerals or hydrocolloids because of lower sensory impact and regulatory prioritization.

Strategic focus on customized formulations, clean-label compliance, and supply-chain robustness further supports adoption, while challenges such as consumer skepticism and geopolitical input disruptions shape operational and product-level decisions. The market reflects a confluence of nutritional necessity, technological adaptability, and regulatory enforcement.

Key Takeaways

- The global food premix market was valued at USD 2.4 billion in 2025.

- The global food premix market is projected to grow at a CAGR of 6.7% and is estimated to reach USD 4.6 billion by 2035.

- Based on type, vitamins dominated the food premix market, constituting 47.8% of the total market share.

- Based on the form, powdered food premix dominated the market, with a substantial market share of around 74.9%.

- Among the applications, dietary supplements held a major share in the food premix market, 44.2% of the market share.

- In 2025, North America was the most dominant region in the food premix market, accounting for 34.7% of the total global consumption.

Type Analysis

Vitamins are a Prominent Segment in the Food Premix Market.

The food premix market is segmented based on type into vitamins, minerals, and hydrocolloids. The vitamin led the food premix market, comprising 47.8% of the market share, due to stronger regulatory anchoring, broader deficiency prevalence, and easier formulation integration.

The health frameworks led by the World Health Organization emphasize vitamins such as A, D, and folic acid in mass fortification programs, with mandatory or widely adopted enrichment of staples such as flour and milk. Additionally, deficiency burdens are more pervasive, as vitamin A and D insufficiencies affect large population segments, driving routine inclusion across everyday foods.

Similarly, vitamins typically require lower inclusion levels, have less impact on taste and texture, and are easier to standardize in blends. In contrast, minerals can cause metallic taste, color changes, or reduced bioavailability, complicating application. Hydrocolloids serve primarily functional rather than nutritional roles, limiting their use to specific product categories.

Form Analysis

Powdered Food Premix Dominated the Market.

On the basis of the form, the food premix market is segmented into powder and liquid. The powdered food premix dominated the market, comprising 74.9% of the market share, due to advantages in stability, handling, and process compatibility. The powders exhibit longer shelf life as several micronutrients are less prone to degradation in low-moisture environments.

Reduced water activity further minimizes microbial growth, simplifying storage and transport requirements without reliance on preservatives. Additionally, powdered premixes integrate efficiently into dry-mix manufacturing systems, enabling precise dosing and uniform dispersion at scale. They are lighter and less bulky, lowering logistics complexity compared to liquids that require sealed containers and stricter temperature control. By contrast, liquid premixes face shorter shelf life, higher contamination risk, and formulation constraints. These factors collectively make powdered premixes more versatile across diverse food processing environments.

Application Analysis

Food Premixes Are Mostly Utilized in Dietary Supplements.

Based on the applications, the food premix market is divided into dietary supplements, beverages, dairy products, and others. The dietary supplements dominated the food premix market, with a notable market share of 44.2%, due to regulatory flexibility, higher nutrient dosing requirements, and fewer formulation constraints. Dietary supplements operate under distinct frameworks, which permit higher concentrations of vitamins and minerals than conventional foods.

In contrast, beverages and dairy products are subject to stricter compositional and sensory constraints, limiting fortification levels. The supplements are less sensitive to taste, color, and texture, whereas beverages and dairy must maintain sensory quality. Additionally, supplements are designed specifically for nutrient delivery rather than basic nutrition, making premixes central to product design, unlike broader food categories where fortification is optional or secondary.

Key Market Segments

By Type

- Vitamin

- Minerals

- Hydrocolloids

By Form

- Powder

- Liquid

By Application

- Dietary Supplements

- Beverages

- Dairy Products

- Others

Drivers

Escalating Global Demand for Fortified and Functional Foods Drives the Food Premix Market.

Escalating global demand for fortified and functional foods is structurally anchored in persistent micronutrient deficiencies and policy-driven nutrition interventions, directly stimulating demand for food premixes, vitamin-mineral blends used in fortification.

More than 2 billion individuals globally suffer from micronutrient deficiencies, including one in two pre-school-aged children and two in three women of reproductive age. This scale of deficiency has led to widespread adoption of fortification, as at least 60 countries have implemented national fortification programmes, institutionalizing recurrent demand for standardized premix inputs. The World Food Programme distributed 1.48 million metric tons of fortified foods in 2021, equivalent to over 3 billion rations. Such large-scale procurement requires consistent micronutrient blending, a core function of premix suppliers.

Regulatory frameworks further embed demand, as governments mandate the addition of micronutrients to staple foods such as cereals, salt, and oils as part of mass fortification strategies. Similarly, fortified foods demonstrate measurable efficacy, such as reduced anaemia prevalence and improved micronutrient biomarkers, reinforcing sustained adoption. High deficiency burdens, mandated fortification programs, and functional food uptake converge to create a stable, volume-driven demand base for food premixes.

Restraints

Consumer Skepticism Might Pose a Challenge to the Food Premix Market.

Consumer skepticism toward fortified and functional foods constitutes a structural demand constraint for the food premix market, rooted in risk perception, information asymmetry, and sensory trade-offs. According to the 2025 IFIC Food & Health Survey, overall confidence in the safety of the U.S. food supply fell for the second consecutive year to 62%, with those reporting they are very confident dropping to 11%, near the historical low of 10%.

Similarly, product-level data indicate that consumers reject the view that additives are harmless, reflecting entrenched caution toward chemically perceived ingredients. This skepticism extends to fortified foods, where acceptability is conditional. The consumers frequently detect off-tastes in fortified products and prioritize sensory attributes over health benefits, directly reducing purchase intent. Furthermore, the majority of consumers report insufficient understanding of food additives, linking low knowledge to adverse safety perceptions.

Structurally, fortified foods function as credence goods, meaning consumers cannot verify nutrient claims independently and must rely on labeling, heightening trust sensitivity. The skepticism is driven by perceived health risks, sensory compromises, and limited transparency, factors that constrain the adoption of premix-enabled products despite demonstrated nutritional benefits.

Opportunities

Infant & Pediatric Nutrition Creates Opportunities in the Food Premix Market.

The infant and pediatric nutrition segment represents a critical opportunity for the food premix market, driven by the physiological necessity for precise micronutrient delivery during periods of rapid developmental growth. In 2024, 150.2 million children under five were stunted, 42.8 million wasted, and 35.5 million overweight, indicating nutrition challenges. Undernutrition alone is linked to 45% of deaths among children under five, underscoring the clinical urgency of nutrient-dense interventions.

Infants are particularly vulnerable due to elevated micronutrient requirements during rapid growth phases. Consequently, policy responses directly embed premix demand. The World Health Organization recommends point-of-use fortification with micronutrient powders for children aged 6-23 months in populations with more than 20% anaemia prevalence, formalizing the use of vitamin-mineral premixes in complementary feeding. Additionally, fewer than 25% of infants globally receive adequate dietary diversity, reinforcing reliance on fortified complementary foods.

The premixes enable standardized delivery of iron, vitamin A, and zinc in formats such as powders and ready-to-use therapeutic foods, which have demonstrated reductions in anaemia risk in young children. The convergence of high deficiency prevalence, clinical validation, and guideline-driven fortification positions pediatric nutrition as a sustained demand channel for food premixes.

Trends

Shift Towards Clean Label and Natural Ingredients.

The shift toward clean label and natural ingredients is a structurally significant trend shaping formulation strategies in the food premix market, driven by measurable changes in consumer preferences and risk perceptions. Clean label attributes are operationally defined as free from artificial additives, preservatives, and synthetic ingredients, emphasizing simplicity and recognizability.

Several surveys indicate strong behavioral alignment with ingredient transparency. In the U.S., 64% of consumers report trying to choose foods with clean ingredients, while 63% state ingredient lists influence purchasing decisions. Globally, preference intensity is reinforced by comprehension, as consumers are more likely to purchase products with familiar, understandable ingredients.

The consumers systematically prefer additive-free or natural labels and associate them with higher safety and nutritional value, despite inconsistent willingness-to-pay outcomes. This is reinforced by a documented negativity bias, where additives, irrespective of origin, are actively avoided. For premix suppliers, this trend translates into demand for naturally derived vitamins, minerals, and carriers, alongside reformulation pressures to eliminate synthetic excipients while maintaining stability and bioavailability.

Geopolitical Impact Analysis

Increased Prices of Food Products Market Amid Geopolitical Tensions.

The geopolitical tensions are exerting systemic, multi-channel pressures on the food premix market by disrupting upstream inputs, trade flows, and cost structures. In March 2026, a disruption in the Strait of Hormuz reduced tanker traffic by over 90% within days, affecting flows that normally carry about 35% of global crude oil, one-fifth of LNG, and up to 30% of internationally traded fertilizers. Fertilizers are critical for micronutrient-rich crop production and for fermentation substrates used in vitamin synthesis. These supply shocks might propagate into premix input availability.

The war in Ukraine triggered high and volatile energy, food, and fertilizer prices, alongside export constraints and reduced fertilizer production due to gas shortages. Concurrently, governments report that geopolitical tensions have caused observable disruptions to agriculture and food supply chains and trade flows.

The global food trade is increasingly exposed to chokepoint risks, where concentrated transit routes amplify cascading failures across food and nutrient supply chains. For premix markets, which depend on globally sourced vitamins, minerals, and carriers, these disruptions translate into input volatility, logistical uncertainty, and constrained production continuity.

Regional Analysis

North America Held the Largest Share of the Global Food Premix Market.

In 2025, North America dominated the global food premix market, holding about 34.7% of the total global consumption, underpinned by entrenched fortification practices, regulatory standardization, and high penetration of fortified foods in daily diets.

The regulatory frameworks in the United States and Canada institutionalize micronutrient addition across staple categories. For instance, Canadian regulations mandate or permit fortification across multiple food groups, including mandatory vitamin D addition to milk and iodine in salt, with defined nutrient thresholds under federal law. Similarly, U.S. policy embeds enrichment standards for staple foods such as flour, ensuring consistent micronutrient delivery through industrial processing.

Additionally, industrial capacity supports high-volume premix utilization, with large-scale milling and processed food systems enabling standardized nutrient blending across product lines. Collectively, regulatory enforcement, high dietary reliance on fortified foods, and advanced processing infrastructure sustain North America’s dominant demand base for food premixes.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of food premixes focus on integrated product, regulatory, and supply-chain strategies to strengthen competitive positioning. A primary lever is customized formulation, where premixes are tailored to specific applications and aligned with national fortification standards set by agencies such as the World Health Organization and the Food and Agriculture Organization. Firms further prioritize clean-label reformulation, shifting toward naturally derived vitamins, minerals, and carriers to meet consumer scrutiny of additives.

Similarly, quality assurance and traceability systems are expanded to comply with stringent food safety frameworks, ensuring batch consistency and regulatory acceptance across jurisdictions. In parallel, companies invest in application-specific R&D, improving nutrient stability, bioavailability, and sensory neutrality in fortified products.

The Major Players in The Industry

- Archer Daniels Midland Company

- DSM

- Cargill Incorporated

- BASF SE

- Corbion N.V.

- Glanbia plc

- Associated British Foods plc

- Barentz International

- Prinova Group LLC

- Other Key Players

Key Development

- In March 2026, ADM, one of the world’s largest agribusiness companies, opened a facility in Apucarana, Paraná, with production capacity 40% higher than its previous facility in the city to produce up to 40,000 tonnes of premix, a blend of minerals, amino acids, vitamins, and additives.

- In March 2026, DSM-Firmenich announced the completion of a US$10 million modernization program on its Schenectady premix facility in the United States, transforming the site into a flagship premix hub for the Americas.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$2.4 Bn |

| Forecast Revenue (2035) | US$4.6 Bn |

| CAGR (2026-2035) | 6.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Vitamin, Minerals, and Hydrocolloids), By Form (Powder and Liquid), By Application (Dietary Supplements, Beverages, Dairy Products, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Archer Daniels Midland Company, DSM, Cargill Incorporated, BASF SE, Corbion N.V., Glanbia plc, Associated British Foods plc (AB Agri Ltd), Barentz International, Prinova Group LLC, and Other Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |