Quick Navigation

Report Overview

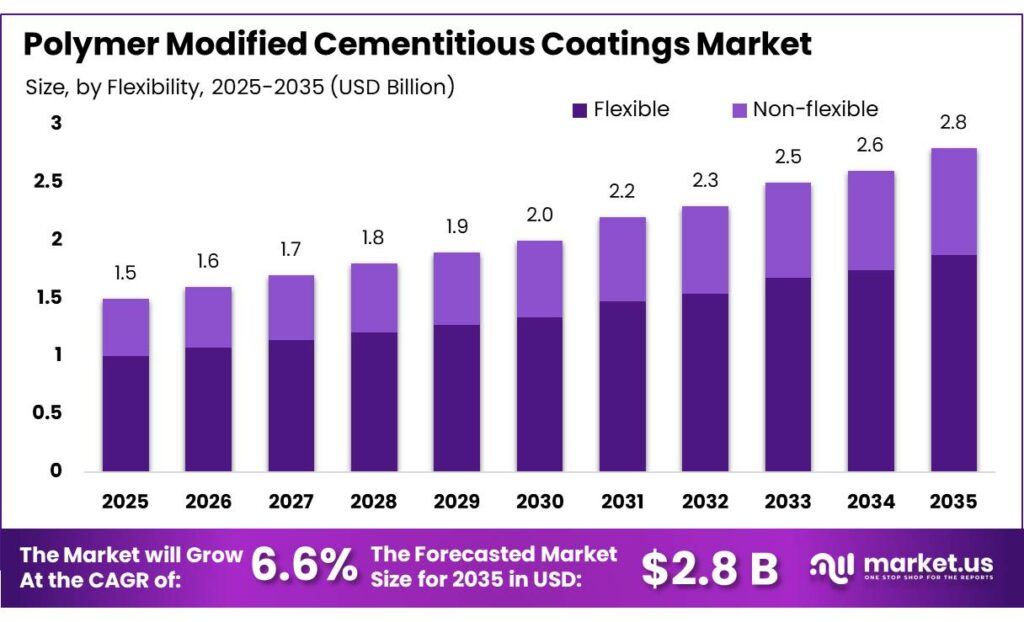

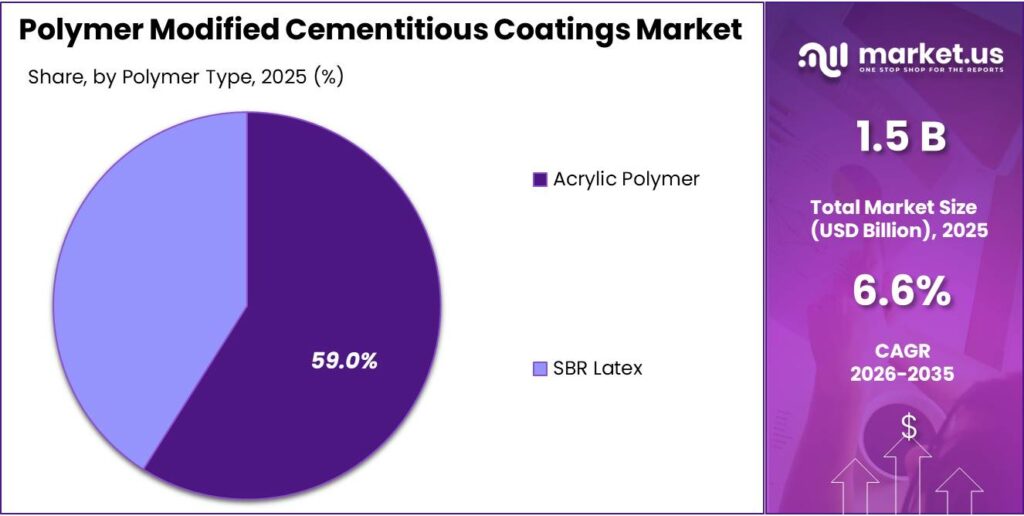

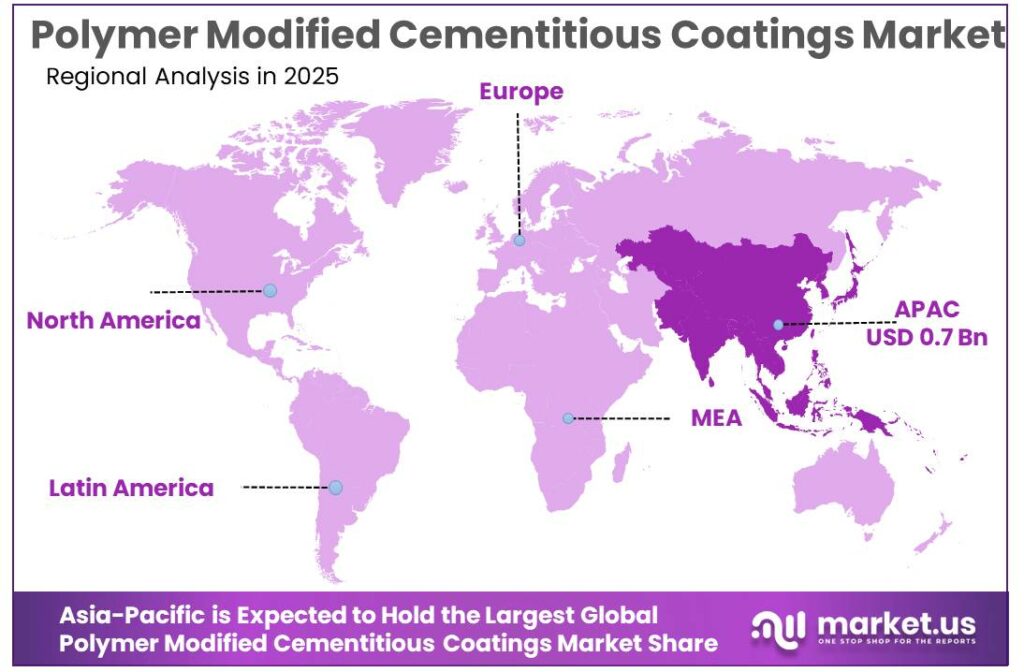

The Global Polymer Modified Cementitious Coatings Market size is expected to be worth around USD 2.8 Billion by 2035, from USD 1.5 Billion in 2025, growing at a CAGR of 6.6% during the forecast period from 2026 to 2035. In 2025, Asia-Pacific held a dominant market position, capturing more than a 48.8% share, holding USD 0.7 Billion revenue.

Polymer modified cementitious coatings are positioned as high-performance protective systems for concrete and masonry where waterproofing, crack-bridging, adhesion, and durability are critical. In practical industrial use, they are increasingly specified for basements, water-retaining structures, podium decks, wet rooms, processing zones, and refurbishment projects because they combine cement-based compatibility with polymer-enhanced flexibility and resistance to moisture ingress.

Their relevance is reinforced by the scale of retrofit demand in developed markets: in the EU, more than 220 million building units represent 85% of the building stock, 85–95% of today’s buildings are expected to remain in use in 2050, and buildings account for about 40% of total EU energy consumption and 36% of energy-related greenhouse-gas emissions.

The current industrial scenario is being shaped less by speculative demand and more by asset preservation, compliance, and lifecycle economics. Public policy is a major support pillar. Under the EU Recovery and Resilience Facility, 20 Member States included residential energy-efficiency measures covering almost 420 million m² or nearly 4.7 million dwellings, which creates a broad retrofit pipeline where substrate protection and moisture management products become important enabling materials.

At the same time, the food-processing environment remains a relevant downstream demand center: Eurostat reports that food and beverage processing enterprises generated €266 billion in value added, while EU food manufacturing sold production rose by €17 billion in 2024 versus 2023.

Demand is also being reinforced by the condition of global water assets and sanitary processing environments. UN-Water reported in 2024 that, among reporting countries, only 38% of industrial wastewater was treated and only 27% was safely treated, while the UN Statistics Division reported that 56% of global domestic wastewater, equal to 332 billion m³, was safely treated in 2024.

In downstream hygienic manufacturing, FoodDrinkEurope states that the EU food and drink industry employs 4.7 million people, generates about €1.2 trillion in turnover and around €250 billion in value added, while USDA reports that the U.S. agriculture and food industry contributes $1.1 trillion to GDP and nearly 11% of total U.S. employment. Such facilities are major users of easy-to-clean, moisture-tolerant protective building materials.

From a competitive and technology perspective, the sector is benefiting from sustainability-driven raw material innovation among large coating and specialty-material suppliers. Akzo Nobel N.V. reported €10,158 million in revenue for 2025, underscoring the scale and balance-sheet strength available for protective and construction-adjacent coatings innovation. Arkema S.A. reported around €9.1 billion in 2025 sales and operated in about 55 countries with 20,700 employees, indicating strong global reach in coating materials and additives.

Key Takeaways

- Polymer Modified Cementitious Coatings Market size is expected to be worth around USD 2.8 Billion by 2035, from USD 1.5 Billion in 2025, growing at a CAGR of 6.6%.

- Flexible held a dominant market position, capturing more than a 67.2% share.

- Two-component held a dominant market position, capturing more than a 62.1% share.

- Acrylic Polymer held a dominant market position, capturing more than a 59.4% share.

- Non-residential Buildings held a dominant market position, capturing more than a 37.9% share.

- Asia-Pacific stands out as the dominating region in the Polymer Modified Cementitious Coatings market, accounting for around 48.8% share and nearly USD 0.7 billion.

By Flexibility Analysis

Flexible coatings dominate with 67.2% share driven by demand for crack-resistant and durable solutions

In 2025, Flexible held a dominant market position, capturing more than a 67.2% share. This strong lead was mainly supported by the rising need for coatings that can handle structural movement and prevent cracking in buildings and infrastructure. Flexible polymer modified cementitious coatings are widely used in areas exposed to temperature changes, moisture, and minor vibrations, making them a preferred choice in both residential and commercial construction. Their ability to bridge hairline cracks and provide long-lasting waterproofing has made them especially popular in regions with harsh weather conditions.

By Composition Analysis

Two-component coatings lead with 62.1% share as users prefer stronger and more reliable performance

In 2025, Two-component held a dominant market position, capturing more than a 62.1% share. This was mainly due to its better strength, higher bonding ability, and improved resistance to water and chemicals compared to single-component systems. These coatings are made by mixing a liquid polymer with a cement-based powder, which gives them enhanced flexibility and durability. Because of these benefits, they are widely used in critical applications like basements, water tanks, roofs, and wet areas where long-term protection is needed.

By Polymer Type Analysis

Acrylic polymer leads with 59.4% share as it offers easy use and reliable protection

In 2025, Acrylic Polymer held a dominant market position, capturing more than a 59.4% share. This was largely because acrylic-based coatings are easy to apply, cost-effective, and provide good flexibility along with strong adhesion. They are widely used in waterproofing applications such as terraces, bathrooms, and external walls where protection against moisture is important. Their ability to form a smooth and durable layer makes them a practical choice for both small and large construction projects. Many users prefer acrylic polymers as they balance performance and affordability without making the process complicated.

By Application Analysis

Non-residential buildings lead with 37.9% share as large projects demand durable waterproofing

In 2025, Non-residential Buildings held a dominant market position, capturing more than a 37.9% share. This growth was mainly driven by the increasing number of commercial spaces, offices, hospitals, malls, and industrial facilities where strong and long-lasting coatings are essential. These structures often face heavy usage, moisture exposure, and strict safety requirements, making polymer modified cementitious coatings a preferred option. Their ability to provide reliable waterproofing and protect surfaces from wear and damage has made them widely used in such large-scale projects.

Key Market Segments

By Flexibility

- Flexible

- Non-flexible

By Composition

- One-component

- Two-component

By Polymer Type

- Acrylic Polymer

- SBR Latex

By Application

- Non-residential Buildings

- Residential Buildings

- Public Infrastructure

Emerging Trends

Shift toward antimicrobial and hygiene-focused coatings in food facilities

One clear latest trend in polymer modified cementitious coatings is the growing focus on antimicrobial and hygiene-friendly surfaces, especially in food processing areas. Food industries are no longer satisfied with just strong or waterproof coatings—they now want surfaces that actively support cleanliness and reduce contamination risks.

This shift is strongly connected to real-world food safety concerns. According to the Centers for Disease Control and Prevention, about 48 million people fall sick every year due to foodborne illnesses in the U.S. alone . These numbers push food companies to rethink even basic infrastructure like floors and walls. Coatings are now expected to resist bacteria, handle heavy cleaning chemicals, and prevent moisture build-up where microbes can grow.

Rise of sustainable and long-life coatings driven by government policies

Another important trend is the move toward sustainable, long-lasting coating solutions. Governments and industries are now focusing on reducing waste, extending building life, and lowering maintenance cycles. Polymer modified cementitious coatings are gaining attention because they help structures last longer and reduce the need for frequent repairs.

Globally, infrastructure investments are increasing, and governments are linking them with sustainability goals. For example, several countries are pushing for durable materials that reduce lifecycle costs and environmental impact. Studies show that these coatings improve adhesion, waterproofing, and crack resistance, which helps extend the life of concrete structures . That directly supports sustainability goals by reducing material waste over time.

Drivers

Rising need for waterproof and long-lasting buildings is pushing coating demand

One of the biggest reasons behind the growth of polymer modified cementitious coatings is the increasing need for strong waterproofing in buildings and infrastructure. Water damage is still one of the most common problems in construction, and builders are now focusing more on long-term protection instead of short-term fixes. In 2025, the global waterproofing chemicals market alone was valued at around USD 8.07 billion, showing how important moisture protection has become in modern construction.

This shift is not just about new buildings but also about repairing older ones. Governments across many countries are investing in infrastructure upgrades, especially where water leakage and cracks are common. Polymer modified cementitious coatings are being widely used because they create a strong barrier that reduces water entry and protects concrete from damage over time.

Government focus on infrastructure durability and safety standards is driving adoption

Another major driver is the growing push from governments and regulatory bodies to improve the durability and safety of buildings and public infrastructure. Many countries are now enforcing stricter construction standards to reduce long-term repair costs and improve building life. For example, around 68% of waterproofing demand today comes directly from infrastructure development projects such as bridges, tunnels, and public utilities.

Governments are also promoting sustainable construction practices, encouraging the use of materials that extend the life of structures and reduce maintenance needs. These coatings help meet those goals by improving durability and reducing water-related damage. As infrastructure spending continues and regulations become tighter, the use of such advanced coating systems is expected to stay strong in both developed and developing regions.

Restraints

High cost of compliance and maintenance slows down adoption

One major restraining factor for polymer modified cementitious coatings is the high cost of installation, maintenance, and compliance in food facilities. While these coatings are strong and long-lasting, they are not cheap. Food processing companies already spend heavily on safety, cleaning systems, audits, and compliance upgrades. When a facility considers upgrading floors or walls, cost becomes a serious decision point.

The numbers show how tight things already are. According to the USDA Economic Research Service, foodborne illness costs the U.S. around $74.7 billion annually, including medical care, lost productivity, and deaths. Because of this burden, companies invest heavily in prevention—but that also means budgets are stretched. For example, serious illness cases account for 60% of total costs, even though they are only about 20% of cases.

Strict regulations increase pressure but also create hesitation

Government rules are meant to improve food safety, but they can also slow down adoption decisions. Regulations from the U.S. Food and Drug Administration under FSMA push companies to maintain hygienic, traceable, and contamination-free environments. At the same time, they require detailed planning, audits, and validation before any structural changes are made.

The pressure is real. The Centers for Disease Control and Prevention estimates that around 9.9 million illnesses, 53,300 hospitalizations, and 931 deaths occur annually from major foodborne pathogens alone. Over time, more than 9,000 outbreaks were reported between 2011 and 2022 across the U.S. These numbers push regulators to tighten rules.

Opportunity

Expanding food processing industry is opening new demand for durable coatings

One strong growth opportunity for polymer modified cementitious coatings comes from the steady expansion of food processing and manufacturing facilities. As food demand grows, companies are building new plants and upgrading older ones. These spaces need floors and walls that can handle water, chemicals, and heavy equipment without breaking down. That is exactly where these coatings fit naturally.

The numbers show how big this opportunity really is. According to the USDA Economic Research Service, total food spending in the U.S. crossed $2.58 trillion in 2024, showing how large and active the food system has become. At the same time, food and agriculture industries together generate more than $10.4 trillion in economic activity and support nearly 49 million jobs across the country.

Rising hygiene standards and modern infrastructure upgrades create long-term demand

According to the Centers for Disease Control and Prevention, millions of foodborne illness cases still occur each year, which keeps pressure on industries to improve hygiene standards. At the same time, the food manufacturing sector employs around 1.7 million people in the U.S. alone, showing how large and active these facilities are

Government initiatives like the Food Safety Modernization Act (FSMA) push companies to focus on prevention instead of reaction. This means better facility design, improved surfaces, and materials that reduce contamination risks. Older factories are being upgraded, and new ones are being designed with hygiene in mind from the start.

Regional Insights

Asia-Pacific dominates the Polymer Modified Cementitious Coatings Market with strong infrastructure growth

Asia-Pacific stands out as the dominating region in the Polymer Modified Cementitious Coatings market, accounting for around 48.8% share and nearly USD 0.7 billion in value. This leadership position is closely tied to the region’s fast-paced urbanization, expanding construction sector, and strong government-backed infrastructure investments. Countries such as China, India, Japan, and Southeast Asian nations are continuously investing in residential housing, transportation networks, and industrial facilities, all of which require durable waterproofing and protective coating systems.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Akzo Nobel N.V. is a global leader in paints and performance coatings, playing a strong role in cementitious coating technologies. The company reported €10.7 billion revenue in 2023, with €488 million net income and operates in 150+ countries with around 35,200 employees. Its wide product portfolio, including protective coatings and waterproofing systems, supports infrastructure and food-grade applications.

Arkema S.A. is a major specialty chemicals company with a strong presence in coating solutions and advanced materials. The company generated around €9.5 billion revenue in 2024 and operates in 55 countries with approximately 21,150 employees. Arkema’s coating solutions segment contributes nearly 24.5% of its total business, highlighting its focus on performance coatings. Its expertise in polymers, adhesives, and specialty resins supports the development of polymer modified cementitious coatings used in construction and industrial protection applications globally.

Berger Paints India Limited is one of the leading paint and coating companies in India with strong growth in construction chemicals. The company recorded around ₹11,600 crore revenue in FY2025 and employs over 3,000–3,600 people. It operates 16 manufacturing units in India and has a distribution network of over 25,000 dealers. Berger’s expansion into waterproofing and construction solutions supports demand for cementitious coatings, especially in residential and infrastructure projects across emerging markets.

Top Key Players Outlook

- Akzo Nobel N.V.

- Arkema S.A.

- BASF SE

- Berger Paints India Limited

- Evercrete

- Fosroc, Inc

- H.B. Fuller

- MAPEI S.p.A

- Pidilite Industries Limited

- LO Saint-Gobain Weber

- Sika AG

Recent Industry Developments

Evercrete’s sealing technologies demonstrate measurable improvements, such as up to 97% reduction in water absorption, 30% increase in compressive strength, and 400–600% higher resistance to chemical and chloride penetration, highlighting its durability advantage in harsh environments.

BASF also invested heavily in innovation, spending nearly €2.0 billion on R&D in 2025, which supports advanced materials used in coatings and construction applications.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.5 Bn |

| Forecast Revenue (2035) | USD 2.8 Bn |

| CAGR (2026-2035) | 6.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Flexibility (Flexible, Non-flexible), By Composition (One-component, Two-component), By Polymer Type (Acrylic Polymer, SBR Latex), By Application (Non-residential Buildings, Residential Buildings, Public Infrastructure) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Akzo Nobel N.V., Arkema S.A., BASF SE, Berger Paints India Limited, Evercrete, Fosroc, Inc, H.B. Fuller, MAPEI S.p.A, Pidilite Industries Limited, LO Saint-Gobain Weber, Sika AG |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |