Quick Navigation

- Report Overview

- Key Takeaways

- Color Type Analysis

- Product Type Analysis

- Resin Type Analysis

- Technology Analysis

- Coating Type Analysis

- Application Analysis

- Key Market Segments

- Emerging Trends

- Drivers

- Restraints

- Growth Factors

- Regional Analysis

- Key Regions and Countries

- Key Company Insights

- Recent Developments

- Report Scope

Report Overview

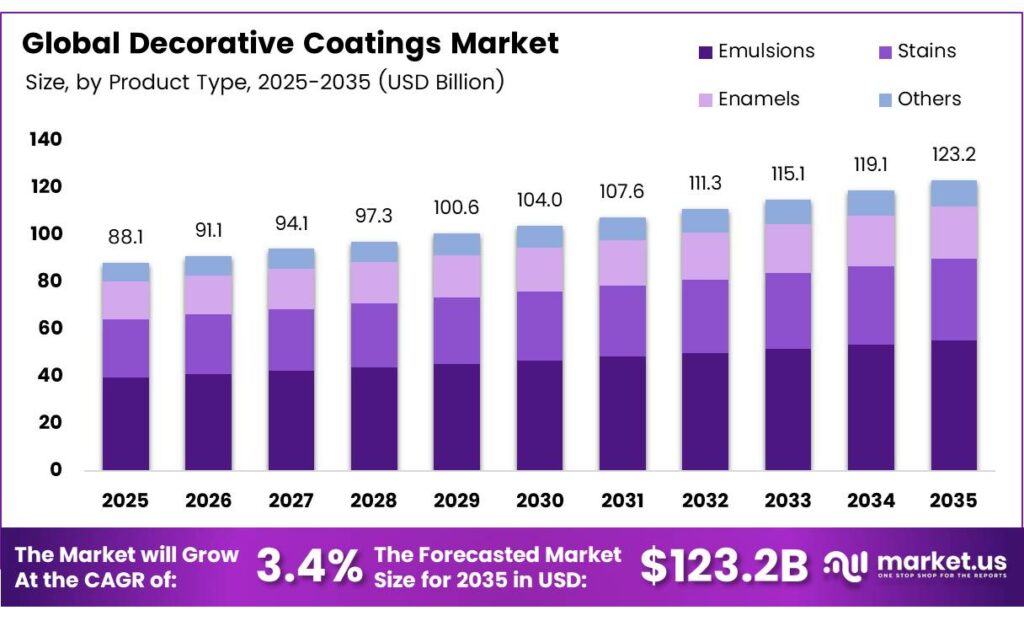

The Global Decorative Coatings Market size is expected to be worth around USD 123.2 billion by 2035 from USD 88.1 billion in 2025, growing at a CAGR of 3.4% during the forecast period 2026 to 2035.

Decorative coatings encompass a broad category of surface finishing products applied to walls, ceilings, wood surfaces, and structural elements for both aesthetic enhancement and protective performance. These products span emulsions, enamels, varnishes, stains, and wood coatings, serving residential, commercial, industrial, and infrastructure end-users across global markets.

Urban construction activity continues to shape product demand. Architects and developers in emerging economies specify decorative finishes earlier in the project lifecycle, shifting coatings from an afterthought to a structural design decision. This change in procurement behavior creates consistent volume commitments for manufacturers with broad product portfolios and reliable supply chains.

Functional coatings with anti-microbial, self-cleaning, and thermal management properties are opening new specification pathways beyond traditional aesthetics. Cool roof coatings reduced roof surface temperatures by 8.7°C to 34.2°C, representing a 13.2% to 53.6% reduction. This performance range demonstrates that functional decorative coatings now deliver measurable energy efficiency outcomes — a value proposition that appeals to green building certifiers and facility managers simultaneously.

Renovation and remodeling activities add a counter-cyclical layer of stability to this market. When new construction slows, homeowners redirect spending toward interior upgrades and exterior repaints. Consequently, manufacturers supplying both new build and repaint channels carry lower revenue volatility than those concentrated in a single end-use segment.

The performance gap within functional coatings is itself a strategic signal. The best-performing cool roof coating reduced surface temperature from 62.9°C to 34.3°C, a 45.5% reduction. This spread between top and baseline performers indicates that product differentiation on technical metrics — not just color or finish — will increasingly determine specification wins in commercial and infrastructure segments.

Key Takeaways

- The Global Decorative Coatings Market was valued at USD 88.1 billion in 2025 and is forecast to reach USD 123.2 billion by 2035 at a CAGR of 3.4% from 2026 to 2035.

- By Color Type, White dominates with a 58.2% share in 2025.

- By Product Type, Emulsions lead the segment with a 52.7% share.

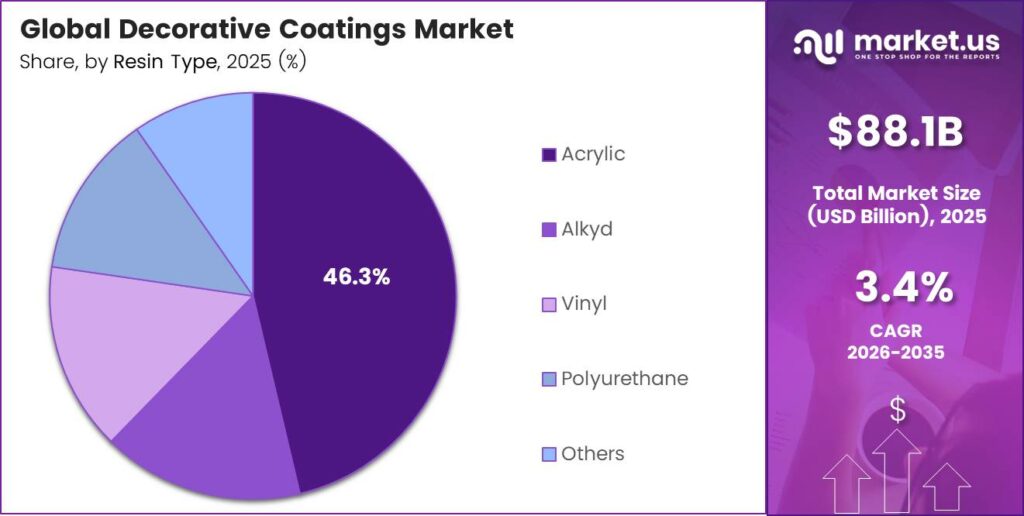

- By Resin Type, Acrylic holds the largest share at 46.3%.

- By Technology, Waterborne coatings account for 67.1% of the technology segment.

- By Coating Type, Interior coatings dominate with a 69.4% share.

- By Application, Residential end-use leads at 69.6%.

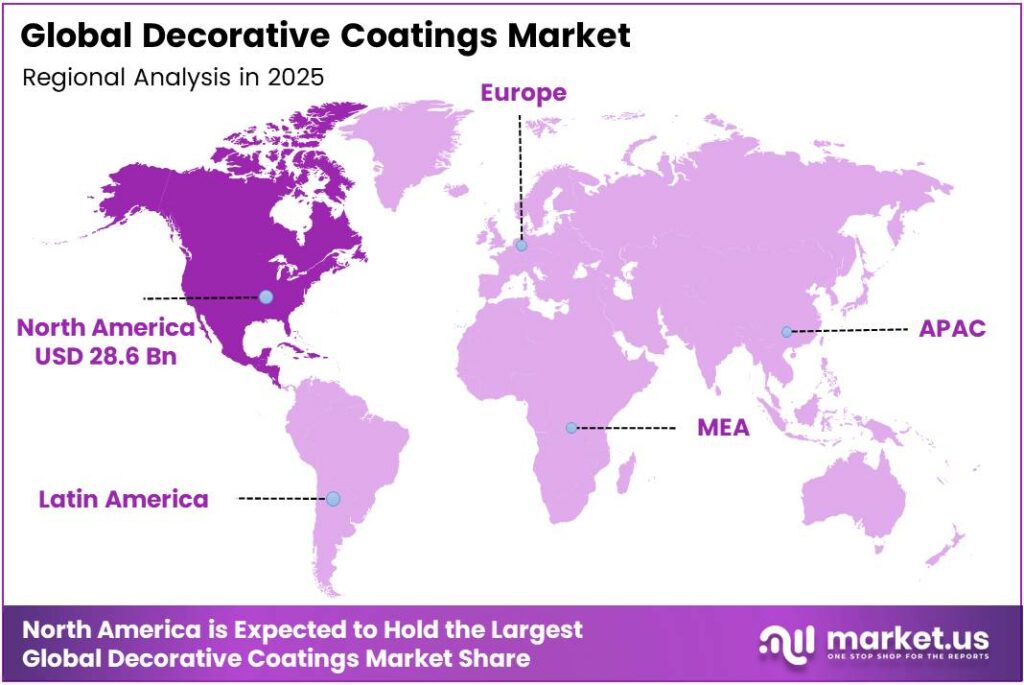

- North America holds the dominant regional share at 32.5%, valued at USD 28.6 billion.

Color Type Analysis

White dominates with 58.2% due to universal architectural and regulatory preference.

In 2025, White held a dominant market position in the By Color Type segment of the Decorative Coatings Market, with a 58.2% share. White coatings fulfill both aesthetic and functional roles — reflecting heat, meeting light reflectance requirements in commercial building codes, and serving as a base layer for decorative tinting systems. This dual utility makes white the default specification across residential, commercial, and institutional projects.

Others in the color type segment capture demand for specialty tints, accent finishes, and custom color-matching services. Tinted and colored decorative coatings carry higher margins per liter than standard white formats, making them commercially attractive for premium product lines. However, volume concentration in white limits the revenue contribution of specialty colors to niche renovation and interior design projects.

Product Type Analysis

Emulsions dominate with 52.7% due to water-based formulation advantages in residential interiors.

In 2025, Emulsions held a dominant market position in the By Product Type segment of the Decorative Coatings Market, with a 52.7% share. Emulsions deliver fast drying times, low odor profiles, and washable surfaces — properties that align directly with residential buyer preferences and professional contractor efficiency requirements. Their compatibility with waterborne technology reinforces their position as the category default for interior wall applications.

Wood Coatings address the specific performance requirements of timber surfaces in both interior furniture and exterior cladding applications. Penetration resistance, UV stability, and grain enhancement drive specification decisions in this sub-segment. Moreover, the renovation cycle for wood-clad structures creates recurring demand independent of new construction activity, providing manufacturers with a stable replacement volume.

Resin Type Analysis

Acrylic dominates with 46.3% due to superior weatherability and formulation versatility.

In 2025, Acrylic held a dominant market position in the By Resin Type segment of the Decorative Coatings Market, with a 46.3% share. Acrylic resins deliver consistent adhesion, UV resistance, and color retention across both interior and exterior applications. Their compatibility with waterborne formulations positions acrylic as the resin of choice for manufacturers aligning product lines with low-VOC compliance requirements in key regulated markets.

Alkyd resins maintain relevance in applications requiring hard, high-gloss finishes and strong adhesion to ferrous metal surfaces. Although alkyd formulations carry higher VOC profiles than acrylic alternatives, their performance characteristics in trim and enamel applications preserve their specification position in markets where regulation allows. Waterborne alkyd development is an active R&D focus for manufacturers seeking to extend alkyd’s market life.

Technology Analysis

Waterborne dominates with 67.1% due to regulatory compliance and low-VOC performance requirements.

In 2025, Waterborne technology held a dominant market position in the By Technology segment of the Decorative Coatings Market, with a 67.1% share. Waterborne formulations meet VOC emission standards enforced across North America, Europe, and increasingly in the Asia Pacific — removing a regulatory barrier that continues to erode the addressable market for solventborne alternatives. Manufacturers who built waterborne capacity early now hold a structural cost and compliance advantage over late-adopting competitors.

Solventborne technology retains specification positions in applications where waterborne chemistry cannot yet match performance requirements — particularly in industrial protective decorative finishes, marine coatings, and certain wood coating categories requiring deep penetration. However, solventborne formats face an accelerating substitution timeline as waterborne R&D narrows the performance gap. Manufacturers dependent on solventborne product lines face both a regulatory and a competitive threat over the forecast period.

Coating Type Analysis

Interior dominates with 69.4% due to residential repaint cycle frequency and renovation activity.

In 2025, Interior coatings held a dominant market position in the By Coating Type segment of the Decorative Coatings Market, with a 69.4% share. Interior surfaces are repainted more frequently than exterior ones — driven by lifestyle changes, occupancy transitions, and commercial tenant fit-outs. This shorter repaint cycle compresses the replacement timeline and generates recurring demand that insulates interior coating revenues from construction slowdowns.

Exterior coatings address weatherproofing, UV resistance, and facade aesthetics for both residential and commercial structures. Exterior repaints require more product volume per project and involve professional contractor application in most markets, supporting higher average transaction values per job. Additionally, the growing specification of functional exterior coatings with thermal and self-cleaning properties is expanding exterior coating revenue beyond purely aesthetic applications.

Application Analysis

Residential dominates with 69.6% due to high renovation frequency and DIY market participation.

In 2025, Residential held a dominant market position in the By Application segment of the Decorative Coatings Market, with a 69.6% share. Residential users drive both professional repaint demand and direct-to-consumer DIY product sales. The dual channel structure — contractor-applied and self-applied — gives residential the broadest volume base of any application segment, creating stable consumption across economic cycles that commercial and industrial segments cannot replicate.

New Construction within the residential segment captures first-coat specification decisions made early in the project cycle. Developers and builders select decorative coating brands at the project planning stage, creating large bulk orders that reward suppliers with contractor-grade pricing programs and job site logistics capabilities.

Key Market Segments

By Color Type

- White

- Others

By Product Type

- Emulsions

- Wood Coatings

- Varnishes

- Stains

- Enamels

- Others

By Resin Type

- Acrylic

- Alkyd

- Vinyl

- Polyurethane

- Others

By Technology

- Waterborne

- Solventborne

By Coating Type

- Interior

- Exterior

By Application

- Residential

- New Construction

- Remodel and Repaint

- Non-residential

- Commercial

- Industrial

- Infrastructure

Emerging Trends

Matte, Textured, and Nanotechnology-Enhanced Finishes Redefine Specification Standards in Modern Architecture

Modern architects and interior designers specify matte, textured, and metallic finishes at a rate that standard emulsion formats cannot address. This shift compresses the product life cycle for flat-finish commodity coatings and creates specification windows for manufacturers with differentiated effect-coating portfolios targeting premium residential and commercial projects.

Nanotechnology integration is moving decorative coatings from surface aesthetics into performance engineering territory. Nano-enhanced coatings deliver measurably superior durability, scratch resistance, and self-cleaning properties — converting a previously aesthetic purchase into a long-term infrastructure investment. Even the least-effective cool roof coating achieved a surface temperature reduction of 15.8°C (25.1%), demonstrating that performance-led decorative solutions now offer quantifiable value beyond appearance.

The DIY segment adds a direct-to-consumer demand channel that operates independently of professional contractor cycles. Rising online retail penetration enables manufacturers to market specialty matte and effect finishes directly to homeowners — bypassing traditional paint store distribution. Consequently, water-based and powder coating formats with simple application requirements are gaining a consumer audience that previously had no access to professional-grade decorative finishes.

Drivers

Urban Construction Growth and Rising Consumer Preference for Eco-Friendly Finishes Expand Coating Demand Across Multiple Channels

Residential and infrastructure construction activity in emerging economies is increasing the volume of surfaces requiring a first-coat decorative specification. Urban housing projects in Asia Pacific, the Middle East, and Latin America bring first-time coating buyers into the market — buyers who then enter the repaint cycle, generating recurring consumption over the building’s lifetime. This structural demand creation is more durable than cyclical consumer spending patterns.

Eco-friendly and low-VOC formulations are no longer optional for manufacturers targeting regulated markets in North America and Europe. Sherwin-Williams Paint Stores Group sales grew 5.1% in Q3 2025, driven by professional repaint demand, demonstrating that compliant professional-grade products continue to command consistent volume in mature markets.

Renovation and remodeling activity provides a demand floor that does not depend on new construction starts. Changing consumer lifestyles — particularly post-pandemic emphasis on home environments — are shortening repainting intervals among residential owners. Cool roof coatings reduced surface temperatures by 8.7°C to 34.2°C, a 13.2%–53.6% reduction, confirming that functional decorative coatings now deliver energy cost arguments that accelerate specification decisions beyond traditional aesthetic motivations.

Restraints

Raw Material Price Volatility and Environmental Compliance Costs Compress Manufacturer Margins Across the Value Chain

Titanium dioxide, acrylic resins, and petrochemical-derived solvents are the primary raw material inputs for decorative coatings, and all three track commodity price cycles that manufacturers cannot control. When input costs rise faster than pricing power allows, gross margins compress, forcing manufacturers to choose between absorbing costs or risking volume loss through price increases.

PPG Industries implemented price increases of up to 20% in 2026 due to rising input and logistics costs. This scale of price action signals that raw material inflation has reached a threshold where cost pass-through to end customers is unavoidable. For price-sensitive residential buyers and cost-conscious commercial contractors, significant price increases risk accelerating product substitution toward lower-specification or private-label alternatives.

Stringent environmental regulations add compliance costs that fall disproportionately on mid-size manufacturers without the R&D scale to reformulate rapidly. Transitioning from solventborne to waterborne or powder coating formats requires capital investment in production equipment, testing protocols, and regulatory certification processes. Therefore, smaller producers face a cost barrier that either limits their addressable market or forces margin sacrifice to remain competitive on price.

Growth Factors

Smart Coating Properties, Green Building Investment, and E-Commerce Channel Expansion Create New Revenue Streams for Manufacturers

Anti-microbial and self-cleaning decorative coatings are opening specification pathways in healthcare, hospitality, and food processing environments where hygiene requirements previously excluded standard decorative products. Manufacturers who certify anti-microbial performance claims gain access to institutional procurement channels with higher contract values and longer supply agreements than standard residential paint distribution.

Green building certification programs — LEED, BREEAM, and equivalent regional standards — now require documented coating performance on VOC emissions, thermal management, and material sustainability. Sherwin-Williams Paint Stores’ sales increased 3.7% in Q1 2026, with Consumer Brands rising 19.2% year-over-year, indicating that sustainable and compliant product lines are capturing both professional and consumer channel growth simultaneously — a dual-channel recovery that validates investment in green product development.

E-commerce channel development enables decorative coating manufacturers to reach DIY residential buyers directly, bypassing traditional retail intermediaries and improving per-unit margin capture. Automotive customization and decorative finishing applications add a non-construction demand vertical that tracks vehicle ownership trends rather than housing cycles. Consequently, manufacturers expanding into e-commerce and automotive channels reduce their dependence on construction market conditions.

Regional Analysis

North America Dominates the Decorative Coatings Market with a Market Share of 32.5%, Valued at USD 28.6 Billion

North America holds a 32.5% share of the global decorative coatings market, valued at USD 28.6 billion. Mature professional repainting infrastructure, established contractor procurement networks, and early-mover compliance with low-VOC standards give North American manufacturers a structural pricing advantage. These conditions support consistent volume even during housing market slowdowns.

Europe enforces some of the most stringent VOC emission limits globally, effectively mandating waterborne and low-emission product formulations across member states. This regulatory environment rewards manufacturers with compliant product portfolios while eliminating market access for non-compliant producers. Renovation activity in Western European housing stock — much of it aging beyond 30 years — sustains a durable repaint volume base.

Asia Pacific represents the highest absolute growth opportunity in global decorative coatings, driven by urbanization rates exceeding those of any other region and large-scale government-backed housing programs. China, India, and Southeast Asian markets are adding new residential and commercial surface area at a pace that supports first-coat specification volume well beyond repaint cycle demand alone.

Infrastructure megaprojects, government-funded social housing, and commercial real estate development across Gulf Cooperation Council countries are creating sustained first-coat decorative coating demand. Extreme climate conditions in the region also accelerate exterior coating degradation, shortening repaint cycles and generating recurring volume that supplements project-based demand.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

AkzoNobel N.V. positions itself as a sustainability-led coatings manufacturer, investing in waterborne and low-VOC product lines that align with tightening European and North American environmental standards. This compliance-forward strategy reduces future regulatory risk while allowing AkzoNobel to command specification preference in green building projects where certified low-emission coatings are a procurement requirement.

Asian Paints Limited leverages deep distribution penetration across India and Southeast Asian markets, where expanding urban housing demand creates high-volume first-coat opportunities. Its localized manufacturing infrastructure reduces raw material logistics costs — a structural margin advantage over multinational competitors importing finished goods into price-sensitive emerging markets. This scale gives Asian Paints pricing flexibility that sustains volume even during inflationary periods.

Axalta Coating Systems, LLC applies its automotive and industrial coatings expertise to decorative finishing applications, delivering documented performance data that supports premium pricing in commercial and infrastructure specifications. Its technical sales model — targeting specifiers and contractors rather than retail consumers — insulates Axalta from the DIY demand volatility that affects mass-market decorative coating revenues.

BASF SE operates in the decorative coatings value chain primarily through resin and raw material supply, giving it margin exposure at the input stage rather than the finished goods level. This upstream positioning means BASF captures value regardless of which finished coating brand wins specification — a structurally differentiated revenue model that reduces dependence on end-consumer brand preference trends.

Key Players

- AkzoNobel N.V.

- Asian Paints Limited

- Axalta Coating Systems, LLC

- BASF SE

- Bayer AG

- Jotun A/S

- Kansai Paint Co., Ltd.

- KCC Corporation

- Nippon Paint Holdings Co., Ltd.

- PPG Industries, Inc.

- RPM International Inc.

- The Sherwin-Williams Company

Recent Developments

- In 2025, AkzoNobel N.V. announced an all-stock merger of equals with Axalta, creating a coatings company with about $17B revenue, $25B enterprise value, and expected $600M cost synergies. The combined portfolio includes Decorative Paints, plus powder, refinish, mobility, marine, protective, and industrial coatings.

- In 2025, Asian Paints Ltd. India’s decorative business reported 7.9% volume growth and 2.8% value growth; 9M FY26 decorative volume growth was 7.5% and value growth 2.4%. Standalone Q3 FY26 net sales grew 2.9% to ₹7,602 crore, and gross margin rose to 44.9%.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 88.1 Billion |

| Forecast Revenue (2035) | USD 123.2 Billion |

| CAGR (2026-2035) | 3.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Color Type (White, Others), By Product Type (Emulsions, Wood Coatings, Varnishes, Stains, Enamels, Others), By Resin Type (Acrylic, Alkyd, Vinyl, Polyurethane, Others), By Technology (Waterborne, Solventborne), By Coating Type (Interior, Exterior), By Application (Residential: New Construction, Remodel and Repaint; Non-residential: Commercial, Industrial, Infrastructure) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | AkzoNobel N.V., Asian Paints Limited, Axalta Coating Systems LLC, BASF SE, Bayer AG, Jotun A/S, Kansai Paint Co. Ltd., KCC Corporation, Nippon Paint Holdings Co. Ltd., PPG Industries Inc., RPM International Inc., The Sherwin-Williams Company |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |