Quick Navigation

Report Overview

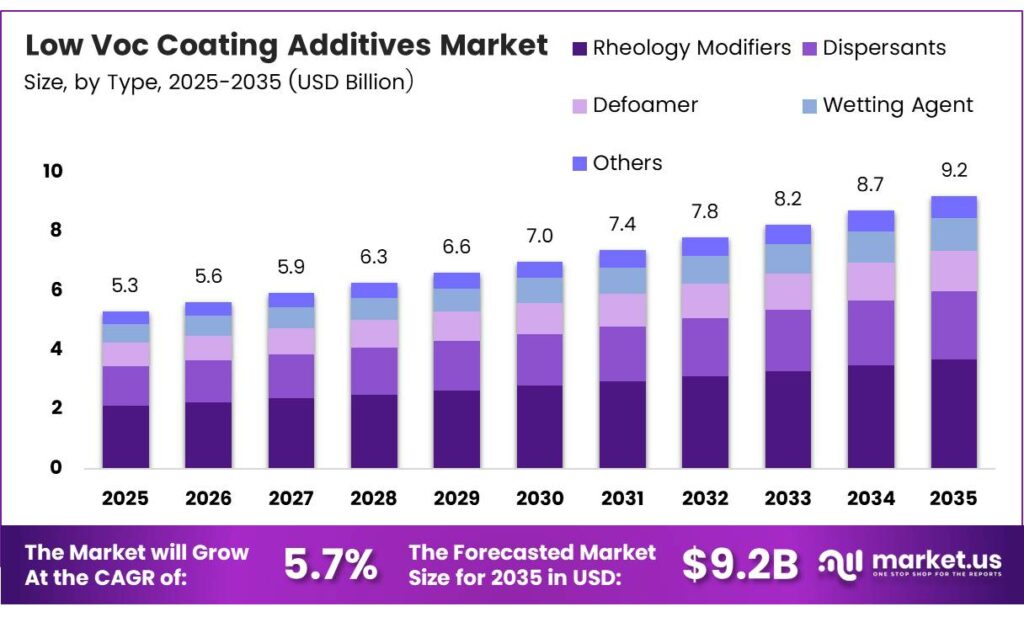

The Global Low VOC Coating Additives Market size is expected to be worth around USD 9.2 billion by 2035 from USD 5.3 billion in 2025, growing at a CAGR of 5.7% during the forecast period 2026 to 2035.

Low VOC coating additives are specialty chemicals added to paint and coating formulations to reduce volatile organic compound emissions. They include rheology modifiers, dispersants, defoamers, and wetting agents. These additives help manufacturers meet emission standards without sacrificing coating performance across architectural, automotive, and industrial applications.

The automotive sector’s shift toward eco-friendly finishing systems is another structural driver. OEMs and Tier-1 suppliers are reformulating coating lines to reduce VOC output per vehicle unit. This creates a captive buyer base for high-performance, low VOC additives that meet both emission and durability thresholds required in automotive coatings.

Bio-acrylic interior paint polymer, reporting approximately 27% bio-based carbon content, signals that bio-based additive chemistry is now commercially viable — not just experimental. Advancing low-VOC coating technologies through high-performance, compliant additives and binders. Bio-based acrylic emulsions can meet strict VOC limits while maintaining formulation quality, signaling growing commercial viability for renewable polymer platforms in architectural coatings.

Key Takeaways

- The Global Low VOC Coating Additives Market is valued at USD 5.3 billion in 2025 and is forecast to reach USD 9.2 billion by 2035 at a CAGR of 5.7% during the forecast period 2026 to 2035.

- Rheology Modifiers lead the segment with a 31.5% share in 2025.

- Waterborne technology dominates with a 47.2% share, reflecting the industry’s primary reformulation pathway.

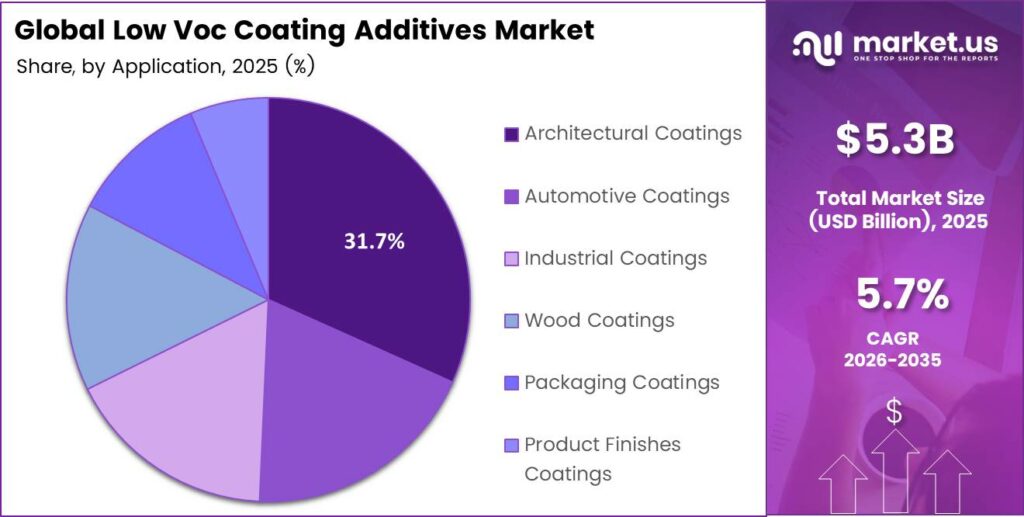

- Architectural Coatings holds the largest share at 31.7% in 2025.

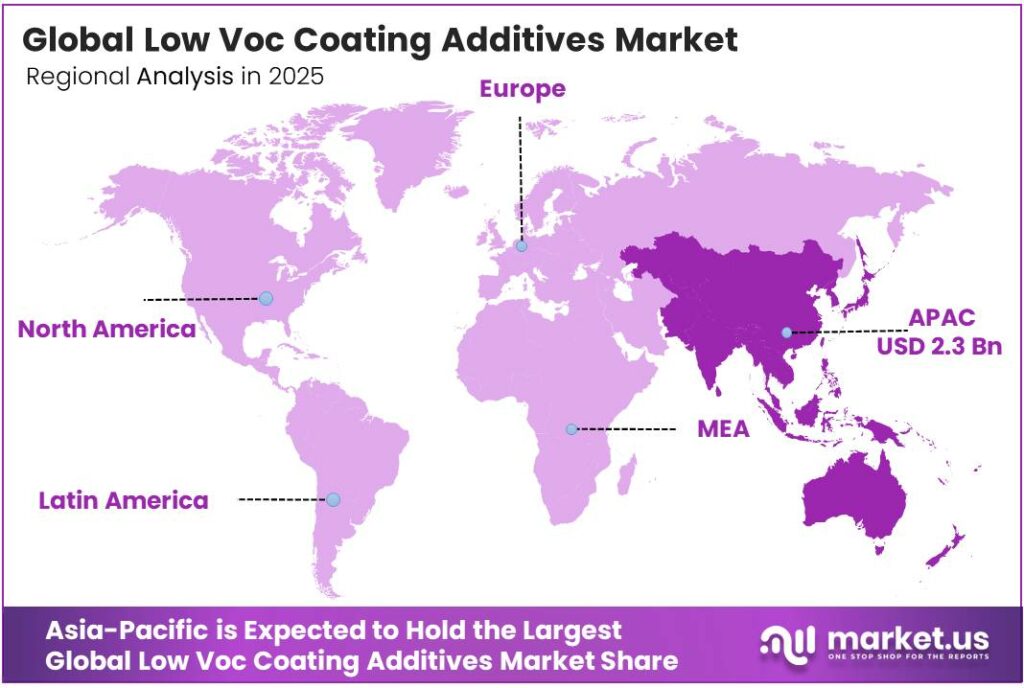

- Asia-Pacific is the leading region with a 44.8% share, valued at USD 2.3 billion.

Product Analysis

Rheology Modifiers dominate with 31.5% due to critical viscosity control in waterborne systems.

In 2025, Rheology Modifiers held a dominant market position in the By Type segment of the Low VOC Coating Additives Market, with a 31.5% share. Their dominance reflects a technical necessity — waterborne formulations require precise flow and leveling control that only high-performance rheology modifiers deliver. As waterborne adoption expands, demand for this additive type scales proportionally.

Dispersants serve as the functional backbone for pigment stability in low VOC systems. Without effective dispersants, pigment agglomeration compromises color strength and finish quality. Formulators switching away from solvent-based carriers rely on dispersants to maintain pigment distribution in water-based media — making this sub-segment structurally tied to waterborne technology growth.

Technology Analysis

Waterborne technology dominates with 47.2% due to regulatory compliance and broad reformulation adoption.

In 2025, Waterborne technology held a dominant market position in the By Technology segment of the Low VOC Coating Additives Market, with a 47.2% share. This reflects a decade of deliberate reformulation by coating manufacturers under pressure from VOC emission regulations. Waterborne systems now serve as the primary platform for low VOC compliance — and the additive ecosystem built around them is the market’s commercial core.

Powder-based coatings eliminate solvent, making them a zero-VOC application method. Their share reflects strong adoption in industrial and automotive finishing lines where oven-cure infrastructure exists. However, their requirement for heat-cure equipment limits penetration in residential architectural applications — creating a market ceiling that waterborne systems do not face.

Application Analysis

Architectural Coatings dominate with 31.7% due to green building mandates and residential VOC regulations.

In 2025, Architectural Coatings held a dominant market position in the By Application segment of the Low VOC Coating Additives Market, with a 31.7% share. Green building certification programs — including LEED, WELL, and national equivalents — mandate low-emission interior coatings as specification requirements.

Automotive Coatings represent a high-performance segment where low VOC compliance intersects with strict durability requirements. OEMs demand coatings that meet both environmental mandates and functional specifications — for hardness, adhesion, and chip resistance.

Industrial Coatings serve protective applications across infrastructure, machinery, and equipment. Industrial users operate under permitting systems that cap facility-level VOC emissions — not just product-level limits. Consequently, additive procurement decisions are driven by total VOC load management, not simply product specification.

Key Market Segments

By Type

- Rheology Modifiers

- Dispersants

- Defoamer

- Wetting Agent

- Others

By Technology

- Water Borne

- Powder Based

- High Solids

- Radiation Cure

By Application

- Architectural Coatings

- Automotive Coatings

- Industrial Coatings

- Wood Coatings

- Packaging Coatings

- Product Finishes Coatings

Emerging Trends

Nanotechnology and Multifunctional Additive Design Redefine Low VOC Performance Standards

Nanotechnology integration is reshaping additive performance in low-VOC coating systems. Nano-scale particles improve dispersion efficiency, scratch resistance, and barrier properties without increasing solvent content. This allows formulators to meet both emission limits and performance benchmarks — a combination that previously required trade-offs.

Multifunctional additive development is compressing formulation complexity for coating manufacturers. Instead of sourcing multiple single-function additives, manufacturers can deploy one additive that delivers VOC compliance alongside durability and aesthetic performance. Point-of-sale colorants must add no more than 50 g VOC per liter above the base product’s allowed level — a threshold that multifunctional additive design helps manufacturers meet without reformulating the entire product system.

Strategic collaborations among additive producers are accelerating this innovation cycle. Arkema’s ENCOR 2171 — with ultra-low VOC capability of 50 g/L for 1K/2K stoving systems — demonstrates how partnership-driven R&D produces commercially viable low VOC solutions for industrial coating lines. Formulators who align with suppliers investing in this next-generation chemistry position themselves ahead of the tightening compliance window.

Drivers

Tightening VOC Emission Regulations and Green Building Mandates Restructure Coating Additive Demand

Environmental regulations across major economies have moved from advisory to mandatory — with specific VOC thresholds embedded in building codes, industrial permits, and product certification schemes. This regulatory architecture removes discretion from procurement decisions. Coating manufacturers must reformulate, and additive suppliers who deliver compliance without performance loss gain structural pricing power in the supply chain.

Green building standards are reshaping specification behavior at the project level. Architects and developers now write low VOC performance into material specifications as baseline requirements — creating a demand signal that flows directly to additive formulators. Evonik’s Hybridur 870 clear coat reduced VOC content from 108 g/L to 36 g/L versus a standard formulation — a reduction that directly enables manufacturers to meet increasingly strict certification thresholds without losing functional performance.

Consumer awareness of indoor air quality is translating into purchasing behavior that rewards low-emission products. Retailers and commercial buyers now request third-party certification before listing coating products. This retail channel pressure compounds regulatory pressure — creating a dual compliance incentive that sustains additive demand even in market segments not yet covered by binding regulation.

Restraints

High Formulation Costs and Performance Limitations Constrain Low VOC Additive Adoption in Demanding Applications

Advanced low-VOC additive technologies carry significant production cost premiums over conventional solvent-based chemistries. Formulators in cost-sensitive segments — particularly in emerging markets without binding compliance mandates — cannot justify these premiums without regulatory incentives. This cost barrier slows voluntary adoption and concentrates low VOC additive use in regulated markets where compliance is non-negotiable.

Performance compatibility remains a genuine technical constraint in extreme industrial and environmental conditions. Low VOC additives engineered for standard architectural applications do not always perform equivalently when exposed to high humidity, temperature cycling, or chemical exposure in heavy industrial settings. Interior products must complete the full 14-day (336-hour) CDPH emissions testing period — a rigorous standard that many reformulated systems fail to meet without costly re-engineering of the additive package.

The performance gap between solvent-based and low VOC systems in demanding applications gives industrial buyers reason to delay transition. Until additive suppliers close this gap — through either chemistry advances or application-specific product development — segments like marine coatings and heavy-duty protective applications will remain partial adopters, limiting the total addressable market for low VOC additives in industrial end-use categories.

Growth Factors

Bio-Based Raw Materials and Waterborne Technology Innovation Open New Revenue Pathways

Bio-based raw materials are moving from concept to commercial formulation in low-VOC coating additive development. Suppliers sourcing renewable feedstocks reduce both carbon footprint and regulatory exposure — two factors increasingly weighted in enterprise procurement decisions. Dow’s EVOQUE emulsion technology delivers up to 20% TiO₂ savings in high-performance coatings, demonstrating that bio-informed additive innovation can simultaneously reduce material costs and environmental impact for downstream manufacturers.

Infrastructure expansion in developing economies creates a demand base that did not previously exist at this scale. Urbanization in South and Southeast Asia, Sub-Saharan Africa, and Latin America is generating construction volumes that require large quantities of architectural coatings — and increasingly, those coatings must meet evolving local VOC standards. This creates a new buyer pool for low VOC additives that is growing independently of the regulatory maturity seen in North America and Europe.

Technological advancement in waterborne and powder coating systems is broadening the performance envelope of low-VOC-compliant products. Additives that were once limited to light-duty architectural applications can now meet the technical specifications of automotive and industrial users. This performance convergence expands the addressable market for each additive category — transforming what were once niche compliance products into volume segments with cross-industry applicability.

Regional Analysis

Asia-Pacific Dominates the Low VOC Coating Additives Market with a Market Share of 44.8%, Valued at USD 2.3 Billion

Asia-Pacific commands 44.8% of the global market, valued at USD 2.3 billion. This position reflects the region’s dominant construction output, manufacturing scale, and accelerating regulatory convergence. China’s national emission standards and India’s growing green building sector are compelling coating manufacturers to source compliant additives at volume, creating the largest single regional demand base globally.

North America operates the most mature regulatory framework for VOC emissions, with California’s CARB standards setting benchmarks that influence national and international policy. This regulatory leadership drives early additive adoption and creates a stable, high-value demand base. The region’s concentration of automotive OEMs and commercial construction activity sustains premium additive consumption across multiple application segments.

Europe enforces comprehensive VOC directives through the EU Paints Directive and national transpositions, creating mandatory compliance demand across all coating categories. Germany and France anchor industrial coating consumption, while Scandinavian countries lead in architectural low-VOC adoption, driven by indoor air quality standards. This multi-country regulatory architecture creates a fragmented but large and structurally reliable demand base.

Latin America presents an infrastructure-led demand base where urbanization in Brazil and Mexico is generating construction volumes that require architectural coatings at scale. Voluntary low VOC adoption is limited without binding regulation, but export-oriented manufacturers in the region are adopting compliant formulations to access North American and European markets — creating indirect regulatory pull.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

BASF SE anchors its market position through an integrated additive portfolio spanning rheology, dispersancy, and surface control — covering the full formulation stack for low VOC coating systems. Its scale allows it to support large coating manufacturers with system-level solutions, not single-product supply. This breadth reduces customer switching and deepens supply chain entrenchment across architectural, automotive, and industrial coating segments.

Evonik AG differentiates through specialty chemistry and application-specific product engineering. Its Hybridur and AEROSIL product lines address precise formulation challenges in waterborne and low VOC systems — enabling customers to hit compliance thresholds without reformulating entire systems from scratch. This technical depth positions Evonik as a preferred innovation partner, not merely a commodity supplier, in high-performance, low VOC coating development.

Dow combines polymer science with sustainability chemistry to lead in bio-based and high-efficiency additive development. Its RHOPLEX and EVOQUE emulsion platforms serve architectural coating manufacturers targeting both VOC compliance and material efficiency simultaneously. This dual-value positioning — compliance plus cost savings — gives Dow a differentiated commercial argument that resonates with large industrial buyers managing both regulatory and margin pressure.

Eastman Chemical Company focuses on coalescent and specialty additive solutions that enable low VOC compliance in formulations that would otherwise require higher solvent content for film formation. Its coalescent technologies reduce the minimum film formation temperature of waterborne systems — solving a specific technical barrier that limits low VOC adoption in cold-climate architectural applications.

Key players

- BASF SE

- Evonik AG

- Dow

- Eastman Chemical Company

- Allnex

- Axalta Coating Systems

- AkzoNobel

- Elementis PLC

- Huntsman Corporation

- Seqens

Recent Developments

- In 2025, BASF highlighted ongoing innovation in surface modifiers and wetting agents used in coatings to improve performance while addressing formulation challenges like foam control and substrate wetting—critical for waterborne / low-VOC systems. BASF continues to emphasize multifunctional additives (wetting, leveling, slip) that allow formulators to reduce solvent load and simplify formulations, supporting low-VOC transitions.

- In 2025, Evonik AG is advancing its “Next Generation Solutions” strategy, which targets a growing share of revenue from sustainable products. The company’s sustainability reports indicate a strong push toward resource-efficient and low-emission additive systems, including dispersants and surface modifiers tailored for low-VOC formulations.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 5.3 Billion |

| Forecast Revenue (2035) | USD 9.2 Billion |

| CAGR (2026-2035) | 5.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Rheology Modifiers, Dispersants, Defoamer, Wetting Agent, Others), By Technology (Water Borne, Powder Based, High Solids, Radiation Cure), By Application (Architectural Coatings, Automotive Coatings, Industrial Coatings, Wood Coatings, Packaging Coatings, Product Finishes Coatings) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | BASF SE, Evonik AG, Dow, Eastman Chemical Company, Allnex, Axalta Coating Systems, AkzoNobel, Elementis PLC, Huntsman Corporation, Seqens |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |